where in the code does it calculate the ‘positionsize’ for which PositionSizeLong and PositionSizeShort are derived?

At line 7 you can have positionsize = any value you like. With MM= 0 it won’t change.

// VECTORIAL MM - DJ 3m

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 50000

//Money Management

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize=.5

I have been running a 5m long version of this over the past couple of months. It’s basically a merger between Vectorial and MoD, so far fairly consistent with the back test.

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 50000

//Money Management

MM = 1 // = 0 for optimization

if MM = 0 then

positionsize=.5

ENDIF

if MM = 1 then

ONCE startpositionsize = .5

ONCE factor = 10 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE margin = (close*.005) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.01)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 55 // IG first tier margin limit

ONCE maxpositionsize = 550 // IG tier 2 margin limit

ONCE minpositionsize = .2 // enter minimum position allowed

IF Not OnMarket THEN

positionsize = startpositionsize + Strategyprofit/(factor*margin)

ENDIF

IF Not OnMarket THEN

IF startpositionsize + Strategyprofit/(factor*margin) > tier1 then

positionsize = (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 //incorporating tier 2 margin

ENDIF

IF Not OnMarket THEN

if startpositionsize + Strategyprofit/(factor*margin) < minpositionsize THEN

positionsize = minpositionsize //keeps positionsize from going below allowed minimum

ENDIF

IF (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 > maxpositionsize then

positionsize = maxpositionsize// keeps positionsize from going above IG tier 2 margin limit

ENDIF

ENDIF

ENDIF

ENDIF

Ctime = time >= 010000 and time <= 230000

TIMEFRAME(2 hours)

Period= 240

inner = 2*weightedaverage[round( Period/2)](typicalprice)-weightedaverage[Period](typicalprice)

HULLa = weightedaverage[round(sqrt(Period))](inner)

c9 = HULLa > HULLa[1]

//c2 = HULLa < HULLa[1]

TIMEFRAME(15 minutes)

mx1 = average[16,1](close)

c7 = mx1 > mx1[1]

//c8 = mx1 < mx1[1]

TIMEFRAME(10 minutes)

mx2 = average[15,0](close)

c5 = mx2 > mx2[1]

//c6 = mx2 < mx2[1]

//Stochastic RSI | indicator

lengthRSI = 10//RSI period

lengthStoch = 16//Stochastic period

smoothK = 16 //Smooth signal of stochastic RSI

smoothD = 3 //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K = average[smoothK](stochrsi)*100

D = average[smoothD](K)

c3 = K>D

//c4 = K<D

TIMEFRAME(default)

indicator4 = SuperTrend[1,7]

c1 = (close > indicator4)

//c2 = (close < indicator4)

//VECTEUR = CALCUL DE L'ANGLE

ONCE PeriodeA = 5

ONCE nbChandelierA= 42

MMA = Exponentialaverage[PeriodeA](close)

ADJASUROPPO = (MMA-MMA[nbchandelierA]*pipsize) / nbChandelierA

ANGLE = (ATAN(ADJASUROPPO)) //FONCTION ARC TANGENTE

CondBuy1 = ANGLE >= 31

//CondSell1 = ANGLE <= - 25

//VECTEUR = CALCUL DE LA PENTE ET SA MOYENNE MOBILE

ONCE PeriodeB = 24

ONCE nbChandelierB= 50

lag = 4

MMB = Exponentialaverage[PeriodeB](close)

pente = (MMB-MMB[nbchandelierB]*pipsize) / nbchandelierB

trigger = Exponentialaverage[PeriodeB+lag](pente)

CondBuy2 = (pente > trigger) AND (pente < 0)

//CondSell2 = (pente CROSSES UNDER trigger) AND (pente > -1)

//ENTREES EN POSITION

CONDBUY = CondBuy1 and CondBuy2 and Ctime and c1 and c3 and c5 and c7 and c9

//CONDSELL = CondSell1 and CondSell2 and Ctime and c2 and c4 and c6 and c8

//POSITION LONGUE

IF CONDBUY THEN

buy positionsize contract at market

SET STOP %LOSS 1.7

SET TARGET %PROFIT 2.1

ENDIF

//POSITION COURTE

//IF CONDSELL THEN

//Sellshort positionsize contract at market

//SET STOP %LOSS sls

//SET TARGET %PROFIT tps

//ENDIF

//Break even

once breakeven = 1//1 on - 0 off

breakevenPercent = .22

PointsToKeep = 2

startBreakeven = tradeprice(1)*(breakevenpercent/100)

