the system becomes more and more balanced and reliable. big work. thank you

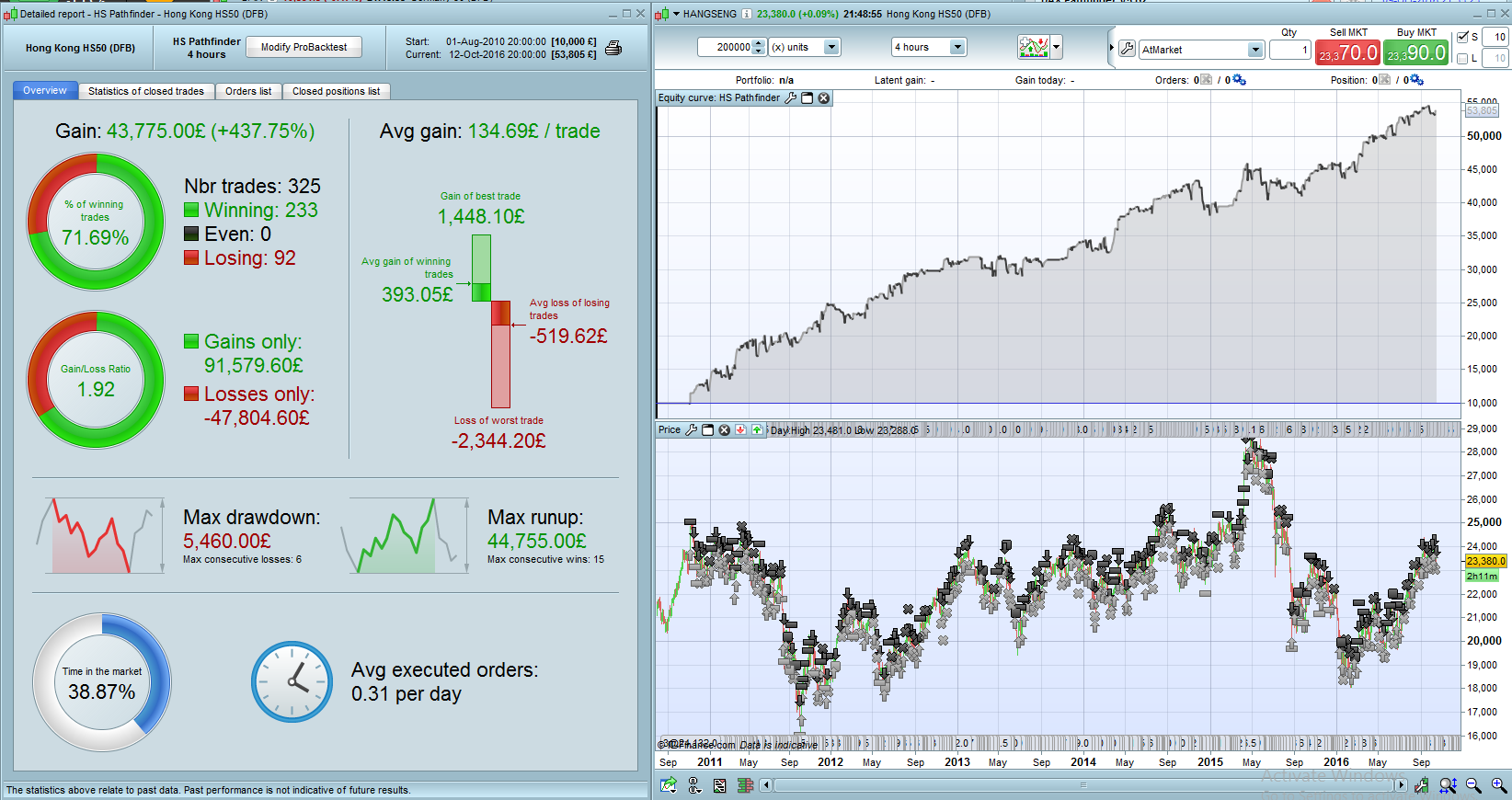

I try to improve Pathfinder for instruments with changing trends and big moves on both sides. Hang Seng index is such an instrument that is perfect suitable for testing. I’m a little bit confused about the backtest result > 4.000% profit in 4 years. I never traded HS and therefore the question to the HS pros: Is that realistic?

