Please find attached the backtests based on daily data for DAX and Soybeans suitable for life trading.

best, Reiner

Hi Reiner,

First of all let me give my thanks on your excellent work so far on all versions of Pathfinder.

I have been running OMX v5b2 live since November 7. Here follows some short feedback on live tests versus backtests.

v5b2 opened long at 1436.98 on Nov 7 21.00. Backtest opened at 1436.92 the same day and time.

However, the live test closed with loss at 1365.13 on Nov 9 5.53 (US election morning) and the backtest did not.

The backtest continued to increase the long position on Nov 9 21.00 and Nov 10 13.00 and closed on Nov 16 9.00 at 1468.76 with profit. The live test opened another long position on Nov 10 13.00 and closed with loss on Nov 17 13.00. After this the 2 tests are in sync again.

This shows the importance of a 0.6 point difference 😉

Best regards,

David

Hi David,

Thanks for your feedback. Backtest and life trading results could be different that is something I also observed. Sometimes trades not triggered only due some pips after the comma and that could be a performance killer.

I have been made some tests with a Pathfinder version based on daily data for the OMX. With the help of the daily version it’s possible to quick check whether an intrument is suitable for Pathfinder’s breakout algo or not. Please find attached the results. It works, return is positiv but the equity curve isn’t very smooth. To be honest OMX isn’t my favorit index for Pathfinder.

best, Reiner

Hi guys,

I want to share my vision with Pathfinder and this will be the last step of this idea before I move to other projects.

I’m trading around 20 instruments as future/cfd/ETF such as DAX, YM, NQ, GBL, NG, CL, GC, SI, PL, PA, HG, ZW, ZC, ZS, KC, SB, CC, LE. I will check all these instruments and figure out which are particulary suittable. The idea is to trade the top rated instruments (top 5 or 10) as a portfolio and using PRT as a signal generator.

