Hi MichaelE and wp01,

I have fixed the problem with the SELL command and start life test with one contract (reduce November multiplier from 3 to 1). Let see if it works like the backtest.

best, Reiner

wp01

wp01Participant

Master

Goodmorning Reiner.

Thank you very much for the changes.

It just works perfectly now.

regards,

Patrick

Hey reiner,

your code is way too complicated for me, so excuse my question.

in the 1 hour version you do not have any short orders. but in the code I see the short conditions and the “normal” code for short, that you used in previouse versions.

So how do you make sure that there are no short positions? And do you use the previouse “short entry conditions” as exit conditions for the long positions?

because I think eventhoug it seems as your strategy is just a bundle of six single strategies, together they seem to complement each other.

thank you

mfg

Flo

Hi Reiner – thank you for all this work. I saw in an earlier post that you made an earlier code for the Hang Seng, based on v5 perhaps? I’ve wondered if you’d looked at it with V6? I had a quick play around amalgamating the two and it looks promising although my coding isn’t good enough to do it properly.

J.

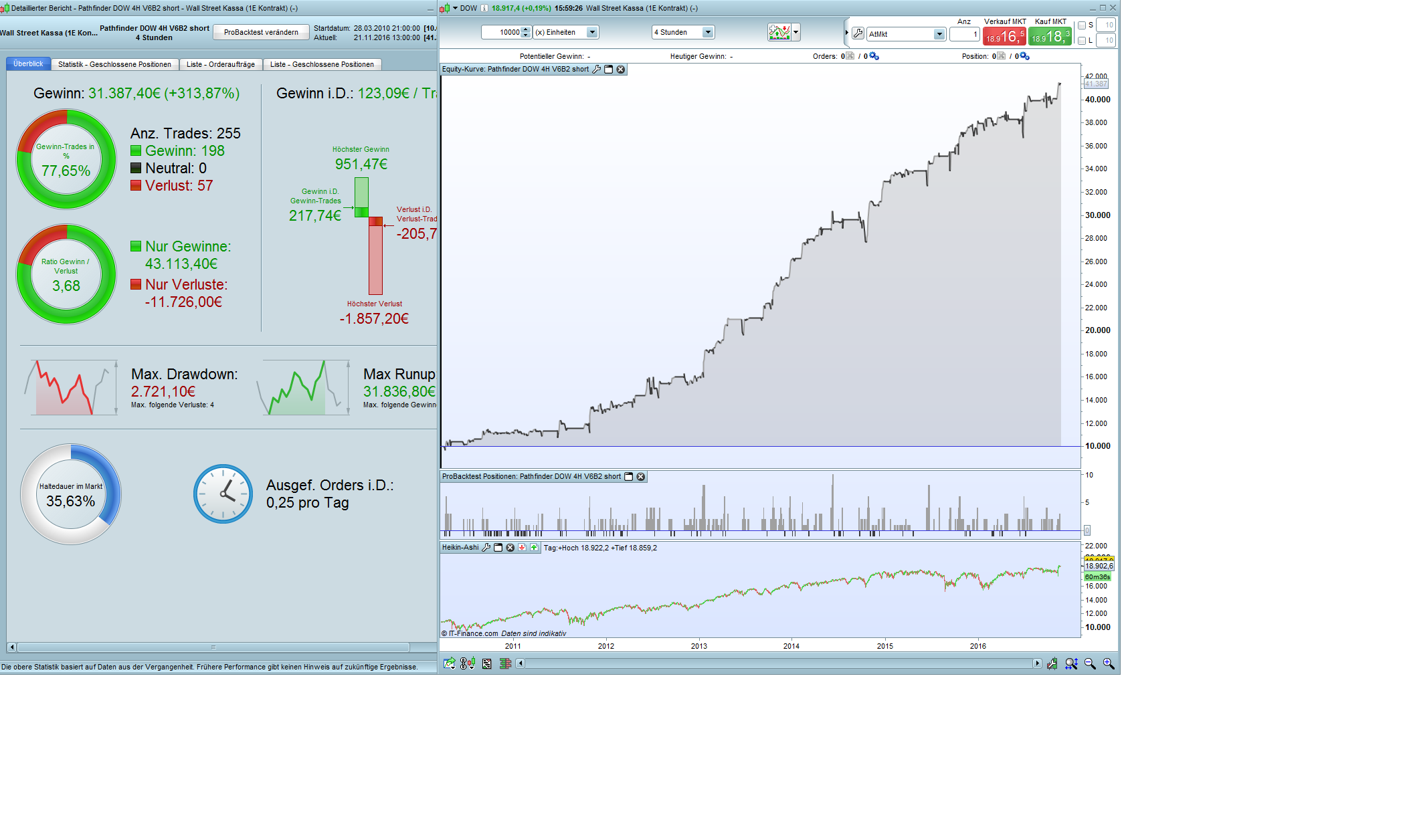

Hi arke,

I have adjusted Pathfinder V6B2 for the DOW. Please find attached two versions of Pathfinder DOW 4H V6B2 (long backtest starts on April 2006 and short on May 2010). Long version has a significant drawdown of 50%. I tried to reduce the drawdown and the risk in the short version.

best, Reiner

Hi Flo,

I’m sure you’re one of the guys who understand the ideas behind Pathfinder and the dependencies and how it’s implemented in the code.

Backtests have showen that in 1H the short side was poor. I played around with different additional levels such as dailyHigh, weeklyLow and montlyLow but didn’t find any improvement. As you know from all your tests that the short side is also very important for the balance of the whole system. To get the benefits of the short side I changed the SELLSHORT command to SELL so a short trigger will close the long postion but won’t further short the market.

best, Reiner

Hi Jimbob,

I will adjust Hang Seng to V6 but I need some time to fullfill all the requests here in the forum. I already promised OMX, FTSE and Bund. I comeback to you as soon I have somthing.