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 5 Beta 3

// Instrument: Hang Seng mini 4H, 2:15-16:45 CET, 6 points spread, account size 10.000 Euro

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 21500

ONCE endTime = 164500

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 8

// define filter parameter

ONCE periodLongMA = 380

ONCE periodShortMA = 30

// define position and money management parameter

ONCE positionSize = 1

Capital = 10000

Risk = 5 // in %

equity = Capital + StrategyProfit

maxRisk = round(equity * Risk / 100)

ONCE stopLossLong = 3.25 // in %

ONCE stopLossShort = 2.75 // in %

ONCE takeProfitLong = 2 // in %

ONCE takeProfitShort = 2.25 // in %

maxPositionSizeLong = MAX(5, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

maxPositionSizeShort = MAX(5, abs(round(maxRisk / (close * stopLossShort / 100) / PointValue) * pipsize))

ONCE trailingStartLong = 1.75 // in %

ONCE trailingStartShort = 1 // in %

ONCE trailingStepLong = 0.2 // in %

ONCE trailingStepShort = 0.2 // in %

ONCE maxCandlesLongWithProfit = 20 // take long profit latest after 20 candles

ONCE maxCandlesShortWithProfit = 13 // take short profit latest after 13 candles

ONCE maxCandlesLongWithoutProfit = 30 // limit long loss latest after 30 candles 30

ONCE maxCandlesShortWithoutProfit = 6 // limit short loss latest after 6 candles

// define saisonal position multiplier >0 - long / <0 - short / 0 no trade

ONCE January = 2

ONCE February = 2

ONCE March = 2

ONCE April = 3

ONCE May = 2

ONCE June = 2

ONCE July = 3

ONCE August = -1

ONCE September = -2

ONCE October = 1

ONCE November = 3

ONCE December = 3

// calculate daily high/low (include sunday values if available)

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// save position before trading window is open

If Time < startTime then

startPositionLong = COUNTOFLONGSHARES

startPositionShort = COUNTOFSHORTSHARES

EndIF

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// set saisonal pattern

IF CurrentMonth = 1 THEN

saisonalPatternMultiplier = January

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplier = February

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplier = March

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplier = April

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplier = May

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplier = June

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplier = July

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplier = August

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplier = September

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplier = October

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplier = November

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplier = December

ENDIF

// define trading filters

// 1. use fast and slow averages as filter because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

f4 = signalline < Average[periodshortMA](close)

// 2. check if position already reduced in trading window as additonal filter criteria

alreadyReducedLongPosition = COUNTOFLONGSHARES < startPositionLong

alreadyReducedShortPosition = COUNTOFSHORTSHARES < startPositionShort

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s4 = signalline CROSSES UNDER dailyHigh

s5 = signalline CROSSES UNDER dailyLow

// long entry with order cumulation

IF ( (l1 OR l4 OR l2 OR (l3 AND f2) ) AND NOT alreadyReducedLongPosition) THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier > 0 THEN

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry with order cumulation

IF ((s1 AND f3) OR (s5 AND f1) OR (f4 AND (s4 AND f2)) ) AND NOT alreadyReducedShortPosition THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier < 0 THEN

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

IF LONGONMARKET THEN

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

ELSIF SHORTONMARKET THEN

posProfit = (((positionprice - close) * pointvalue) * countofposition) / pipsize

ENDIF

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

// trailing stop function

trailingStartLongInPoints = tradeprice(1) * trailingStartLong / 100

trailingStartShortInPoints = tradeprice(1) * trailingStartShort / 100

trailingStepLongInPoints = tradeprice(1) * trailingStepLong / 100

trailingStepShortInPoints = tradeprice(1) * trailingStepShort / 100

// reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

ENDIF

// manage long positions

IF LONGONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND close - tradeprice(1) >= trailingStartLongInPoints * pipsize THEN

