Optimization moving average crossing strategy with “machine learning”

{kind=link}

This is a “machine learning” strategy for finding the best crossing strategy, comparing 70 different averages with each other, given a certain time frame and a certain market.

(The source of the very most of the averages is https://www.prorealcode.com/prorealtime-indicators/average-filter-regression/ posted by Laurenzo in 2017)

The strategy is simple:

If the first average crosses above the second average, go buy long

and vice versa if the first average crosses under the second average, sell short

It can be used for currencies and indices, presumably also for stocks (non-daytrading)

This strategy determines which of the 70 different averages is to be crossed with which of the same 70 different averages to give the best result in a certain market in a certain time frame, what in my opinion can be seen as a kind of “machine learning”

Further added to this strategy: (up to the user to adjust those variables if wanted)

- to protect the position, a stop loss (TSL) is added (coded TSL = round(100/10000*close))

- exit a position every day at 16:00 hr (coded Defparam Flatafter = 160000) (Daytrading)

- limit to only one trade per day (coded OTD = Barindex – TradeIndex(1) > IntradayBarIndex, If using “TradeIndex(3)”, it would allow 2 opening trades per day, TradeIndex(5) would allow 3 trades per day, and so on.

- Opening trades only between 8:00 and 11:30, for American trades other times can be set.

There are 70 different types of averages, (listed below), which are used to cross each other (the first is named MAType, to be crossing the second MATypeV2)

To limit zigzagging of the averages due to market noise, an exponential average of 30 is added before the crossing condition is measured (Coded as wAFR = exponentialaverage[30](AFR) and wAFRv2 = exponentialaverage[30](AFRv2))

To limit the possibilities, the period is set for all average-types to 15 (Coded as Period = 15, Period2 = 15), periods may be adjusted.

Different stop distances can be used or a trailing stop can be used.

Be aware that if you use this “machine learning” on a small set of data, the outcome will be over- fitted and a different optimized set of averages for a different small set of data will appear (this happens with all strategies, robustness of the strategy has to be tested).

Be aware when running the given strategy, already 70 x 70 combinations has to be optimized, which is already 4.900 combinations, which makes the optimizing process (very) slow. It might be a good idea to split the combination into 5 sets, lets say from 0 to 13 averages comparing to the 69 averages, and next 14 to 26 comparing to 69 averages, and so on, then taking the best from the 5 sets.

I run the code first without In Sample/Out of Sample, to find the top 10 best average combinations, and around those top 10 run several In Sample/Out of Sample optimizations.

For In Sample/Out of Sample optimizations use 66% IS and 34% OOS, non repeated (not five runs)

The code is extremely long (> 3.600 lines), due to defining 70 and 70 different averages. Maybe it can be coded shorter ?

The crossing strategy itself can be found at the last rows !

I was not aware that PRT allows more then 3.600 lines of code as a strategy!

- Ahrens Moving Average

1. Adjustable Lag FIR

2. Arnaud Legoux Moving Average

3. 2-Pole Butterworth Smoothing Filter

4. 3-Pole Butterworth Smoothing Filter

5. Corrected Moving Average by A.Uhl

6. d9 Unscented Kalman Filter (Responsiveness Version)

