@Bandido

That explains it. Your version differs on several points.

Maybe we need to point out when a version other than the official is used when reporting opening and closing of trades?

Soybeans closed at 1am at 1001 with a loss. As we say in Sweden: up like a sun, down like a pancake.

Best regards, David

Morning everyone, Can someone confirm NG long 2 contracts opened this morning?

Also I had a quick look at STXE and it shows: maxPositionSizeLong = MAX(0, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

Regards

Malek

@maleknf

I am running the Reiner version of NG and no position opened today, nor rejected.

Hmm, yes, my fault. Change it to 15. Didn’t show in the backtest.

Best regards, David

@DAJVOP

Order details attached.

Keep on mind I am using the version shared by @Pfeiler few days ago.

Regards

Malek

@maleknf

Is it the version with PeriodThirdMa = 3?

wp01

wp01Participant

Master

@Maleknf, David,

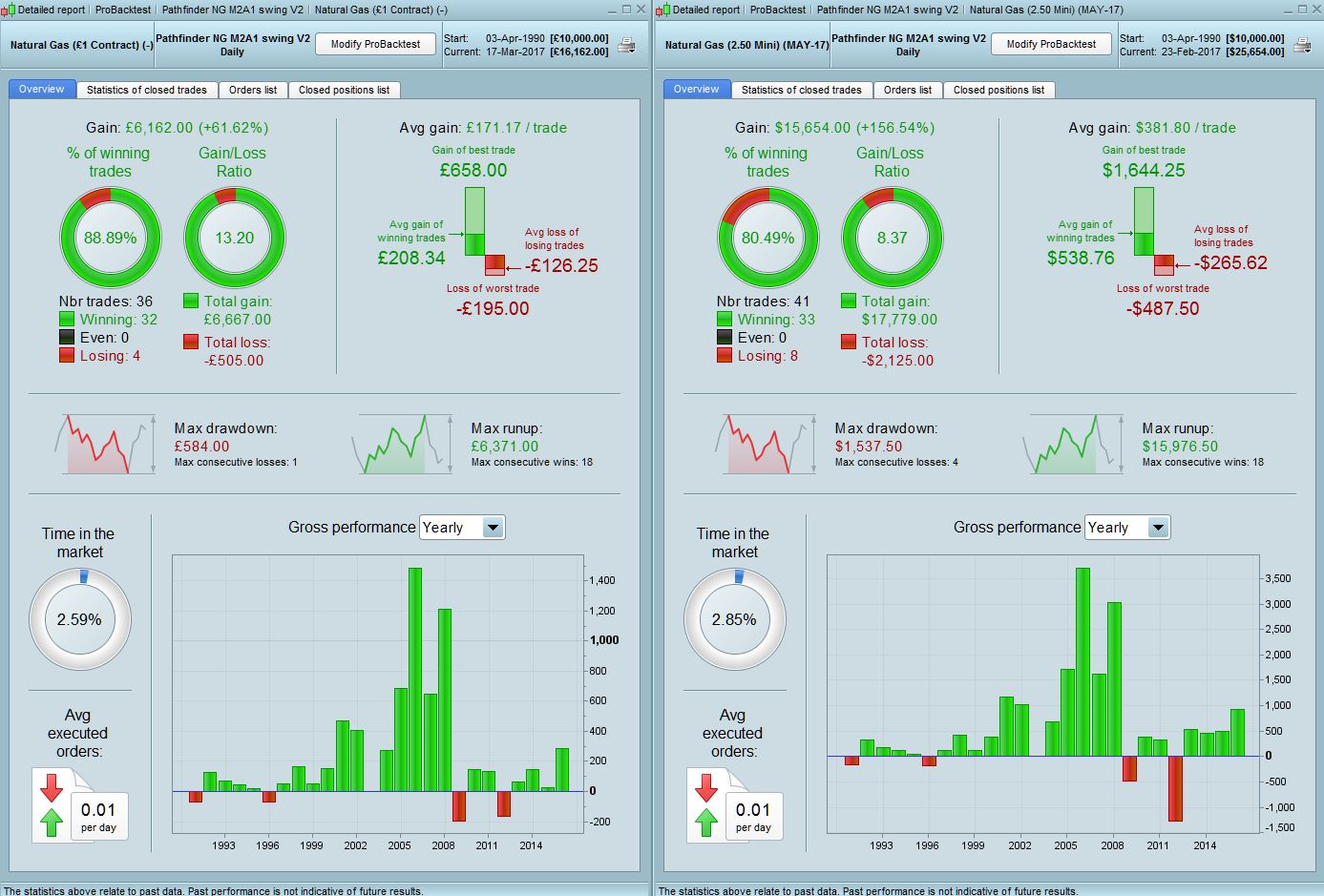

The NG should be adapted to the May future as far as i understand it correctly.

