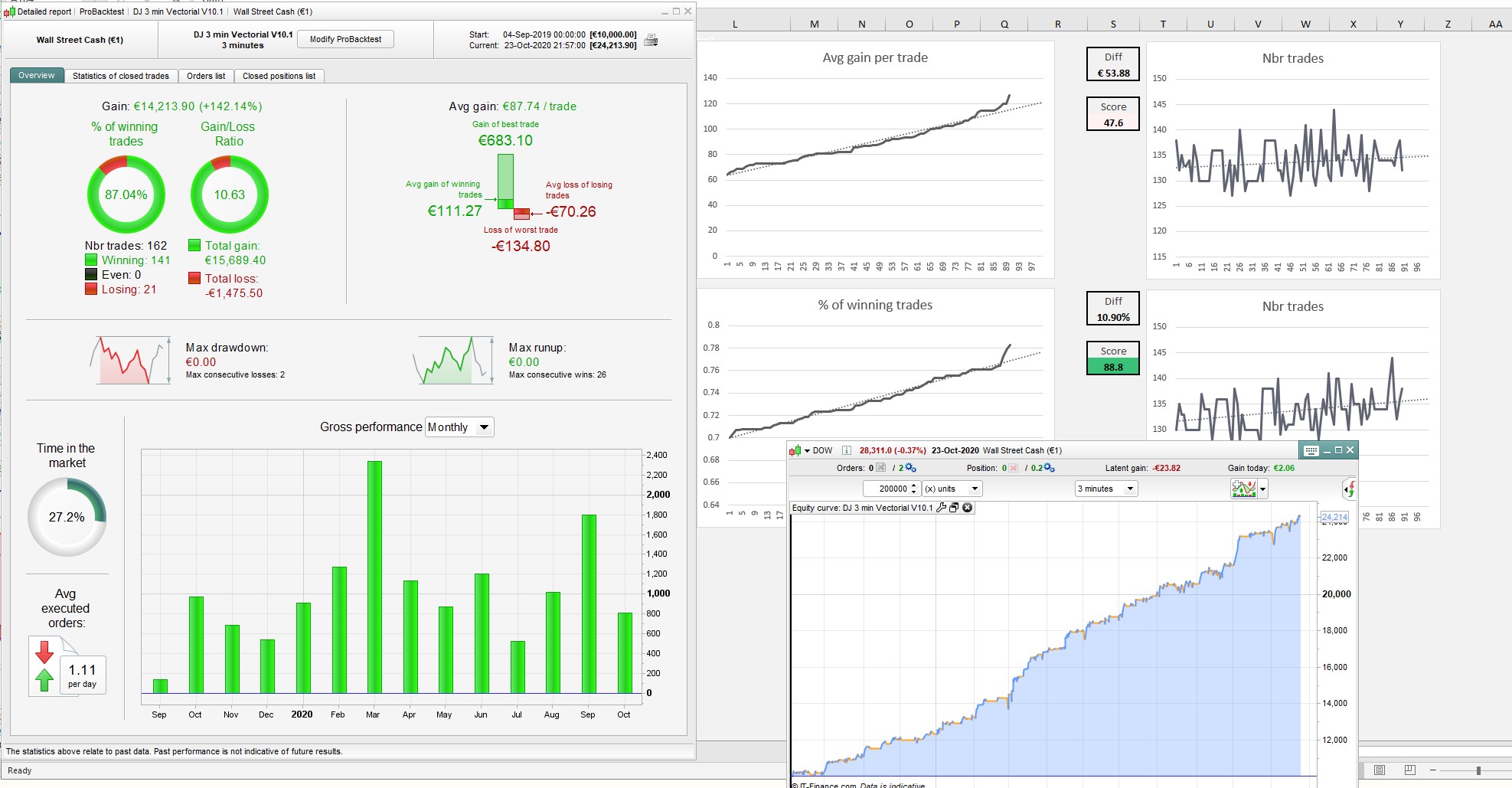

I’m ok with that @VinzentVega as my goal is to increase the $by point with a stable code instead of a shotgun with very little $/point and low percentage loss/gain ratio 🙂

@Paul Haha, I just observed with diferent toolsand this one seems to be ok 😉

I’m going to have a look at your option Paul!

