Dear Antonio

This is an english channel so please write again but in english

Cheers

Please avoid to quote entire codes, you pollute the topic unnecessarily.

Léo

LéoParticipant

Average

Hi Francesco,

Yes, sorry for this – first time I quote someone. I was expecting that only the text would be copied.

I tried to update my post but could not. Sorry Again.

Alex.

Could you attach the two .itf files? 🙂

Thank you very much.

Paul

PaulParticipant

Master

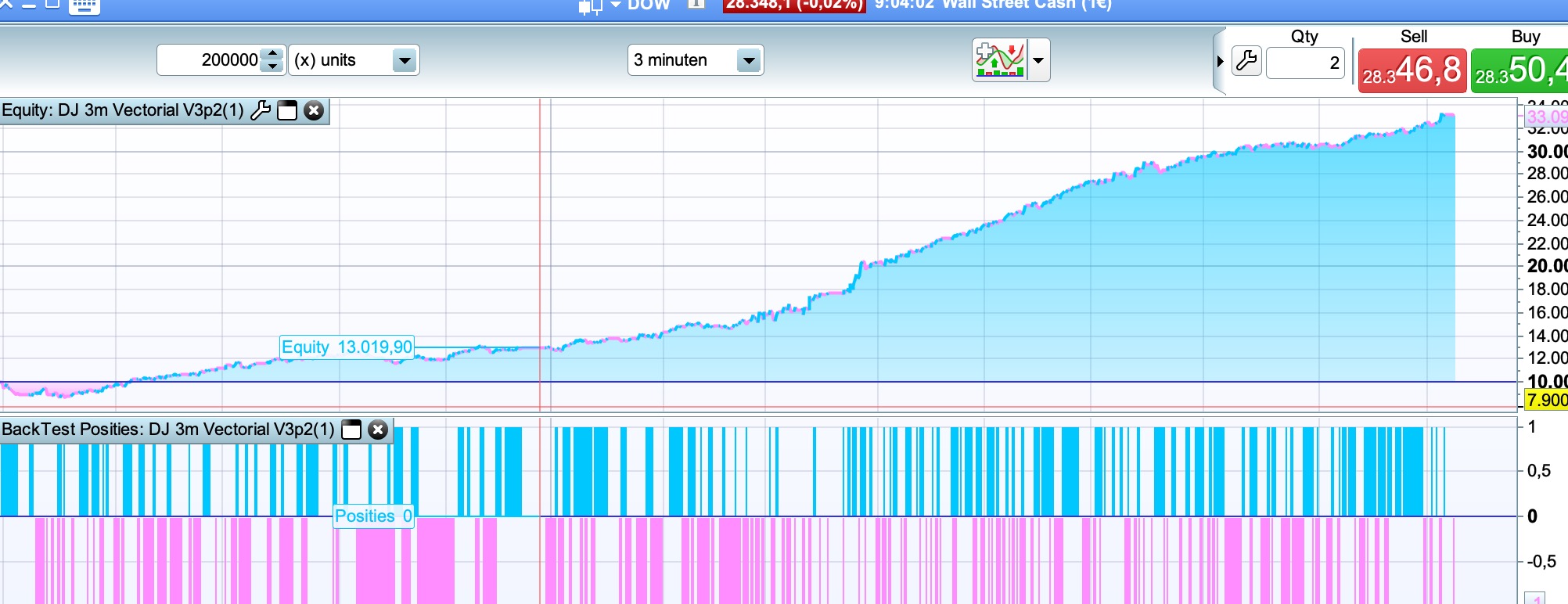

hello, 3min timeframe code can be improved, not by using pente > trigger, but using cross over, that together with pente setting > -xx and <xx as below and not using the breakeven.

cb2 = (pente crosses over trigger) and (pente >-3 and pente < 4)

cs2 = (pente crosses under trigger) and (pente >-4 and pente < 2)

also for the atr trailing stop, I found a small bug which cause the trade to exit too early in a very few cases.

I replace the last part with this. (first row is the change).

if barindex-tradeindex>1 then

if longonmarket then

if tsnewsl>0 then

sell at tsnewsl stop

endif

if tsnewsl>0 then

if low crosses under tsnewsl then

sell at market

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

exitshort at tsnewsl stop

endif

if tsnewsl>0 then

if high crosses over tsnewsl then

exitshort at market

endif

endif

endif

endif

however, using a % trailingstop works just as good, if not better.

