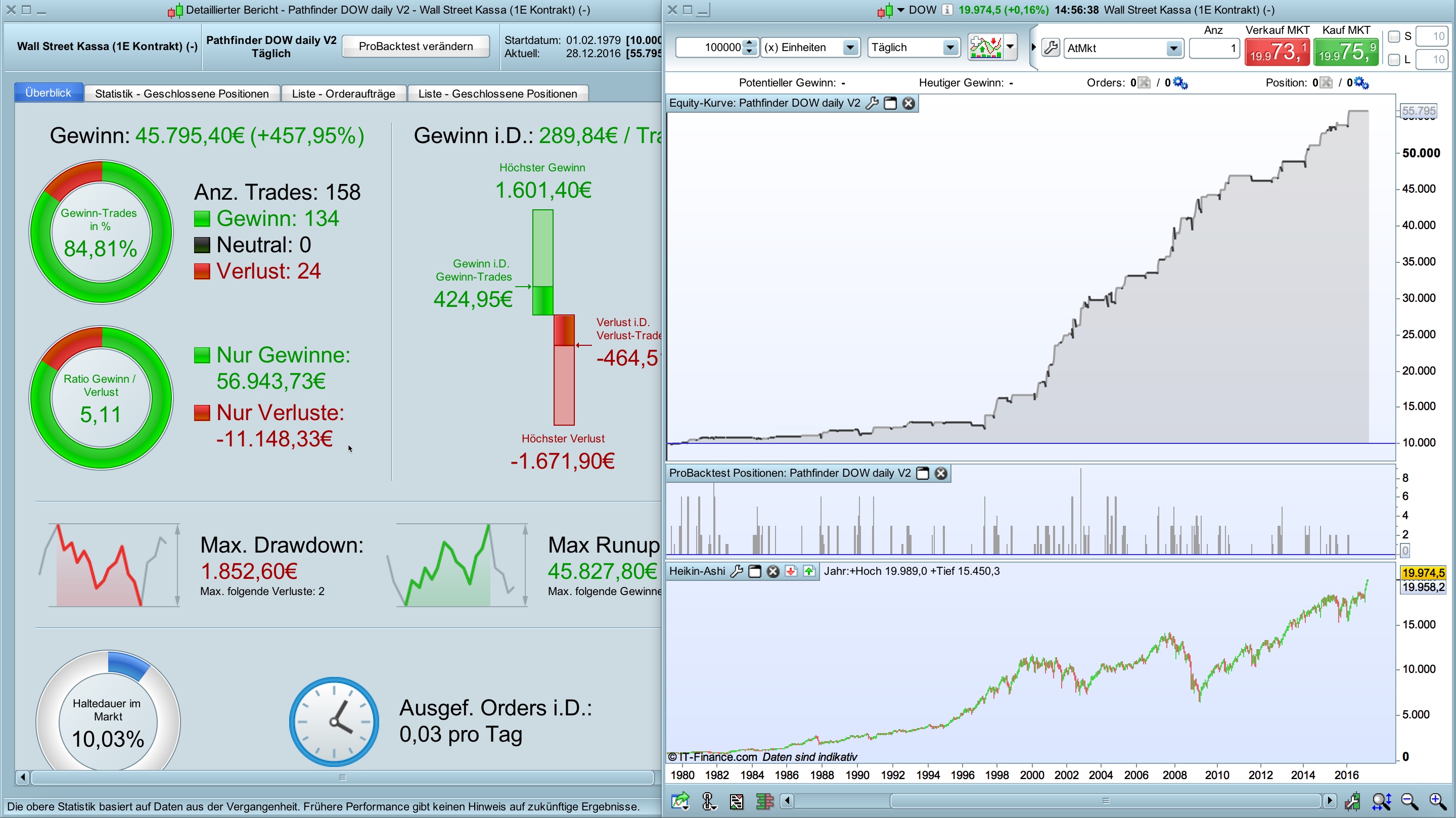

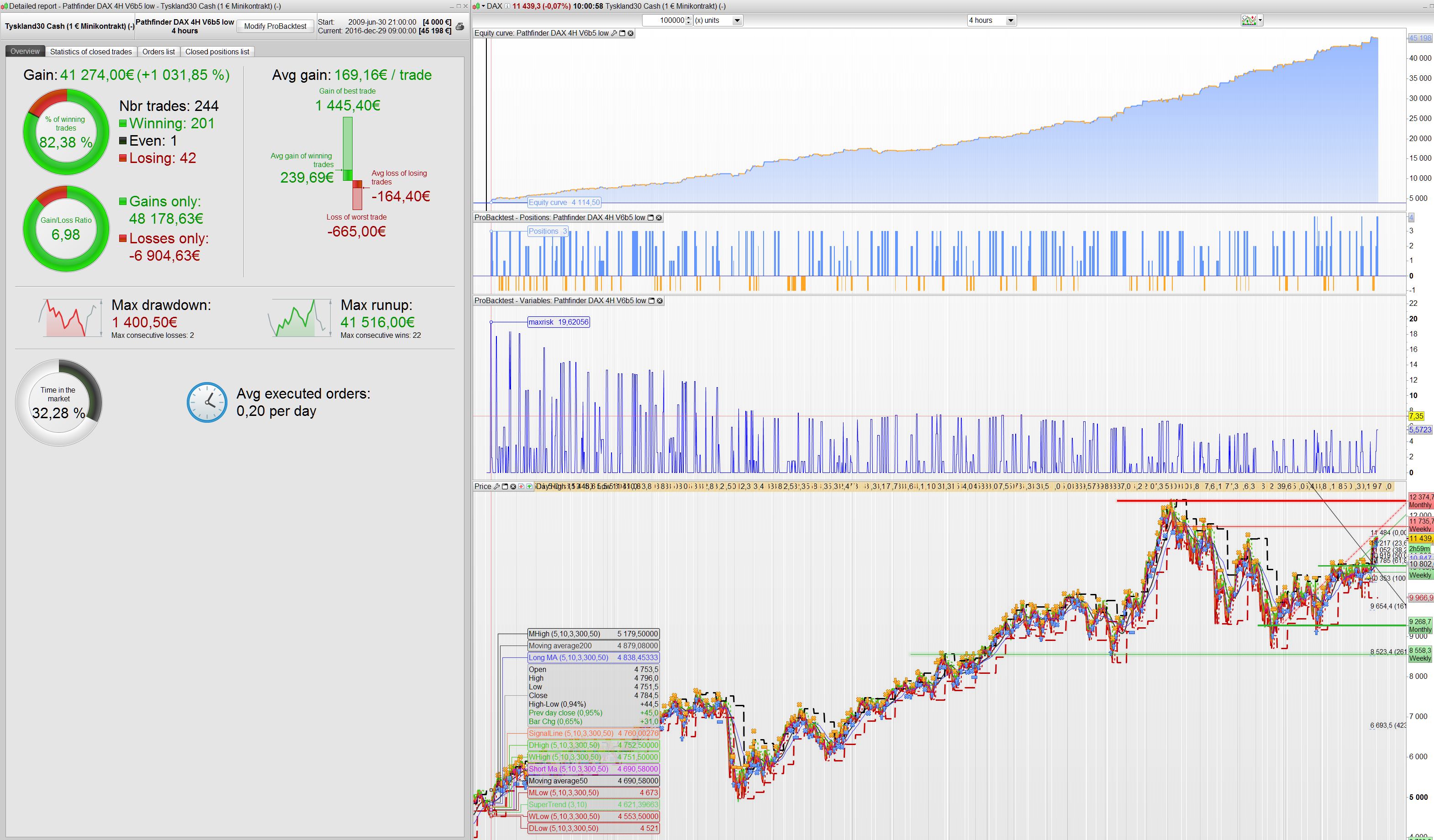

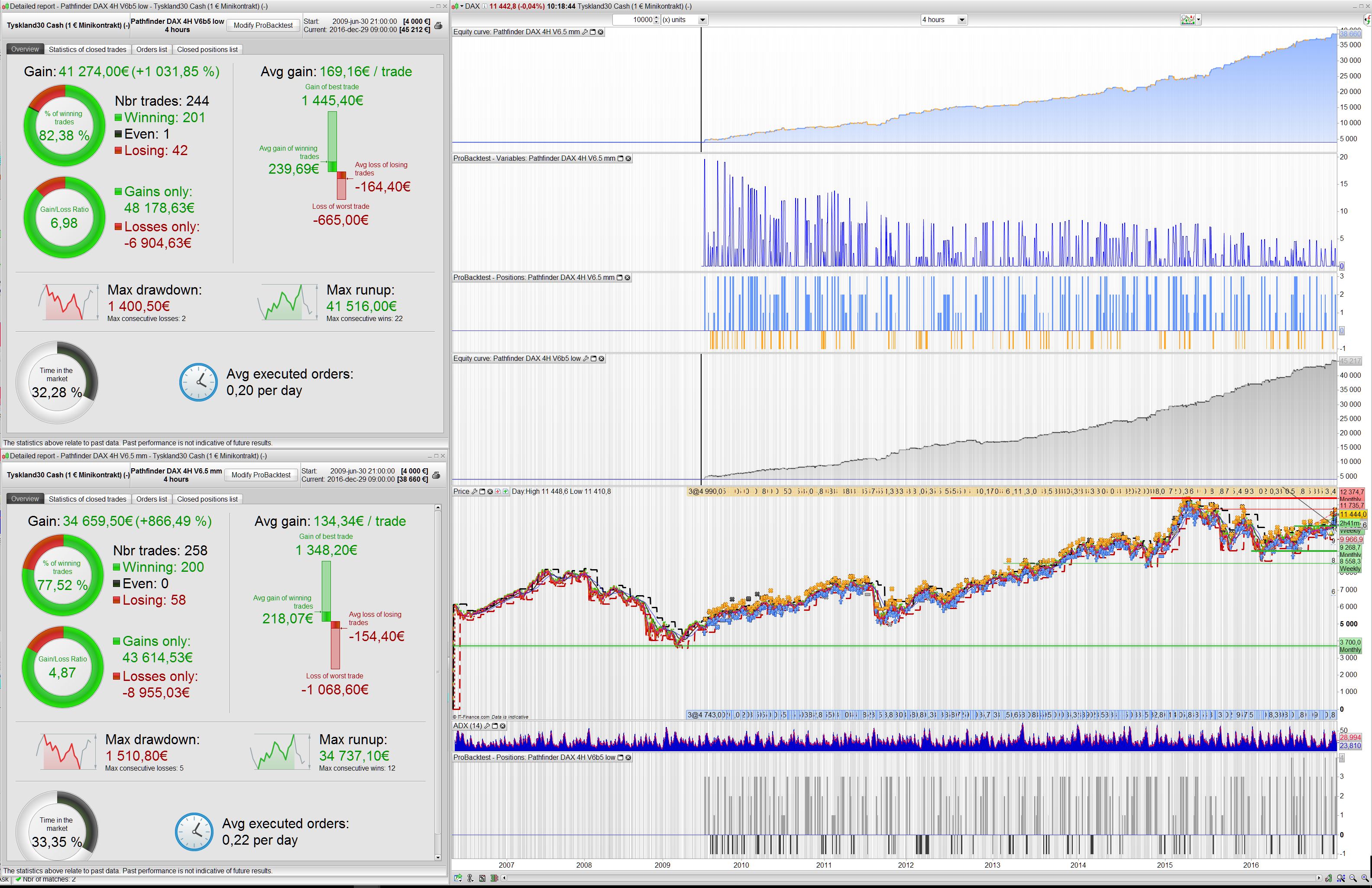

Hi Reiner. I’m still trying to make a more conservative version of DAX 4H v6. I wrote about the risk before, also someone asked about a ver. for a small account. I saw you suggested a max 3 positionsize ver. I tested many variation of v6 code but since the positionsize is not linear I can’t find a solution that would go all the way including a money management code. I discovered that simplify the original code to only maxpositionsize=3 it also cut more on the gain side. So perhaps a new optimisation was needed? I multiplied the DD with 2 and added 1K for margin if the 3 positions. So this should be for a 4k account. Downside is that the DD is still more or less same as the V6 but the gain is only half. On the good side, it only risk a third of the orginal V6.- it has max 2 consecutive loss and 22 wins since July 2009

