Hi @nonetheless,

I was wondering … what version of the DJ do you have live? is that I’m seeing the version DJ-5m-MotherOfDragons-v4.7.2a opens some positions very late or should not. What do you think? thanks

@StingRe, @josef1604, as I’ve explained elsewhere in this v long thread, rather than the typical ‘buy low, sell high’, MoD works on a ‘buy high, sell higher’ basis – ie it will only enter when the run is well established. Backtest shows that 9 times out of 10 there is enough continuation to turn a profit. This does mean however that it can also buy at the very top of a run (or sell short at the bottom) – and when you see that happening it looks colossally dumb, like only a moron would enter there. Obviously there is still room for improvement in this regard, but I have yet to solve it. Personally I’m at the point where I just accept that sometimes it will do dumb things, but in the long term it tends to get it right. Hope that helps.

I am running DJ v5.1 and NAS v4.1 L & S

Thanks @

@nonetheless, for your answer, I have understood perfectly.

Best regards

Paul

PaulParticipant

Master

Thanks for all the work you put into this strategy Nonetheless!

I had a different idea for a robustness check and your strategy is perfect to test it on.

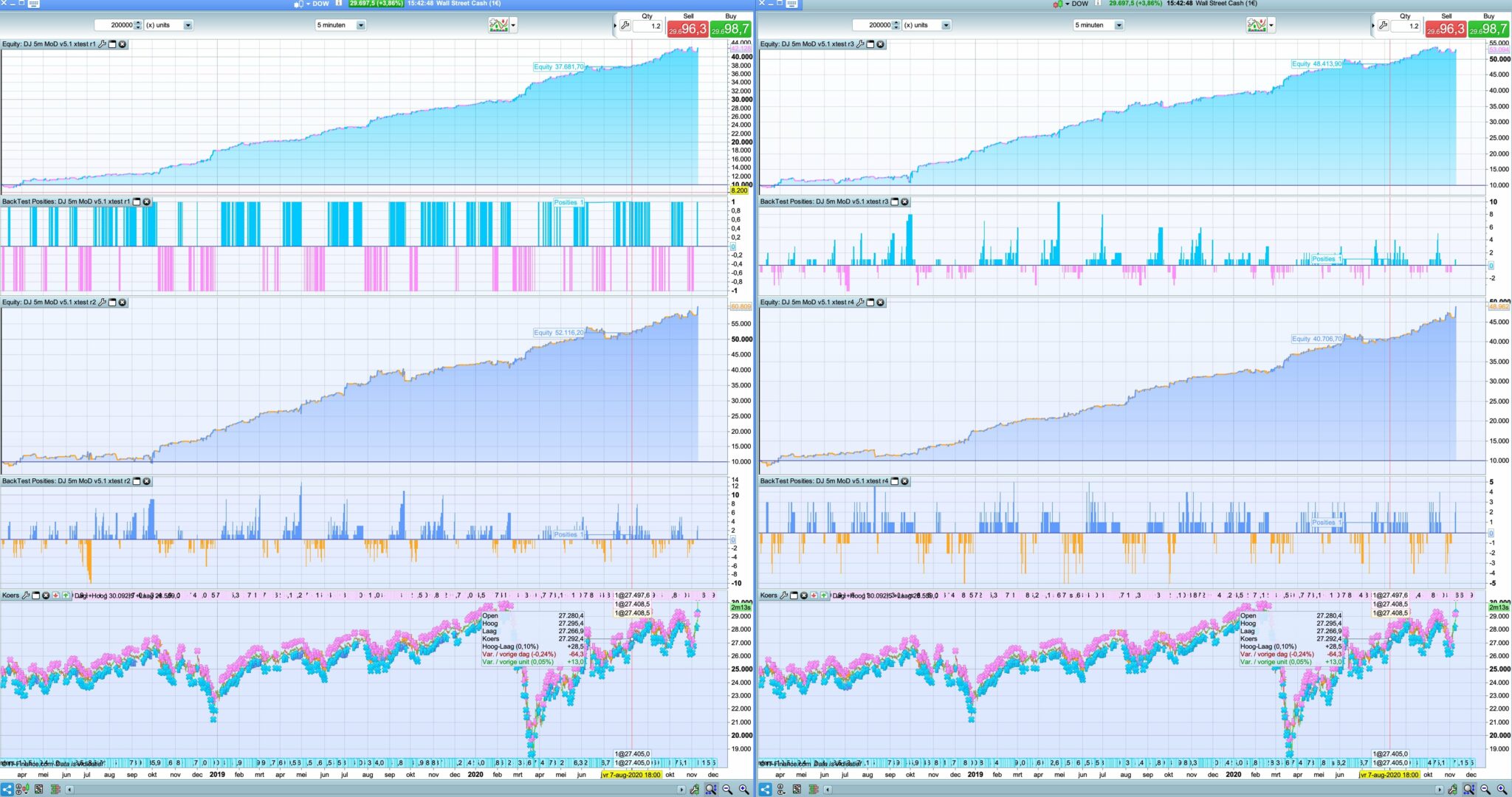

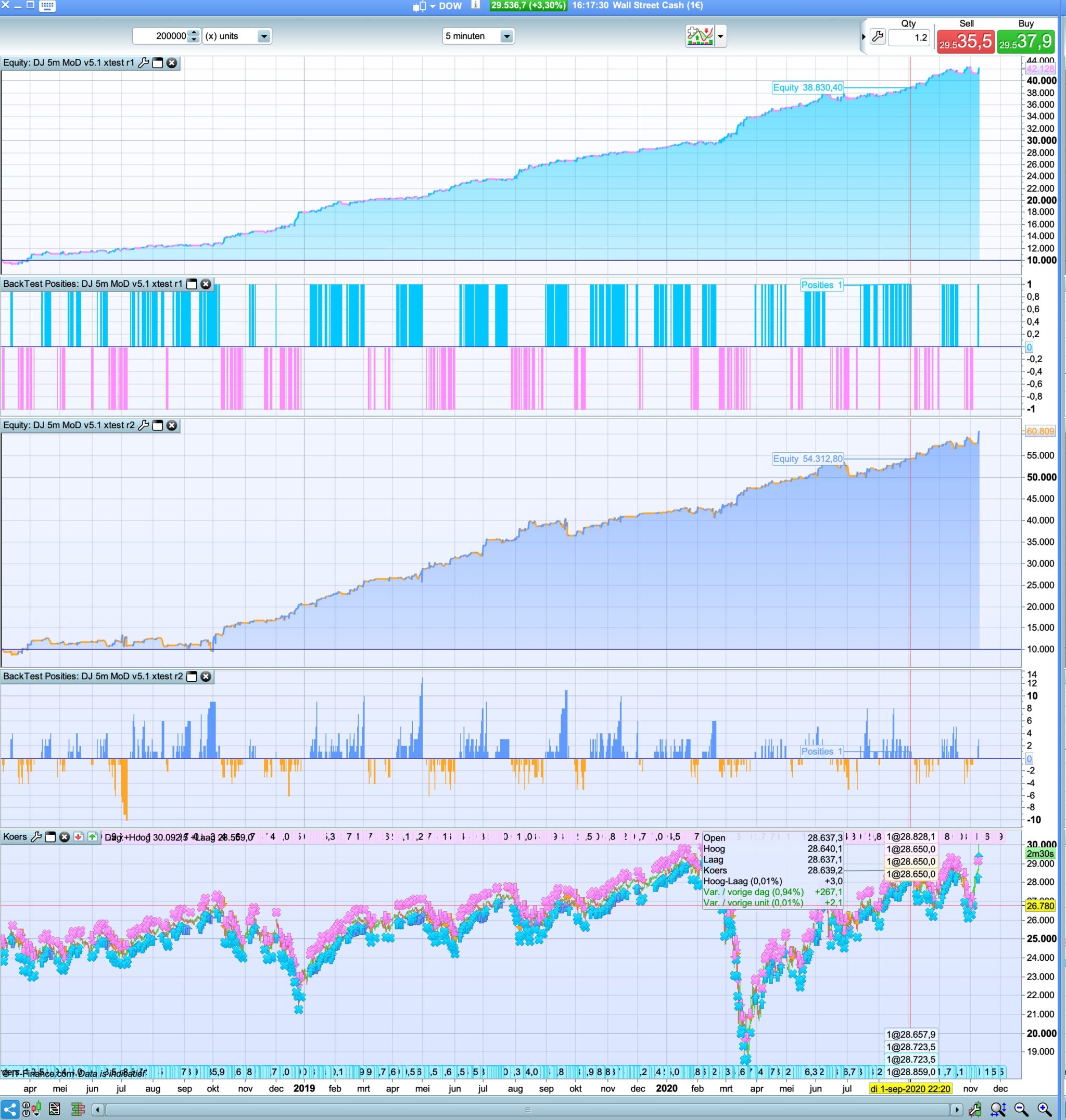

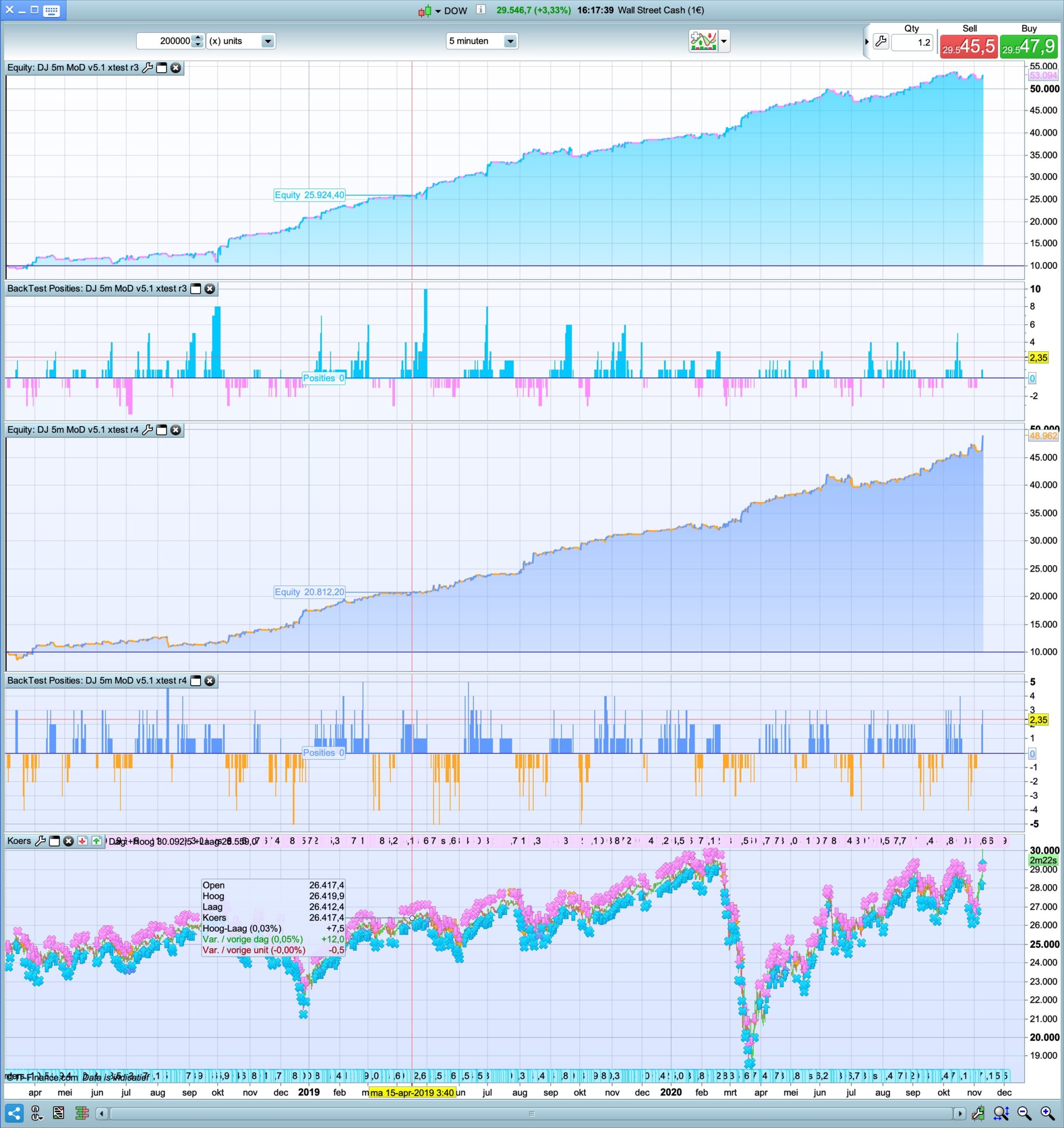

When in a position, you don’t see normally the same signals. To have them reflected in the equitycurve I used cumulative position orders = true.

However the main difference is normally a strategy uses a set ( stoploss )command, tradeprice(1) or positionprice for exits.

Now it’s all based on the first position, so i.e. stoploss exits are the same but coded differently and all other references to above too but that was changed easily.

The purpose is to let the equiycurve intact or improved when acting on all or selective signals but keeping the total countofposition = same signals relatively in low in backtesting & optimising and having more insight on the number of good & bad signals and improve on them.

Additonally I’ve added the reenter when same signals come as default (not using cum.orders), every-time, when losing or when winning.

Here’s a comparision on the code v5.1, I added r.. to reflect below

// reenter [1] (default) no action on same signals until closed

// reenter [2] action on same signals when in position

// reenter [3] action on same signals when position is in loss

// reenter [4] action on same signals when position is in profit

Since the code doesn’t use a hard stoploss command it’s not recommended to use live. Risks are higher i.e. when adding to a winning position all positions have the same exits from the first position, so if it fails completely, all next signals (=new positions) have a higher losses.