//reset the breakevenLevel when no trade are on market

if breakeven>0 then

IF NOT ONMARKET THEN

breakevenLevel=0

ENDIF

// --- BUY SIDE ---

//test if the price have moved favourably of "startBreakeven" points already

IF LONGONMARKET AND close-tradeprice(1)>=startBreakeven*pipsize THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)+PointsToKeep*pipsize

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

SELL AT breakevenLevel STOP

ENDIF

// --- end of BUY SIDE ---

IF SHORTONMARKET AND tradeprice(1)-close>startBreakeven*pipsize THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)-PointsToKeep*pipsize

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

EXITSHORT AT breakevenLevel STOP

ENDIF

endif

//****************************************************************************************

// trailing atr stop II

once trailingstoptype = 1 // trailing stop - 0 off, 1 on

once tsincrements = 0 // set to 0 to ignore tsincrements

once tsminatrdist = 2

once tsatrperiod = 14 // ts atr parameter

once tsminstop = 12 // ts minimum stop distance

once tssensitivity = 0 // [0]close;[1]high/low

if trailingstoptype then

if barindex=tradeindex then

trailingstoplong = 9 // ts atr distance

trailingstopshort = 9 // ts atr distance

else

if longonmarket then

if tsnewsl>0 then

if trailingstoplong>tsminatrdist then

if tsnewsl>tsnewsl[1] then

trailingstoplong=trailingstoplong

else

trailingstoplong=trailingstoplong-tsincrements

endif

else

trailingstoplong=tsminatrdist

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

if trailingstopshort>tsminatrdist then

if tsnewsl<tsnewsl[1] then

trailingstopshort=trailingstopshort

else

trailingstopshort=trailingstopshort-tsincrements

endif

else

trailingstopshort=tsminatrdist

endif

endif

endif

endif

tsatr=averagetruerange[tsatrperiod]((close/10)*pipsize)/1000

//tsatr=averagetruerange[tsatrperiod]((close/1)*pipsize) // (forex)

tgl=round(tsatr*trailingstoplong)

tgs=round(tsatr*trailingstopshort)

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

tsmaxprice=0

tsminprice=close

tsnewsl=0

endif

if tssensitivity then

tssensitivitylong=high

tssensitivityshort=low

else

tssensitivitylong=close

tssensitivityshort=close

endif

if longonmarket then

tsmaxprice=max(tsmaxprice,tssensitivitylong)

if tsmaxprice-tradeprice(1)>=tgl*pointsize then

if tsmaxprice-tradeprice(1)>=tsminstop then

tsnewsl=tsmaxprice-tgl*pointsize

else

tsnewsl=tsmaxprice-tsminstop*pointsize

endif

endif

endif

if shortonmarket then

tsminprice=min(tsminprice,tssensitivityshort)

if tradeprice(1)-tsminprice>=tgs*pointsize then

if tradeprice(1)-tsminprice>=tsminstop then

tsnewsl=tsminprice+tgs*pointsize

else

tsnewsl=tsminprice+tsminstop*pointsize

endif

endif

endif

if longonmarket then

if tsnewsl>0 then

sell at tsnewsl stop

endif

if tsnewsl>0 then

if low crosses under tsnewsl then

sell at market // when stop is rejected

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

exitshort at tsnewsl stop

endif

if tsnewsl>0 then

if high crosses over tsnewsl then

exitshort at market // when stop is rejected

endif

endif

endif

Welcome back nonetheless 🙂

@nonetheless

Welcome back 🙂

I put Your last code above in PRT but my backtest is different from Yours. I also needed to add an “endif” in the end. I’m running version 10.3

Have I done something wrong?

Hello nonetheless

Hope you are well. Many thanks for your reply. I just tried your suggestion with the code you posted above and it worked. I will try to incorporate this back into the version of the Vectorial code I had downloaded preciously.

