@volpiemanuele

Thanks you for the file🙏.

I will try it this afternoon.👍

Paul

PaulParticipant

Master

which parameters would you then optimise?

There are many parameters, but with walk forward I focussed on the rsi stochastic, only 2 parameters, 10-50k bars, unlinked with 3 repeats. Whatever you try, likely the last week will be neutral to very bad.

@ichimoku18 yes your right that was the intend, changing it would make it worse, so I leave it at current & previous bar and removed the last part. It could be better written too.

Great, in particular which are these two parameters to optimize?

Thank you

PaulParticipant

Master

Hi,

only the first 2. Having said that i’am just a bit experimenting.

lengthrsi = 2 // rsi period

lengthstoch = 6 // stochastic period

smoothk = 4 // smooth signal of stochastic a

smoothd = 8 // smooth signal of smoothed stochastic

dax 10s today. I know it’s not realistic with the stops etc and a lot would needs to be changed, but still.

@Paul, juste for fun i launch the v5b on Dax in 10s timeframe, but il crashed.

I use Stoch/RSI a lot, it’s one of my favourite indicators, but I find that you really have to optimise all the variables as each one reacts to other changes. With most indicators you usually have a reasonable expectation that if a value of 14 is good, then 12 or 16 will be a bit better or a bit worse. With Stoch/RSI values of 12, 14, 8, 2 could look good one minute then suddenly something like 8,6,8,4 is miles better – impossible to predict the optimal result. Default values are 14,14,10,3 as a theoretical starting point.

I usually run it with variations of 4 to 16 by 2 for the first 3, and 2 to 5 by 1 for smoothd (must be >1). Unfortunately that makes +1000 permutations so it’s time consuming, but almost always worth it – can massively improve almost any algo if you get it right.

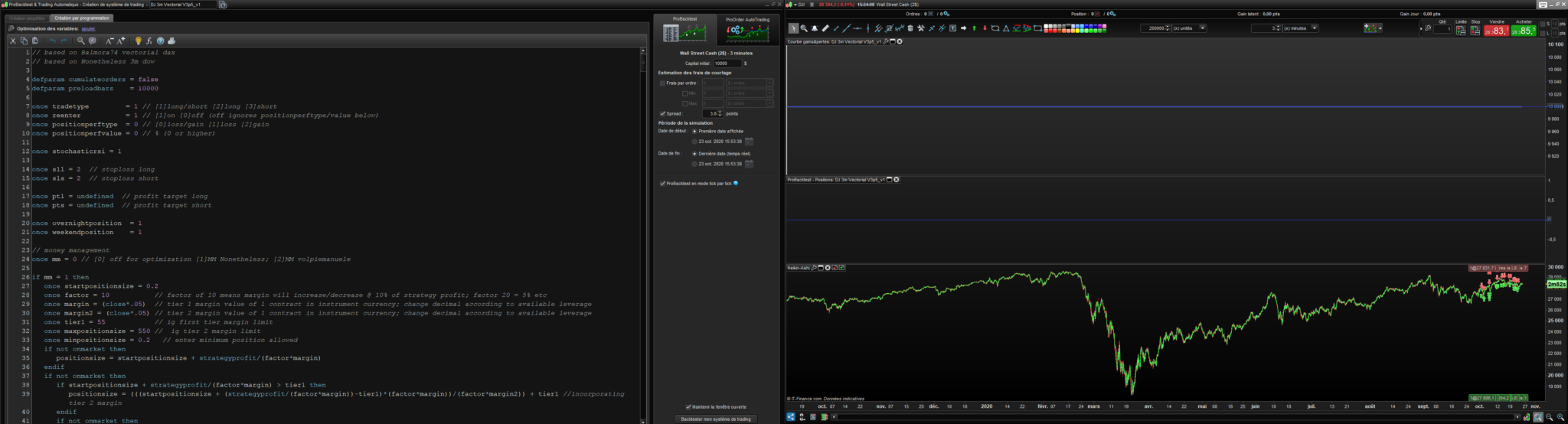

@Volpiemanuele, I tried to implement it on DJ 3 minutes and no orders showed up… Any ideas why?

@tanou: The last entry was this morning at 5am and still in progress … my live account

You simply implement it / Backtest it on Dow Jones 3 minutes or Dax ? Which UT?

