Trend Balance Point (TBP)

April 10, 2017, 9:36 AM

Indicators

8 Comments

{kind=link}

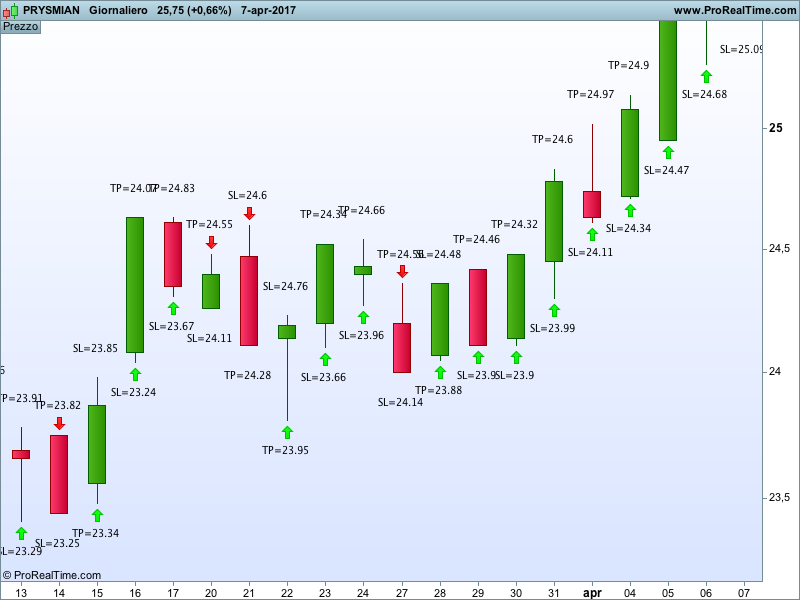

The Trend Balance Point is a system created by J. Welles Wilder and published in his book ‘New Concepts In Technical Trading Systems’. The system uses momentums to define whether to enter the market long or short and provide a Stop Loss and a Target Price for each entry. Positions are opened on THE CLOSE of the current day and closed as soon as the Target Price or the Stop Loss is hit.

According to Mr. Wilder the system works well in ranging markets and when ADX is below 20.

I personally never used this system and I haven’t done any backtesting either because PRT doesn’t allow to buy on close.

Blue skies!

periodo=2

i=1

f=i+periodo

MFieri=dclose(i)-dclose(f)

MFaltroieri=dclose(i+1)-dclose(f+1)

massimo=MAX(MFieri,MFaltroieri)

minimo=MIN(MFieri,MFaltroieri)

//Calcolo TBP

TBPiflong=dclose(periodo)+minimo

TBPifshort=dclose(periodo)+massimo

//Calcolo dello Stop loss

atr1=dhigh(1)-dlow(1)

atr2=dhigh(1)-dclose(2)

atr3=dlow(1)-dclose(2)

a=MAX(atr1,atr2)

b=max(a,atr3)

SLiflong=((dclose(1)+DLow(1)+dhigh(1))/3)-b

SLifshort=((dclose(1)+DLow(1)+dhigh(1))/3)+b

////Calcolo del Target Price

TPiflong=(2*((dclose(1)+DLow(1)+dhigh(1))/3))-dlow(1)

TPifshort=(2*((dclose(1)+DLow(1)+dhigh(1))/3))-dhigh(1)

TPL=round(100*TPiflong)/100

TPS=round(100*TPifshort)/100

SLL=round(100*SLiflong)/100

SLS=round(100*SLifshort)/100

once long=0

once short=0

if (close crosses over TBPifshort) then

long=1

short=0

endif

if (close crosses under TBPiflong) then

long=0

short=1

endif

if short=1 then

if close crosses over TBPiflong then

long=1

short=0

endif

endif

if long=1 then

DRAWARROWUP(barindex, low*0.999) coloured (0,255,0)

endif

if long[1]=1 then

DRAWTEXT("TP=#TPL#", barindex, high*1.005)

DRAWTEXT("SL=#SLL#", barindex, low*0.995)

endif

if short=1 then

DRAWARROWDOWN(barindex, high*1.001) coloured (255,0,0)

endif

if short[1]=1 then

DRAWTEXT("SL=#SLS#", barindex, high*1.005)

DRAWTEXT("TP=#TPS#", barindex, low*0.995)

endif

return

Download

Filename:

Trend-Balance-Point.itf

Downloads:

356

Master

Code artist, my biography is a blank page waiting to be scripted. Imagine a bio so awesome it hasn't been coded yet.

Author’s Profile

Loading...