Thanks

S

my backtest is different from Yours

hi Artemois, live forward tests will always vary from the back test for multiple reasons. Also, I think mine was stopped and restarted some time in August so the MM will have reset. But when I run a back test for those 2 months, I see v similar performance ~91%

and yes, it does need another endif – got lost in the copy/paste

Also, please note that i didnt do any WF or VRT for this; the straight back test looked good and I was curious about the basic concept so I put it on demo for a couple of months, that’s all. I’m sure it can be improved

Hi Nonetheless

My bad, I didn’t understand it was Your actual result but thought it was the backtest 😉

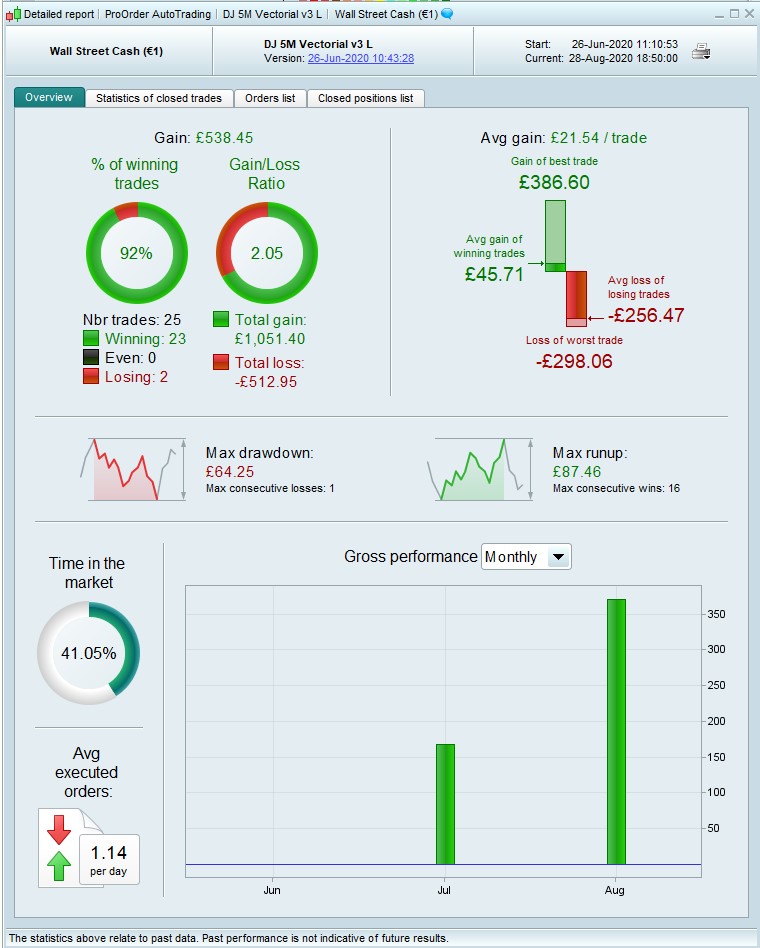

Below is a backtest for the same dates.