Here what appears when I backtest it in 200k candles / DJ / 3min, nothing…

Restart the platform because it works, I just made a BT

It’s working now, it was coming from the positionsize

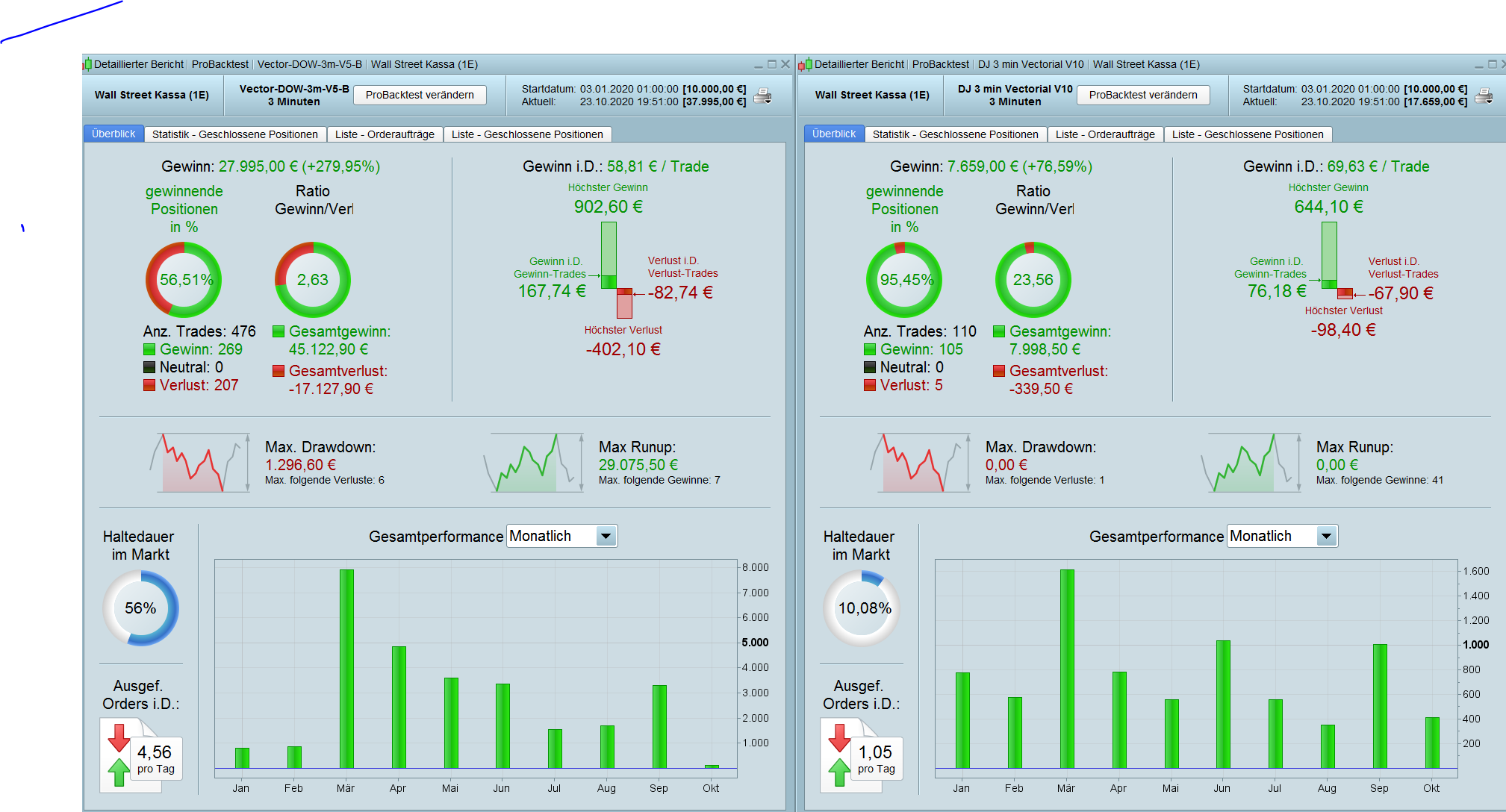

Do not hesitate to give me your feedback. I’ve worked on this, I haven’t fully optimize it for now, just had a look at the mistakes it was doing and try to eliminate them with a simple Ichimoku.