newSL = tradeprice(1) + trailingStepLongInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND close - newSL >= trailingStepLongInPoints * pipsize THEN

newSL = newSL + trailingStepLongInPoints * pipsize

ENDIF

ENDIF

// manage short positions

IF SHORTONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND tradeprice(1) - close >= trailingStartShortInPoints * pipsize THEN

newSL = tradeprice(1) - trailingStepShortInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND newSL - close >= trailingStepShortInPoints * pipsize THEN

newSL = newSL - trailingStepShortInPoints * pipsize

ENDIF

ENDIF

// stop order to exit the positions

IF newSL > 0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

// superordinate stop and take profit

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

I think the hang seng index is for us Europeans to trade or difficult to follow. It would be more useful to examine in addition to the FTSE100 and DAX Wall street and then begin to see better OIL, GOLD and SILVER. As always good job Reiner. thank you.

Miguel

Ok, it’s clear now. Hang Seng backtest results are in HK$ and this mean that initial capital has to converted to HK$ as well (multiplied by 10). The performance is around 400% and not 4.000%. Sorry for the confusion.

@miguel: as mentioned above the topic isn’t to develop a fancy Hang Seng backtest, the aim is to improve the results under “stormy” conditions. Hang Seng had a wild ride over the last 3 -4 years and is perfect to hardening Pathfinders behavior esspecially in tough downtrends.

Also works on 200k units. Good test.

It’s actually a good one to run on demo to see how it goes. The spread varies from 6-20 points at various times of the day for UK spread bet. Same for Europeans?

Yes, correct. Though adjusted for CEST, so 2.15-5.00 and so on.

Just want to say thanks to Reiner and you all for this great work on a very interesting code. Looking forward to coming progress:)

I have seen that some guys are interested to test Pathfinder V5 with Hang Seng in demo mode.

Here is an improved backtest version. Spread of 10 points is now a more realistic value and the drawdown looks much better now. Nevertheless drawdown is significant but the return is also exceptionally good . I recommend 100.000 HKD as capital. Tests did show that it’s important for the result to let it run until 1600 (New York’s open).

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 5 Beta 3

// Instrument: Hang Seng mini 4H, 2:15-16:00 CET, 10 points spread, account size 100.000 HKD

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 21500

ONCE endTime = 160000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 8

// define filter parameter

ONCE periodLongMA = 380

ONCE periodShortMA = 30

// define position and money management parameter

ONCE positionSize = 1

Capital = 10000

Risk = 5 // in %

equity = Capital + StrategyProfit

maxRisk = round(equity * Risk / 100)

ONCE stopLossLong = 3.25 // in %

ONCE stopLossShort = 2 // in %

ONCE takeProfitLong = 2.25 // in %

ONCE takeProfitShort = 2.25 // in %

maxPositionSizeLong = MAX(6, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

maxPositionSizeShort = MAX(6, abs(round(maxRisk / (close * stopLossShort / 100) / PointValue) * pipsize))

ONCE trailingStartLong = 1.75 // in %

ONCE trailingStartShort = 1 // in %

ONCE trailingStepLong = 0.2 // in %

ONCE trailingStepShort = 0.2 // in %

ONCE maxCandlesLongWithProfit = 20 // take long profit latest after 20 candles

ONCE maxCandlesShortWithProfit = 13 // take short profit latest after 13 candles

ONCE maxCandlesLongWithoutProfit = 25 // limit long loss latest after 25 candles

ONCE maxCandlesShortWithoutProfit = 6 // limit short loss latest after 6 candles

// define saisonal position multiplier >0 - long / <0 - short / 0 no trade

ONCE January = 1

ONCE February = 1

ONCE March = 1

ONCE April = 3

ONCE May = 1

ONCE June = 1

ONCE July = 3

ONCE August = -1

ONCE September = -2

ONCE October = 1

ONCE November = 3

ONCE December = 2

// calculate daily high/low (include sunday values if available)

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// save position before trading window is open

