Hi All,

Great to see fellow HE subs trying to back solve the RR and signal lines. I’ve been trying to do this solo for nearly three years, imagine my joy I stumbled across this thread!

My findings so far are below on both the Risk Range and the signal lines (Trade/Trend/Tail), I hope this helps the debate and understanding for everyone.

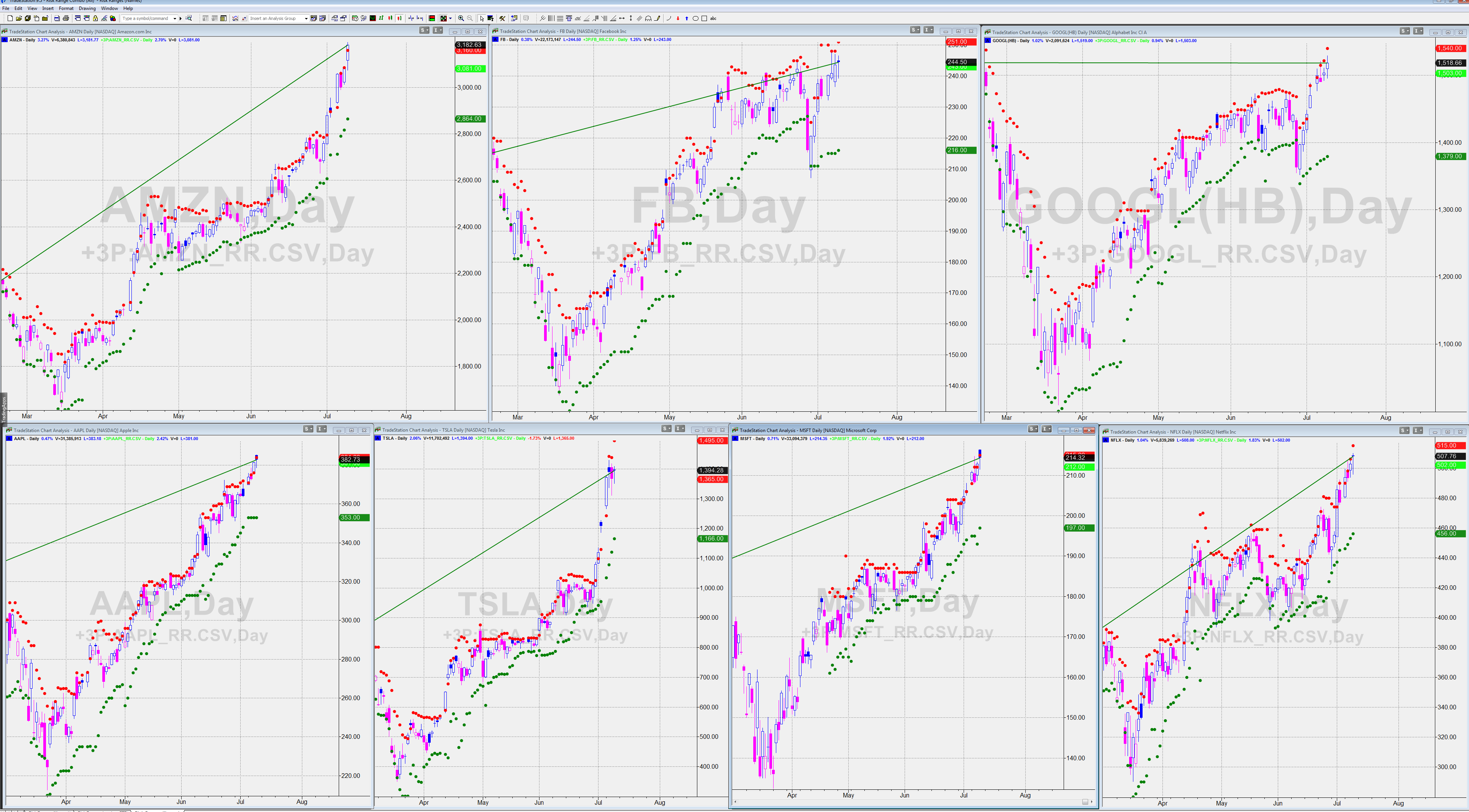

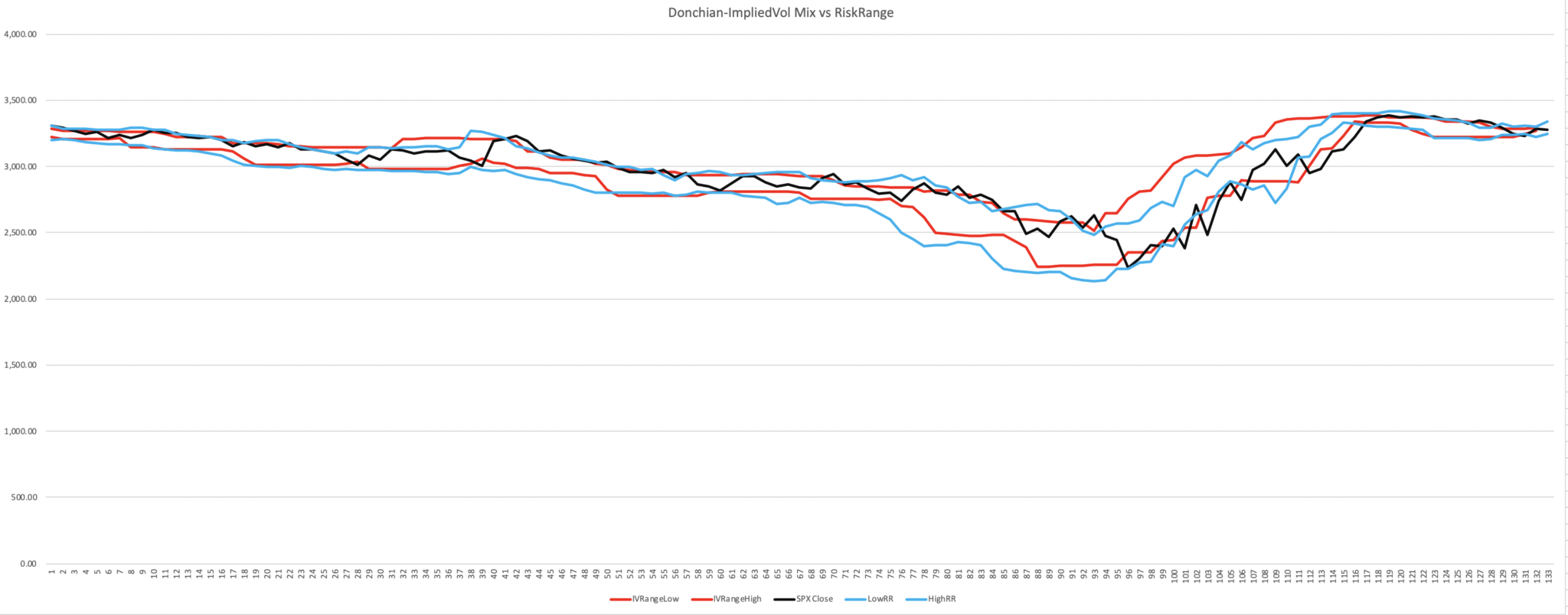

Risk Range

The Volatility parameter is the Implied Volatility for that asset scaled down to daily. Currencies and Treasuries might be a bit harder for some to get, but they do exist (mainly OTC derivatives). Remember the VIX is a weighted aggregate options of the S&P 500, not the index itself. So if you can get S&P 500 IVOL, use thatm if not then the VIX will suffice.

I have used realised volatility as a substitute when there is no options market readily available.

On the Hurst Exponent, I’m thinking this is a scaling factor of volatility, a power-law relationship. H is equivalent to 1/alpha in fractal math e.g is H = 0.5, alpha = 2. So if H<0.5 this would provide a wider range for a security which is mean-reverting and a narrow one for those that are trending strongly.

The range itself is around a dynamic moving average. I’m thinking this has to do with fractal time (“Risk happens slowly, then all at once”, the “or” when KM mentions the duration). It is discussed in the Behaviour of Markets. Haven’t worked the math out yet, my skills are not what they used to be when I was at university! I have tried Volatility & Volume Weighted Moving Averages, but it’s not really solving the issue at hand and overcomplicating the Volatility and Volume aspect of it. IMO, VWAP falls into the same boat here.

I’m not sure where the skew in the range comes from, but I know it does not come from using the Max/Min used in the Rescaled Range calculation. Tried that and it produced a mess.

On the Vol of Vol, I don’t think this is VVIX or equivalent but the evolution of volatility over time and is not involved in the calculation.

On volume, I am not sure how this works with FX and Bonds. It could be a variable, but I think it is the same as Vol of Vol, e.g. Daily volume was down X% vs the 1M average, and the range is signalling a lower high etc.