@Nonetheless & @Paul, hope you see something interesting, I think it is

// VECTORIAL MM - DJ 3m - Tanou v10

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 50000

//--------------------------------------------------------------------------------------------------------------------------------------------------

//Money Management

positionsize=1

//--------------------------------------------------------------------------------------------------------------------------------------------------

//HORAIRES DE TRADING

Ctime = time >= 153000 and time < 210000

//--------------------------------------------------------------------------------------------------------------------------------------------------

//STRATEGIE

//VECTEUR = CALCUL DE L'ANGLE

i1 = HistoricVolatility[10](close)

c1 = (i1 >= 0.06)

ONCE PeriodeA = 4

ONCE nbChandelierA= 30

MMA = Exponentialaverage[PeriodeA](close)

ADJASUROPPO = (MMA-MMA[nbchandelierA]) / nbChandelierA

ANGLE = (ATAN(ADJASUROPPO)) //FONCTION ARC TANGENTE

CB1 = ANGLE >= 34

CS1 = ANGLE <= - 48

//VECTEUR = CALCUL DE LA PENTE ET SA MOYENNE MOBILE

ONCE PeriodeB = 30

ONCE nbChandelierB= 35

lag = 0

MMB = Exponentialaverage[PeriodeB](close)

pente = (MMB-MMB[nbchandelierB]) / nbchandelierB

trigger = Exponentialaverage[PeriodeB+lag](pente)

CB2 = (pente > trigger) AND (pente < 0)

CS2 = (pente CROSSES UNDER trigger) AND (pente > - 0.5)

mx = average[67,0](close)

CB3 = mx > mx[1]

mx2 = average[21,0](close)

CS3 = mx2 < mx2[1]

// ichimoku

Tenkan = (highest[9](high)+lowest[9](low))/2

Kijun = (highest[26](high)+lowest[26](low))/2

SSpanA = (tenkan[26]+kijun[26])/2

SSpanB = (highest[52](high[26])+lowest[52](low[26]))/2

////chikou=close

//If SSpanA>SSpanB then

//IntervalS=SSpanA-SSpanB

//Elsif SSpanB>SSpanA then

//IntervalS=SSpanB-SSpanA

//endif

If SSpanA>SSpanB then

if open<SSpanA and open>SSpanB or close<SSpanA and close>SSpanB then

CondIchi = 0

Else

CondIchi = 1

endif

endif

If SSpanB>SSpanA then

if open>SSpanA and open<SSpanB or close>SSpanA and close<SSpanB then

CondIchi = 0

Else

CondIchi = 1

endif

endif

//--------------------------------------------------------------------------------------------------------------------------------------------------

//ENTREES EN POSITION

CONDBUY = CB1 and CB2 and CB3 and CTime and c1 and CondIchi

CONDSELL = CS1 and CS2 and CS3 and Ctime and c1 and CondIchi

VarDistIchiBuy = 6

VarDistIchiSell = 21

If CONDBUY then

DistIchiSSA = Open - SSpanA

DistIchiSSB = Open - SSpanB

CondDistIchi = DistIchiSSA >= VarDistIchiBuy AND DistIchiSSB >= VarDistIchiBuy

Endif

If CONDSELL then

DistIchiSSA = SSpanA - Open

DistIchiSSB = SSpanB - Open

CondDistIchi = DistIchiSSA >= VarDistIchiSell AND DistIchiSSB >= VarDistIchiSell

Endif

CONDBUY = CONDBUY and CondDistIchi

CONDSELL = CONDSELL and CondDistIchi

//--------------------------------------------------------------------------------------------------------------------------------------------------

//Entrée en position

//POSITION LONGUE

IF CONDBUY THEN

buy positionsize contract at market

SET STOP %LOSS 2.6

ENDIF

//POSITION COURTE

IF CONDSELL THEN

Sellshort positionsize contract at market

SET STOP %LOSS 0.6

ENDIF

//--------------------------------------------------------------------------------------------------------------------------------------------------

//SET TARGET %PROFIT 2

//Break even

breakevenPercent = 0.13

PointsToKeep = 1

startBreakeven = tradeprice(1)*(breakevenpercent/100)

once breakeven = 1//1 on - 0 off

//reset the breakevenLevel when no trade are on market

if breakeven>0 then

IF NOT ONMARKET THEN

breakevenLevel=0

ENDIF

// --- BUY SIDE ---

//test if the price have moved favourably of "startBreakeven" points already

IF LONGONMARKET AND close-tradeprice(1)>=startBreakeven THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)+PointsToKeep

