Just a couple of points I’m seeing: these tests are apparently done with 10k capital. But even with your fixed amount systems, you have 100,000+ contracts on?? Let’s say this was a mini market eurusd, say $60 margin US per $1 contract @ 0.5% margin rates, that’s $6,000,000 for margin-but you said your account has $10k in it? It is something lacking in PRT, it tracks your profit/loss, but not your used margin/margin risk as well. Am I wrong here??

So, out of the 3 things that you say are important, 1-the signal is insignificant; 2-you identify market structure; 3-you have now said that you essentially use fixed fractional money management.

Can you tell us more about how you identify market structure? You have said in the past that you use adx? It seems a lot is revolving around this identification process as well? It seems to me that there might be something valuable with what you are doing here with market structure identification??

Some might say that with a low enough risk:reward ratio you can make anything temporarily work-I’ve certainly proved that to myself many a time.

Still interested to know more about your market structure identification process Zilliq.

and for the drawdown thé stop loss is at 25-45 pips, of course not 500 pips

My mistake – I miscalculated (forgot to divide by 300!) – but then that is the problem when you don’t always test with a position size of 1 as it is difficult to easily make direct comparisons between tests or strategies if the position size is not always the same.

Money management on its own cannot make a bad strategy good but it can make a good strategy better.

So just to be clear, the results you are showing with the screenshots are pure In-Sample optimization? right? Thanks.

Yes Nicolas and this week the 2 algos are in OOS test

Bye

Hi Guys,

Sorry I had not a lot of time to be here this week because of a lot of work

Whatever, sadly these 2 Donkey signals don’t win the challenge 🙁

BUT, is it a real problem ? No ! “We never fail, we learn” as I say often!

What is interesting is to see which trades the algo took. I never had a problem if the market take a reversal, bad luck, but as Forrest Gump say “It happens !”