If Time < startTime then

startPositionLong = COUNTOFLONGSHARES

startPositionShort = COUNTOFSHORTSHARES

EndIF

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// set saisonal pattern

IF CurrentMonth = 1 THEN

saisonalPatternMultiplier = January

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplier = February

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplier = March

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplier = April

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplier = May

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplier = June

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplier = July

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplier = August

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplier = September

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplier = October

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplier = November

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplier = December

ENDIF

// define trading filters

// 1. use fast and slow averages as filter because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

f4 = signalline < Average[periodshortMA](close)

// 2. check if position already reduced in trading window as additonal filter criteria

alreadyReducedLongPosition = COUNTOFLONGSHARES < startPositionLong

alreadyReducedShortPosition = COUNTOFSHORTSHARES < startPositionShort

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s4 = signalline CROSSES UNDER dailyHigh

s5 = signalline CROSSES UNDER dailyLow

// long entry with order cumulation

IF ( (l1 OR l4 OR l2 OR (l3 AND f2) ) AND NOT alreadyReducedLongPosition) THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier > 0 THEN

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry with order cumulation

IF ((s1 AND f3) OR (s5 AND f1) OR (f4 AND (s4 AND f2)) ) AND NOT alreadyReducedShortPosition THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier < 0 THEN

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

IF LONGONMARKET THEN

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

ELSIF SHORTONMARKET THEN

posProfit = (((positionprice - close) * pointvalue) * countofposition) / pipsize

ENDIF

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

// trailing stop function

trailingStartLongInPoints = tradeprice(1) * trailingStartLong / 100

trailingStartShortInPoints = tradeprice(1) * trailingStartShort / 100

trailingStepLongInPoints = tradeprice(1) * trailingStepLong / 100

trailingStepShortInPoints = tradeprice(1) * trailingStepShort / 100

// reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

ENDIF

// manage long positions

IF LONGONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND close - tradeprice(1) >= trailingStartLongInPoints * pipsize THEN

newSL = tradeprice(1) + trailingStepLongInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND close - newSL >= trailingStepLongInPoints * pipsize THEN

newSL = newSL + trailingStepLongInPoints * pipsize

ENDIF

ENDIF

// manage short positions

IF SHORTONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND tradeprice(1) - close >= trailingStartShortInPoints * pipsize THEN

newSL = tradeprice(1) - trailingStepShortInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND newSL - close >= trailingStepShortInPoints * pipsize THEN

newSL = newSL - trailingStepShortInPoints * pipsize

ENDIF

ENDIF

// stop order to exit the positions

IF newSL > 0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

// superordinate stop and take profit

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

wp01

wp01Participant

Master

Many thanks for the latest code Reiner.

With the same startingdate and HKD100K in the backtest + 10points spread my report shows a different outcome. Less profit and more trades.

Regards,

hey reiner,

ich würde gerne dabei helfen pathfinder für andere instrumente anzupassen, aber es gibt so viele variablen die man anpassen kann, dass ich gar nicht weiß wo ich anfangen soll/kann/muss.

bei dir scheint das ja immer recht gut zu funktionieren 😉 hast du mir vllt einen tipp in welcher reihenfolge du dabei vorgehst?

