Hi all,

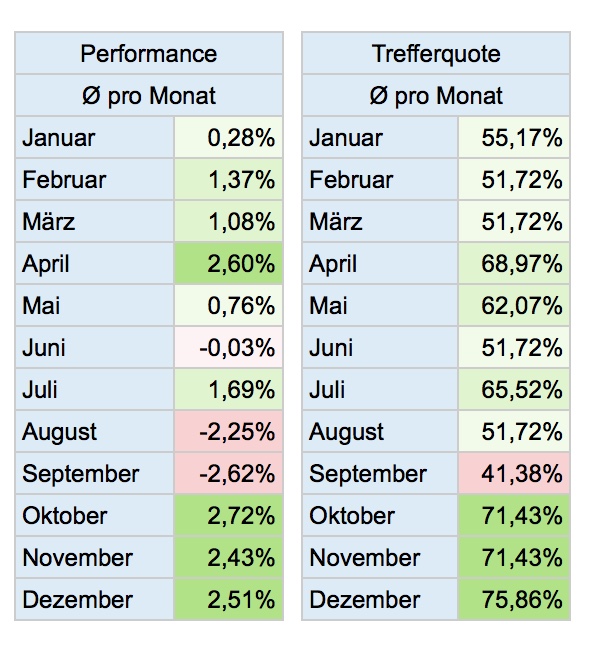

I realized that the consideration of saisonal behavior could be an advantage for all mid and longterm strategies. Please find attached the monthly average DAX return and hit rate over the last 30 years (since 1987). Pathfinder consider this pattern with the following settings:

// define saisonal position multiplier >0 - long / <0 - short / 0 no trade

ONCE January = 2

ONCE February = 2

ONCE March = 2

ONCE April = 3

ONCE May = 2

ONCE June = 2

ONCE July = 3

ONCE August = -1

ONCE September = -2

ONCE October = 1

ONCE November = 3

ONCE December = 3

When a trade signal is present the algorithm check the saisonal pattern and calculate the appropriate position size. For example November delivered historical strong results on the long side and Pathfinder will booster the position size with multiplier 3 for each long trade. Saisonal pattern could be a statistical edge but of course isn’t the holy grail or a 100% guarantee as the DAX showed this August/September.

best, Reiner

Hi Reiner,

I’m looking into having different strategies running simultaneously using the same capital. It would be interesting to compare DAX, DOW, FTSE and CAC for each month to find the worst month combined to calculate the minimum capital needed plus some extra safety capital on top.

The idea then is that it wouldn’t hurt to have CAC running along with the other strategies despite a long sideway range.

Combining the best strategies this way along with smart positioning when capital increase who knows what gain we could be looking at!

Thanks,

Mikael

reb

rebParticipant

Master

Hi Michael

As proposal you can calculate the needed minimum capital : the number max of contracts that the strategy can take multiplied by a average week variation of the index

Regards,

Reb

Hi reb and Everyone 🙂

How do I export the backtest data? I’m good with Excel so then I could calculate formulas to compare different strategies together on the timeline.

Even the Pathfinder results from gold and oil is not discouraging as long as it’s not moving downways. Combined strategies could weigh against each other in the same way for monthly saisonal positions where DAX obviously would be rated highest.

Combining correct strategies would also possibly flatten out the overall drawdown during different time periods. Obviously I need Excel to find out and easily compare everything!

Thanks,

Mikael

wp01

wp01Participant

Master

Mikael,

You open Excel end the closed position list and you drag it into your Excel.

If that is what you mean.

regards,

Patrick

As it has already said reiner European indices are related therefore in my opinion and’ useless to play on so many similar indices in the end the result is the same. it would be more fair instead diversify ideal and DAX GOLD OIL WALL STREET those who want to enter again FTSE100 and Hangseng.

Come ha gia’ detto reiner gli indici europei sono correlati pertanto a mio avviso e’ inutile giocare su tanti indici simili alla fine il risultato e lo stesso . sarebbe piu giusto invece diversificare ideale e DAX GOLD OIL WALL STREET chi vuole inserire ancora FTSE100 e HANGSENG

Thanks wp01. Didn’t know it was that easy! 🙂

Miguel, yes the relations between European indices might be problem but still they somehow triggers slightly different. Diversify with gold and oil for example sounds like a better idea.

Let’s find out what Excel says about it!

Thanks,

Mikael

Hi Mikael!

Don´t know if you already seen it but Reiner has tweaked the Pathfinder strategy to OMXS30.

Du får gärna mejla mig på tilltims at hotmail.com om du känner för det

/Tim

HI Reiner,

Is it necessary to have 10k on the account to use pathfinder or could it be used with for example a 5k capital?

/Trader

Nyb,you can also start with € 2,000.00

Reiner

It can also work with any forex currency pair ?

Thanks for clarification Miguel,

Im only trading manually at the moment but are interested in automated trading and coding, however only learning yet and won’t trade automatically for quite a while yet.

I think I will try this code in demo though, could you help me by sharing what needs to be adapted in the code for set it up for 2000 instead of 10000, maybe positiong size and so on should be adapted also and not only the initial capital?

Nothing changes . I live with € 2,000 starting

rebParticipant

Master

Be careful Nyborjare1981 and miguel33, we have already had this discussion with Reiner in this post.

If the strat opens 15 trades with your capital of 2k, you will have a range of 130 points.

A daily average variation on the dax is around 150 pts

So in one day, you may kill your account

To my opinion, you need a minimum 10k capital and 15k is better, under this level you are playing gambling casino.

Reb

Thanks reb 🙂

So to adjust the pathfinder for a 2k capital would be maybe to limit the 15 open trades to for example as little as 2 open trades?