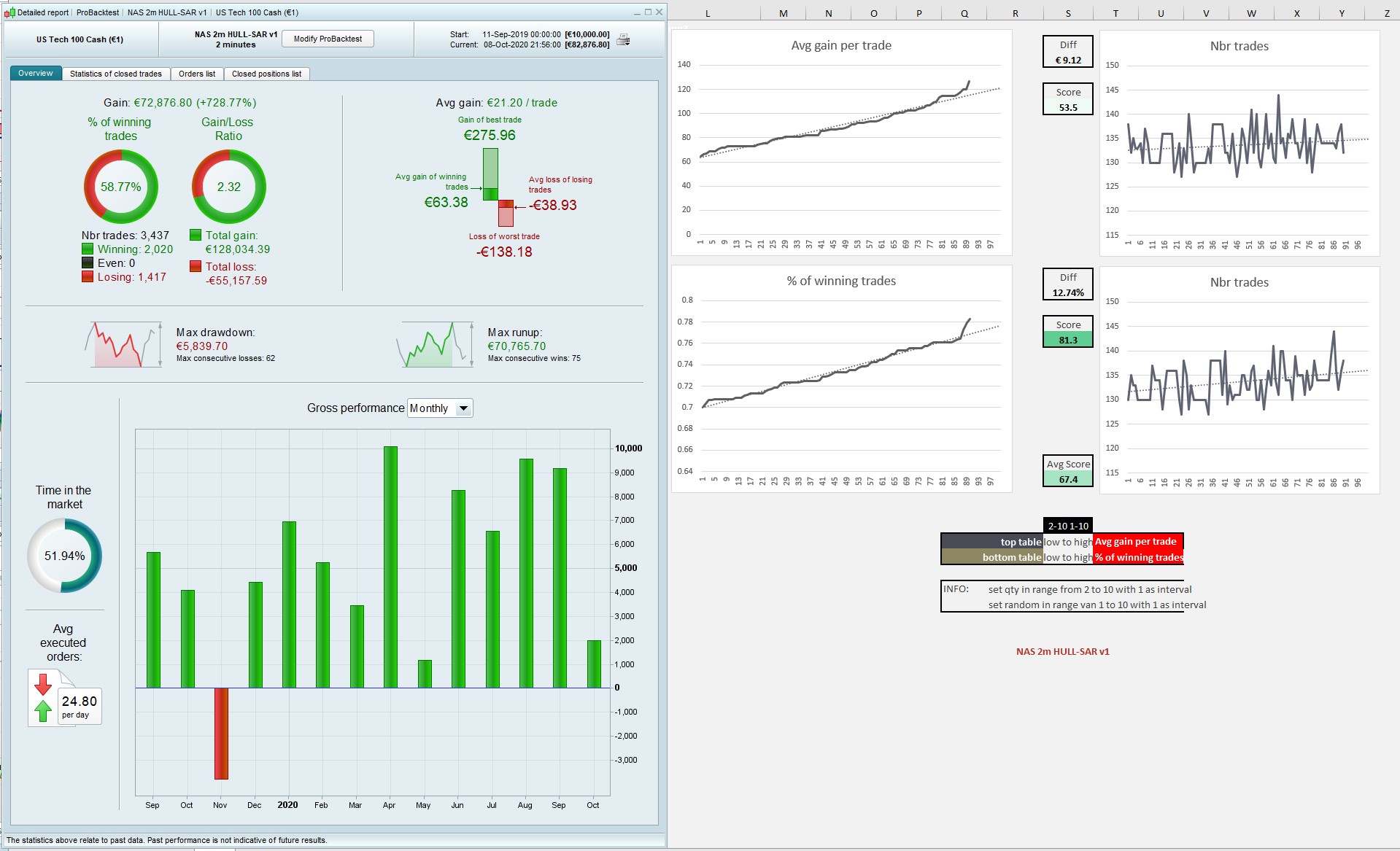

This is a new 2m strategy I’ve been working on, uses Hull MA and Parabolic SAR in 3 time frames with cumulative orders. Short back test so may be a curve fit but the VRT is good.