Hello,

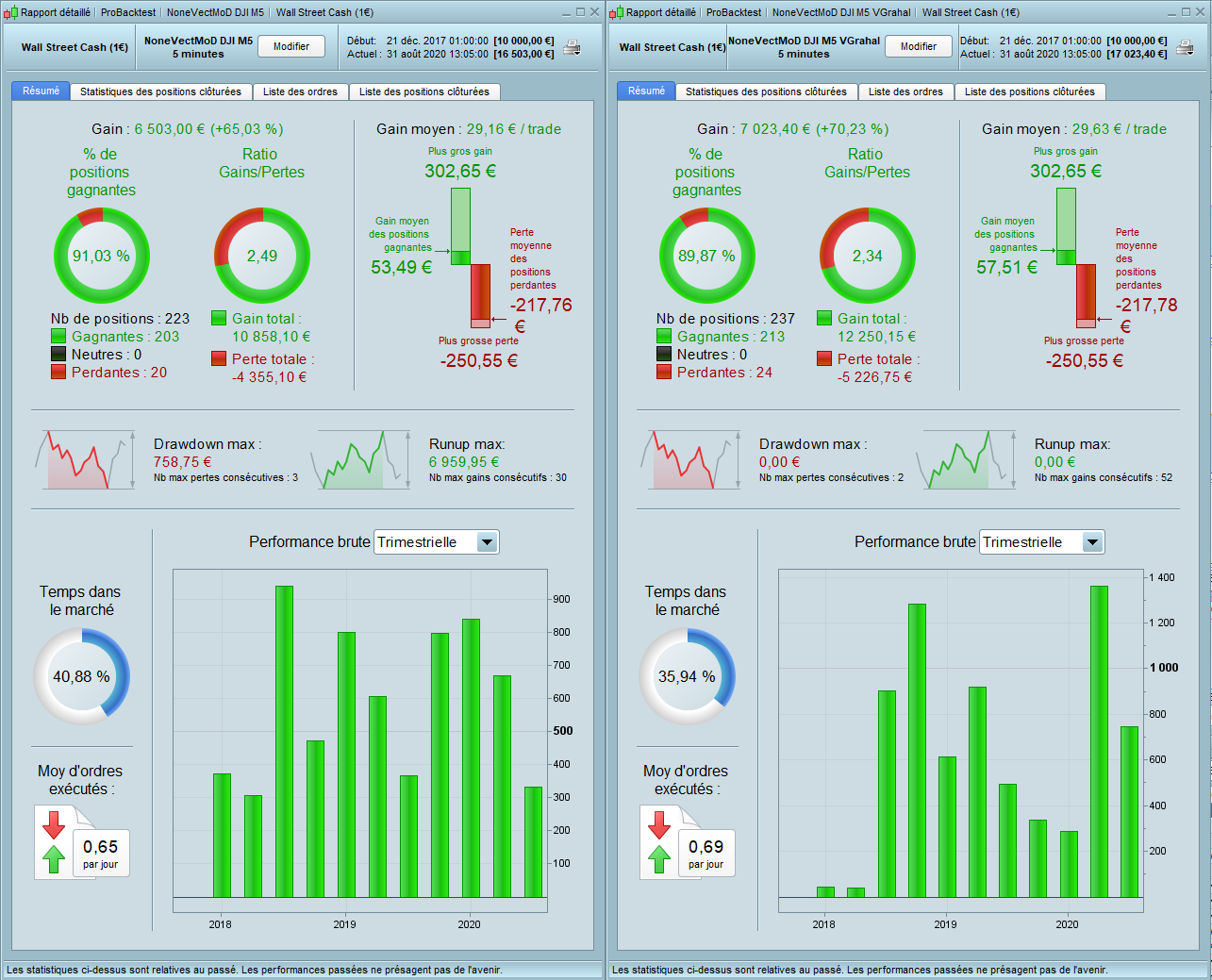

Vectorial DJI 3 minute

After some further testing I have found that by changing the below three variables as follows, you are able to increase the returns of the strategy by 17%

Variables:

tsatrperiod – change from 14 to 12

tsminstop – change from 12 to 10

tsincrements – change from 0.05 to 0.1

Testing Account Parameters:

Account – IG Spread Betting

Capital – 1,000

Position Size – 1

Original strategy on the left of the image, enhanced on the right.

Thank you again to Balmora74 for sharing, and to everyone else for the numerous updates along the way! Most enjoyable exercise.

