the problem is the number of bars / historic

Just set an end / cut off date on backtest of 1 week before the end of 100k bars then do your normal optimisation on In Sample (IS) 100k bars – / minus 1 week.

Then ride / test your donkey over the (most recent) 1 week worth of Out of Sample (OOS) data and the results should be very close to running the donkey on Live / Forward Test for 1 week.

If you can optimize on 70% of available history, then you have still 30% of data for your robustness test. Why is it not sufficient for you?

OOS is OOS. It does not matter whether the OOS is part of history that has already happened or the OOS is what happens in the next week, month, year or minute. So use what history we already know to confirm if an idea works on OOS before testing it on the future OOS. If it passes two OOS tests then you might(?) be on to something….. further robustness testing is then required before it is a three legged donkey turned racehorse!

Thanks for the reminder @Grahal

Always a good Idea. Fatser, but with less historic

Whatever, seems that the Algo with the same signal but modifying snippet for market structure start better. We will see at the end of the week

Bye Guys

If historic data is that important to you, how come you dont have 200k for backtests?

seems like it would be a great investment for you since you depend on huge amout of historic data

With PRT v11, there’s 1 million bars available. Do you have access to that huge data history Zilliq?

I know @Nicolas. I have the complete V1 version and some months for backtest I take the premium version but it’s 2 times more expensive only to have more historic !

And sadly I never succeed in doing a backtest on 1 millions bars

I think as many people I’m waiting the IG v11

For the moment I’m like a farmer , I sow, and I reap the good plants for the future 🙂

I know @Nicolas. I have the complete V1 version and some months for backtest I take the premium version but it’s 2 times more expensive only to have more historic !

And sadly I never succeed in doing a backtest on 1 millions bars

Do you know when the V11 will be released?

Prorealtime version 11 is available at https://www.prorealtime.com (released more than 1 year ago).

And we wait for the ig V11 version since thé extinction of dinosaurs 😂

Maybe a kind of petition from us could push IG to hurry up ?

I modify the code on analyze structure for the Bollinger setup, and we will see if now it will win the challenge

The IS Backtest enclosed

Great! How did you use Bollinger indicator…which conditions?

Thank you very much.

Hi Guys,

Sorry, a lot a lot of work at this time, and not a lot of free time

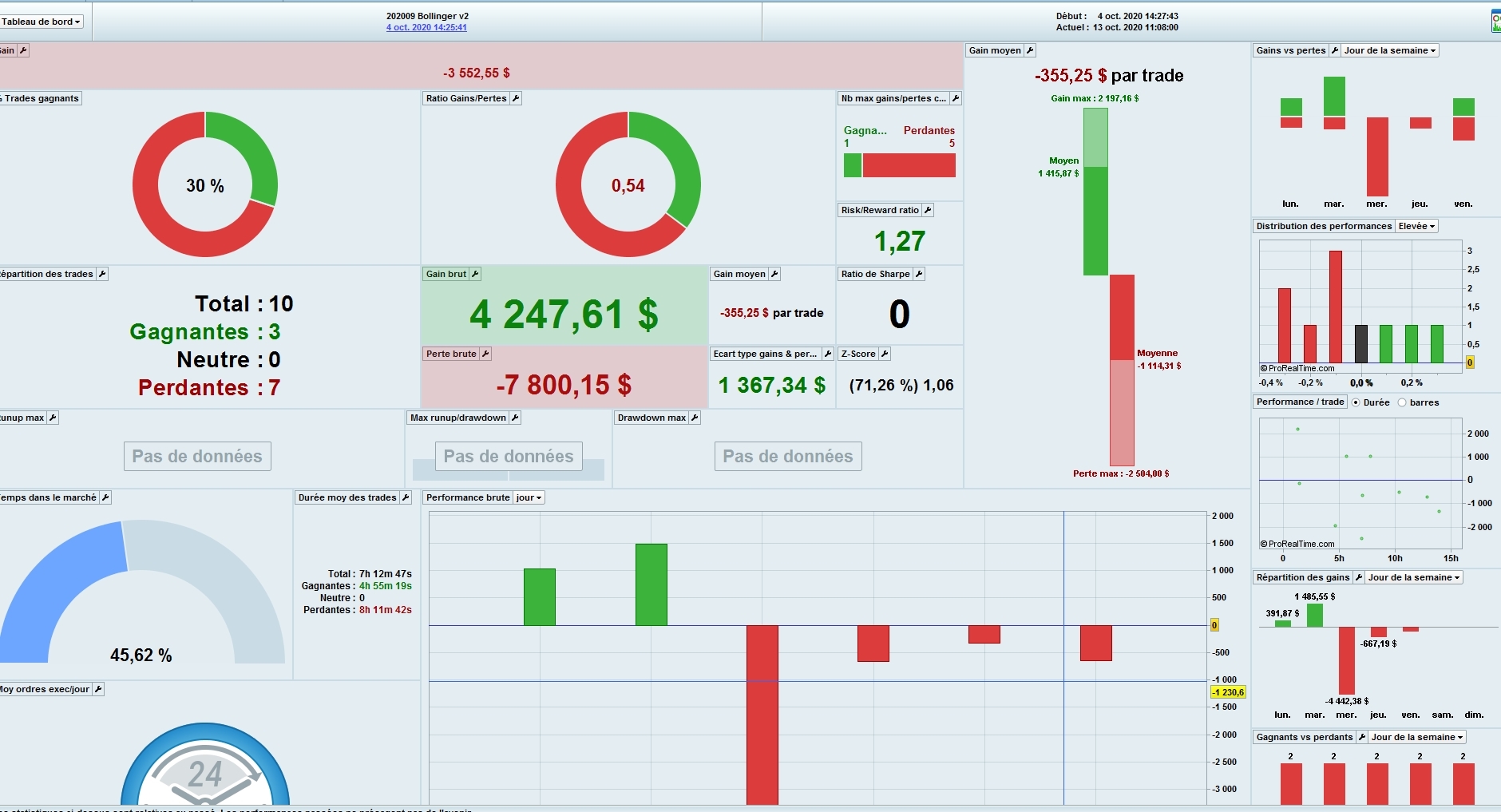

Well, the Bollinger Algo didn’t win the challenge 🙁 as you see on the pictures

What is interesting is to see what’s wrong.

As we see, most of the trades respect the Dow Theory, but 1/ Lot of range on EUR/USD (We are still near 1.18/1.2, very nervous market 2/ I suspect more and more that Trailing stop is a problem

I will test different things, more historic and comme back ASAP

Bye

I suspect more and more that Trailing stop is a problem

Are you cumulating positions?

Did you see Nicolas / Roberto / Paul TS code for cumulating strategies? Follow link below

NAS 2m HULL-SAR trading system