I think it can still be improved but I’ve run out of ideas so any suggestions are welcome, maybe a limit to the number of positions? Cumulative orders are not to everyone’s taste, and the drawdown is huge – you’d need a lot of capital to run it – but as a % of the runup it’s not that bad. Could be worth playing with…

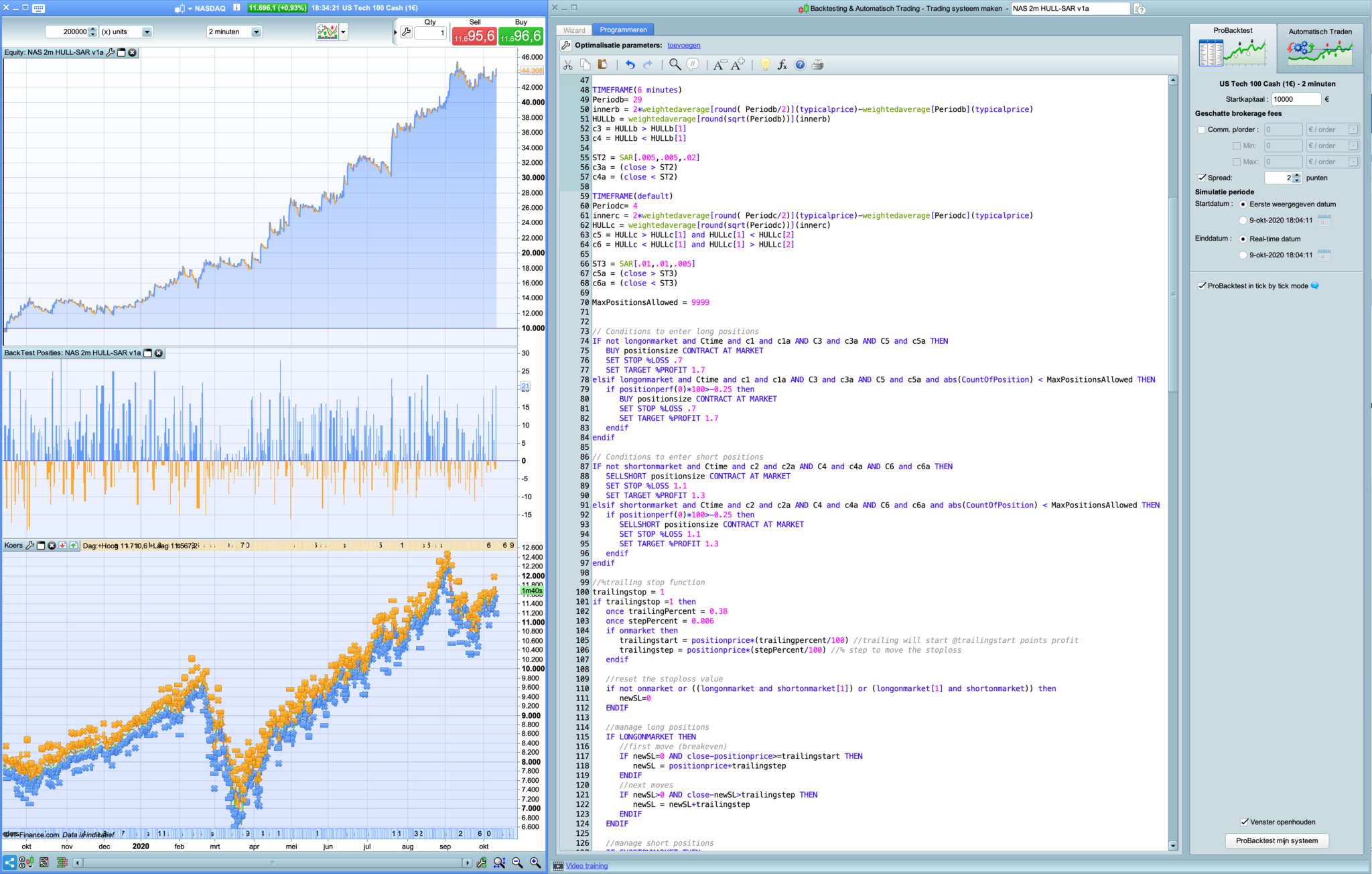

Ctime = time >=143000 and time <210000

TIMEFRAME(18 minutes)