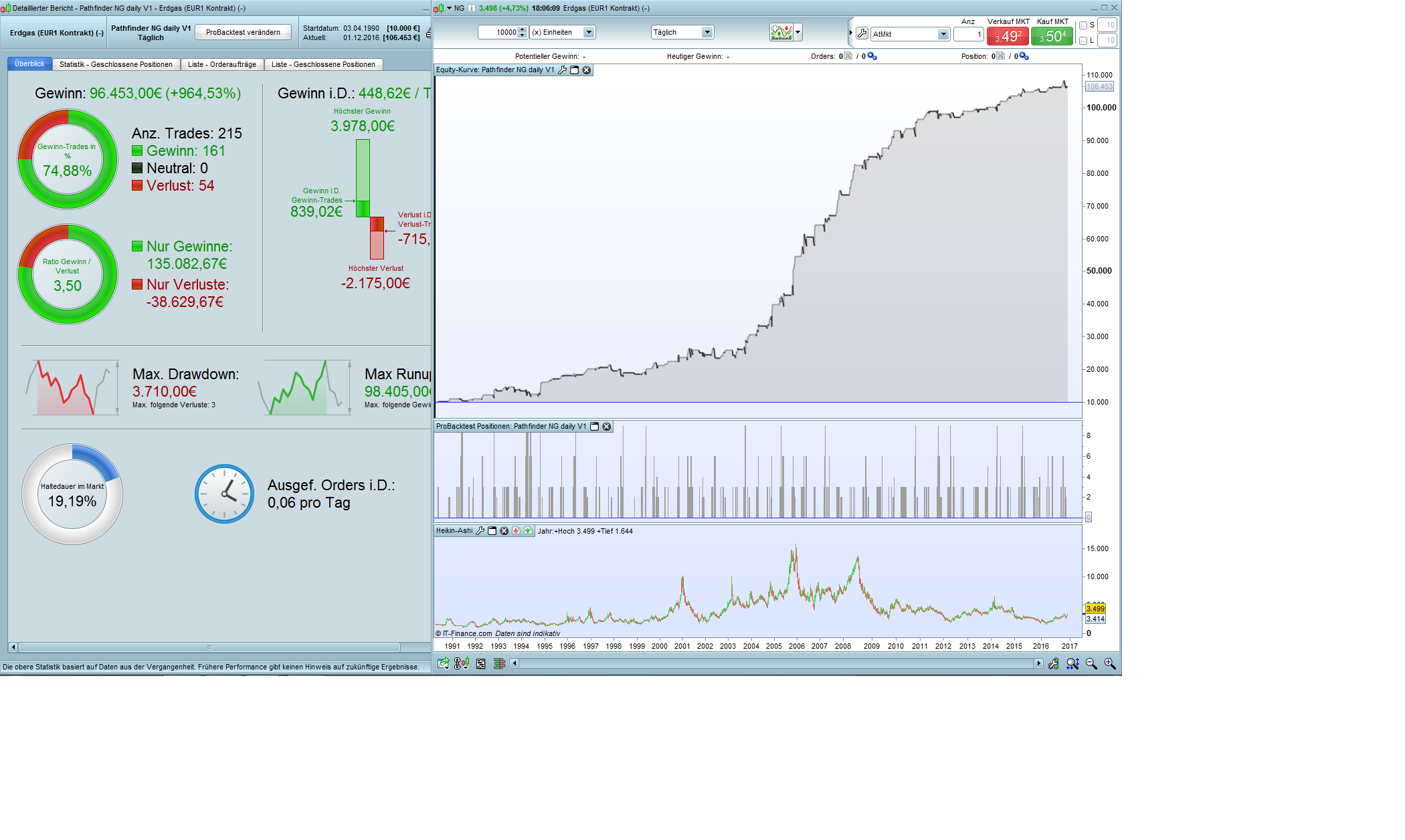

I will share the results here starting with an real seasonal monster Natural Gas.

best, Reiner

Hi Reiner,

Above all, thank you very much for sharing the fruit of your work which had to ask you a lot of time!

Are not you afraid that your Pathfinder system will become too popular and inefficient? Is Pathfinder not in danger of being challenged by professionals traders?

Best regards,

DJ

Are not you afraid that your Pathfinder system will become too popular and inefficient? Is Pathfinder not in danger of being challenged by professionals traders?

Since everyone is already trading breakout of same levels (highest high and lowest low), I don’t believe it would make any differences IMO 🙂

Hi DJ,

Thanks, but that’s to much honor for a simple logic implemented with a few lines of code. The basic idea behind Pathfinder is a breakout of previous daily/weekly/monthly high-low levels and I believe that many algos trade this signal already.

best, Reiner

I wanted to adapt Reiners algo Pathfinder-S-Daily-V1-1 for Aluminium because it has very strongly seasonal character in the end of the year.

But I can only backtest the last 2 years for daily candles (Instrument “Aluminium (5 Mini) -” . Soybeans can be backtested until the year 1978.

Is there a list, where I can see, which instruments can be backtested for which period of time in PRT?

Good morning, for anyone using the Pathfinder DAX Daily V1 could I check whether or not you were filled at 00:00 GMT?

Many Thanks

J.

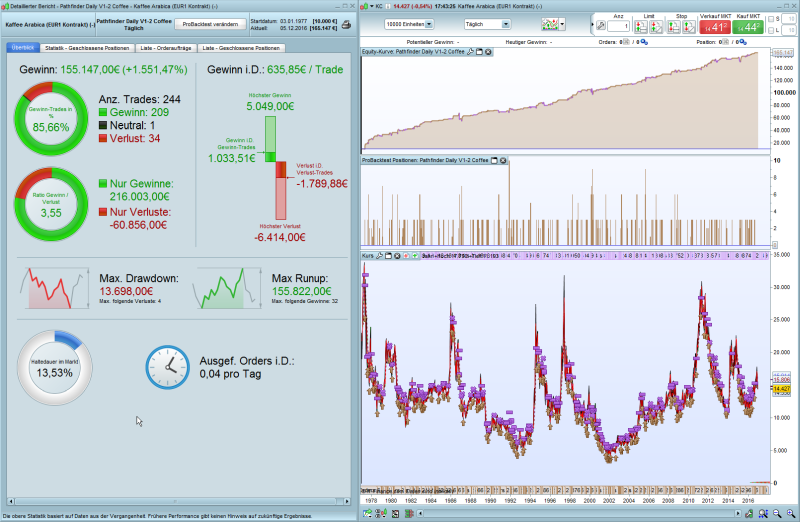

Heres is a Pathfinder-Daily version for the Instrument Coffee Arabica (“Kaffee Arabica (EUR1 Kontrakt). It has a significant drawdown but also an impressive profit curve. Please have a look.

I called this V1-2, because I changed from monthly seasonal pattern to a 2-weeks pattern, which almost doubled the profit on this instrument.

Unfortunately, this change did boost coffee only, there is no improvement on Natural Gas or Soybeans.

@Reiner: I hope this algo on coffee supports your vision of a portfolio strategy, which is an excellent idea. Thanks for sharing!

Hi Pfeiler,

Your idea is realy valueable – thanks for sharing. Coffee is a saisonal beast, difficult to tame but if you find a way it’s very profitable. Could you please verify whether the origin 6 breakout signal algo also work with your idea.

best, Reiner

Hi Jimbob,

I can’t confirm because I’m trading only the 1H and 4H systems. It’s a lucky trade if you get filled around 10.450.

best, Reiner

Hi all ,

First,let me thanks everybody who contribute in this website especially Reiner.

Second,can you please guide me to the last version of the Pathfinder strategy for the DAX?

