Hey michi,

I checked dax v6 /v6b2 on prorealcode v10.3. it was almost the same, some minor differences. I will upload the results of the backtest.

but I think if you open a new demo account on ig , you will be able to work with the beta version of v10.3

Hey Flowsen

Thank you for your message. I think Switzerland will be updated after Germany.

Thanks for the screen.

Michi

Hey Reiner,

on the first page you list the “good” setups for each seasonality. is it still the plan to optimize the systems for longer periods (e.g. jan2-mar1) if the results are good and you just put it in the list several times? or do you prefer a separate optimized itf for each seasonality? I hope you get what I am trying to ask 🙂

Hi Flowsen

Yes you have to optimized for each seasonality where you find a 3 in the Excelsheet.

Michi

Hi

Silver is not so easy to test. In the attachment the itf.

One for J1 – F1 January to February

One for M2 May

One for J2 -A2 July to August.

Michi

Mark

MarkParticipant

Senior

@flowsen

i understand what you’re asking, I think it would be less work to just list them in each month several times. I suppose we just need to list them the clearest way possible. Would the results be much different if you optimised them separately e.g. Jan2, mar1 instead of jan2-mar1 I’m not sure they would so can’t see much reason to do each season separately.

Hi Kasper, in my opinion Gold in March could be a profitable setup. I’ve increased the position size to get a good result.

Hi Jesús, the London Wheat future March 17 has a history from 2011. I agree we have not enough historical data to consider it further. May be someone else find a longer history for wheat or corn as well. Both are very related to seasonal behavior.

Hi David, your Hang Seng backtest is perfect. I take it as it is and move it to the hall of fame.

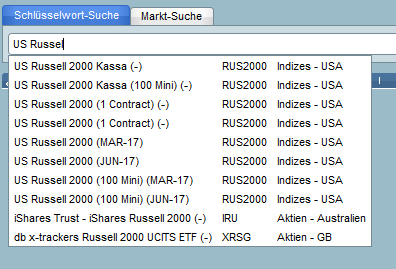

@Robin: Thanks for your amazin work with the US Russel 2000. I try to replay your results, but with my Russel instruments I am not able to. I do not have a “US Russel 2000 (DFB)” .. see screenshot. Could you please advice, which instrument exactly you have used?

Besides, I tried to merge all the single programs in one program, that can be run over the whole year. I think this is, what we need for all the other instruments too (can’t really handle 200+ programs for Pathfinder).

What do you think? Does it run with your Russel instrument and return equal results?

David, ASX is also very good. Only one change and welcome to the hall of fame.

Hi Pfeiler,

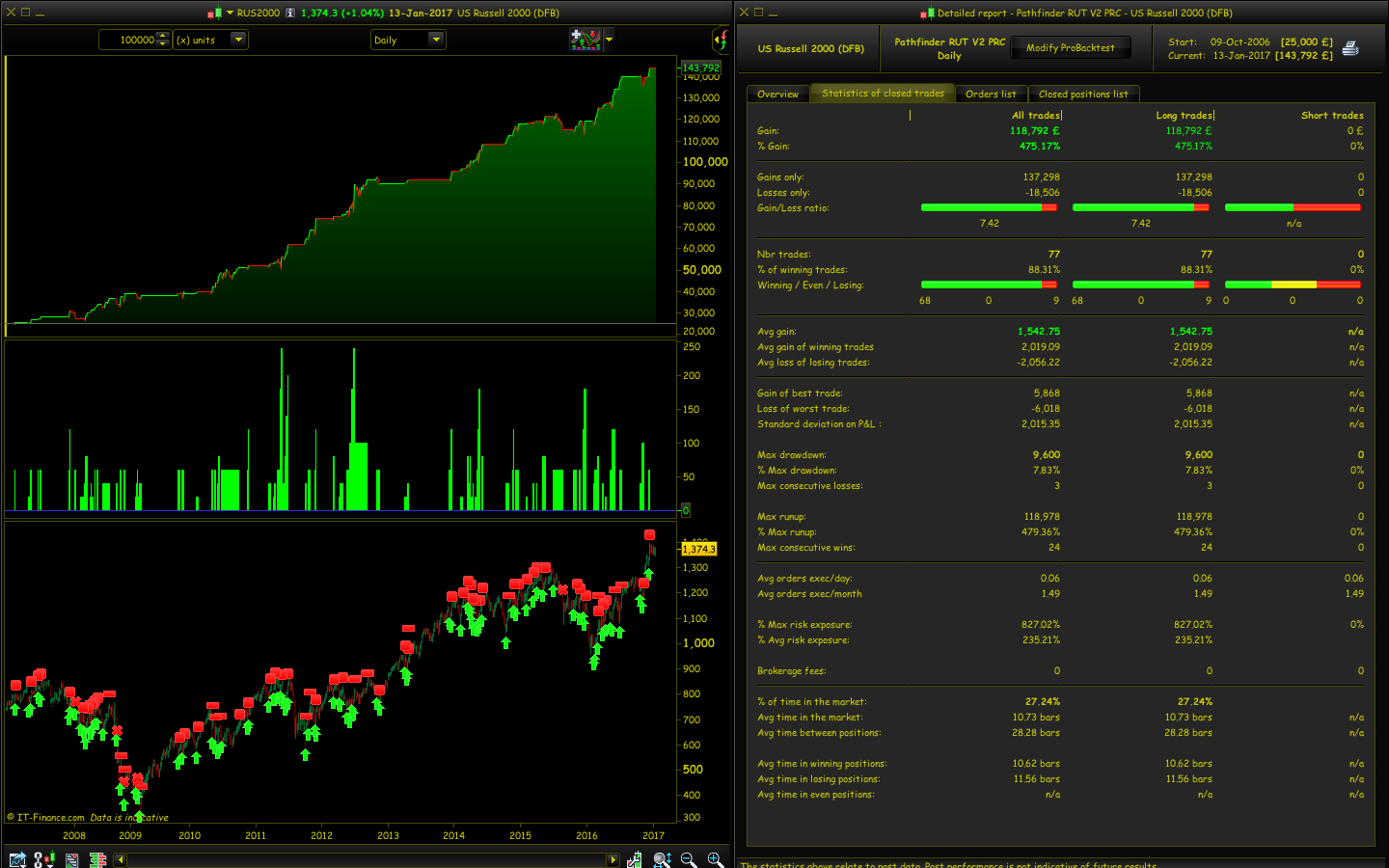

Thanks for your work. I use the DFB (daily funded bet) as it gives the most past data, it mirrors the futures almost exactly on IG. Below I enclose the results of your compiled code. The results of the compiled code are slightly different to running the individual robots, and this will be due to trades overlapping end/starts of months (we can cross into a stronger period with the previous code running). I did consider that this could be an issue, so perhaps it’s better to join together the months that run consecutively and optimise a longer period. The results of your compiled code still give very strong results. I think it’s possible to run the RUT with a lower sized account, but I made it £25k to be on the safe side. When we have multiple months optimised for each market, I think putting them together in 1 robot is a great idea.

Robin.

Hi Ale, MIB is very good but I reduces the position size to 1 and move it to the hall of fame. I also tested Feb1 together with Jan2 but it was not better.

Pfeiler, these are the results I get on the IG RUT futures using the compiled code, they go back to March 2011. The draw down looks large on paper, but it’s still a low % as the strategy profit has accumulated in the account through the period.

Robin.

Hi Martin (Brage), I agree Cotton looks very promising. Excellent job and welcome in the hall of fame.