Period= 155

inner = 2*weightedaverage[round( Period/2)](typicalprice)-weightedaverage[Period](typicalprice)

HULLa = weightedaverage[round(sqrt(Period))](inner)

c1 = HULLa > HULLa[1]

c2 = HULLa < HULLa[1]

ST1 = SAR[.005,.005,.02]

c1a = (close > ST1)

c2a = (close < ST1)

TIMEFRAME(6 minutes)

Periodb= 29

innerb = 2*weightedaverage[round( Periodb/2)](typicalprice)-weightedaverage[Periodb](typicalprice)

HULLb = weightedaverage[round(sqrt(Periodb))](innerb)

c3 = HULLb > HULLb[1]

c4 = HULLb < HULLb[1]

ST2 = SAR[.005,.005,.02]

c3a = (close > ST2)

c4a = (close < ST2)

TIMEFRAME(default)

Periodc= 4

innerc = 2*weightedaverage[round( Periodc/2)](typicalprice)-weightedaverage[Periodc](typicalprice)

HULLc = weightedaverage[round(sqrt(Periodc))](innerc)

c5 = HULLc > HULLc[1] and HULLc[1] < HULLc[2]

c6 = HULLc < HULLc[1] and HULLc[1] > HULLc[2]

ST3 = SAR[.01,.01,.005]

c5a = (close > ST3)

c6a = (close < ST3)

// Conditions to enter long positions

IF Ctime and c1 and c1a AND C3 and c3a AND C5 and c5a THEN

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS .7

SET TARGET %PROFIT 1.7

ENDIF

// Conditions to enter short positions

IF Ctime and c2 and c2a AND C4 and c4a AND C6 and c6a THEN

SELLSHORT positionsize CONTRACT AT MARKET

SET STOP %LOSS 1.1

SET TARGET %PROFIT 1.3

ENDIF

//%trailing stop function

trailingstop = 1

if trailingstop =1 then

once trailingPercent = 0.38

once stepPercent = 0.006

if onmarket then

trailingstart = tradeprice(1)*(trailingpercent/100) //trailing will start @trailingstart points profit

trailingstep = tradeprice(1)*(stepPercent/100) //% step to move the stoploss

endif

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart THEN

newSL = tradeprice(1)+trailingstep

ENDIF

//next moves

IF newSL>0 AND close-newSL>trailingstep THEN

newSL = newSL+trailingstep

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart THEN

newSL = tradeprice(1)-trailingstep

ENDIF

//next moves

IF newSL>0 AND newSL-close>trailingstep THEN

newSL = newSL-trailingstep

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

endif

Excellent G/L-ratio on that amount of trades.

I agree that the max amount of cumulative orders should be an option to avoid anxiety. For example this:

MaxPositionsAllowed = 5

// Conditions to enter long positions

IF ctime and c1 and c1a AND C3 and c3a AND C5 and c5a and abs(CountOfPosition) < MaxPositionsAllowed THEN

BUY 1 CONTRACT AT MARKET

SET STOP %LOSS .7

SET TARGET %PROFIT 1.7

ENDIF

// Conditions to enter short positions

IF ctime and c2 and c2a AND C4 and c4a AND C6 and c6a and abs(CountOfPosition) < MaxPositionsAllowed THEN

SELLSHORT 1 CONTRACT AT MARKET

SET STOP %LOSS 1.1

SET TARGET %PROFIT 1.3

ENDIF

Cumulative orders are not to everyone’s taste

Looks good with CumulateOrders = False.

Also positive on performance on 1m and 3m.

Thank you very much for sharing @nonetheless

Can’t wait for 14:30 to see how it performs on Demo Live! 🙂

I don’t think the VRT can be useful on that amount of trades, so be careful before going live.