The “trend” range I’d imagine would use front-month options still as they are more frequently traded vs the quarterly options but only time will tell.

Signal Lines

This is where the 1-month, 3-month, 6-month and longer momentum chasing comes in! The goal is to find the threshold prior to when these systems will flip, it’s not too dissimilar in principle from Charlie M’s (from Nomura) CTA model.

CTA’s and Hedge Funds will often use a weighting system for their momentum systems. Watch MAN AHL’s Quant series on YouTube for more info. In theory, an implied price, P*, could be determined with averaging the momentum durations. This is my line of thought behind what KM is using, he is trying to find P*. This does work somewhat on its own (currently this what I use in the interim) and is similar to a Moving Average but it neglects the role of factors they have on an asset’s momentum 😉

In 2011 KM did provide a hint of what was in his model in the book The StockTwist Edge. KM’s chapter is called Trade, Trend, Tail (https://www.oreilly.com/library/view/the-stocktwits-edge/9781118029053/09_c02.html\)

In that book, he mentioned that there were 27 factors overlayed with the volume and volatility. I think that these 27 factors are Macro in nature e.g. US Equities, CRB Index, Global Equities, 10Y Treasury, DXY, Momentum, Volatility Factor (not volatility itself but High/Low Volatility) etc. Also IRC he did mention that variables on The Macro Show 12 to 18 months ago that are in Trend do not always appear in Trade or Tail lines, eg. Inflation & GDP could make an appearance in Tail for example.

My hypothesis is that he finds P* from individually regressing each factor against the security and does a weighted average based on Correlation^2 or abs(Correlation) for the asset in question to filter what matters to the asset.

Price, Volume and Volatility each have their own individual regressions. The four sub-models are then combined in some form of a weighted average.

It looks complicated, because well it is! When he developed this, not many people knew about factors (mid-2000’s) outside of Hedgies and academics. I inadvertently had done something similar with an FX model I developed in 2017, so this is where my line of thought comes from.

I know its a long post, thanks for reading.

Kauri