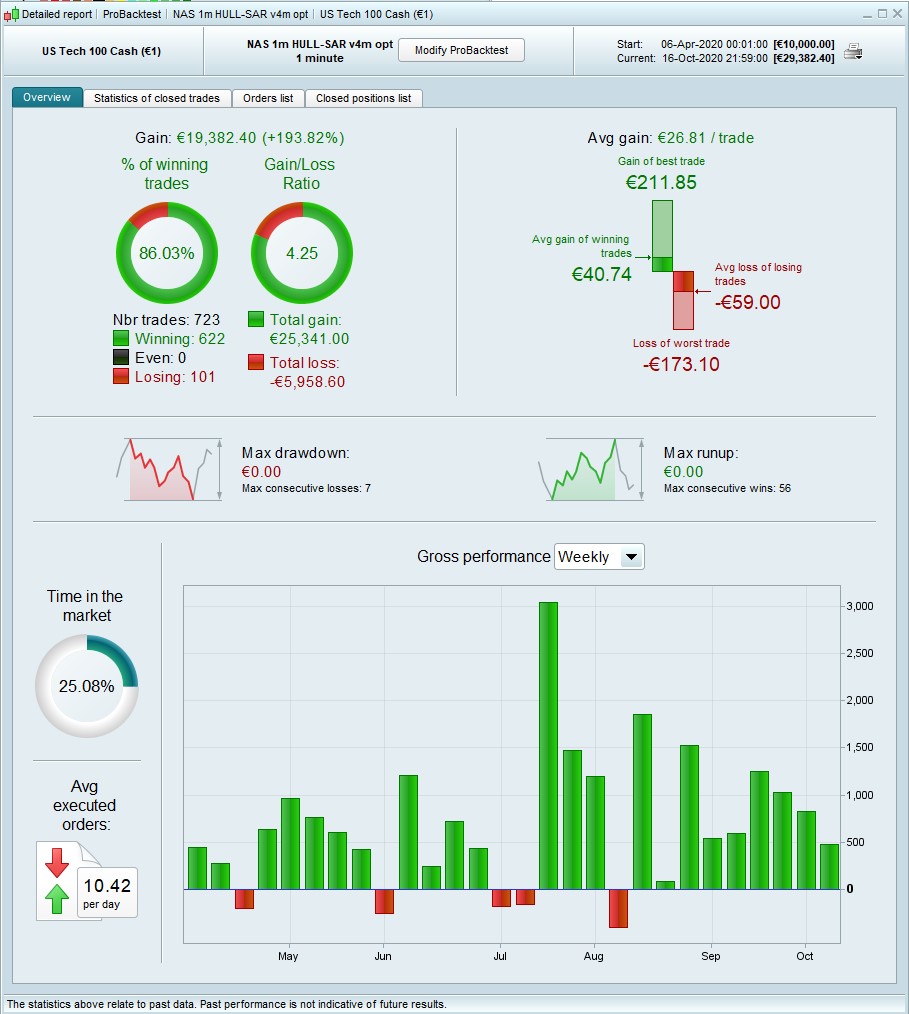

yeah, I like it – better % win, better gain/loss, lower drawdown, only slightly lower profit but probably better in the long term. Thanks Fifi! 👍

Paul

PaulParticipant

Master

Hi Nonetheless,

Looking at your money management code, it calculates the new positionsize when there’s no market position.

However, if going from long to short directly & visa versa, which can happen a lot, regardless gain or loss there is no change in positionsize, so essentially there could be more gains to explore.

Is this something which can be changed? strategyprofit is only calculated when the position is closed.

Do you think it’s worth the effort to change this?

PaulParticipant

Master

Had a try, but doesn’t make much difference overall on vectorial strategy.

It had to be place right above the entry since it needs to know before the reversal takes place what positionsize to use. Seems to work as I tended in a glance.

once startpositionsize = 1

once factor = 10 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

once margin = (close*.05) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

once margin2 = (close*.05) // tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

once tier1 = 55 // ig first tier margin limit

once maxpositionsize = 550 // ig tier 2 margin limit

once minpositionsize = 1 // enter minimum position allowed

strategypp=strategyprofit+(positionperf(0)*100)*(tradeprice(1)/100)

if not onmarket or ((longonmarket and condsell) or (shortonmarket and condbuy)) then

positionsize = startpositionsize + strategypp/(factor*margin)

endif

if not onmarket or ((longonmarket and condsell) or (shortonmarket and condbuy)) then

if startpositionsize + strategyprofit/(factor*margin) > tier1 then

positionsize = (((startpositionsize + (strategypp/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 //incorporating tier 2 margin

endif

if not onmarket or ((longonmarket and condsell) or (shortonmarket and condbuy)) then

if startpositionsize + strategypp/(factor*margin) < minpositionsize then

positionsize = minpositionsize //keeps positionsize from going below allowed minimum

endif

if (((startpositionsize + (strategypp/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 > maxpositionsize then

positionsize = maxpositionsize// keeps positionsize from going above ig tier 2 margin limit

endif

endif

endif

PaulParticipant

Master

one part needed change

if onmarket then

strategypp=strategyprofit+(abs(countofposition)*(positionperf(0)*100)*(tradeprice(1)/100))

else

strategypp=strategyprofit

endif

Downside is, it’s not exactly a snippet anymore because it must know when conditions are met.

it was interesting to test.