I don’t think the VRT can be useful on that amount of trades, so be careful before going live.

I think you’re prob right, but with such a short back test WF wouldn’t tell us much either. It would certainly be discouraging if the VRT were bad. But all short TF systems have to be left on demo for a good few months. Work in progress…

Paul

PaulParticipant

Master

Looks nice nonetheless . Thanks for sharing!

I always have doubts having multiple positions, the way exits are handled are a bit tricky.

If you have xx positions and a new position is openend and a new stop loss is set, the stop loss level for the last position counts for all positions?

That could work positive but also negative in terms of acceptable risk.

Maybe there’s a difference, adding only to a winning position, which means the first positions stop loss is lowered and the risk is reduced.

Same works a bit similar for the trailing stop, but what happens if using instead of trade price(1) position price?

PaulParticipant

Master

here’s the quick change, same ts but using position price and adding to winning positions.

Didn’t optimise stop loss & profit targets.

now I look about it, it using positionperf(0) below, but perhaps better is to look at the positionperf of all current trades in same direction and if that’s positive add a position.

MaxPositionsAllowed = 9999

// Conditions to enter long positions

IF not longonmarket and Ctime and c1 and c1a AND C3 and c3a AND C5 and c5a THEN

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS 1.5

SET TARGET %PROFIT 2.5

elsif longonmarket and Ctime and c1 and c1a AND C3 and c3a AND C5 and c5a and abs(CountOfPosition) < MaxPositionsAllowed THEN

if positionperf(0)*100>0 then

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS 1.5

SET TARGET %PROFIT 2.5

endif

endif

// Conditions to enter short positions

IF not shortonmarket and Ctime and c2 and c2a AND C4 and c4a AND C6 and c6a THEN

SELLSHORT positionsize CONTRACT AT MARKET

SET STOP %LOSS 1.5

SET TARGET %PROFIT 2.5

elsif shortonmarket and Ctime and c2 and c2a AND C4 and c4a AND C6 and c6a and abs(CountOfPosition) < MaxPositionsAllowed THEN

if positionperf(0)*100>0 then

SELLSHORT positionsize CONTRACT AT MARKET

SET STOP %LOSS 1.5

SET TARGET %PROFIT 2.5

endif

endif

PaulParticipant

Master

sorry that was not a good comparison because difference of sl/pt.

new position is openend and a new stop loss is set, the stop loss level for the last position counts for all positions?

Hi Paul, from what I can see in demo, all the stops are different, measured from each entry point.

Only adding to winning positions could be a good idea – i’ll have to play around with it. Of course, then you lose the benefit of averaging down your losing positions. The question is how much you trust the primary trend.

I also tried adding exit conditions, when any of the indicators changed direction, but couldn’t get any improvement. There must be a better way to get out of a losing position without going all the way to the stop… maybe something like the Fibonacci exits you have in your DJ 3m Vectorial – would that bit of code work as it is?

PaulParticipant

Master

Hi Paul, from what I can see in demo, all the stops are different, measured from each entry point.

Hi, then it’s perfect! I wasn’t sure.

about the Fibonacci exits, yes it does add something too it, it appears. That’s nice to see, especially in another market (often it breaks down), but if it’s enough to keep it? I used hour 0 to hour 8 or 9.

Using position price instead of trade price the results go down a bit.

One thing I just noticed, although the stop loss is set individually for each new position, it doesn’t seem to change when the trail moves up. At the moment there are 18 open positions, most of which are up by around .6% but the stop hasn’t moved, even though the trail should go to break even at .38 %

It’s even above the aggregate price by more than that.

Does anyone know how a trailing stop is supposed to work with cumulative orders?

It is probably like in the Forces … follow your last Order 🙂 … so the trail works on the last Order to be executed.

The last Order / trade didn’t reach the Trail Start level?

No, it didn’t but how can it ever if new positions are always being added? It would have to go .38 % without the slightest pullback or it’ll take another trade and start a new trail from there.