ALE

ALEModerator

Master

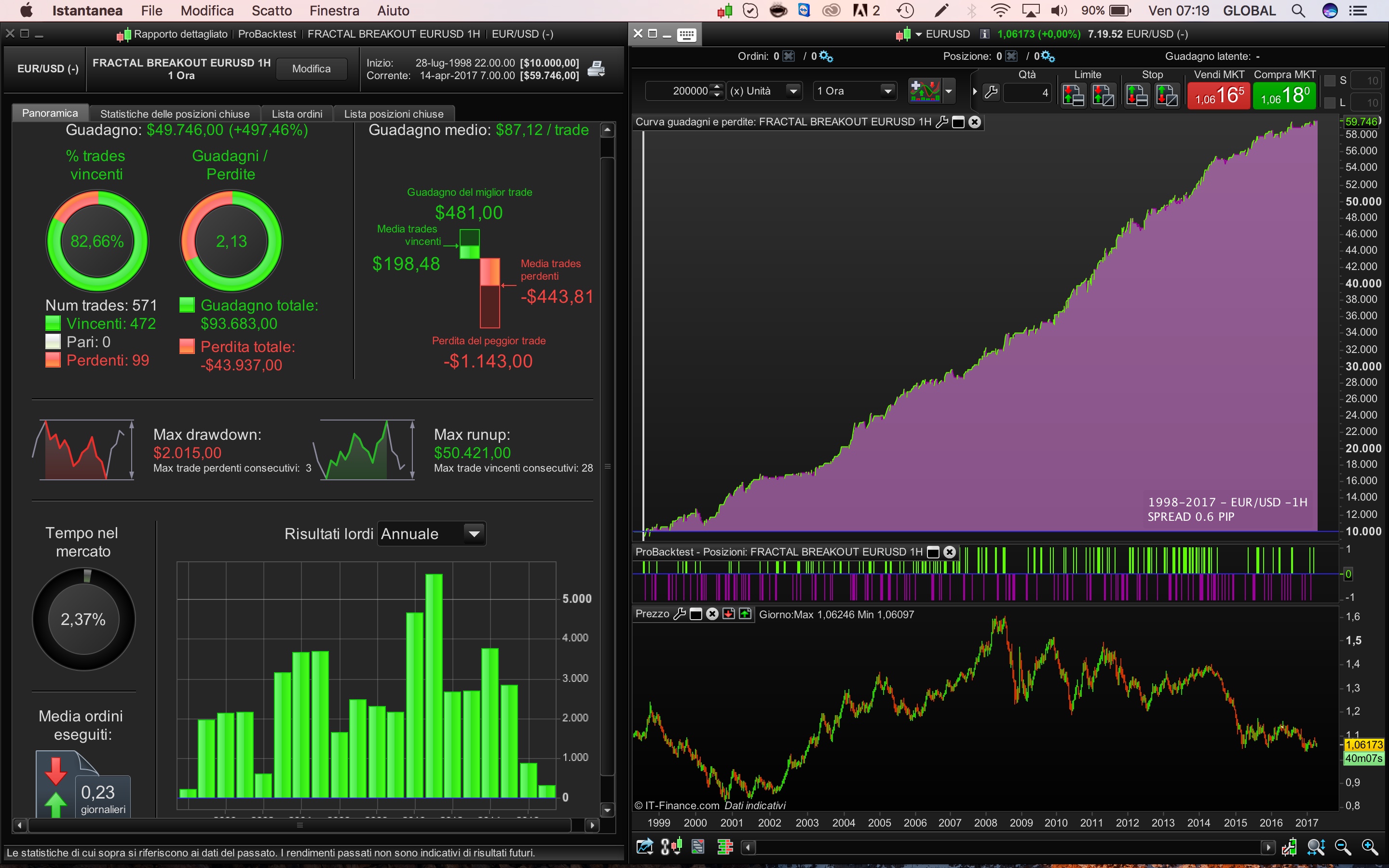

Hello guys We can discuss about the strategy here, we can help together to develop the strategy . This is the strategy posted in the Library there : https://www.prorealcode.com/prorealtime-trading-strategies/fractal-breakout-intraday-strategy-eurusd-1h/ Below you can find 3 screenshot with explanation of the stop, and levels used in this strategy.

// EURUSD(-) - IG MARKET

// TIME FRAME 1H

// PROBACKTEST TICK by TICK - 200.000 bars

// SPREAD 0.6 PIP

// ALE

DEFPARAM CumulateOrders = false

///BILL WILLIAM FRACTAL INDICATOR

//CP=PERIOD

CP=113

if close[cp] >= highest[2*cp+1](close) then

LH = 1

else

LH=0

endif

if close[cp] <= lowest[2*cp+1](close) then

LL= -1

else

LL=0

endif

if LH=1 then

HIL = close[cp]

endif

if LL = -1 then

LOL=close[cp]

endif

//LONG and SHORT CONDITIONS

Positionsize=1

if (time >=100000 and time < 230000) then

C1 = (close CROSSES OVER HIL)

D1 = (close CROSSES UNDER LOL)