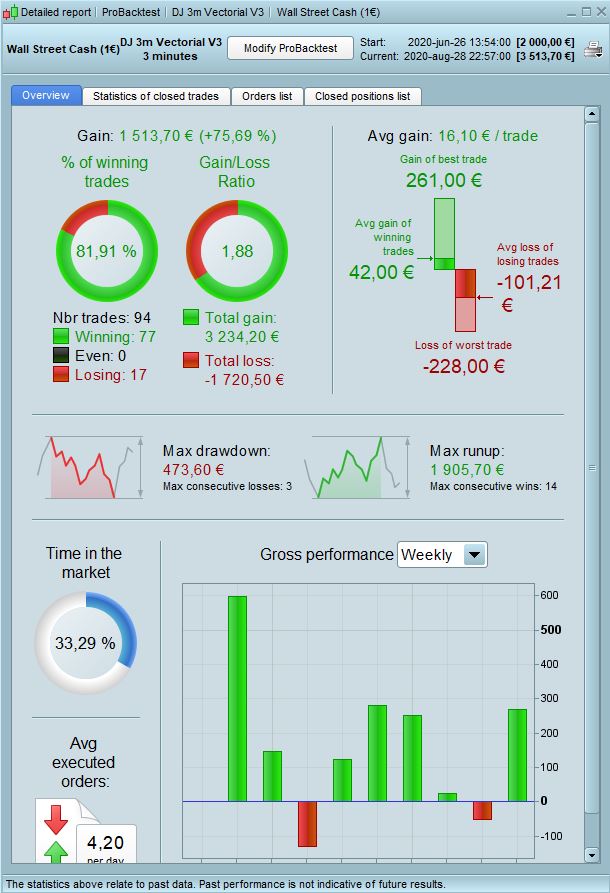

I got same backtest result as Artemois … different / reduced by a factor of 15 ish from Nonetheless Pro-Order results.

Big difference … something must be wrong?

This is well weird … I ran Nonetheless code above again 2 mins ago and got completely different results than I was getting last night!

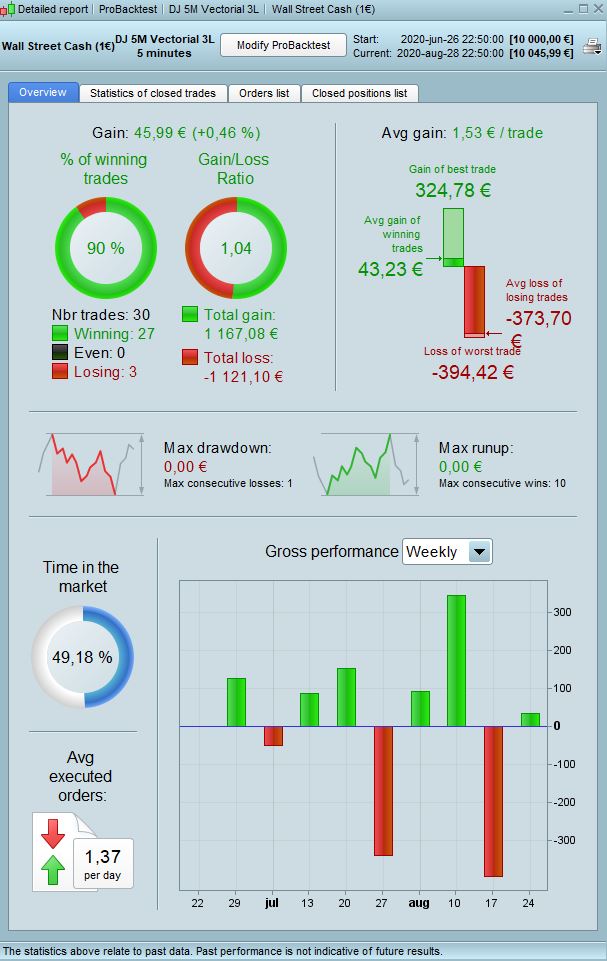

Nearer / more comparable with None’s now … see attached. I still get far more drawdown though … mine dd at £947 vs None’s dd at £64

What do you get this morning @Artemois ??

I’m putting attached on Forward Test on Monday … MM turned off and Period = 55 at Line 37.

Above is all I explored, I’m sure there would be other beneficial changes?

It be great if we had a Short version or Long and Short in same System?

Thank You for sharing Nonetheless!

