I also have it live with the sqme issue as you. can be explained by so many reasons such as: spread in live vs spread in backtest, execution from IG in live. lets see whats PRT says about it

Thanks again to all the contributors on this amazing topic.

Anyone running the NAS 5m MoD v4.1 S here ? I launched it without MM (MM=0 & positionsize=1), and it took a position on Nov 3rd, at 06:00:00 UTC, which hit stoploss at 15:15:27 UTC. However, this doesn’t appear in the backtest.

I reached PRT out, and I am now waiting for their answer.

I read that @BobOgden had a similar issue a few days ago with the DJ version.

I also have it live with the same issue as you. can be explained by so many reasons such as: spread in live vs spread in backtest, execution from IG in live. lets see whats PRT says about it

@April O’Neil, that looks promising. How much result is OOS? or is it optimized on 100% of data?

Hi again @nonetheless,, thank you for answering.

So do you recognize the phenomenon, that after optimizing high tf conditions, adding the m5-tf conditions will actually make the total gain less?

And do you have any thoughts about running this code with only h2 & m15/m30 conditions but executed on tf 5?

adding the m5-tf conditions will actually make the total gain less

not sure what you mean. You get a better result running it on 15m TF without the 5m conditions? if so, i’d like to see the backtest.

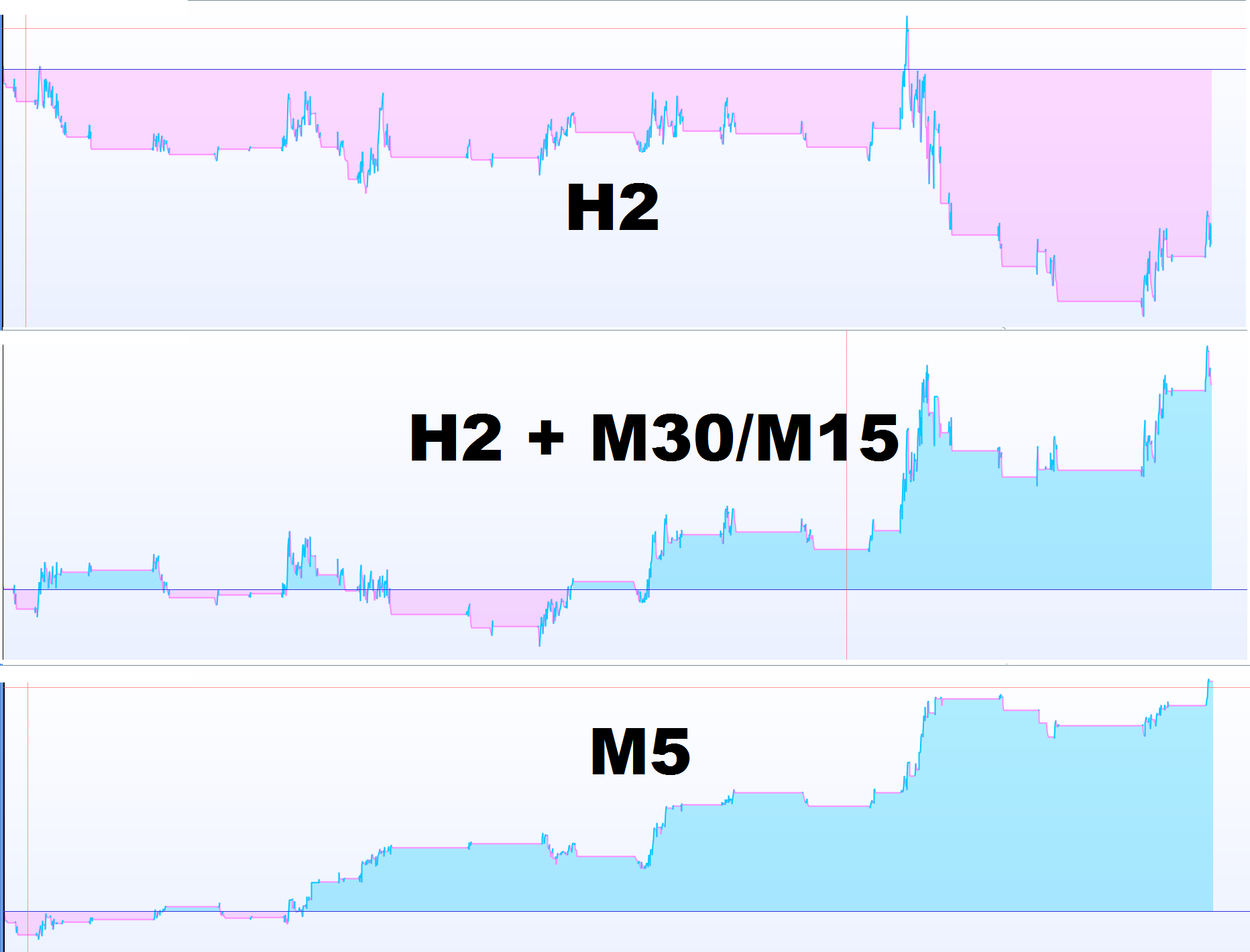

Ok @nonetheless, so in the attached image you see two different attempts to build a MoD Long for DAX.