I tried to do the optimisation, and this was what I came up with. I’d like you comments if you think it’s optimized correct or not since this is my first optimisation try for you code 🙂

I have added a comparison screenshoot of the orginal V6 with max 3 positionsize and the new optimized V6b5

cheers Kasper

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 6.5 MM Elsborgtrading Live ver

// Instrument: DAX mini 4H, 9-21 CET, 2 points spread, account size 10.000 Euro, from August 2010

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 90000

ONCE endTime = 210000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 3

// define filter parameter

ONCE periodLongMA = 300

ONCE periodShortMA = 50

// define position and money management parameter

ONCE positionSize = 1

Capital = 4000

Risk = 5 // in %

equity = Capital + StrategyProfit

maxRisk = round(equity * Risk / 100)

ONCE stopLossLong = 5.5 // in %

ONCE stopLossShort = 3.25 // in %

ONCE takeProfitLong = 3.25//x1//3.25 // in %

ONCE takeProfitShort = 3.5//x2//3.25 // in %

reinvest =1

if reinvest then

positionSize=max(round((equity+Capital)/(capital*10)),1)

maxPositionSizeLong = MAX(positionSize+2, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

maxPositionSizeShort = MAX(positionSize+2, abs(round(maxRisk / (close * stopLossShort / 100) / PointValue) * pipsize))

else

positionSize=1

maxPositionSizeLong = MAX(15, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

maxPositionSizeShort = MAX(15, abs(round(maxRisk / (close * stopLossShort / 100) / PointValue) * pipsize))