IF c1 and not shortonmarket THEN

BUY positionsize CONTRACT AT MARKET

ENDIF

IF D1 and not longonmarket THEN

SELLSHORT positionsize CONTRACT AT MARKET

ENDIF

ENDIF

//TRAILING STOP

TGL =5

TGS=5

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

// DONCHIAN STOP

DC=20

e= Highest[DC](high)

f=Lowest[DC](low)

if longonmarket then

laststop = f[1]

endif

if shortonmarket then

laststop = e[1]

endif

if onmarket then

sell at laststop stop

exitshort at laststop stop

endif

set target pprofit 30

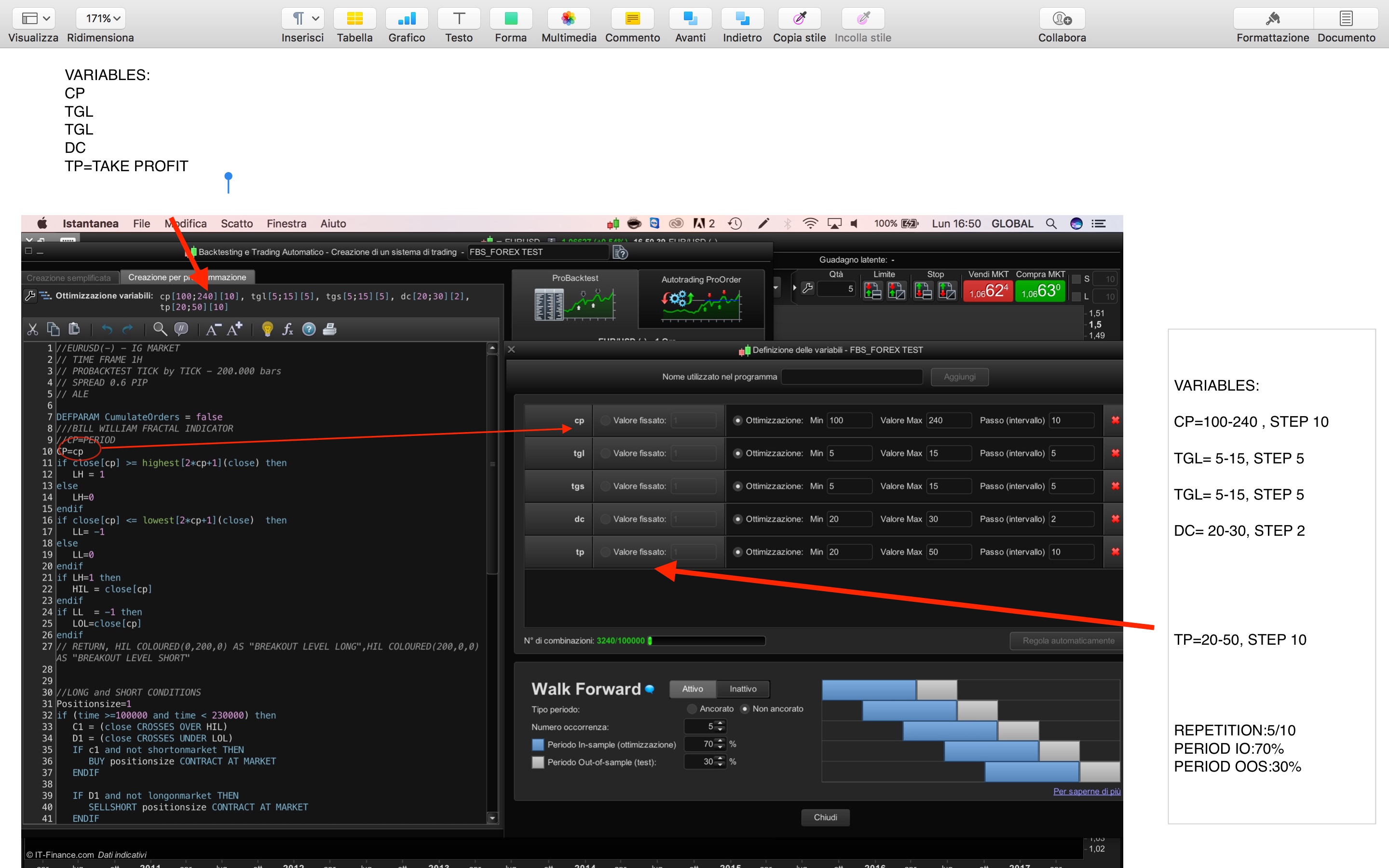

This trading sistem can be used with other currency pairs. To find the values of variables suitable for other currency pairs, you must use WF, to avoid an overfitted values: if the WF will be done on bars 200,000 may be divided into two halves, the first test will be carried out with a large range value starting with the value in the attached picture below, the second test will have a range around the variables choices during the first test. IN THE LAST YEAR THE OPTIMIZATION OF TRAILING STOP SUGGEST THIS VALUE: TGL=9 TGS=10 … THIS MEAN ABOUT 10 PIP FOR BOTH