PaulParticipant

Master

tips are always nice

here’s an other one, don’t use the mx/mx2 averages but use stochastic rsi | indicator

curve is the same with 1% or 2% stoploss

thanked this post

Hi Paul

Would you be so kind as to share the section of code I should replace the mx/mx2 with the stochastic RSI please?

Thank you

PaulParticipant

Master

sure

this is what I use

//stochastic rsi | indicator

if stochasticrsi then

lengthrsi = 2 // 2 rsi period

lengthstoch = 6 // 6 stochastic period

smoothk = 4 // 4 smooth signal of stochastic rsi

smoothd = 8 // 8 smooth signal of smoothed stochastic rsi

myrsi = rsi[lengthrsi](totalprice)

minrsi = lowest[lengthstoch](myrsi)

maxrsi = highest[lengthstoch](myrsi)

stochrsi = (myrsi-minrsi) / (maxrsi-minrsi)

k = average[smoothk](stochrsi)*100

d = average[smoothd](k)

c13 = k>d

c14 = k<d

condbuy = condbuy and c13

condsell= condsell and c14

else

c13=c13

c14=c14

endif

and the code below above the code above

cb1 = angle >= 41

cs1 = angle <= -34

cb2 = (pente crosses over trigger) and (pente >-2 and pente < 4)

cs2 = (pente crosses under trigger) and (pente >-4 and pente < 2)

//entrees en position

condbuy = cb1 and cb2 //and close<>high and high<>dhigh(0)

condsell = cs1 and cs2 //and close<>low and low<>dlow(0)

Hi Paul, could you post your last .ITF file please? Thank you very much.

PaulParticipant

Master

and change nbchandelierb 40 to 41 and it looks better

PaulParticipant

Master

here are the changes above made in the original. On the other one I’am still working.

// VECTORIAL MM - DJ 3m

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 50000

//Money Management

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize=1

ENDIF

if MM = 1 then

ONCE startpositionsize = .2

ONCE factor = 10 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE margin = (close*.05) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.05)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 55 // IG first tier margin limit

ONCE maxpositionsize = 550 // IG tier 2 margin limit

ONCE minpositionsize = .2 // enter minimum position allowed

IF Not OnMarket THEN

positionsize = startpositionsize + Strategyprofit/(factor*margin)

ENDIF

IF Not OnMarket THEN

IF startpositionsize + Strategyprofit/(factor*margin) > tier1 then

positionsize = (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 //incorporating tier 2 margin

ENDIF

IF Not OnMarket THEN

if startpositionsize + Strategyprofit/(factor*margin) < minpositionsize THEN

positionsize = minpositionsize //keeps positionsize from going below allowed minimum

ENDIF

IF (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 > maxpositionsize then

positionsize = maxpositionsize// keeps positionsize from going above IG tier 2 margin limit

ENDIF

ENDIF

ENDIF

ENDIF

//HORAIRES DE TRADING

Ctime = time >= 050000 and time < 230000

//STRATEGIE

//VECTEUR = CALCUL DE L'ANGLE

ONCE PeriodeA = 2

ONCE nbChandelierA= 30

MMA = Exponentialaverage[PeriodeA](close)

ADJASUROPPO = (MMA-MMA[nbchandelierA]*pipsize) / nbChandelierA

ANGLE = (ATAN(ADJASUROPPO)) //FONCTION ARC TANGENTE

CB1 = ANGLE >= 41

CS1 = ANGLE <= - 34

//VECTEUR = CALCUL DE LA PENTE ET SA MOYENNE MOBILE

ONCE PeriodeB = 29

ONCE nbChandelierB= 41

lag = 0

MMB = Exponentialaverage[PeriodeB](close)

pente = (MMB-MMB[nbchandelierB]*pipsize) / nbchandelierB

trigger = Exponentialaverage[PeriodeB+lag](pente)

cb2 = (pente crosses over trigger) and (pente >-2 and pente < 4)

cs2 = (pente crosses under trigger) and (pente >-4 and pente < 2)