Both of these have only been optimzed for H2 and M30+M15 Timeframes so far.

The first one(the one on top) I tried to optimize for high WF and many trades (85.37% winrate, 369 trades)

The second one(the on the bottom) I tried to optimize for highest possible gain (Only 138 trades).

So I have optimized these two from the top down, so the next step now is to optimize the conditions for the M5 timeframe.

I use the differrent code bits shown below, but whatever values i optimize for variables “l, m, n, o, k, j” the results are not getting any better.

I can’t make the M5 conditions to enhance the performance: For the first example I can make small improvements to the gain/wf/pf but just slightly.

When I’m looking at the different versions that you have made, I see that the M5-conditions is the most significant for the performance of the algo. i.e. when I strip the M5-condititions from your versions the backtests often looks bad (similar to what you see in the second attached image).

I’m thinking I’m doing the process wrong. After optimizing the 4 entry conditions of H2 and the 3 entry conditions for M15/M30 I rarely can make the algo any better with the M5 conditions. Scratching my head here.

M5 conditions used:

lengthRSIa = l //RSI period

lengthStocha = m //Stochastic period

smoothKa = n //Smooth signal of stochastic RSI

smoothDa = o //Smooth signal of smoothed stochastic RSI

myRSIa = RSI[lengthRSIa](close)

MinRSIa = lowest[lengthStocha](myrsia)

MaxRSIa = highest[lengthStocha](myrsia)

StochRSIa = (myRSIa-MinRSIa) / (MaxRSIa-MinRSIa)

Ka = average[smoothKa](stochrsia)*100

Da = average[smoothDa](Ka)

c23 = Ka>Da

c24 = Ka<Da

ma3 = average[k,3](typicalPrice)

c21 = ma3 > ma3[1]

c22 = ma3 < ma3[1]

Periodb= j

innerb = 2*weightedaverage[round( Periodb/2)](typicalprice)-weightedaverage[Periodb](typicalprice)

HULLb = weightedaverage[round(sqrt(Periodb))](innerb)

c5 = HULLb > HULLb[1]and HULLb[1]<HULLb[2]

c6 = HULLb < HULLb[1]and HULLb[1]>HULLb[2]

When you optimize the longer TFs, what values do you have in the 5m TF?

Also, are you using WF or 100% of data?

When you optimize the longer TFs, what values do you have in the 5m TF?

Also, are you using WF or 100% of data?

When I optimize the longer TFs I have removed the M5 timeframe completely. Should one have some kind of default / unoptimized starting values on M5 (and on M15) when optimizing H2. If yes, what should that starting values be?

In this example I use 80%/20% like you.

Yes, you have to have something entered for all the indicators as they act as a whole, each one reacting to other changes. For DAX long you can use NAS long as a template and start with those values. Or you can use ballpark figures like sl =1, tp =2

the default for StochasticRSI is 14, 14, 10, 3 (although it never ends up that way)

You’ll have to go through them all at least 3 times as by the time you get to the bottom, the ones at the top will need changing – it takes days!

Yes, you have to have something entered for all the indicators as they act as a whole, each one reacting to other changes. For DAX long you can use NAS long as a template and start with those values. Or you can use ballpark figures like sl =1, tp =2

the default for StochasticRSI is 14, 14, 10, 3 (although it never ends up that way)

You’ll have to go through them all at least 3 times as by the time you get to the bottom, the ones at the top will need changing – it takes days!

Thank you @nontheless. That kind of explains it, I will use those start values and let you know my results. Cheers!

@April O’Neil, that looks promising. How much result is OOS? or is it optimized on 100% of data?

I optimised with 100% of data. Basically, for a known stratgy with variables previously validated , the more data you got the better it is. The purpose was mainly to validate the process of construction. Wich is sucessfull, i obtened sometheing very similar with the v2.2 and i fell on very similar variables. I put Dax v3 in demo for the next month.

Swetraders, i think the problem is your start, did you start with natural exits conditions ? At the begin you should have c1 to c7. This is your core strategy. Use a large TP, small SL (like 1.5) and a basic TS (0.3).

By the way nonetheless , do you use this Money management in live with Margin = (close*.005 ) and margin2 = (close*.01) ? Very agressive.

My IG account is in Switzerland and that is the leverage they offer. This varies from country to country and you need to alter those decimals to reflect whatever leverage you get. In the UK it would be .05 for tier 1 and tier 2, possibly also in France.

If you want less aggressive MM just increase the Factor – whatever you feel comfortable with!

@April O’Neil Yes you are right. @nonetheless What would you say is the minimum number of trades you want to see to start the strategy in demo? 250+ or even more?

minimum number of trades

Not something I’ve ever thought about. I’d be more concerned with the win% – number of trades just is what it is.

Hi @nonetheless,

I’ve noticed in all the strategies that there are about 5-10 trades that have an MFE of 0$. Meaning the trade went red as soon as it was opened.

I’m wondering if there was a way to potentially mitigate these by placing limit / stop orders a few points out from where the daily high / low entry criteria activate.

I understand you would likely miss a few points on trades that ended up being winners but it might keep you out of the MFE 0’s.

I’ve tried to come up with a way to test this in the conditions for long / shot but haven’t had any luck.

Interested in your thoughts or if you’ve tried something similar.

Cheers,