The problem is when there is some curious trades and/or stop

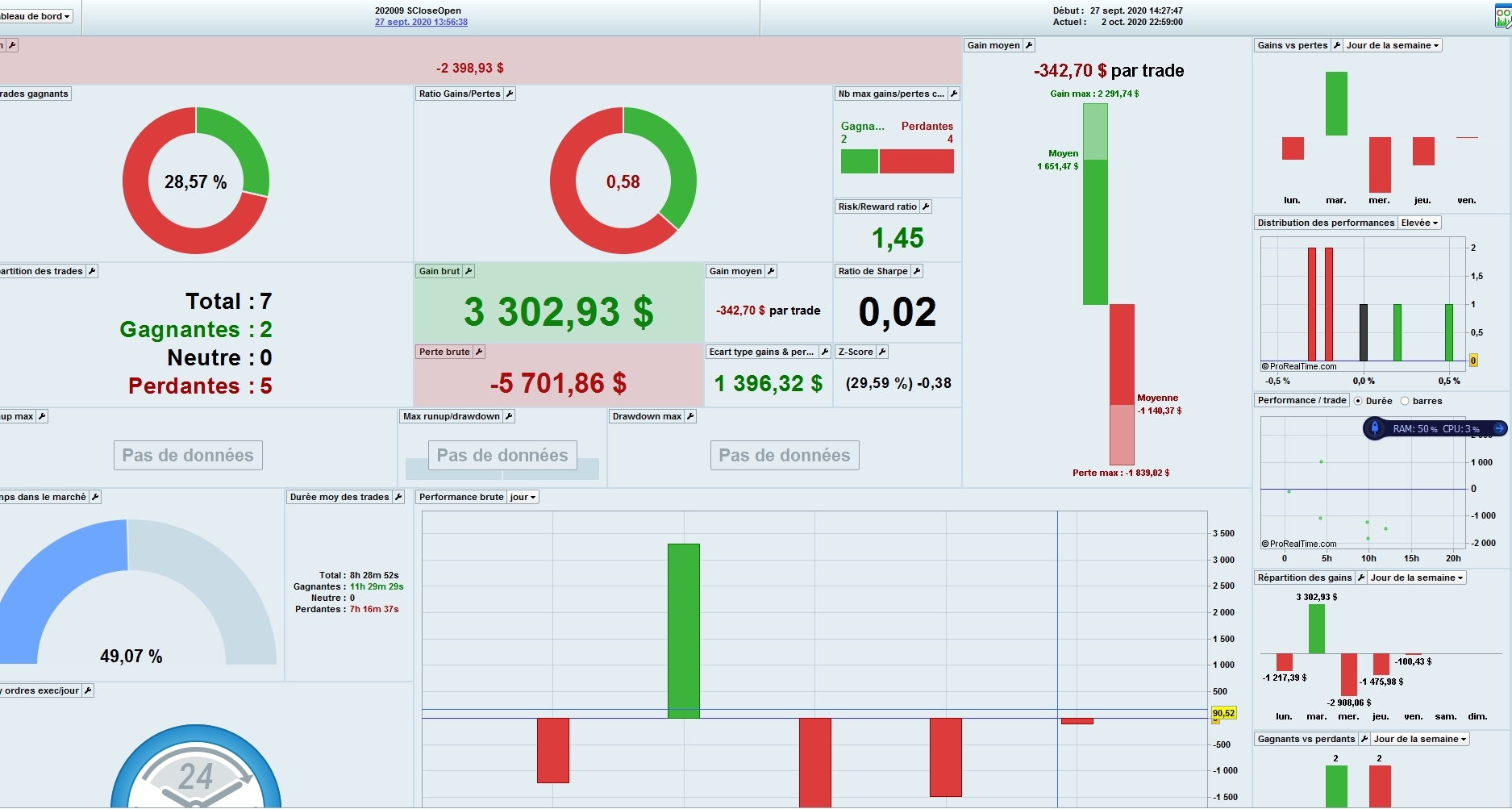

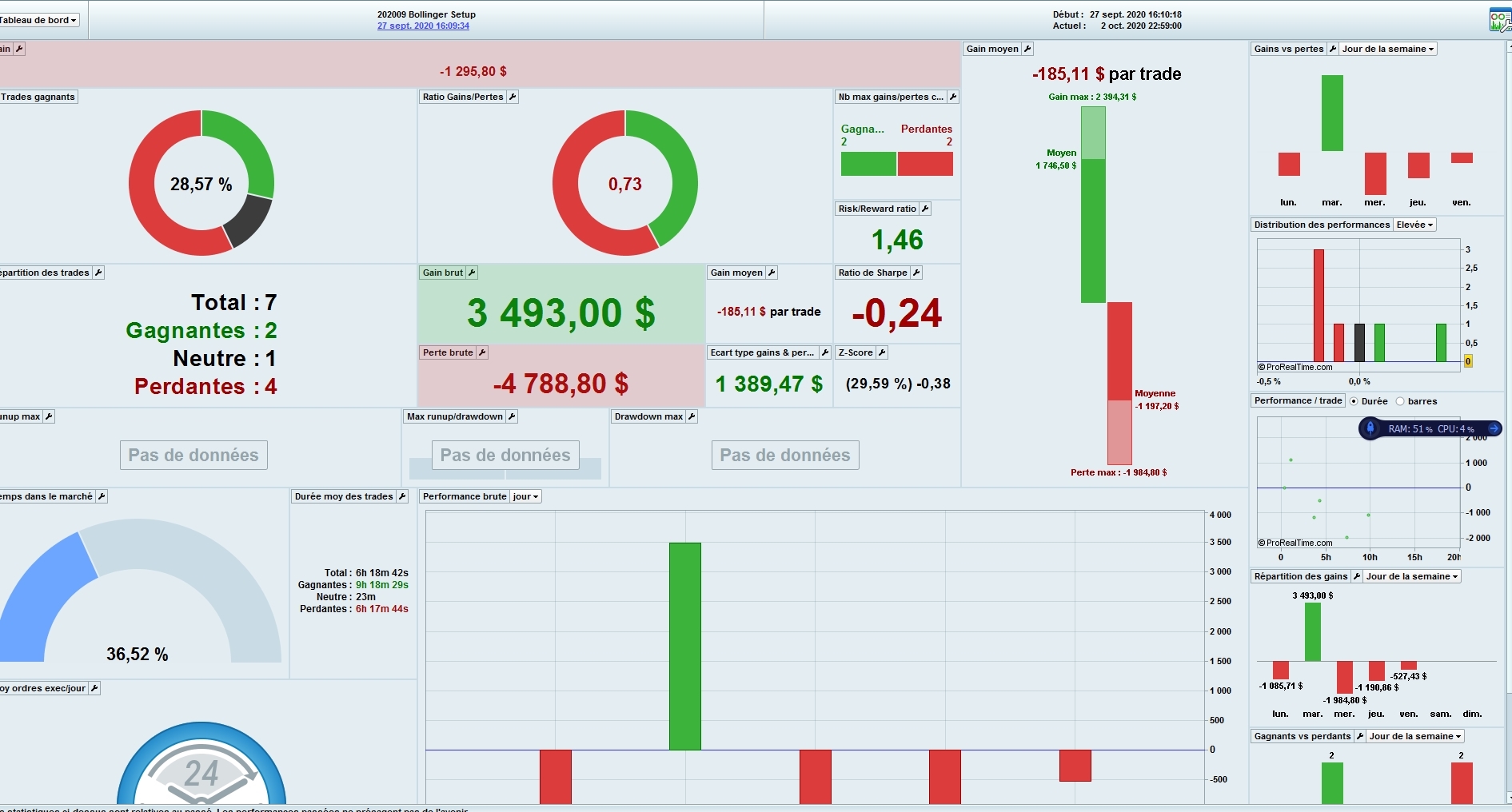

And on the different trades I see some problems (See pictures)

As you see some trades stop very soon even if they were right

And when you put some part of the strategy on trades and prices we see it’s a problem in the analyze of the maret structure, not a real problem with the entries signals

Conclusion : Need to optimize/ameliorate the analyze of the market structure because there is some problems. Moreover the EUR/USD market is a traitor as this time as we are between a big down and a big up (1.2…) and so the market on EUR/USD is very nervous

Bye

And just a quick last comment:

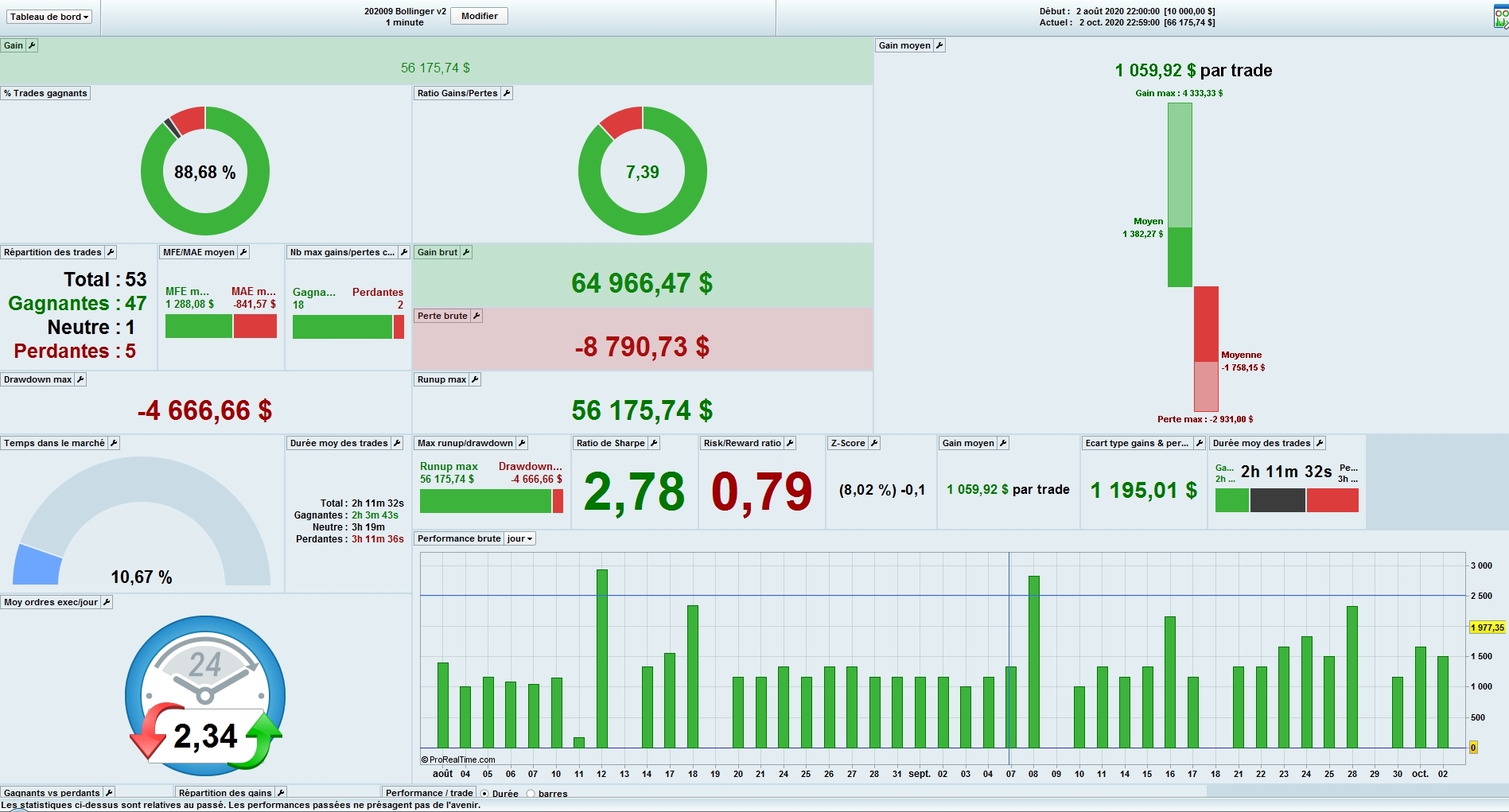

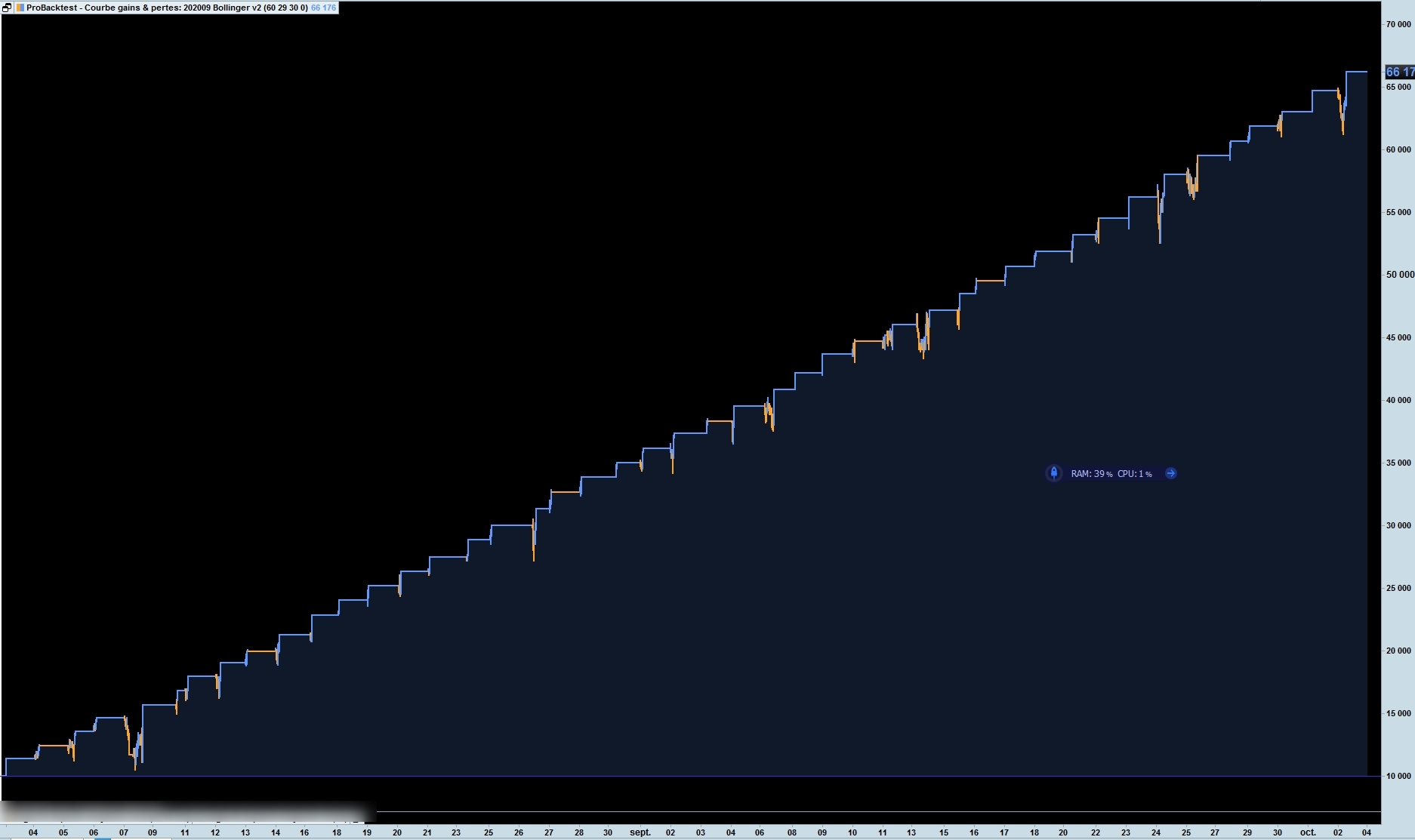

See as IS backtest are so beautiful, and how the OOS results this week is bad, not correlate

As I always said beautiful IS backtest means NOTHING (Just the first step, a good IS backtest means a good challenger, and a bad IS backtest go to the trash)

The “Graal” is not in the IS backtest but in the understanding in the correlation in IS/OOS results 😉

Bye

Indeed. Use the Walk-Forward tool, you will gain times.

No @Nicolas as I previously said the WF is actually unuseful as we can’t make a backtest and WF on a indicator or criteria othe than gain, % winners …and the best combinations is generally not the first results on a backtest

(You can find a comparaison on one of the previous file with parameters as first results and parameters as better results for me and it’s completely different)

Bye

I modify the code on analyze structure for the Bollinger setup, and we will see if now it will win the challenge

The IS Backtest enclosed

Paul

PaulParticipant

Master

hi zilliq do you also have a donkey that can run the 2s timeframe dow €1 long only & no overnight? Curious how that would perform.

Hi @Paul

I’m afraid it will be too fast and very dependant on your Internet connexion ?

Not really a problem of Donkey or Algo I think

Just my opinion

@Zilliq You said that you have optimized on a IS period. So you just have to take another set of period to test your optimized variables, in a backtest, the same way as you are doing it in live = OOS.

Not so easy Nicolas, because the WF don’t work as I work/choose parameters (It will if it can WF on an indicator 😉 )

This is not WF, but a simple backtest optimization first, then a second one on unknown data in the first place and with fixed variables and without optimization.

Thanks Nicolas, I understand what you mean, the problem is the number of bars / historic (We already speak about that with Grahal if I remember)