Since NG minimum amount af contracts is 2,5 it doesn’t work for the EUR1 unless you change the code to 2.5. But than the results are not ok.

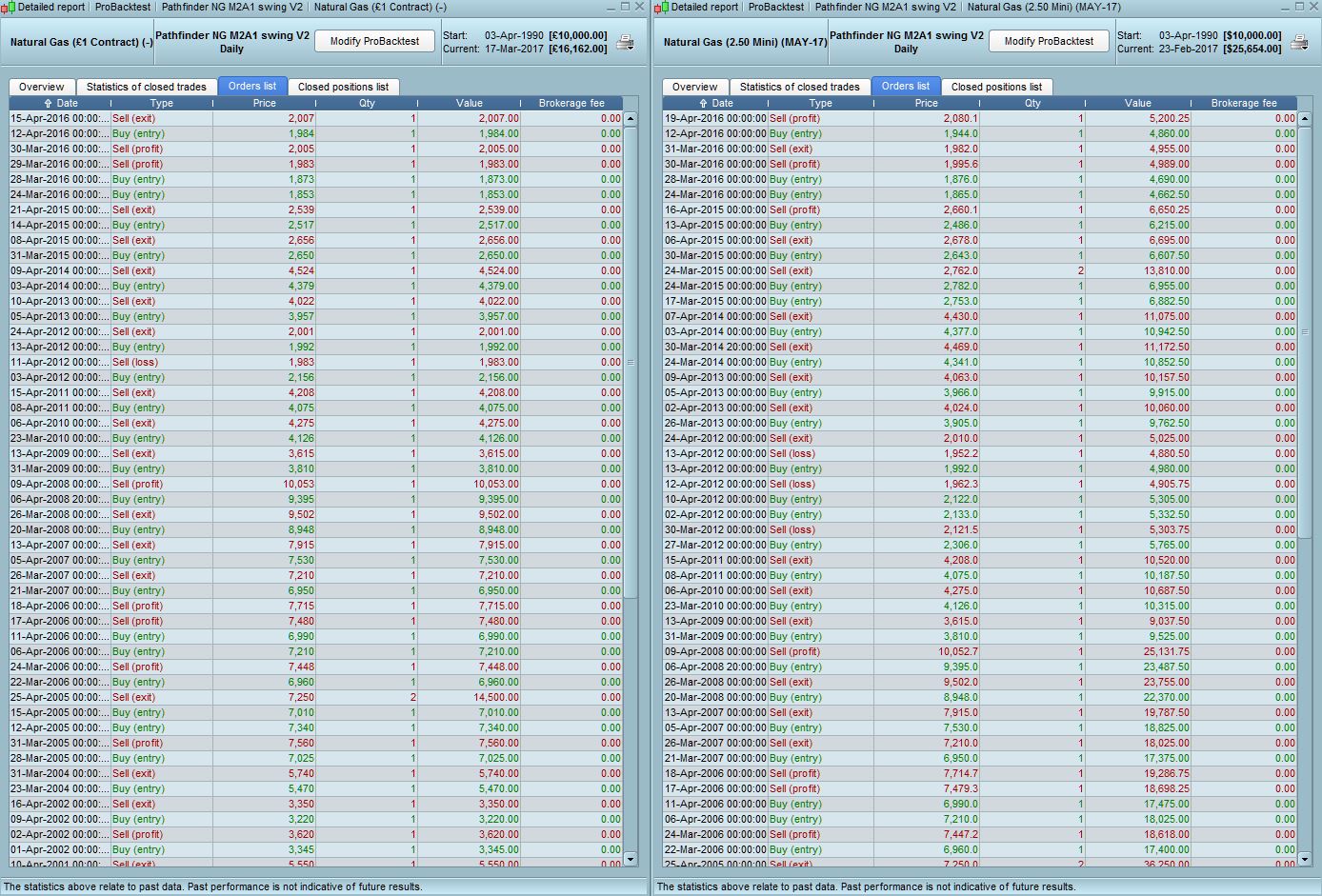

When you take the future it is already multiplied by $2,5. You can read the discussion on page 45 with pictures of the versions from Pfeiler.