Best Regards

Adam

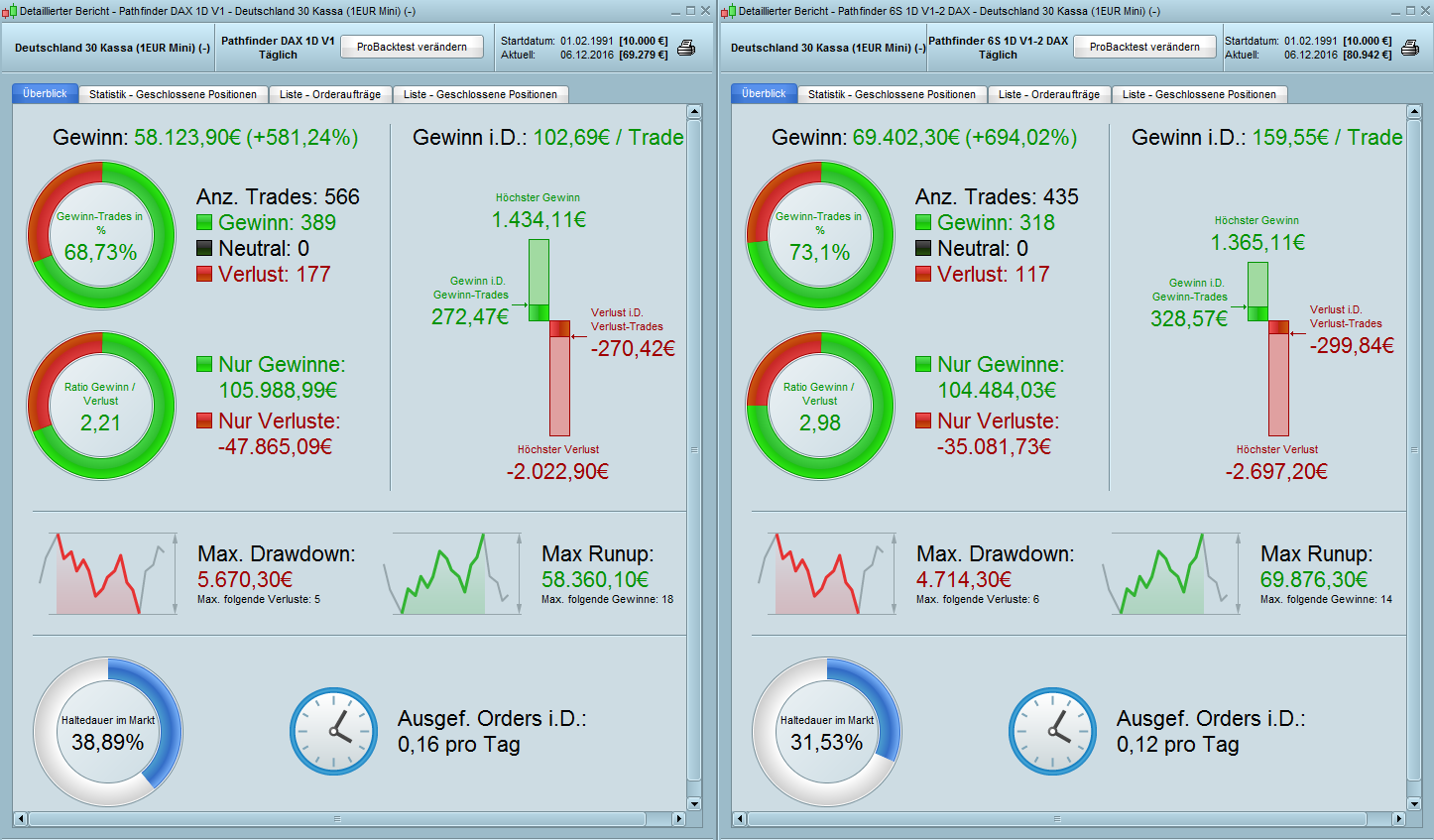

I have worked the 2-week seasonal setting in the Pathfinder Daily with 6 signals (“Pathfinder-DAX-Daily-V1-1.itf”) and curve fitted the numbers with an eye on a high Win/Loss Ratio (Ratio Gewinn/Verlust) but the result is not a step forward.

Definitly a better Ratio (old 2.21, new 2.98) .. but still much worse to the Pathfinder DAX 4H V6B2 (11,75 Ratio!!).

On the DAX I stick with V6B2 which triggered today at 13:00 and runs a nice profit so far.

Hi Pfeiler,

Thanks for your contribution. I have incorporated your idea in the Pathfinder framework because of the additional opportunities. 4H and 1H is ready so far and I hope to adjust the two daily versions today.

I can confirm that Pathfinder DAX open a position at 10724 yesterday. When the DAX cross over around 10830 Pathfinder will cumulate an addition position. It seems that DAX will test the resistance area 10850 and hoply start a year end rally. We will see whether it’s sustainable.

best, Reiner