Very clever! Reassuring to see that all the re-enter options still give healthy results – thanks for that!

I have just discovered this very long topic, and only one word (or 2) : THANK YOU to all of you.

I am learning so much with this topic

thank you again

thanks for everything simple question though, can one set in the software that it takes smaller contracts? for me it is not possible to choose less than 1.

se code below. for me that tells me that i can set 0.2 contract

MM = 1 // = 0 for optimization

if MM = 0 then

positionsize=1

ENDIF

if MM = 1 then

ONCE startpositionsize = .4

ONCE factor = 10 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE margin = (close*.005) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.01)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 55 // DOW €1 IG first tier margin limit

ONCE maxpositionsize = 550 // DOW €1 IG tier 2 margin limit

ONCE minpositionsize = .2 // enter minimum position allowed

IF Not OnMarket THEN

You should be able to use this:

MM = 1 // = 0 for optimization

if MM = 0 then

positionsize=1

ENDIF

if MM = 1 then

ONCE startpositionsize = .2

ONCE factor = 10 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE margin = (close*.05) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.05)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 55 // DOW €1 IG first tier margin limit

ONCE maxpositionsize = 550 // DOW €1 IG tier 2 margin limit

ONCE minpositionsize = .2 // enter minimum position allowed

IF Not OnMarket THEN

In the UK the minimum position on the DJ is 0.2 but you need to check what that is in Sweden. If it’s 1 then you have to put that for startpositionsize and minpositionsize (startpositionsize can of course be higher). I have also changed the margin leverage but you have to check that too (probably 5%).

ty alot! now i can go from demo to live with 0.2 contract. feels good! 🙂

This does mean however that it can also buy at the very top of a run

As we have this exact situation right now, here’s one way of dealing with it:

Yesterday DJ v5.1 opened a long position at 29988, just 100 points away from the all-time high. As this trade seemed likely to fail, when it started going south I manually opened a hedge for the same amount. These are presently both still open. The short has a breakeven stop and a limit equal to the stop on the long position. So if it does turn around and make good, the short will close for no loss. But if, as I expect, it falls all the way to the stop then the short will cover the cost. It’s a way of letting the algo run it’s course while having an insurance policy against likely failures.

I’m sure that most people already know this trick, but for anyone who doesn’t …

This does mean however that it can also buy at the very top of a run

As we have this exact situation right now, here’s one way of dealing with it:

Yesterday DJ v5.1 opened a long position at 29988, just 100 points away from the all-time high. As this trade seemed likely to fail, when it started going south I manually opened a hedge for the same amount. These are presently both still open. The short has a breakeven stop and a limit equal to the stop on the long position. So if it does turn around and make good, the short will close for no loss. But if, as I expect, it falls all the way to the stop then the short will cover the cost. It’s a way of letting the algo run it’s course while having an insurance policy against likely failures.

I’m sure that most people already know this trick, but for anyone who doesn’t …

Too late for me…. i am waiting for the conclusion of this trade….

This does mean however that it can also buy at the very top of a run

As we have this exact situation right now, here’s one way of dealing with it:

Yesterday DJ v5.1 opened a long position at 29988, just 100 points away from the all-time high. As this trade seemed likely to fail, when it started going south I manually opened a hedge for the same amount. These are presently both still open. The short has a breakeven stop and a limit equal to the stop on the long position. So if it does turn around and make good, the short will close for no loss. But if, as I expect, it falls all the way to the stop then the short will cover the cost. It’s a way of letting the algo run it’s course while having an insurance policy against likely failures.

I’m sure that most people already know this trick, but for anyone who doesn’t …

Too late for me…. i am waiting for the conclusion of this trade….

Same for me, it’s now closed… I hope the next trades will be better.

Thanks again to all the contributors on this amazing topic.

Anyone running the NAS 5m MoD v4.1 S here ? I launched it without MM (MM=0 & positionsize=1), and it took a position on Nov 3rd, at 06:00:00 UTC, which hit stoploss at 15:15:27 UTC. However, this doesn’t appear in the backtest.

I reached PRT out, and I am now waiting for their answer.

I read that @BobOgden had a similar issue a few days ago with the DJ version.

Regarding this issue I mentioned a few days ago, PRT investigated and told me it was due to a problem related to MTF synchronization. They will try to fix it within the next few weeks.

Hi, i’ve only just recently found this message string and i have to say its a fantastic system. Thank you for sharing this. Can you tell me the timezone that these work on please?

Can you tell me the timezone that these work on please?

You can run it straight out of the box on UK time. If you want to use MM be sure to double check what leverage you get (prob 5%) and change these lines to 0.05

ONCE margin = (close*.005) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.01)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage