@Nicolas, yes that was my meening. Code and opti numbers are from first page.

@Ale, can you take a fast look so theres no missunderstanding.

Regards

Henrik

Noticed that opti number for tp step was wrong, my mistake, here is new code.

ALE

ALEModerator

Master

@Kasper and Henrik

unfortunately Brent historical data with 200.000 bars start 3-agu-2015.

Remember that we can test other currencies/indices/commodities/etc.. with different trading hour not only 10000 to 230000 like EURUSD, and we can search others with different time frame. The research will be very long. Before to start research, we may establish which market could be more profitable.

We must consider this feature:

- Spread

- Minimum distance of stop loss (it should be available very close, or in some cases, might be rejected because Donchian stop loss level is variable)

- Historical data available (es: Brent it’s too short).

I Prepare a list of commodities, currencies etc .. with good features

if you think of any possible problem, talk about it so we try to resolve it.

Thanks All!

ALEModerator

Master

HI

If someone want to test more market I’ve attached file with a list.

Thank a lot

Hi,

Thank you for a nice piece of code ALE.

I ran Henrik’s FBI OPTI code on AUD/USD (WF 5/70/30) overnight. I did a pdf of the results but file’s too big to attach so I created a GoogleDrive folder for sharing. Also I’m thinking it would be nice to keep results in one place for practical purposes, so if you guys test on other markets/with different settings and so on, feel free to add content to the GoogleDrive-folder. It should be accessible to anyone using https://drive.google.com/open?id=0B6gmkKnnn7-gREJWYVpMWk9scWs

Page 3 in the pdf has comments containing the variables for each sample, you might need to download the pdf to read them though…

Interestingly the hitrate and gain from short trades were far superior to thise of long trades in this case.

Cheers!

Hi Tedvin. just a suggestion- a freeware such as Lightshoot for capturing screenshoots works very good for this site 🙂

Cheers Kasper

@Elsborgtrading, that’s right, I’m using it myself! 🙂 http://app.prntscr.com/en/index.html

Launched an optimisation on NZDUSD this morning and suddenly get an error from the platform. I’m trying to do it again now..

Hi @ALE this code looks really good!

I am playing around with the reinvestment snippet of it and I am just wondering what is your reason for choosing 48 as the stop loss value? Is that based on an optimisation?

ALEModerator

Master

Hi @ kg6450

In the original version, stop loss is dinamic. Eilsborgtrading make another version with a money management part code. We have seen that 48 stop loss fixed work well.

Hi KG6450- yes I added the stoploss 48. both on the comments by ALE as this was one parameters that also worked very well above 40(I think it was)

By defining a SL we know how much we are risking and there for can calculate our risk and MM. Also when define SL this becomes one of the strategies on the site that has a defined RR above 1- not many of those. RR is actually the magic number 1.6

Nicolas wrote about positionsizing was not limited by the wholes of 1 any more, so we can change the MM code. It does not yield as much as the other, but we are now in total control of our risk. it is precise 1% now- when balanced.

Reinvest=1

if reinvest then

Capital = 5000

Risk = 1//0.1//in % pr position

StopLoss = 48//7//10 // Could be our variable X

REM Calculate contracts

equity = Capital + StrategyProfit

maxrisk = (equity*(Risk/100))

MAXpositionsize=5000

MINpositionsize=1

Positionsize= MAX(MINpositionsize,MIN(MAXpositionsize,abs(((maxrisk/StopLoss)))))//*Pointsize))))

else

Positionsize=1

StopLoss = 48

Endif

graph abs(((Positionsize*stoploss)/equity)*100) COLOURED(0,0,0) AS "MAXRISK"

Would it make sense to WF optimize with pairs of two variables at a time- sort of narrowing it down to see if the instrument is profitable- before making the big WF run with optimizing all variables?

I think it could save a lot of time and I could start on this for some instrument in the list on the 100000 units version- posting the findings- picking potential winners and the people with the 200000 version could run the time consuming WF?

Cheers Kasper

Sounds like a good plan Kasper! I got 200k so just tell me and im ready!

Henrik

ALEModerator

Master

@Elsborg@all

Yes we must avoid to start big WF, we have seen that it became very long test, and may be that we became inefficent.

I’ve make a list to choose the contract with low spread and a close stop if it is necessary for trailing stop. We must consider also volatility to avoid contract with little move. (Nicolas has attached file in page 2 with all currencies volatility range)

I’m preferring commodities to start research to diversify my portfolio.

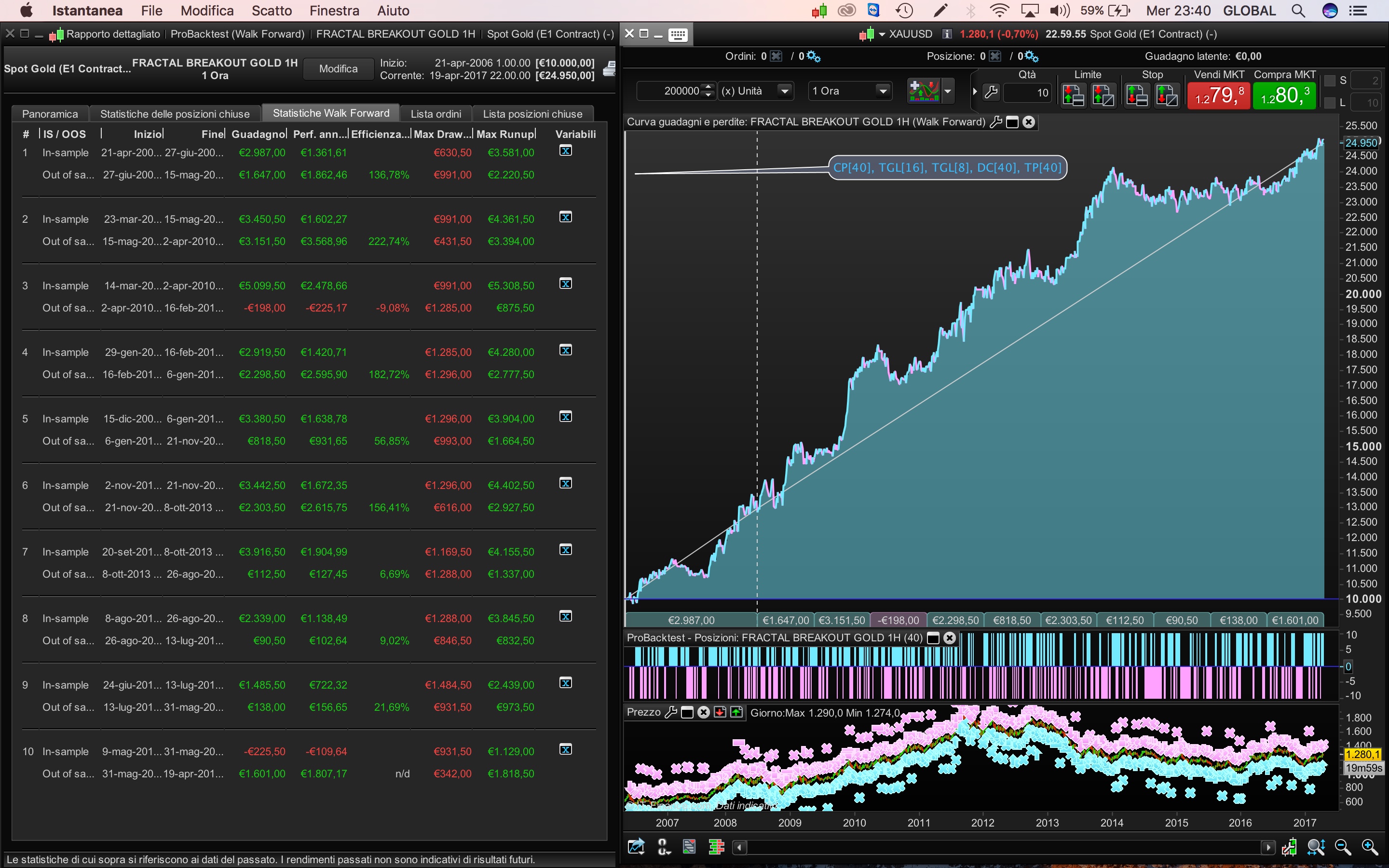

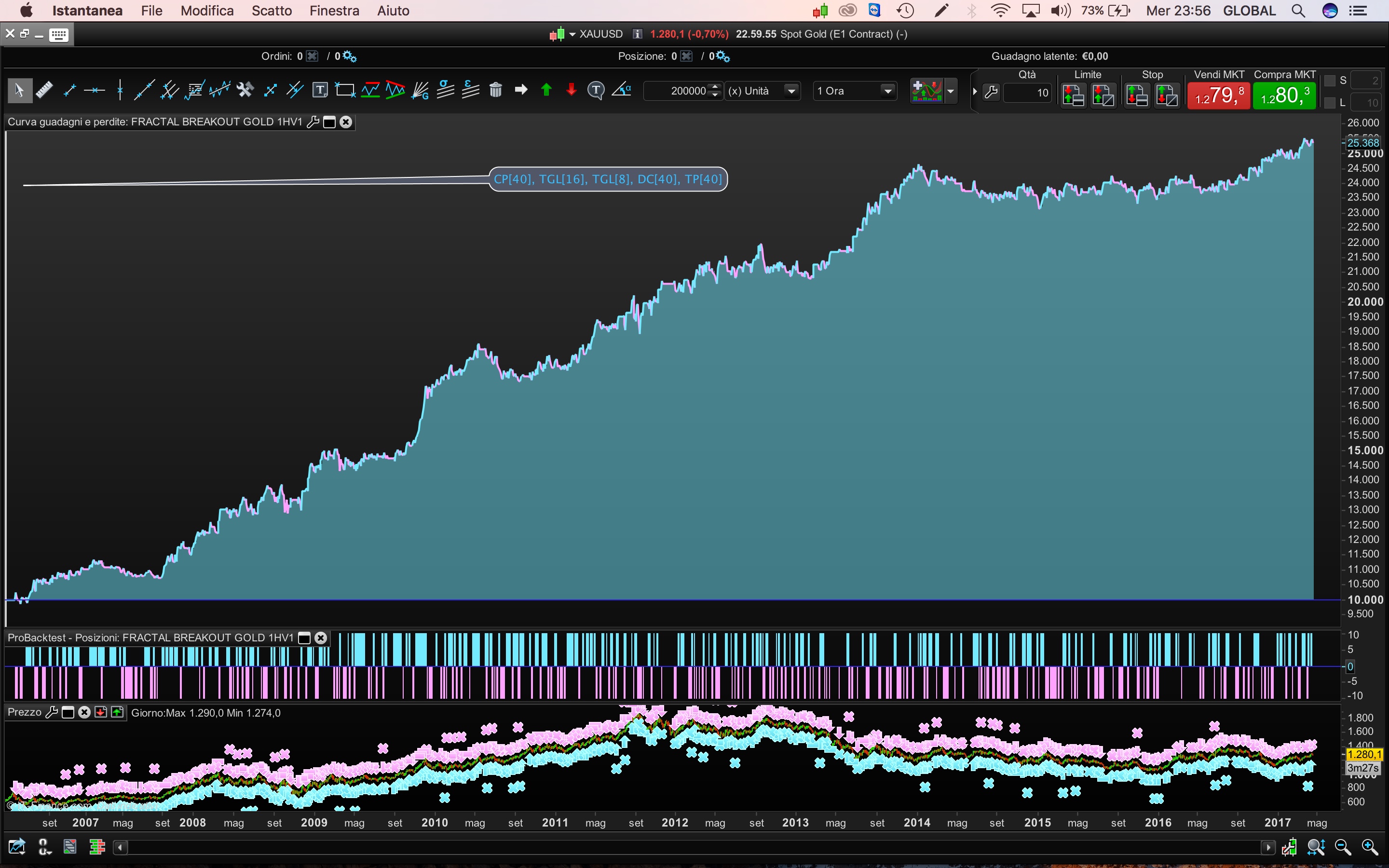

I’ve attached file for GOLD, this is one of many solutions. This set work with many levels and average profit it’s too low to approach real market. Now I’ll try to set Gold strategy on large levels, with a large take profit.

Apologies if stated somewhere (?), but what timezone are the times in the code please?