ALEModerator

Master

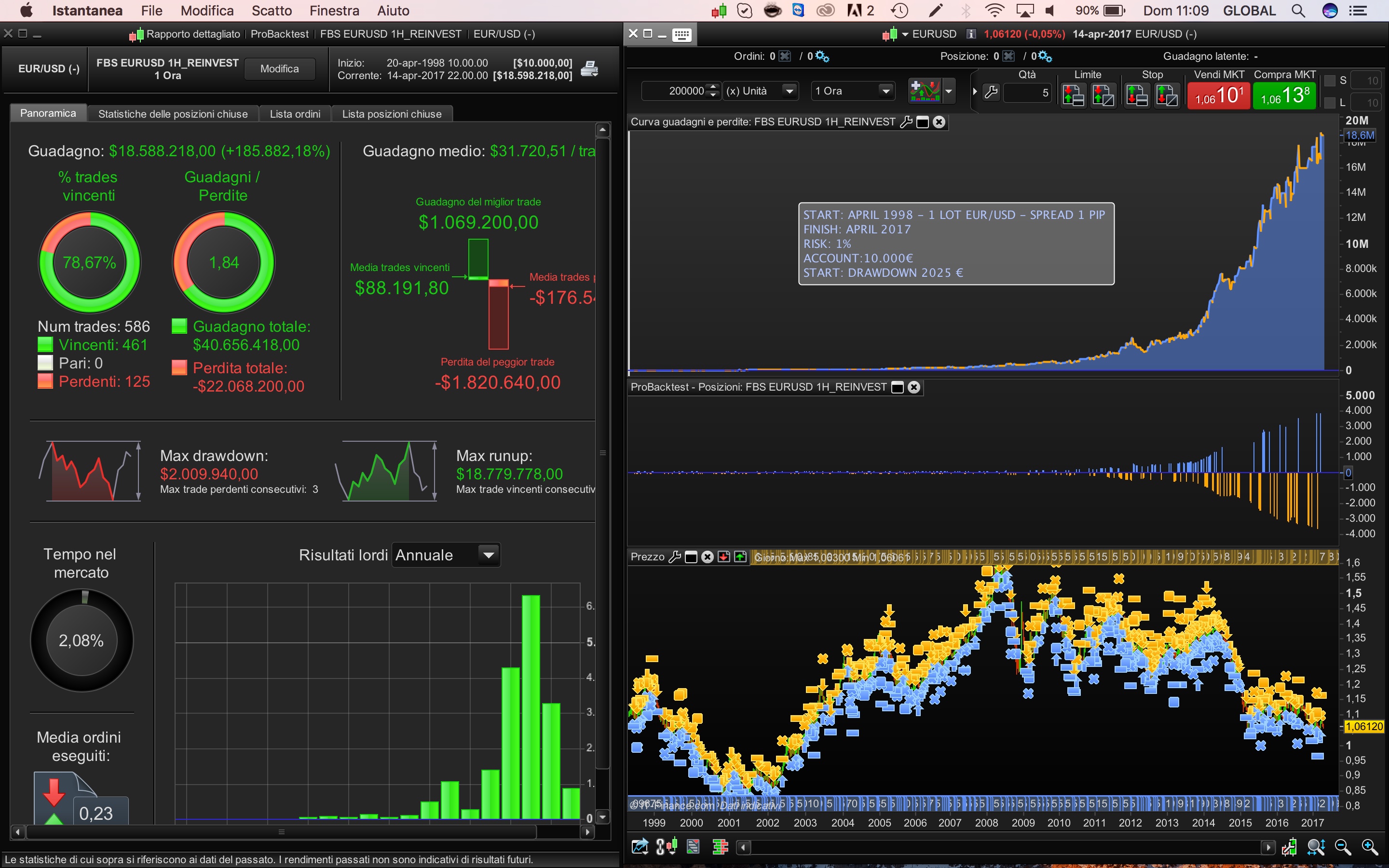

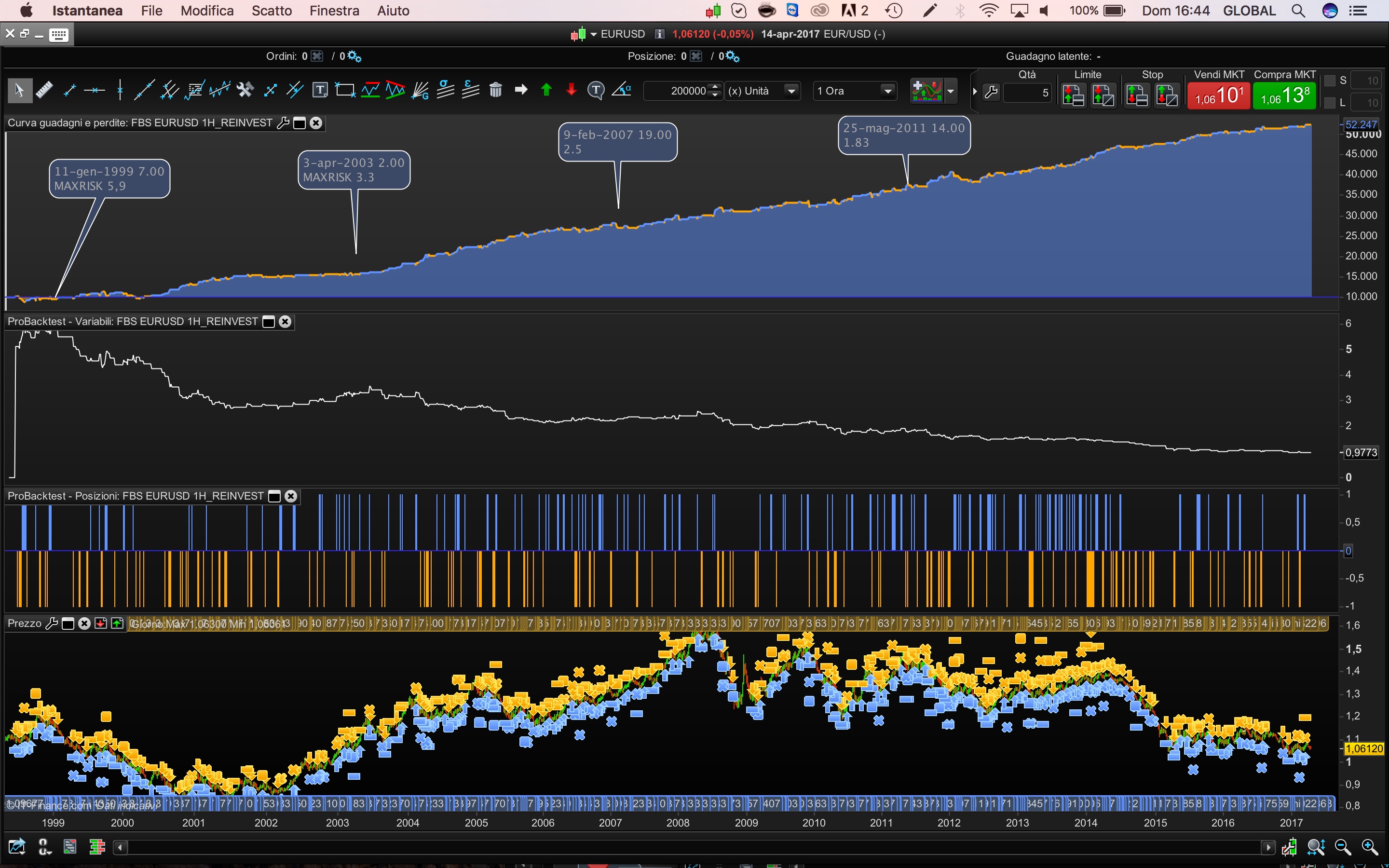

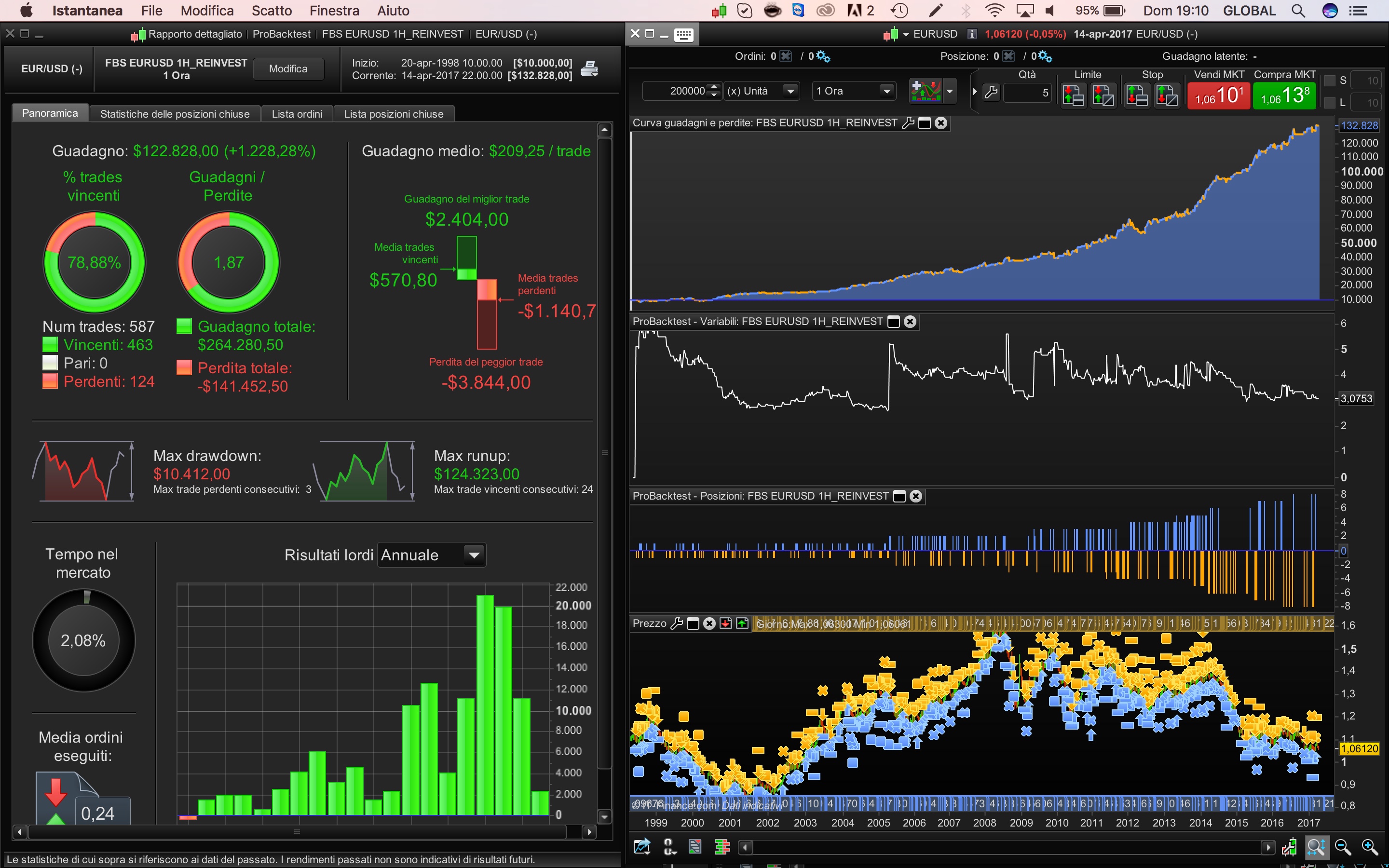

This the reinvestment version of Kasper, in his example him stressed the strategy with 5000 lots:

//EURUSD(-) - IG MARKET

// TIME FRAME 1H

// PROBACKTEST TICK by TICK - 200.000 bars

// SPREAD 0.6 PIP

// ALE - KASPER

DEFPARAM CumulateOrders = false

//KASPER CODE OF REINVESTMENT

Reinvest=1

if reinvest then

Capital = 10000

Risk = 1//0.1//in % pr position

StopLoss = 48

REM Calculate contracts

equity = Capital + StrategyProfit

maxrisk = round(equity*(Risk/100))