But I would like to change a bit of the DJ wich code should I take as base to have a look at the DAX? 🙂

Yeah Tanou, yr right. Well done. 🙂

Paul

PaulParticipant

Master

the reason for short that there are no cumulative positions is below (crosses under)

CB2 = (pente > trigger) AND (pente < 0)

CS2 = (pente CROSSES UNDER trigger) AND (pente > - 0.5)

for long it uses > , the long signals can come as result in rapid succession.

Nice work @Tanou, I like it. much prefer stable and consistent performance to max profit. With such a high win rate you can always jack up the position size with more confidence.

Here’s a quick treatment, just minor changes. i’ll have a look at the ichimoku part over the weekend.

No WF but the VRT is good.

Thanks @Nonetheless 🙂

Do not hesitate to tell us what you’ve improved, curious about it 😉

How did you export the backtest datas to Excel by the way?

(If you look closely I also added a condition with the historical volatility that helps a bit 🙂 )

That was just a very quick re-optimisation of some key variables, nothing sophisticated.

You can drag and drop the optimisation results directly into Excel. You can read more about VRT and how to use it here, if you haven’t already seen it:

Strategy Robustness Tester

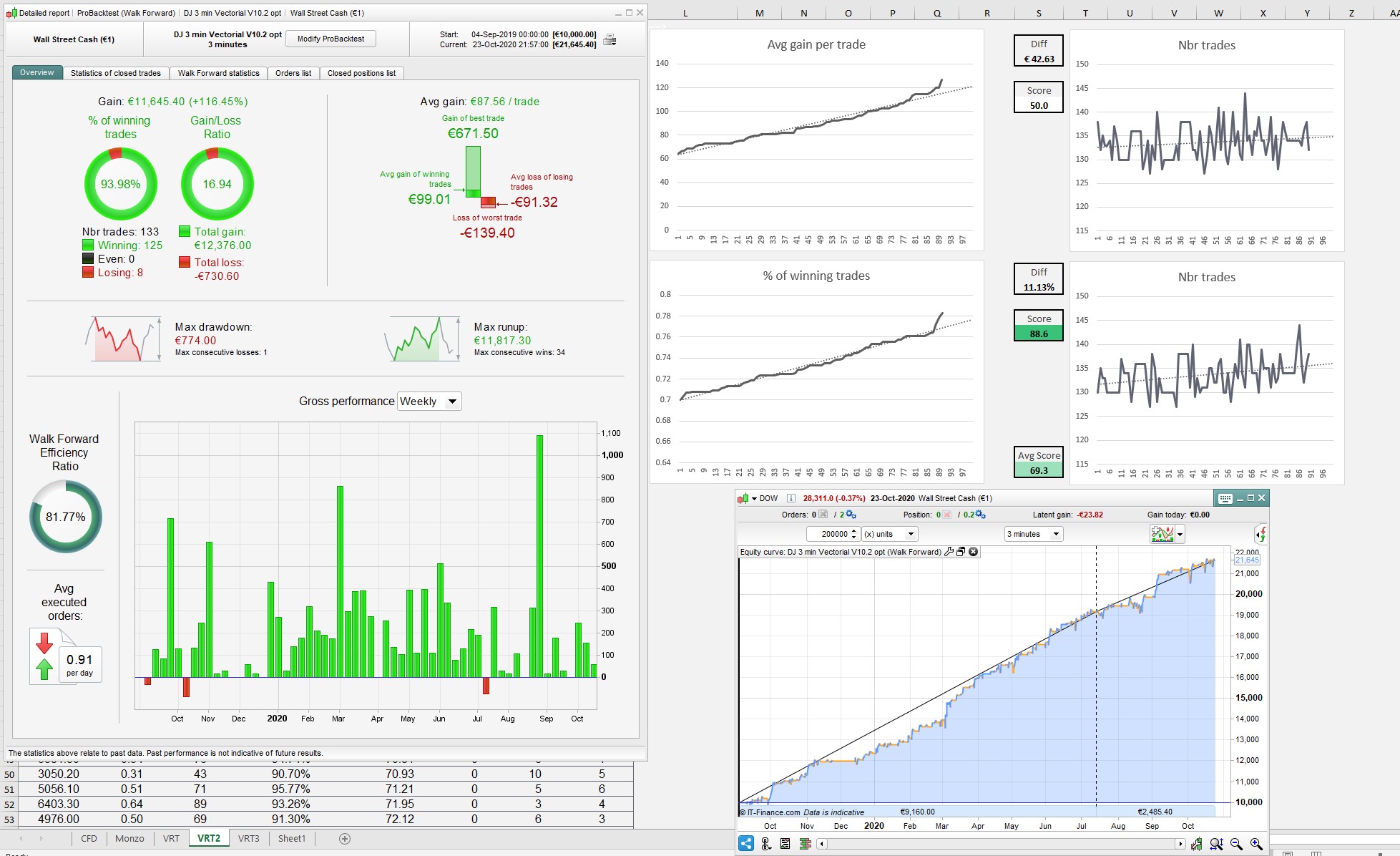

This is the best I could do with it. Added Stochastic Rsi and re-optimised almost everything on a 75/25 WF. Final values are a compromise between what worked best in WF and VRT, but the last 3 months is all out of sample except for the Vectorial values which I left as is. I disabled the historical volatility as it seemed better without it.

Really excellent piece of work @Tanou, thanks for that!

Hello @Paul, @Nonetheless, @VinzentVega thanks for your feedback! 🙂

I will keep thinking about this code to try to improve it 🙂

@Nontetheless, I had a look at your code and it’s promising as well! I’ll try delete other conditions and try wth yours to see if something else appears 😉

However, I saw that you’ve added a %Profit stop, don’t you think that it is too optimized on the backtest? This variable suits perfectly the backtest but don’t you think it could block some positions to go higher if high and sudden volatility?