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

SELL AT breakevenLevel STOP

ENDIF

// --- end of BUY SIDE ---

IF SHORTONMARKET AND tradeprice(1)-close>startBreakeven THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)-PointsToKeep

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

EXITSHORT AT breakevenLevel STOP

ENDIF

endif

//--------------------------------------------------------------------------------------------------------------------------------------------------

//SL above 0 if more than X hours and positive

//if longonmarket and barindex-tradeindex>60 then

//if close-tradeprice(1)>=2 then

//sell at tradeprice(1) STOP

//endif

//endif

//

//if shortonmarket and barindex-tradeindex>40 then

//if tradeprice(1)-close>=2 then

//EXITSHORT at tradeprice(1) STOP

//endif

//endif

//--------------------------------------------------------------------------------------------------------------------------------------------------

// trailing atr stop

once trailingstoptype = 1 // trailing stop - 0 off, 1 on

once tsincrements = 0.19 // set to 0 to ignore tsincrements

once tsminatrdist = 5

once tsatrperiod = 14 // ts atr parameter

once tsminstop = 12 // ts minimum stop distance

once tssensitivity = 1 // [0]close;[1]high/low

if trailingstoptype then

if barindex=tradeindex then

trailingstoplong = 6 // ts atr distance

trailingstopshort = 3 // ts atr distance

else

if longonmarket then

if tsnewsl>0 then

if trailingstoplong>tsminatrdist then

if tsnewsl>tsnewsl[1] then

trailingstoplong=trailingstoplong

else

trailingstoplong=trailingstoplong-tsincrements

endif

else

trailingstoplong=tsminatrdist

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

if trailingstopshort>tsminatrdist then

if tsnewsl<tsnewsl[1] then

trailingstopshort=trailingstopshort

else

trailingstopshort=trailingstopshort-tsincrements

endif

else

trailingstopshort=tsminatrdist

endif

endif

endif

endif

tsatr=averagetruerange[tsatrperiod]((close/10))/1000

//tsatr=averagetruerange[tsatrperiod]((close/1)) // (forex)

tgl=round(tsatr*trailingstoplong)

tgs=round(tsatr*trailingstopshort)

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

tsmaxprice=0

tsminprice=close

tsnewsl=0

endif

if tssensitivity then

tssensitivitylong=high

tssensitivityshort=low

else

tssensitivitylong=close

tssensitivityshort=close

endif

if longonmarket then

tsmaxprice=max(tsmaxprice,tssensitivitylong)

if tsmaxprice-tradeprice(1)>=tgl*pointsize then

if tsmaxprice-tradeprice(1)>=tsminstop then

tsnewsl=tsmaxprice-tgl*pointsize

else

tsnewsl=tsmaxprice-tsminstop*pointsize

endif

endif

endif

if shortonmarket then

tsminprice=min(tsminprice,tssensitivityshort)

if tradeprice(1)-tsminprice>=tgs*pointsize then

if tradeprice(1)-tsminprice>=tsminstop then

tsnewsl=tsminprice+tgs*pointsize

else

tsnewsl=tsminprice+tsminstop*pointsize

endif

endif

endif

if longonmarket then

if tsnewsl>0 then

sell at tsnewsl stop

endif

if tsnewsl>0 then

if low crosses under tsnewsl then

sell at market // when stop is rejected

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

exitshort at tsnewsl stop

endif

if tsnewsl>0 then

if high crosses over tsnewsl then

exitshort at market // when stop is rejected

endif

endif

endif

endif

if onmarket then

if dayofweek=0 and (hour=0 and minute>=57) and abs(dopen(0)-dclose(1))>50 and positionperf(0)>0 then

if shortonmarket and close>dopen(0) then

exitshort at market

endif

if longonmarket and close<dopen(0) then

sell at market

endif

endif

endif

going live for me

Nice. But the profit is in direct comparison to the V5 very low.

PaulParticipant

Master

nice work Tanou and to see another approach!

PaulParticipant

Master

I’ve worked on the entry on p5 version, it was copy & past to see what cumulative orders would do in your strategy. What’s strange is that for the short no cumulative orders happen, only for long. I haven’t put in a limit on them. (ts 0.5% for both long & short)

edit; to make it work, I removed the breakeven & atr trailingstop and put in the % trailingstop for cumulative positions.