Pathfinder swing TS

But there is something weird about the future of May. It is in PRT but not in IG. So i’m not sure if it will be triggered.

Mine isn’t triggerd on the future of May last night.

Patrick

Patrick

Either way, if it was triggered but not executed it should show as rejected.

wp01Participant

Master

That’s right David. To which instrument did you adapt it?

And that you do not see it in the BT isn’t that because it will be shown with a 24hrs. delay?

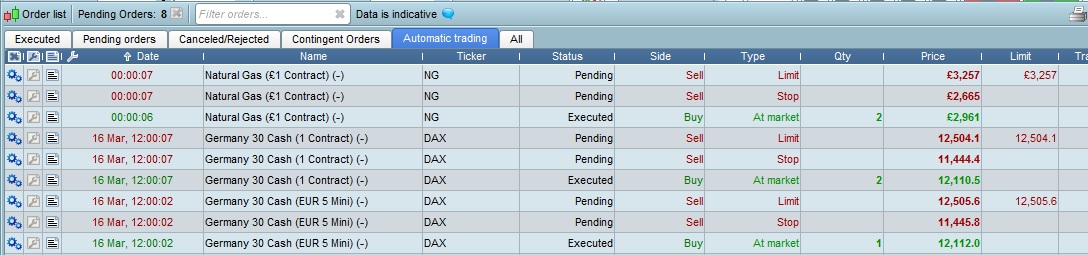

@ maleknf – I can confirm the NG position opened at 12am GMT @ 2961. This is in Live SB. I used the NG DFB market to run it on and not the May future.

@ dajvop – I agree, we need to make clear if we are talking about a version that is not the official one as that would of course lead to differing results between people. As long as users only change the position sizing parameters to suit their own risk profile then the systems should match trades between users (of course we all know that it doesn’t work out like that in practice due to various bugs in PRT- but theoretically it should).

I backtested the DFB vs the May 17 Future and the results are broadly similar – you would expect absolute differences due to one being a £1 contract and the other a E2.5 one and the entry levels to also be different due to DFB vs Futures prices etc etc

Just realised that the reason that nothing is showing up in the trades is because the IG May future in SB is stuck at 2620 price which is Feb 23rd price and is stale. There has been no update since then, hence the code has not triggered a position. The same applies to the CFD platform – the last price is the Feb 23rd one. Think we all just missed this whilst putting together the codes, easy error to make tbh.

The DFB market is uptodate and live so we can use that in SB and for CFD the live contract is the Natural Gas (£1 contract), both have the correct prices.

But now we know this, it’s something to look out for in future when constructing other months (and implementing in live), just make sure that the price/contract is live.

If people want to enter the trade manually, the current price is lower @ around 2943 instead of system entry @ 2961

@MANEL Thank you for your confirmation! can you please confirm on the excel-sheet?

@dajvop the version I using as following:

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 3

// define filter parameter

ONCE periodLongMA = 50

// define position and money management parameter

Capital = 10000

Risk = 5 // in %

equity = Capital + StrategyProfit

maxRisk = round(equity * Risk / 100)

positionSize = 1

ONCE stopLossLong = 10 // in %

ONCE takeProfitLong = 10 // in %

maxPositionSizeLong = MAX(15, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

ONCE maxCandlesLongWithProfit = 10 // take long profit latest after x candles

ONCE maxCandlesLongWithoutProfit = 14 // limit long loss latest after x candles

Regards

Malek

@ maleknf – Thanks for alerting, I missed the fact that we’ve implemented an excel sheet like the one Grahal and myself created on the 4H version, will update it.

@ Grahal – Thanks for creating a trade log for the Daily version here as well

Well, that explains a lot 🙂

Opening 1 manually instead.

@ dajvop. We discover something new each day here, even I wouldn’t spotted the issue if I wasn’t trying to investigate this today.

For info so that you are aware, the stop and limit have been set at 2724 ad 3168 respectively.