danke

flo

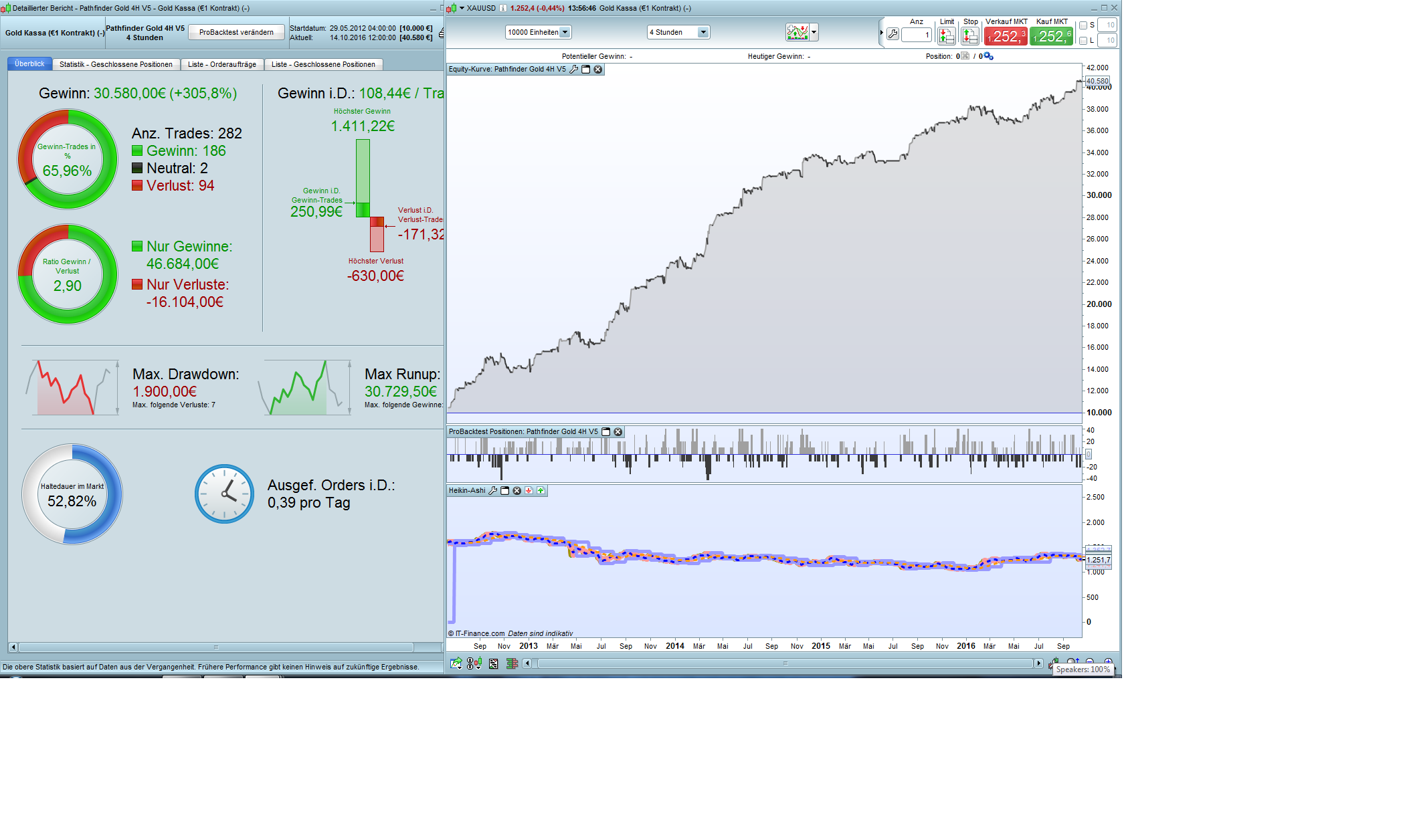

Here is a first Pathfinder version for Gold mini. It would be great if somebody with longer history could verify the backtest result. Return (300% in 4 years) and drawdown (<20%) are OK but number of profitable trades is best case 66%. Pathfinder loses money as probable many systems when long term trend changes (7 loosers in a row Feb-March 16). Please be aware that the minimum contract size for Gold mini is 10 contracts.

Gold won’t be my favorit for Pathfinder.

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 5 Beta 3

// Instrument: Gold mini 4H, 2-22 CET, 0.3 points spread, account size 10.000 Euro

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 20000

ONCE endTime = 220000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 7

// define filter parameter

ONCE periodLongMA = 270

ONCE periodShortMA = 40

// define position and money management parameter

ONCE positionSize = 10 // 10 contracts are the minimum size for Gold mini

Capital = 10000

Risk = 5 // in %

equity = Capital + StrategyProfit

maxRisk = round(equity * Risk / 100)

ONCE stopLossLong = 3.25 // in %

ONCE stopLossShort = 2.75 // in %

ONCE takeProfitLong = 2 // in %

ONCE takeProfitShort = 4 // in %

maxPositionSizeLong = MAX(40, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

maxPositionSizeShort = MAX(40, abs(round(maxRisk / (close * stopLossShort / 100) / PointValue) * pipsize))