Endif

ONCE trailingStartLong = 2 // in %

ONCE trailingStartShort = 0.75 // in %

ONCE trailingStepLong = 0.2 // in %

ONCE trailingStepShort = 0.4 // in %

ONCE maxCandlesLongWithProfit = 17//x1//16 // take long profit latest after 16 candles

ONCE maxCandlesShortWithProfit = 13//x2//15 // take short profit latest after 15 candles

ONCE maxCandlesLongWithoutProfit = 26//x1//30 // limit long loss latest after 30 candles

ONCE maxCandlesShortWithoutProfit = 25//x2//12 // limit short loss latest after 12 candles

// define saisonal position multiplier for each month 1-15 / 16-31 (>0 - long / <0 - short / 0 no trade)

ONCE January1 = 3//x1//3

ONCE January2 = 0//x2//0

ONCE February1 = 1//x1//3

ONCE February2 = 2//x2//3

ONCE March1 = 3//x1//3

ONCE March2 = 3//x2//2

ONCE April1 = 0//x1//1

ONCE April2 = 3//x2//3

ONCE May1 = 1//x1//1

ONCE May2 = 3//x2//1

ONCE June1 = 0//x1//2

ONCE June2 = 2//x2//2

ONCE July1 = 1//x1//3

ONCE July2 = 3//x2//1

ONCE August1 = 2//x1//1

ONCE August2 = 1//x2//1

ONCE September1 = 3//x1//3

ONCE September2 = 0//x2//0

ONCE October1 = 3//x1//3

ONCE October2 = 3//x2//2

ONCE November1 = 2//x1//1

ONCE November2 = 3//x2//3

ONCE December1 = 3//x1//3

ONCE December2 = 2//x2//2

// calculate daily high/low (include sunday values if available)

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month[1] <> Month[2] then

//If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// save position before trading window is open

If Time < startTime then

startPositionLong = COUNTOFLONGSHARES

startPositionShort = COUNTOFSHORTSHARES

EndIF

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// set saisonal multiplier

currentDayOfTheMonth = Date - ((CurrentYear * 10000) + CurrentMonth * 100)

midOfMonth = 15

IF CurrentMonth = 1 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = January1

ELSE

saisonalPatternMultiplier = January2

ENDIF

ELSIF CurrentMonth = 2 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = February1

ELSE

saisonalPatternMultiplier = February2

ENDIF

ELSIF CurrentMonth = 3 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = March1

ELSE

saisonalPatternMultiplier = March2

ENDIF

ELSIF CurrentMonth = 4 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = April1

ELSE

saisonalPatternMultiplier = April2

ENDIF

ELSIF CurrentMonth = 5 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = May1

ELSE

saisonalPatternMultiplier = May2

ENDIF

ELSIF CurrentMonth = 6 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = June1

ELSE

saisonalPatternMultiplier = June2

ENDIF

ELSIF CurrentMonth = 7 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = July1

ELSE

saisonalPatternMultiplier = July2

ENDIF

ELSIF CurrentMonth = 8 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = August1

ELSE

saisonalPatternMultiplier = August2

ENDIF

ELSIF CurrentMonth = 9 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = September1

ELSE

saisonalPatternMultiplier = September2

ENDIF

ELSIF CurrentMonth = 10 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = October1

ELSE

saisonalPatternMultiplier = October2

ENDIF

ELSIF CurrentMonth = 11 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = November1

ELSE

saisonalPatternMultiplier = November2

ENDIF

ELSIF CurrentMonth = 12 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = December1

ELSE

saisonalPatternMultiplier = December2

ENDIF

ENDIF

// define trading filters

// 1. use fast and slow averages as filter because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

// 2. check if position already reduced in trading window as additonal filter criteria

alreadyReducedLongPosition = COUNTOFLONGSHARES < startPositionLong

alreadyReducedShortPosition = COUNTOFSHORTSHARES < startPositionShort

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER dailyLow

// long entry with order cumulation

IF ( (l1 OR l4 OR l2 OR (l3 AND f2)) AND NOT alreadyReducedLongPosition) THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier > 0 THEN

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry without order cumulation

IF NOT SHORTONMARKET AND ( (s1 AND f3) OR (s2 AND f1) ) AND NOT alreadyReducedShortPosition THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier < 0 THEN