MAXpositionsize=5000

MINpositionsize=1

Positionsize= MAX(MINpositionsize,MIN(MAXpositionsize,abs(round((maxrisk/StopLoss)))))//*Pointsize))))

else

Positionsize=1

StopLoss = 48

Endif

///BILL WILLIAM FRACTAL INDICATOR

//CP=PERIOD

CP=113

if close[cp] >= highest[2*cp+1](close) then

LH = 1

else

LH=0

endif

if close[cp] <= lowest[2*cp+1](close) then

LL= -1

else

LL=0

endif

if LH=1 then

HIL = close[cp]

endif

if LL = -1 then

LOL=close[cp]

endif

// RETURN, HIL COLOURED(0,200,0) AS "BREAKOUT LEVEL LONG",HIL COLOURED(200,0,0) AS "BREAKOUT LEVEL SHORT"

//LONG and SHORT CONDITIONS

//Positionsize=1

if (time >=100000 and time < 230000) then

C1 = (close CROSSES OVER HIL)

D1 = (close CROSSES UNDER LOL)

IF c1 and not shortonmarket THEN

BUY positionsize CONTRACT AT MARKET

ENDIF

IF D1 and not longonmarket THEN

SELLSHORT positionsize CONTRACT AT MARKET

ENDIF

ENDIF

//TRAILING STOP

TGL =5

TGS=5

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

// DONCHIAN STOP

DC=20

e= Highest[DC](high)

f=Lowest[DC](low)

if longonmarket then

laststop = f[1]

endif

if shortonmarket then

laststop = e[1]

endif

if onmarket then

sell at laststop stop

exitshort at laststop stop

endif

set target pprofit 30

set stop loss stoploss*pointsize

@kasper could you comment it?

Great idea Ale 🙂 how does the stoploss 48 do in the 200000 units and walk forward?

edit: I see you already did it :). Ill take a look later when on the pc

cheers Kasper

Eric

EricParticipant

Master

tick by tick backtest? trailingstop 5?

tick by tick backtest? trailingstop 5?

This is the

MFE trailing stop, exit levels are only update once per bar at each calculation.