best, Reiner

wp01Participant

Master

Unfortunatley the thanks button doesn’t work anymore, or at least on my computer, so i’d like to thank you for the files on the Dow.

regards,

Patrick

Thanks Reiner. Don’t worry too much about the Hangseng, it was only because v5 worked so well that I thought it might be an easy one to do 🙂 no rush at all!

arke

arkeParticipant

Average

Hi Reiner,

thank you very very much for the DOW Version 🙂 Yes long side has a huge drawdown…

if you reduce the multiplier so that the system is trading just with one contract and backtest it for this year, profit is negative… i’ll try to adjust it a little bit

Arke

Dear Reiner

Many thanks for your response.

I have checked the variable maxPositionSizeLong and the ProOrder maximal number of contracts and everything looks fine. So I do not understand why the 2° position was not open.

But I can confirm, that Pathfinder Oil last evening opened at 9 pm the third position.

Thanks in advance

MichiM

Mark

MarkParticipant

Senior

Hi,

I am about to start DAX V5B2 in live mode, can you tell me if and when you should be increasing the pointsize or should it always stay at 1?

Mark

reb

rebParticipant

Master

Hi mbaker15

It depends on your initial capital, I will increase from 1 to 2 when my capital doubles

Reb

Hi guys!

Maybe a stupid question and maybe answered but I just got to ask to get it out of my head:) On my intraday charts on indices I just have data shown for the actual trading hours because that’s how I want it for my manual trading. How does that affect the result when running Pathfinder live since we want to run the system on 24h data? I see that it has huge effect backtesting but how is it when going live? What settings do you use? Is it possible to have it the way i want it?

Hi all, I follow this thread for a while and I started to use this strategy on IG. I created an indicator to show parameters on graph to verify algoritm. It shows:

- signalline

- monthly high/low

- weekly high

- daily high/low

- longMA

- shortMA

You can customize (with DAX default values):

- periodFirstMA

- periodSecondMA

- periodThirdMA

- periodLongMA

- periodShortMA

Maybe someone finds it useful