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

numberCandles = (BarIndex - TradeIndex)

m1 = posProfit > 0 AND numberCandles >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND numberCandles >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND numberCandles >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND numberCandles >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

// trailing stop function (convert % to pips)

trailingStartLongInPoints = tradeprice(1) * trailingStartLong / 100

trailingStartShortInPoints = tradeprice(1) * trailingStartShort / 100

trailingStepLongInPoints = tradeprice(1) * trailingStepLong / 100

trailingStepShortInPoints = tradeprice(1) * trailingStepShort / 100

//ONCE Breakeven=0

// reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

//breakeven=0

ENDIF

// manage long positions

IF LONGONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND close - tradeprice(1) >= trailingStartLongInPoints * pipsize THEN

newSL = tradeprice(1) + trailingStepLongInPoints * pipsize

stopLoss = stopLossLong * 0.1

takeProfit = takeProfitLong * 2

//breakeven=1

ENDIF

// next moves

IF newSL > 0 AND close - newSL >= trailingStepLongInPoints * pipsize THEN

newSL = newSL + trailingStepLongInPoints * pipsize

//breakeven=1

ENDIF

ENDIF

// manage short positions

IF SHORTONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND tradeprice(1) - close >= trailingStartShortInPoints * pipsize THEN

newSL = tradeprice(1) - trailingStepShortInPoints * pipsize

//breakeven=1

ENDIF

// next moves

IF newSL > 0 AND newSL - close >= trailingStepShortInPoints * pipsize THEN

newSL = newSL - trailingStepShortInPoints * pipsize

//breakeven=1

ENDIF

ENDIF

// stop order to exit the positions

IF newSL > 0 THEN

IF LONGONMARKET THEN

SELL AT newSL STOP

ENDIF

IF SHORTONMARKET THEN

EXITSHORT AT newSL STOP

ENDIF

ENDIF

// superordinate stop and take profit

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

//dif=(newsl1-tradeprice)

//graph ((dif*COUNTOFPOSITION*pipsize*pointvalue)/(equity))*100 COLOURED(0,0,255) AS "MAXRISKNEWSL"//blue

//graph (((tradeprice-(tradeprice-(tradeprice*(stoploss/100))))*positionsize*pipsize*pointvalue)/(equity))*100 COLOURED(0,0,0) AS "MAXRISK"//blue

//graph (((close-positionprice)*pointvalue)*countofposition)/pipsize/(equity)*100 COLOURED(0,0,255) AS "MAXRISK3"//blue

//graph (((positionprice-(positionprice-(positionprice*(stoploss/100))))*COUNTOFPOSITION*pipsize*pointvalue)/(equity))*100 COLOURED(0,0,255) AS "MAXRISK2"//blue

if ((tradeprice-(tradeprice-((tradeprice*(stoploss/100)*COUNTOFPOSITION)))*pipsize*pointvalue)/equity)*100 <0 then

graph -1*((tradeprice-(tradeprice-((tradeprice*(stoploss/100)*COUNTOFPOSITION)))*pipsize*pointvalue)/equity)*100 COLOURED(0,0,255) AS "MAXRISK"//Aqua

else

graph ((tradeprice-(tradeprice-((tradeprice*(stoploss/100)*COUNTOFPOSITION)))*pipsize*pointvalue)/equity)*100 COLOURED(0,0,255) AS "MAXRISK"//Aqua

endif

//graph ((tradeprice-(tradeprice-((tradeprice*(stoploss/100)*COUNTOFPOSITION)))*pipsize*pointvalue)/equity)*100 COLOURED(0,0,255) AS "MAXRISK"//Aqua

//graph ((tradeprice-(tradeprice-((tradeprice*(newsl/100)*COUNTOFPOSITION)))*pipsize*pointvalue)/equity)*100 COLOURED(0,0,255) AS "MAXRISK-NewSL"//Aqua

//graph breakeven COLOURED(255,0,0) AS "breakeven"//Aqua

//graph ((newsl-tradeprice)/equity)*100 COLOURED(0,0,255) AS "newsl"

//graph positionsize COLOURED(0,125,255) AS "position"

//graph countofposition COLOURED(0,125,255) AS "countofposition"

//graph tradeprice-(tradeprice-(tradeprice-newsl)) COLOURED(0,0,255) AS "stoplossin%"

//graph (tradeprice-(tradeprice-((tradeprice*(stoploss/100)))))COLOURED(0,0,0) AS "pointstoSL"//Aqua

//graph (((tradeprice-(tradeprice-((tradeprice*stoploss)/100)))*positionsize*pointvalue*100)/(equity+capital))*100 COLOURED(0,0,0) AS "MAXRISK"//Aqua