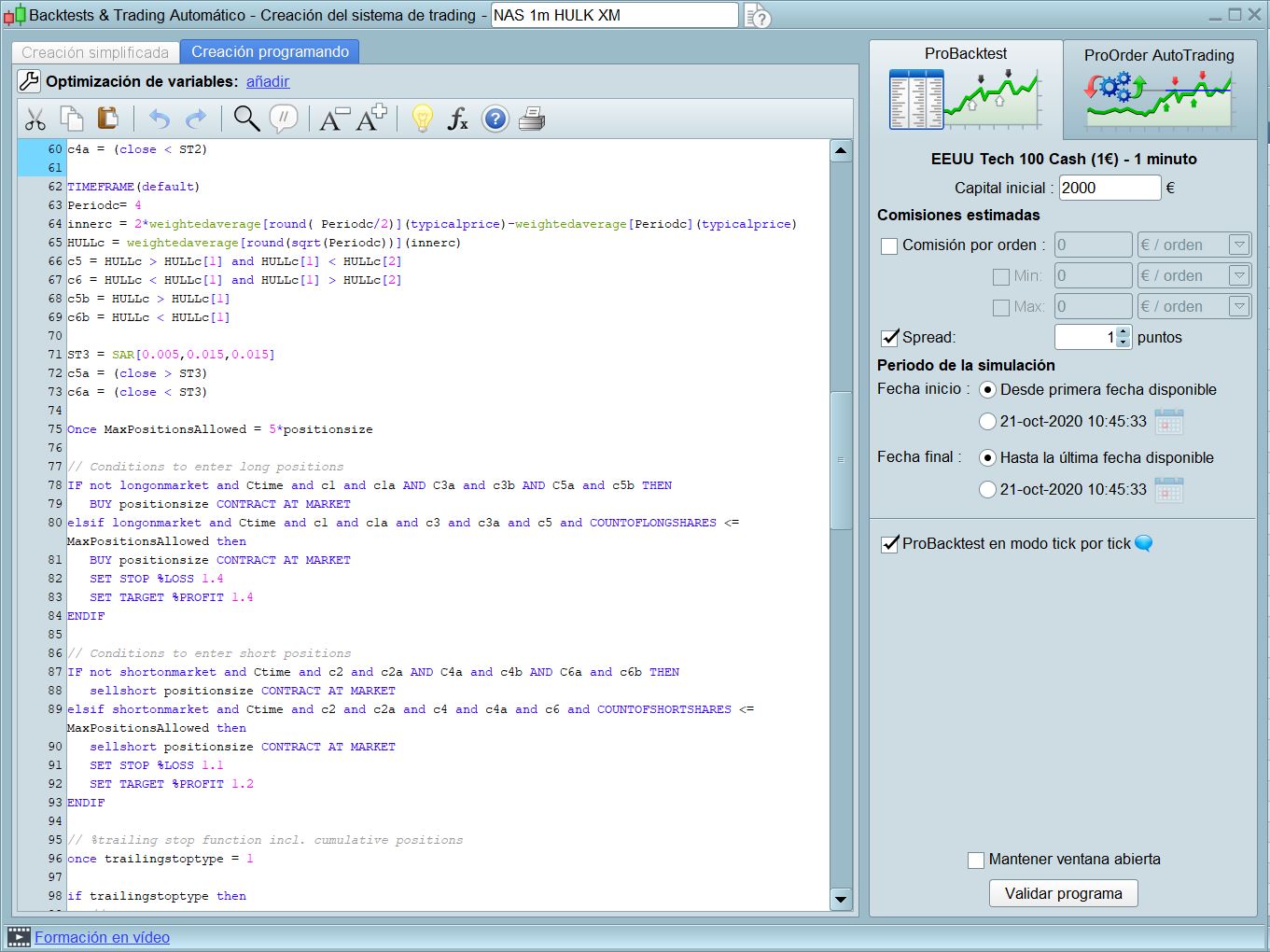

Thanks for that, Paul – def worth having a look at. Recently I changed it to

//Money Management NAS

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize=1

ENDIF

if MM = 1 then

ONCE startpositionsize = 1

ONCE factor = f // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE margin = (close*.005) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.01)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 200 // IG first tier margin limit