I was thinking to have a look at the trailing stop part. Do you guys had already some ideas like another trailing stop or another condition? This is an excellent strategie in my opinion. However, I’d like to make it more effective as it let too many points goes for nothing sometimes…!

I’d like to get into this, suggestions @Paul, @Nonetheless?

I tried swapping out the Break even and ATR for a %TS but atr worked better.

I wouldn’t worry about the profit target restricting your wins, it’s set pretty high. It’s a pretty rare occasion that an algo runs a +2% profit and when you get one I expect you’ll be very happy to bank it.

Hahaha, I agree with that one 😀

This is the best I could do with it. Added Stochastic Rsi and re-optimised almost everything on a 75/25 WF. Final values are a compromise between what worked best in WF and VRT, but the last 3 months is all out of sample except for the Vectorial values which I left as is. I disabled the historical volatility as it seemed better without it.

Really excellent piece of work @Tanou, thanks for that!

Thanks!

I wanna to know if winter time, the time need to change 1530 to 2200?

I’ve optimised it to run only during Wall St opening hours so yes, ideally you should adjust the time for whatever those hours are where you live, also for winter time / summer time.

funny, by mistake I’ve loaded up v5p on the dax 10s

with these settings ;

once tradetype = 1 // [1]long/short [2]long [3]short

once reenter = 1 // [1]on [0]off (off ignores positionperftype/value below)

once positionperftype = 1 // [0]loss/gain [1]loss [2]gain

once positionperfvalue = 0 // % (0 or higher)

once tradetype = 1 // [1]long/short [2]long [3]short

once reenter = 1 // [1]on [0]off (off ignores positionperftype/value below)

once positionperftype = 1 // [0]loss/gain [1]loss [2]gain

once positionperfvalue = 0 // % (0 or higher)

This right here is bananas!

I now have a 10s optimized version of Nasdaq, Dow and DAX prepared for next week. The Dow version looks too good to be true. It will be interesting to see how it really performs.

PaulParticipant

Master

Hi paisantrader all forgot about that!

Worked on something else, includes a small part of vectorial on 15 or 30s and based on mfemae. But I expect it to fail bigtime regardless how it looks.

it does cumulate orders or without

thanked this post