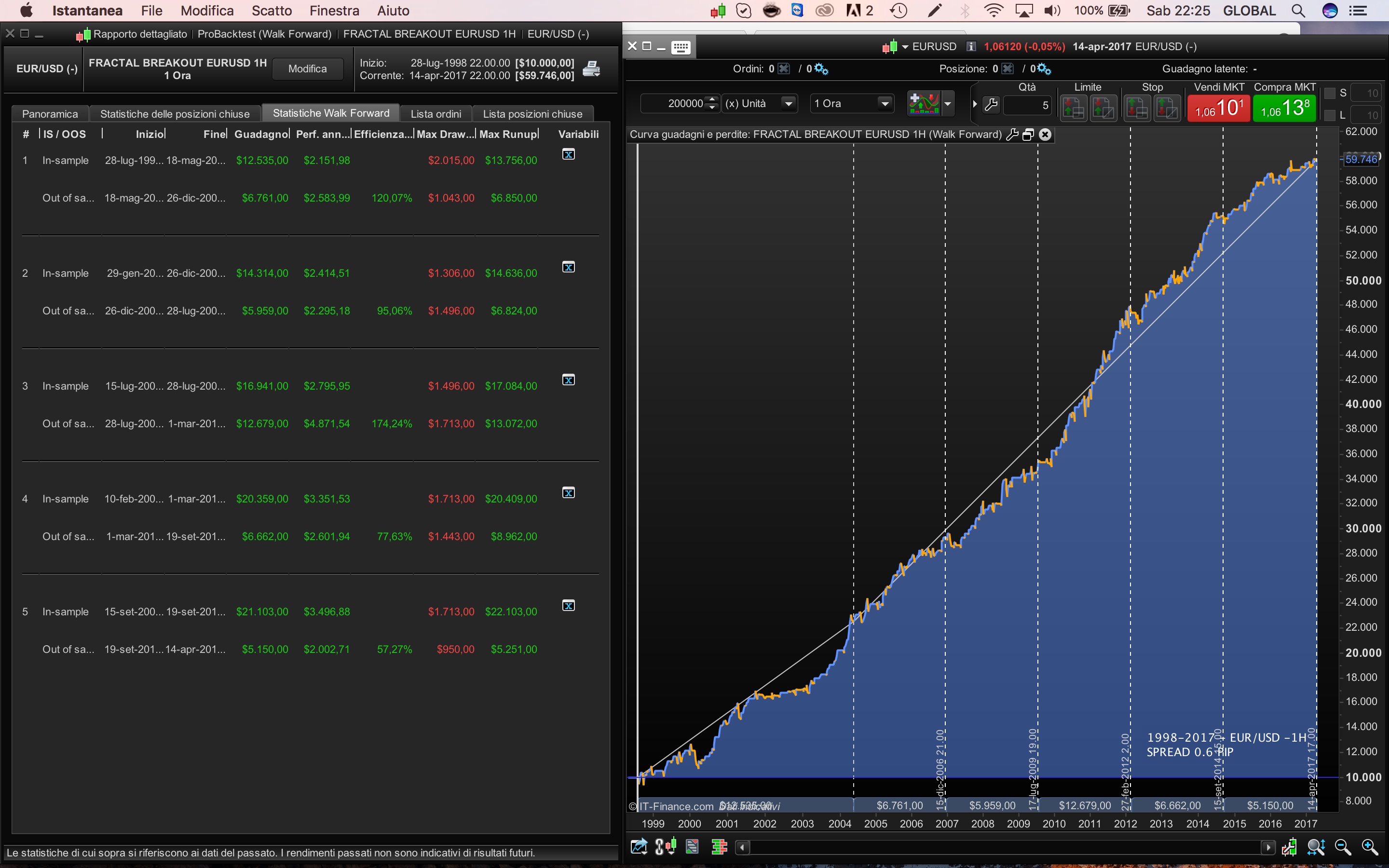

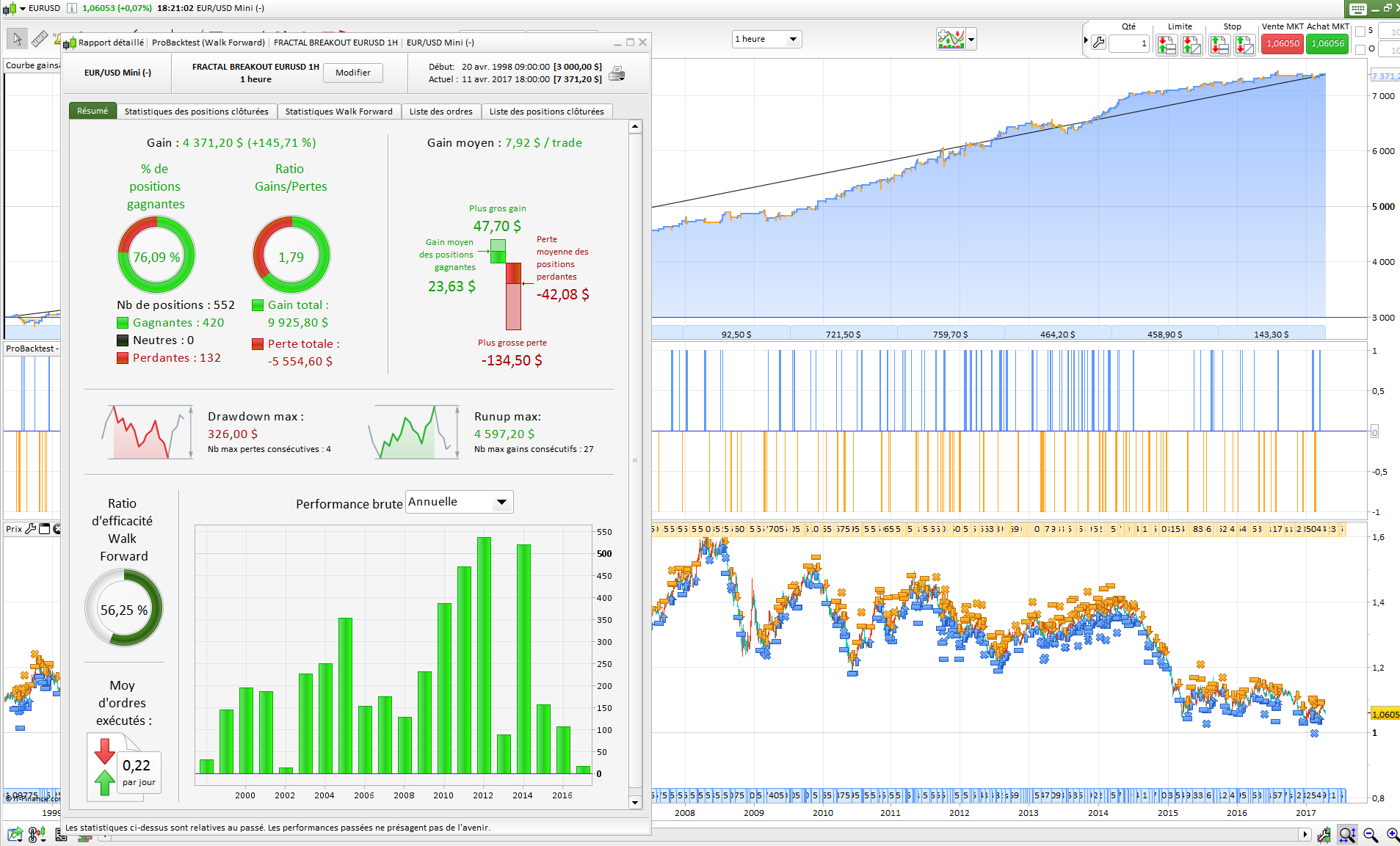

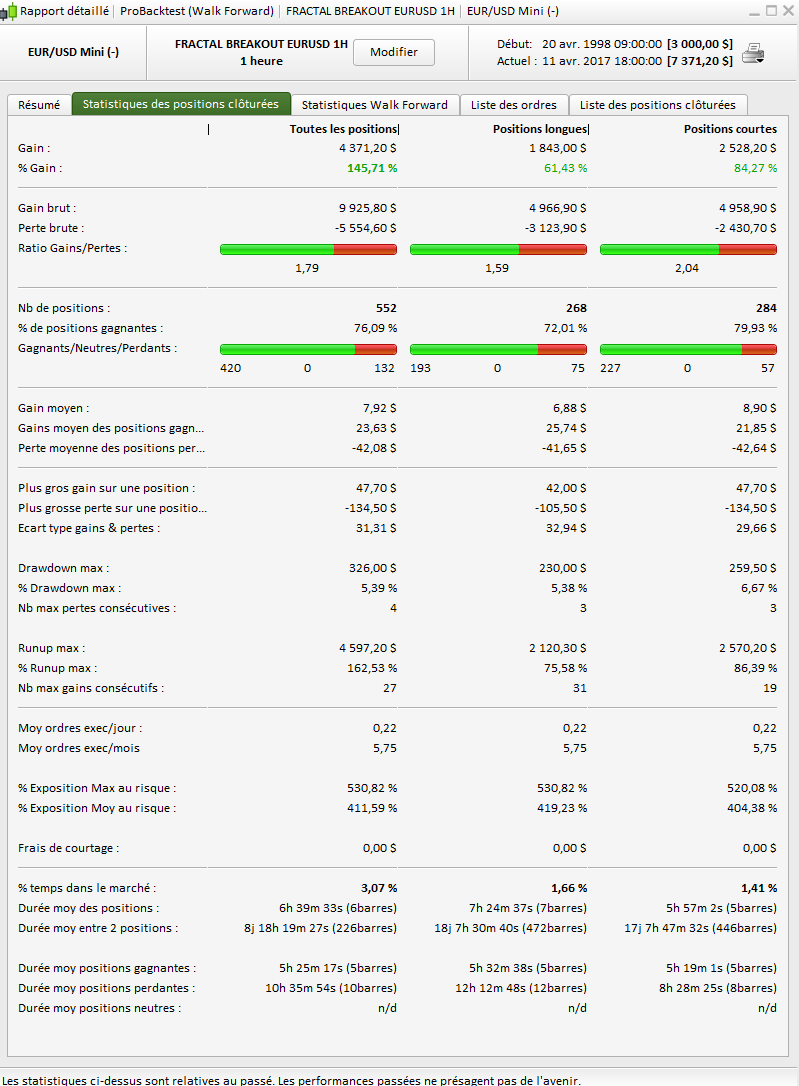

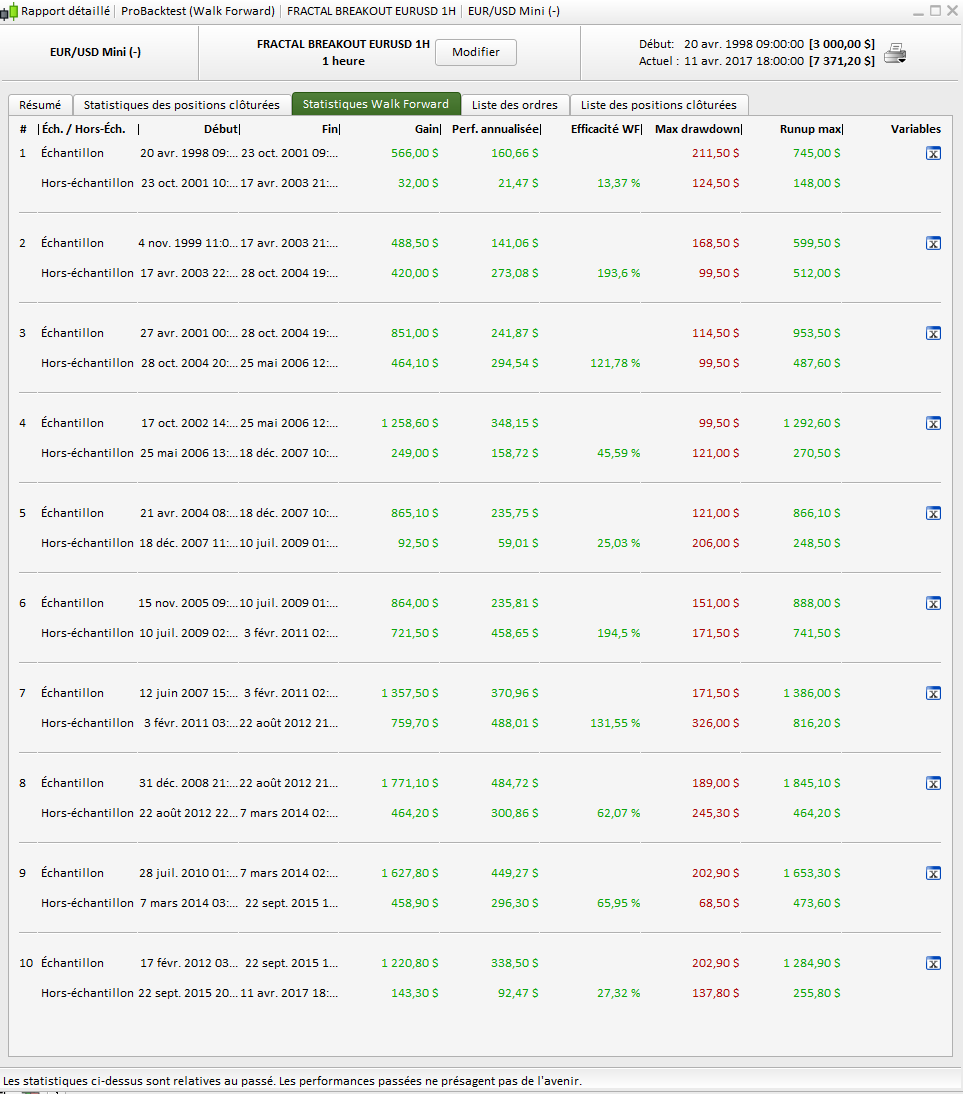

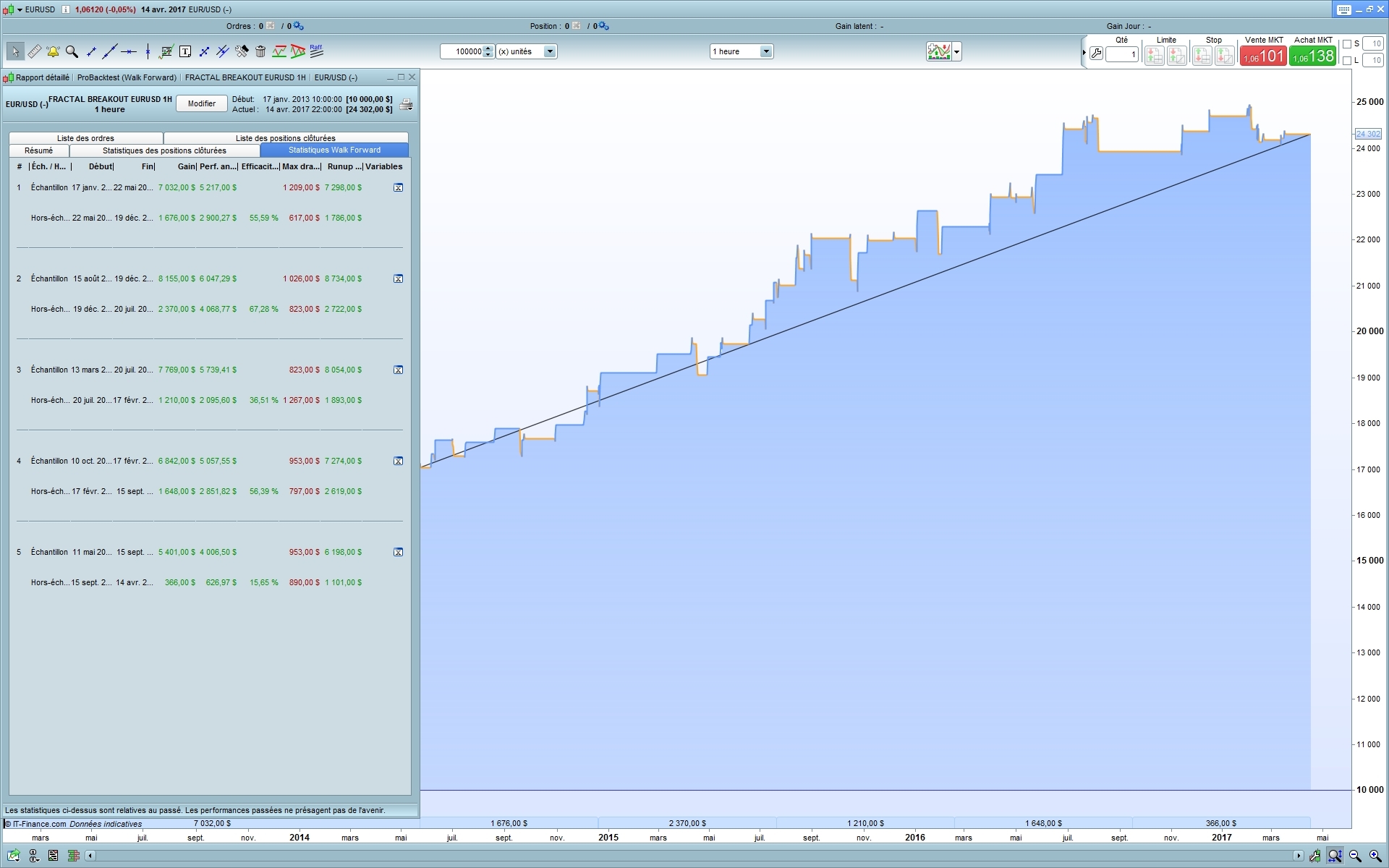

Please find attached the pictures of my own WF test with the first version of the strategy (200.000 bars, ticks mode, 1 point spread) over 10 Out Of Sample iterations.

I think that to suit the strategy for over forex pairs, the best solution would be to enlarge the fractals period (‘cp’ variable) minimum and maximum for the optimisation. That would adapt the high/low fractals for each pair behaviour. Since WF optimisation take ages, I encourage