7. d9 Unscented Kalman Filter

8. Double Exponential Moving Average

9. Exponential Least Square Moving Average

10. Exponential Moving Average

11. Elastic Volume Weighted Moving Average

12. Fast Adaptive Trend Line

13. Fractional-Bar Quick Moving Average

14. Fractal Adaptive Moving Average

15. Generalized DEMA

16. 1-Pole Gaussian Filter

17. 2-Pole Gaussian Filter

18. 3-Pole Gaussian Filter

19. 4-Pole Gaussian Filter

20. Hull Moving Average

21. IE/2 Combination of LSMA and ILRS

22. Integral of Linear Regression Slope

23. iTrend by John Ehlers

24. Jurik Moving Average (Responsiveness Version)

25. Jurik Moving Average

26. Kaufman Adaptive Moving Average

27. Kalman Filter by John Ehlers

28. Kalman Filter (Responsiveness Version)

29. Kalman Filter

30. Leader Exponential Moving Average

31. Laguerre Filter by John Ehlers

32. Least Square Moving Average

33. McGinley Dynamic

34. Middle High Low Range Moving Average

35. McNicholl Moving Average

36. Non Lag Moving Average (Responsiveness Version)

37. Non Lag Moving Average

38. One More Average

39. Pentuple Exponential Moving Average

40. Parabolic Weighted Moving Average

41. Quadruple Exponential Moving Average

42. Regularized EMA by Chris Satchwell

43. Reference Fast Trend Line

44. Reference Slow Trend Line

45. Slow Adaptive Trend Line

46. Simple Moving Average

47. 2-Pole Super Smoothing Filter

48. 3-Pole Super Smoothing Filter

49. Smoothed Simple Moving Average

50. Sine Weighted Moving Average

51. T3 Moving Average

52. Triple Exponential Moving Average

53. Triangular Moving Average

54. Time Series Average

55. Variable Index Dynamic Average

56. Variable Moving Average

57. Volume Weighted Average Price

58. Wilder Moving Average

59. Weighted Least Square Moving Average

60. Weighted Moving Average

61. Zero Lag BMT

62. Zero Lag Double Exponential Moving Average

63. Zero Lag FIR Filter

64. Zero Lag IIR Filter

65. Zero Lag John Ehlers

66. Zero Lag Weighted BMT

67. Range based AV high + STD – low – STD

68. Average highest [period] and lowest[period]

69 DEMA adjusted by itself

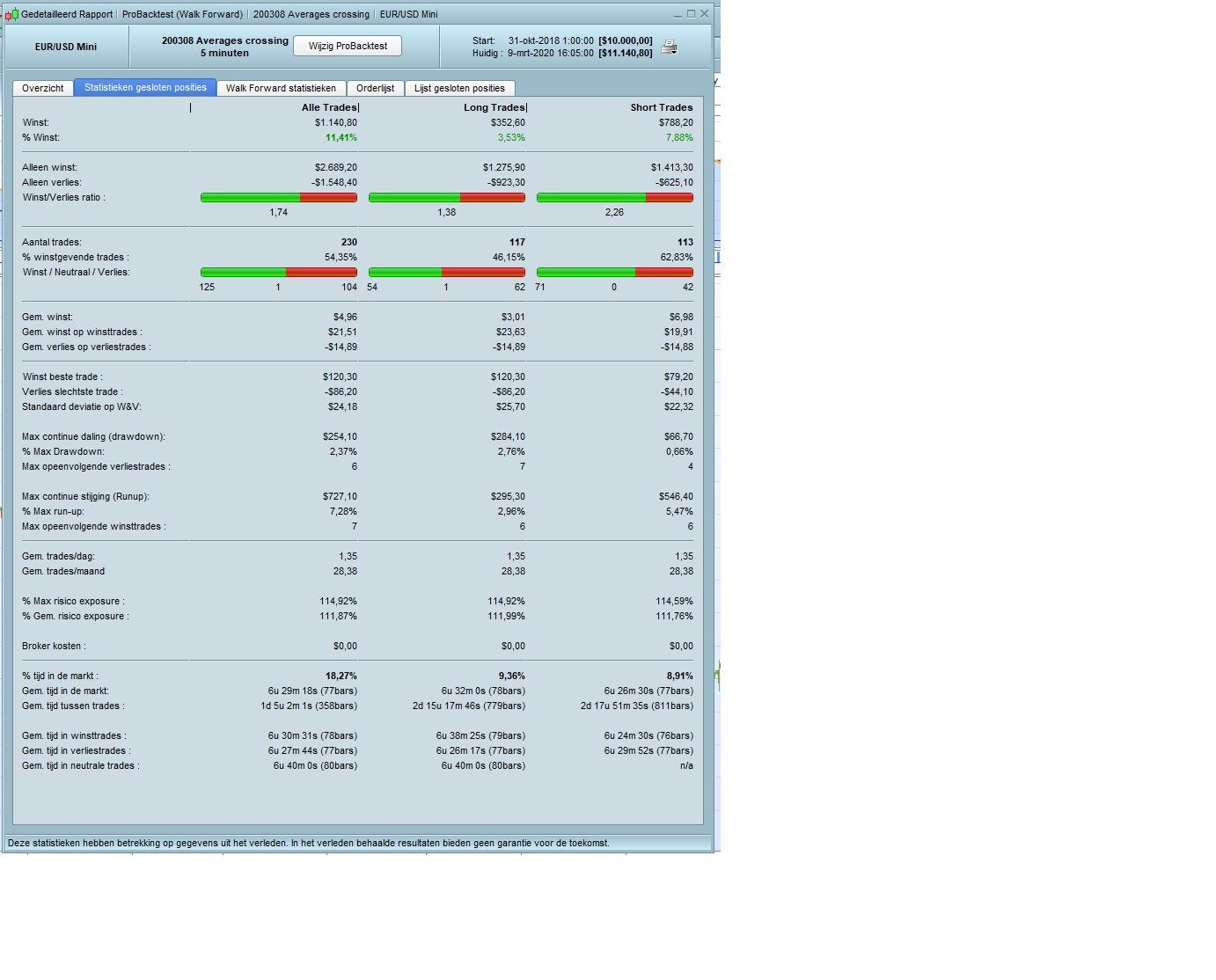

Please download the attached itf (200308-Averages-crossing.itf) to play around with this strategy.

{kind=link}