But what I can’t figure out is why – if your Algo is as good as you show above – are you still selling papers!!!! 🙂 🙂 🙂

Over a couple of beers, the still honest answers are :

- It is very tough to let outpaste the manual trading by auto-trading (but auto is a 100 times more fun – so is the paperwork already !! (really so));

- What I have and showed is for PRT-IB – for PRT-IG this does not work at all (explaining that is for elsewhere but just saying : it is NOT related to spreads (IG) vs. commission (IB)) … but PRT-IB is now a year over-due with its auto-trading. So I let this happily run and a. become virtually auto-rich and b. have a best case of forward testing.

- I forgot – probably something with beers.

Addendum (and for more LYAO) :

I have seriously worked out what would happen if this really “grows” on me. You might be surprised what’s all against it / what will work against you. The main issue is that people will find out automatically (for example, I would be doing as much turn over as the whole of PRT-IB won’t do, mind you, this is ~33 trades of 10M per day, right ?) and others somewhere more close to an exchange for the whatever you trade, will be faster with it (less latency). I think I have this covered though, but this requires an other specialty (sit tight) :

What I have been doing the past year, is work on explicit means of parameters (but say variables which control the algo), on behalf of you guys and gals. Or maybe : as a selling point for that “algo” I seem to have, which are an endless number because of those parameters. Now envision that I give you a fixed version of it, say the same as what I am using now. What will happen ?

Well, we would all be doing the exact same trades. And this is impossible, so probably many losers will be among us (all but one ? not sure).

And so I decided to bring you a parametrized version with some basic set that may play break-even or not make profit at all. Next it is up to yourselves to tune it into something which makes profit and that for the instrument you’d like yourself (that already requires parametrization). Anyway, even for trading all the same instrument, this would lead to a randomized trade pattern, and we won’t be in each others way explicitly. Still it would be so that not everyone can win, but with Fx there’s really sufficient depth for the few PRT traders. And next we’d outsmart each other. Btw, for me this is the biggest fun of auto-trading – outsmart the system.

So you’d be having a real platform for auto-trading which does not require programming – only parameters settings (I did not count, but 30-40 or so). Not sure whether this is new, but I was challenged by the whole “Market Place” idea.

Btw, I would not let this go out before sufficiently trying it in the real $ world. I mean, I would not like to be responsible for people losing 2K on a 25 investment which benefits me. The least I should do in that case is refunding the 25 (just saying – for others to maybe pick up) but which really does not help on a 2K loss.

In the very end it is somewhat more complicated because when do you/we decide that an algo does not work ? is this after 3 subsequent losses setting you back for 2K immediately ?

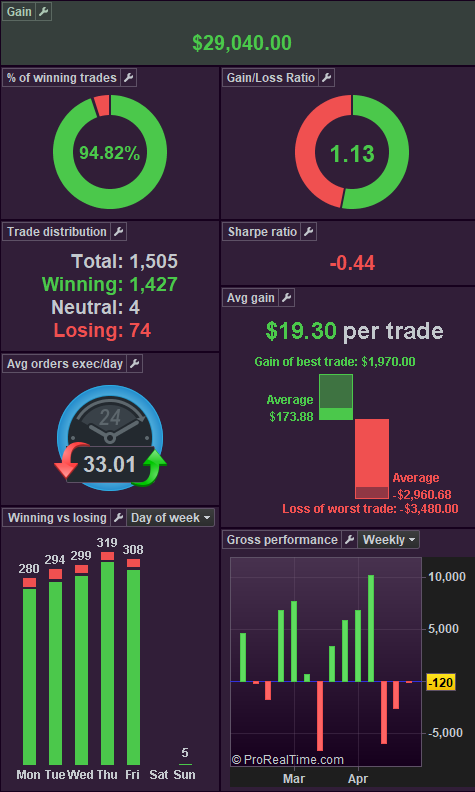

So look at the first attachment for fun. Say that you started the algo (any from anyone) at 09:00 on Feb 12. There goes your 10K investment, right ? you will be broke within two days and the algo clearly does not work at all. But why ? well, because you thought to do it with 10K. Throws 100K at it, and the second attachment will be your share (it vertically does not fit on my screen). So what’s the problem with those 4 losses now ? Notice that the top of the list contains trades as those shown in the first attachment.

It is no news that no matter an algo may look good to you, you must test test test and test even more. Preferably forward only. You need to be able to digest bigger losses. If you can’t, don’t start with this for real (but have fun in the paper environment).

As a bonus you see in the third attachment the real-life performance of the 100% same algo on the 100% same instrument, now running under PRT-IG. The investment (per trade) is here 200K only (1M in the above mentioned) and the loss is EUR 1565. That loss of 1565 is is fine for me, but the relationship with the number of trades already is off. Thus, not talking about the Profit/Loss ratio yet, the number of trades “taken” in 3 weeks of time is totally off compared to the IB version (I know what causes this, but for an other day). Thus, something like 3300 trades in 100 days for the IB version and 128 trades in 21 days for the IG version, gives a relation of 3300:600 or so. The IG version is too much boring already ! haha. It can thus also be that I did not give the IG version the opportunity to recover from that 1500 loss (which is only 3 losses less – ad EUR 550 per time – to break even).

So now you know the reason for me liking paperwork better. 🙂