Recursive Median Oscillator by John Ehlers

March 8, 2018, 11:40 AM

Indicators

6 Comments

{kind=link}

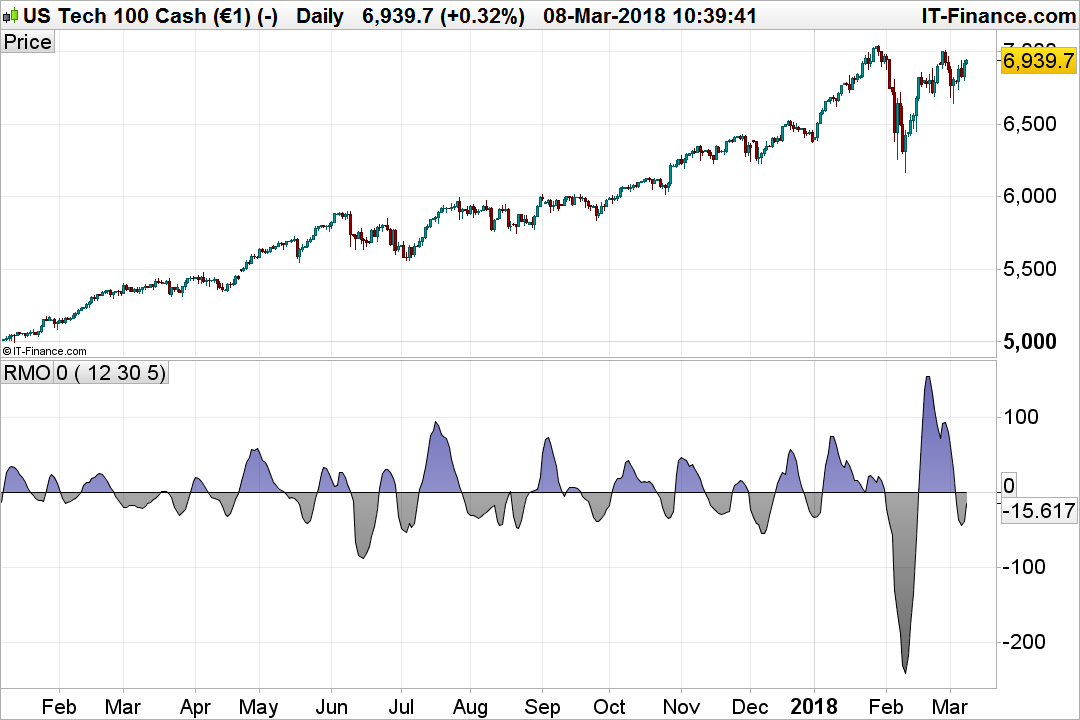

This is the the recursive median Oscillator featured by John Ehlers in the march 2017 issue of Trader’s Tips.

In “Recursive Median Filters” in this issue, author John Ehlers presents an approach for filtering out extreme price and volume data that can throw off typical averaging calculations. Ehlers goes on to present a novel oscillator using this technique, comparing its response to the well-known RSI. He notes that by being able to smooth the data with the least amount of lag, the recursive median oscillator may give the trader a better view of the bigger picture.

LPPeriod=12

HPPeriod=30

length=5

once Median=0

if barindex>length then

// Set EMA constant from LPPeriod input

Alpha1 = ( Cos( 360 / LPPeriod )+ Sin( 360 / LPPeriod ) - 1 )/ Cos( 360 / LPPeriod )

// get the median of the last length (default=5) closes

FOR X = 0 TO length-1

M = close[X] //this example takes the median of the last 5 closes

SmallPart = 0

LargePart = 0

FOR Y = 0 TO length-1

IF close[Y] < M THEN

SmallPart = SmallPart + 1

ELSIF close[Y] > M THEN

LargePart = LargePart + 1

ENDIF

IF LargePart = SmallPart AND Y = length-1 THEN

Median = M

BREAK

ENDIF

NEXT

NEXT

// Recursive Median (EMA of a 5

// bar Median filter)

RM = Alpha1 * Median + ( 1 - Alpha1 ) * RM[1]

// Highpass filter cyclic components

// whose periods are shorter than

// HPPeriod to make an oscillator

Alpha2 = ( Cos( .707 * 360 / HPPeriod ) + Sin( .707 * 360 / HPPeriod ) - 1 ) / Cos( .707 * 360 / HPPeriod )

RMO = ( 1 - Alpha2 / 2 ) * ( 1 - Alpha2 / 2 ) * ( RM - 2 * RM[1] + RM[2] ) + 2 * ( 1 - Alpha2 ) * RMO[1] - ( 1 - Alpha2 ) * ( 1 - Alpha2 ) * RMO[2]

endif

return RMO as "RMO", 0 as "0"

Download

Filename:

Ehlers-Recursive-Median-Oscil..itf

Downloads:

172

Download

{kind=link}

Filename:

bildschirmfoto-um-1520503045c8p4l.png

Downloads:

44

Master

As an architect of digital worlds, my own description remains a mystery. Think of me as an undeclared variable, existing somewhere in the code.

Author’s Profile

Loading...