anyone willing to help to test if this rough idea could be relevant and to continue explore other possibilities of improvements. Thanks.

@Nicolas,

Do you erase of my WF test and the picture ?

Hi Ale, that is just crazy numbers 🙂 I don’t have the premium version- but for 1 H data back to 1999, that is a valid test. I would like to help optimize but the data I have is only back to Jan. 2013

Please add this Graph code- to see how much you are risking at each trade.

graph (((tradeprice-(tradeprice-((tradeprice*stoploss)/100)))*positionsize*pointvalue*100)/(equity))*100 COLOURED(0,0,0) AS "MAXRISK"

@zilliq yes sorry, please repost it here.

ALEModerator

Master

Hi Kasper

I’ve attached pic with maxrisk curve and some value along the curve

Thanks Ale. if you use in the reinvestment code, it should very soon stabilize around 1% risk

No problem Nicolas

I do a WF on 100 000 bars and the WF ratio was 36 % and 3 of 5 periods were >50 %

I did a try by replacing TGL and TGS by a coefficient of averagetruerange, but the results was not good 🙁

ALEModerator

Master

@ Zilliq what do you mean?

ALEModerator

Master

@KASPER

This is results with 1 lot and risk 0.3

@ALE Zilliq tried to use a dynamic step instead of a fixed one with the help of ATR.

Did someone tried to optimize with another pair already?