ONCE maxpositionsize = 2000 // IG tier 2 margin limit

ONCE minpositionsize = 1 // enter minimum position allowed

IF StrategyProfit <> StrategyProfit[1] THEN

positionsize = startpositionsize + Strategyprofit/(factor*margin)

ENDIF

IF StrategyProfit <> StrategyProfit[1] THEN

IF startpositionsize + Strategyprofit/(factor*margin) > tier1 then

positionsize = (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 //incorporating tier 2 margin

ENDIF

IF StrategyProfit <> StrategyProfit[1] THEN

if startpositionsize + Strategyprofit/(factor*margin) < minpositionsize THEN

positionsize = minpositionsize //keeps positionsize from going below allowed minimum

ENDIF

IF (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 > maxpositionsize then

positionsize = maxpositionsize// keeps positionsize from going above IG tier 2 margin limit

ENDIF

ENDIF

ENDIF

ENDIF

using IF StrategyProfit <> StrategyProfit[1] to allow for instant reversals. Seemed to solve the problem of algos that were onmarket near to 100%, but I hadn’t thought of merging it with the entry conditions… could be worth playing around with.

PaulParticipant

Master

I tried that too, but didn’t look close enough using graph! There’s a difference at the bar of the reversal.

Did a side by side comparison between your approach and mine, there’s a very small difference.

It’s easier to use your method which had a +400 on a equity of 117500. I remember you ran into this problem somewhere. I will update it in my strategies. Thanks.

Thank you all for your effor and for sharing this in the forum, it is an inspiration for people like me who are trying to start programming algos in PRT. @nonetheless or anyone, could you tell me which GTM hour is this algo using? I’ve tried it in GMT+2 and it works properly but probably another GMT time would be better to fit the parameters of the algo. Thanks in advance.

Hi @Ryugin, it’s set to UK time so for Spain I expect you need to change it to

Ctime = time >=153000 and time <220000//Euro time, GMT +1

it’s just the Wall St opening hours.

@Paul, did you see I added a line to your %TS

once trailingpercentlong = tsl // %

once trailingpercentshort = tss // %

once accelerator = acc // 1 = default; always > 0 (i.e. 0.5-3)

once accelerator2 = acc2 // 1 = default; always > 0 (i.e. 0.5-3)

once ts2sensitivity = 0 // [0]close;[1]high/low;[2]low;high

//====================

once steppercentlong = (trailingpercentlong/10)*accelerator

once steppercentshort = (trailingpercentshort/10)*accelerator2

accelerator2 gives the option to further optimize the TS going short, usually shows a small advantage.

Hi @Ryugin, it’s set to UK time so for Spain I expect you need to change it to

Ctime = time >=153000 and time <220000//Euro time, GMT +1

Ctime = time >=153000 and time <220000//Euro time, GMT +1

it’s just the Wall St opening hours.

Just to make sure I haven’t missed something since the timezone comes up in every thread. If I set custom trading hours in PRT that matches the exchange, for Nasdaq UTC-4. I just set the regular trading hours (9:30-16:00) in the script?

PaulParticipant

Master

yes, I did see that, nice touch! I would like to say it’s perfect now but it is not cuz I found maybe a bug.

Using it on vectorial, I saw a big difference in results using trailing-stop sensitivity 0 or 2 and the difference was too big to explain. Especially the last trade with the big loss. When it uses the close, the trade can exit too early. Something is off there can you ‘ve a look too?

PaulParticipant

Master

I’ve loaded the original one of nicolas & modifcations by robertoguzzi. That seems to work oke.

Then I took the version from your v3 strategy, which uses % instead of points and uses default close which is off too.

Think I found it

if onmarket then

trailingstart = positionprice[0]*(trailingpercent/100) //trailing will start @trailingstart points profit

trailingstep = positionprice[0]*(stepPercent/100) //% step to move the stoploss

endif

It used positionprice[1] and when there’s no market position and opened a new one it went off the rails.

Hello everybody,

can you provide the complete code again after all the others?

Thanks already heard.

Hello, first thanks for your work.

I keep seeing that he makes many entries in a row without closing the first ones. For that you have to have a large capital.

I have also tried reducing the 0.4lotti, but it keeps coming in with 1lotti.

Can you help me please? is there something that escapes me?

NOTE: In this test I have added the chunk of Fifi:

Mrsi=RSI[14](close)

if longonmarket and CurrentDayOfWeek=5 and close>positionprice and Mrsi crosses under 70 then

sell at market

endif

if shortonmarket and CurrentDayOfWeek=5 and close<positionprice and Mrsi crosses over 30 then

exitshort at market

endif

Nasdaq has a minimum position of 1.