Hi Grahal

I get the same results today as yesterday

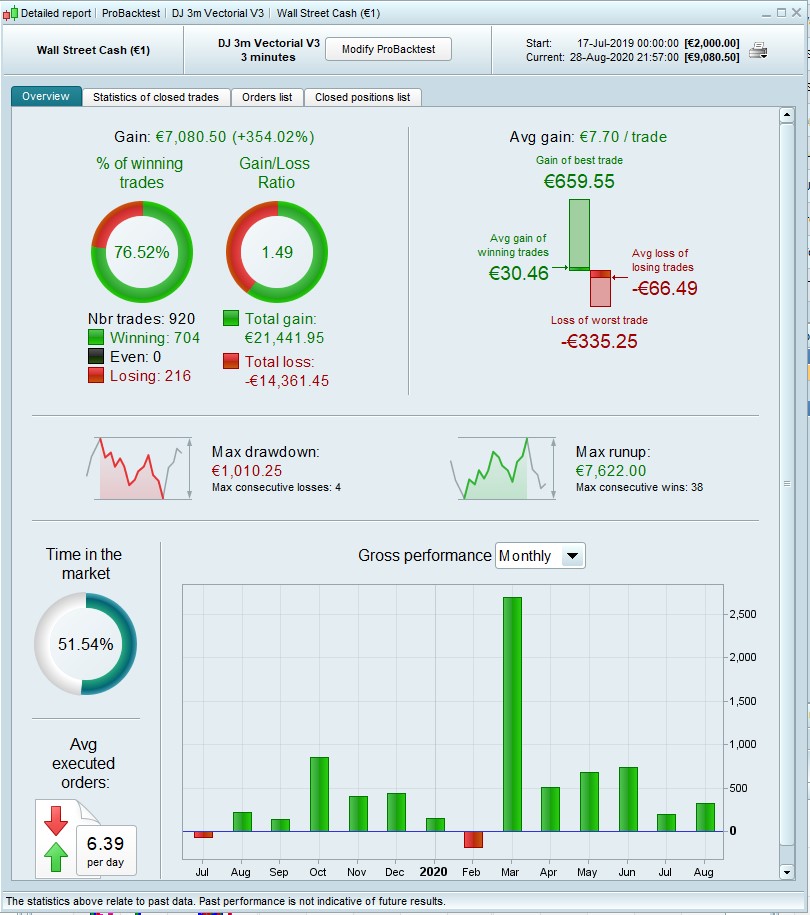

I made a backtest on the DJ 3m Vectorial V3 for the same period and it has been more succesfull.

I also made one of 200 kpts

I find them both interesting!

Thank You @Nonetheless for sharing, it is very interesting as a beginner to se what the more experienced people are doing.

Hi Grahal, how’s it going?