ONCE trailingStartLong = 1 // in %

ONCE trailingStartShort = 2 // in %

ONCE trailingStepLong = 0.7 // in %

ONCE trailingStepShort = 0.7 // in %

ONCE maxCandlesLongWithProfit = 20 // take long profit latest after 20 candles

ONCE maxCandlesShortWithProfit = 20 // take short profit latest after 13 candles

ONCE maxCandlesLongWithoutProfit = 30 // limit long loss latest after 30 candles 30

ONCE maxCandlesShortWithoutProfit = 14 // limit short loss latest after 6 candles

// define saisonal position multiplier >0 - long / <0 - short / 0 no trade

ONCE January = 2

ONCE February = 2

ONCE March = -1

ONCE April = 1

ONCE May = 1

ONCE June = 2

ONCE July = 3

ONCE August = 2

ONCE September = 3

ONCE October = -2

ONCE November = 1

ONCE December = 1

// calculate daily high/low (include sunday values if available)

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// save position before trading window is open

If Time < startTime then

startPositionLong = COUNTOFLONGSHARES

startPositionShort = COUNTOFSHORTSHARES

EndIF

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// set saisonal pattern

IF CurrentMonth = 1 THEN

saisonalPatternMultiplier = January

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplier = February

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplier = March

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplier = April

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplier = May

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplier = June

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplier = July

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplier = August

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplier = September

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplier = October

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplier = November

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplier = December

ENDIF

// define trading filters

// 1. use fast and slow averages as filter because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

f4 = signalline < Average[periodshortMA](close)

// 2. check if position already reduced in trading window as additonal filter criteria

alreadyReducedLongPosition = COUNTOFLONGSHARES < startPositionLong

alreadyReducedShortPosition = COUNTOFSHORTSHARES < startPositionShort

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s4 = signalline CROSSES UNDER dailyHigh

s5 = signalline CROSSES UNDER dailyLow

// long entry with order cumulation

IF ( (l1 OR l4 OR l2 OR (l3 AND f2) ) AND NOT alreadyReducedLongPosition) THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier > 0 THEN

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry with order cumulation

IF ((s1 AND f3) OR (s5 AND f1) OR (f4 AND (s4 AND f2)) ) AND NOT alreadyReducedShortPosition THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier < 0 THEN

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

IF LONGONMARKET THEN

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

ELSIF SHORTONMARKET THEN

posProfit = (((positionprice - close) * pointvalue) * countofposition) / pipsize

ENDIF

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

// trailing stop function

trailingStartLongInPoints = tradeprice(1) * trailingStartLong / 100

trailingStartShortInPoints = tradeprice(1) * trailingStartShort / 100

trailingStepLongInPoints = tradeprice(1) * trailingStepLong / 100

trailingStepShortInPoints = tradeprice(1) * trailingStepShort / 100

// reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

ENDIF

// manage long positions

IF LONGONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND close - tradeprice(1) >= trailingStartLongInPoints * pipsize THEN

newSL = tradeprice(1) + trailingStepLongInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND close - newSL >= trailingStepLongInPoints * pipsize THEN

newSL = newSL + trailingStepLongInPoints * pipsize

ENDIF

ENDIF

// manage short positions

IF SHORTONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND tradeprice(1) - close >= trailingStartShortInPoints * pipsize THEN

newSL = tradeprice(1) - trailingStepShortInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND newSL - close >= trailingStepShortInPoints * pipsize THEN

newSL = newSL - trailingStepShortInPoints * pipsize

ENDIF

ENDIF

// stop order to exit the positions

IF newSL > 0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

// superordinate stop and take profit

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

Hi Reiner,

Here is the backtest for your code for gold since 2006. It seems reliable because I checked that all data, even night data before 2010, were present. So unfortunately the drawdown is much more imortant as you see.

Sorry the attachment does not appear, I don’t know why.