//ENTREES EN POSITION

CONDBUY = CB1 and CB2 and CTime

CONDSELL = CS1 and CS2 and Ctime

once stochasticrsi = 1

//stochastic rsi | indicator

if stochasticrsi then

lengthrsi = 2 // 2 rsi period

lengthstoch = 6 // 6 stochastic period

smoothk = 4 // 4 smooth signal of stochastic rsi

smoothd = 8 // 8 smooth signal of smoothed stochastic rsi

myrsi = rsi[lengthrsi](totalprice)

minrsi = lowest[lengthstoch](myrsi)

maxrsi = highest[lengthstoch](myrsi)

stochrsi = (myrsi-minrsi) / (maxrsi-minrsi)

k = average[smoothk](stochrsi)*100

d = average[smoothd](k)

c13 = k>d

c14 = k<d

condbuy = condbuy and c13

condsell= condsell and c14

else

c13=c13

c14=c14

endif

//POSITION LONGUE

IF CONDBUY THEN

buy positionsize contract at market

SET STOP %LOSS 2

ENDIF

//POSITION COURTE

IF CONDSELL THEN

Sellshort positionsize contract at market

SET STOP %LOSS 2

ENDIF

//SET TARGET %PROFIT 2

//Break even

breakevenPercent = .13

PointsToKeep = 1

startBreakeven = tradeprice(1)*(breakevenpercent/100)

once breakeven = 1//1 on - 0 off

//reset the breakevenLevel when no trade are on market

if breakeven>0 then

IF NOT ONMARKET THEN

breakevenLevel=0

ENDIF

// --- BUY SIDE ---

//test if the price have moved favourably of "startBreakeven" points already

IF LONGONMARKET AND close-tradeprice(1)>=startBreakeven*pipsize THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)+PointsToKeep*pipsize

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

SELL AT breakevenLevel STOP

ENDIF

// --- end of BUY SIDE ---

IF SHORTONMARKET AND tradeprice(1)-close>startBreakeven*pipsize THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)-PointsToKeep*pipsize

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

EXITSHORT AT breakevenLevel STOP

ENDIF

endif

// trailing atr stop

once trailingstoptype = 1 // trailing stop - 0 off, 1 on

once tsincrements = .05 // set to 0 to ignore tsincrements

once tsminatrdist = 3

once tsatrperiod = 14 // ts atr parameter

once tsminstop = 12 // ts minimum stop distance

once tssensitivity = 1 // [0]close;[1]high/low

if trailingstoptype then

if barindex=tradeindex then

trailingstoplong = 4 // ts atr distance

trailingstopshort = 4 // ts atr distance

else

if longonmarket then

if tsnewsl>0 then

if trailingstoplong>tsminatrdist then

if tsnewsl>tsnewsl[1] then

trailingstoplong=trailingstoplong

else

trailingstoplong=trailingstoplong-tsincrements

endif

else

trailingstoplong=tsminatrdist

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

if trailingstopshort>tsminatrdist then

if tsnewsl<tsnewsl[1] then

trailingstopshort=trailingstopshort

else

trailingstopshort=trailingstopshort-tsincrements

endif

else

trailingstopshort=tsminatrdist

endif

endif

endif

endif

tsatr=averagetruerange[tsatrperiod]((close/10)*pipsize)/1000

//tsatr=averagetruerange[tsatrperiod]((close/1)*pipsize) // (forex)

tgl=round(tsatr*trailingstoplong)

tgs=round(tsatr*trailingstopshort)

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

tsmaxprice=0

tsminprice=close

tsnewsl=0

endif

if tssensitivity then

tssensitivitylong=high

tssensitivityshort=low

else

tssensitivitylong=close

tssensitivityshort=close

endif

if longonmarket then

tsmaxprice=max(tsmaxprice,tssensitivitylong)

if tsmaxprice-tradeprice(1)>=tgl*pointsize then

if tsmaxprice-tradeprice(1)>=tsminstop then

tsnewsl=tsmaxprice-tgl*pointsize

else

tsnewsl=tsmaxprice-tsminstop*pointsize

endif

endif

endif

if shortonmarket then

tsminprice=min(tsminprice,tssensitivityshort)

if tradeprice(1)-tsminprice>=tgs*pointsize then

if tradeprice(1)-tsminprice>=tsminstop then

tsnewsl=tsminprice+tgs*pointsize

else

tsnewsl=tsminprice+tsminstop*pointsize

endif

endif

endif

if longonmarket then

if tsnewsl>0 then

sell at tsnewsl stop

endif

if tsnewsl>0 then

if low crosses under tsnewsl then

sell at market // when stop is rejected

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

exitshort at tsnewsl stop

endif

if tsnewsl>0 then

if high crosses over tsnewsl then

exitshort at market // when stop is rejected

endif

endif

endif

endif

Hi Paul,

Apologies, how do you define stochasticrsi please?

//stochastic rsi | indicator

if stochasticrsi then

…….

Thank you