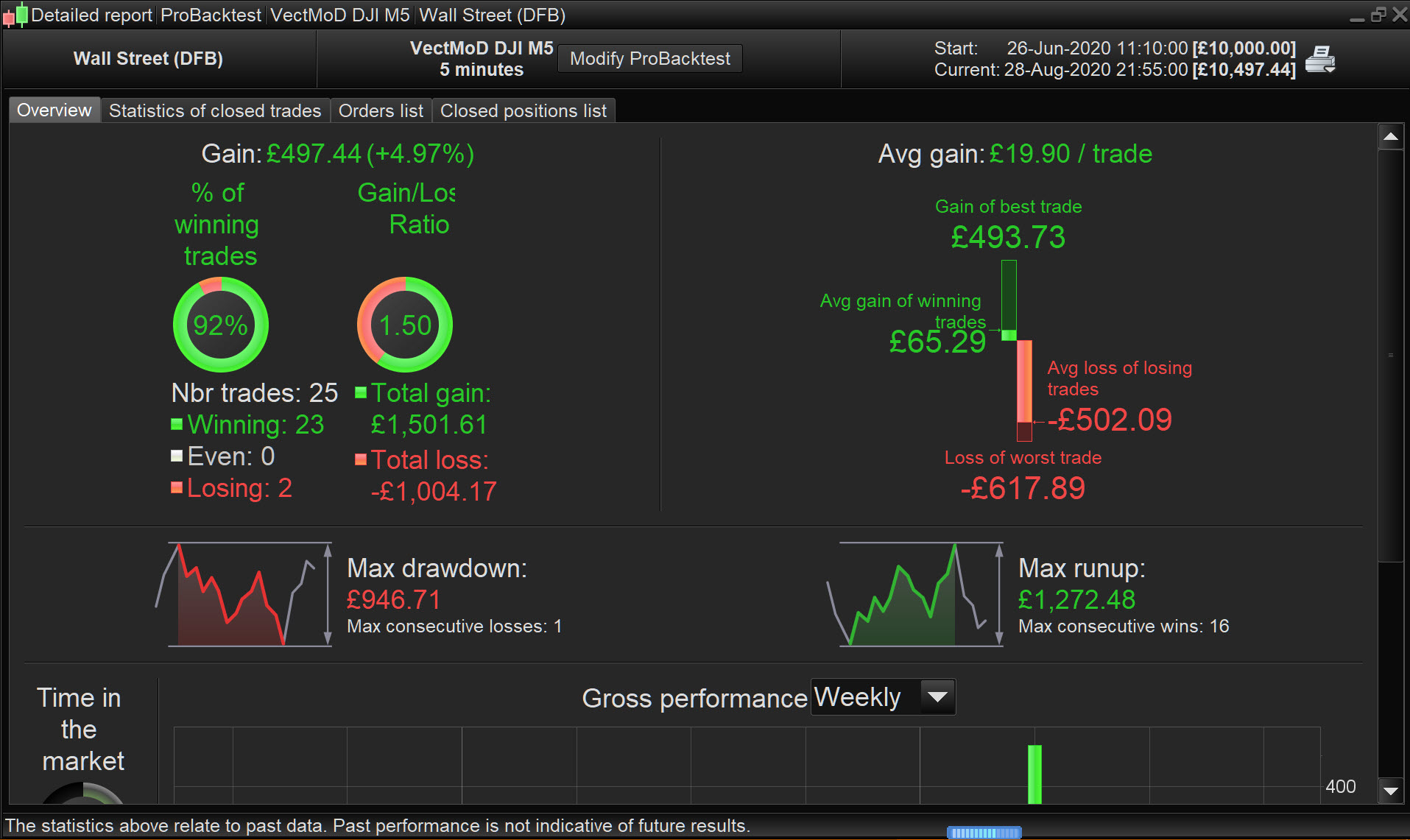

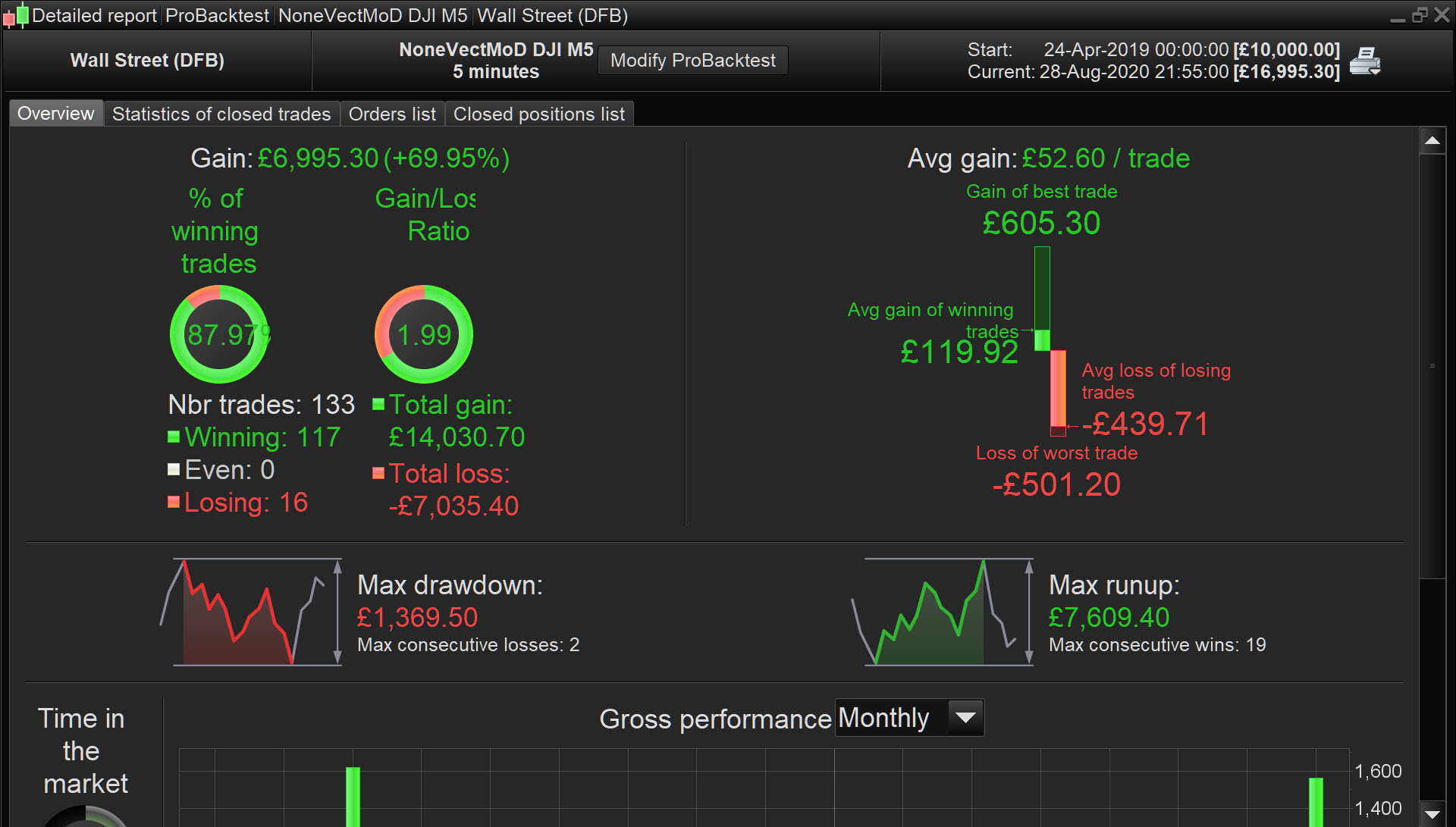

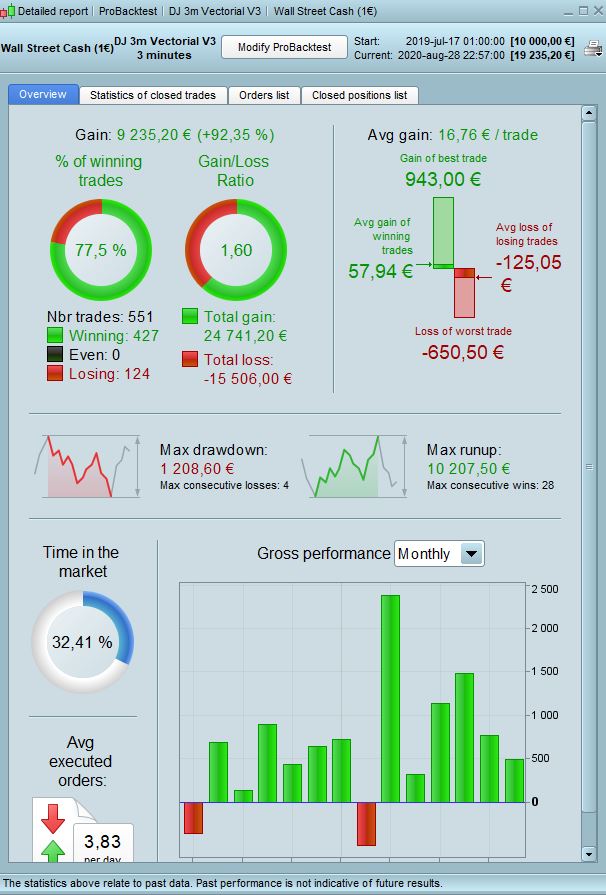

No idea why you got such varying results from this. I have attached the itf, just in case something got corrupted in the copy/paste. Also the 200k back tests for long and short, with a comparison look at the 3m v3. Obviously the latter is only 13 months, as opposed to 32.

I also found some tests that I did back in the spring of the 5m long version … seems to check out. But as I said, I really did this out of curiosity to try marrying Balmora’s Vectorial with MoD … and then I kinda forgot about it.

Both the Vectorial and the MOD are very interesting codes. MOD has a slightly bigger problem with DD but apart from that it has potential. This, and especially the 3 min version is good.

Is there a chance of any further development ?

Ciao Balmora74 vedo che il tuo sistema anche su timeframe ad 1 minuto funziona bene ottimizzato, tu cosa ne pensi?

Hi Balmora74 I see that your system even on 1 minute timeframe works well optimized, what do you think?