Pere

PereParticipant

Veteran

@Mark, perhaps you are running a version lower tan V6. I’m running the V6, and do not have, like Alco, any trade since 9th of January (closed on 11th).

Hi guys,

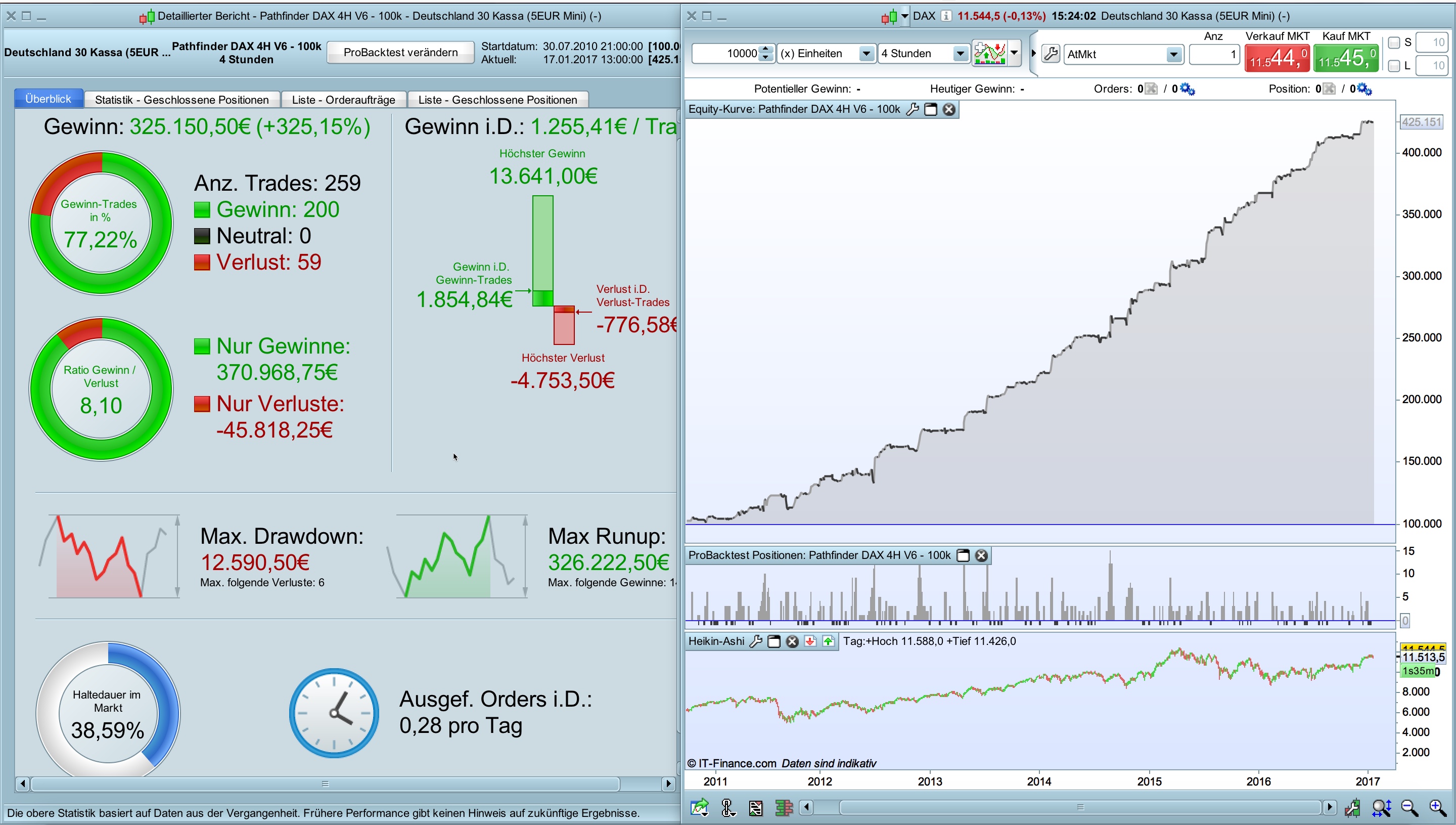

some of you asked me for a parameter setup for large account size (100k) for the Pathfinder DAX 4H V6.

I strictly recommend to start in life trading with a smaller account size such as 10k. The backtest looks very promising but the project status is still experimental and when you followed the topic discussions there are still some open points such as differences between backtest und life trading results.

In my opinion a good approach for a 100k account would be to trade the DAX mini 5Euro contract instead of DAX mini 1Euro. Enclosed is a version for an 100k account and DAX mini 5Euro. I can’t recommend to trade Pathfinder with a full DAX 25Euro future.

Best, Reiner

Hi

I see this right that tomorrow the soybeans could go long?

Michi

For information:

CAC 40 4h V5B2 is short in live trading.

Michi

ALE

ALEModerator

Master

Hello REINER hello GUYS

Good news.. TRAILING STOP OF PATHFINDER WORKS WELL

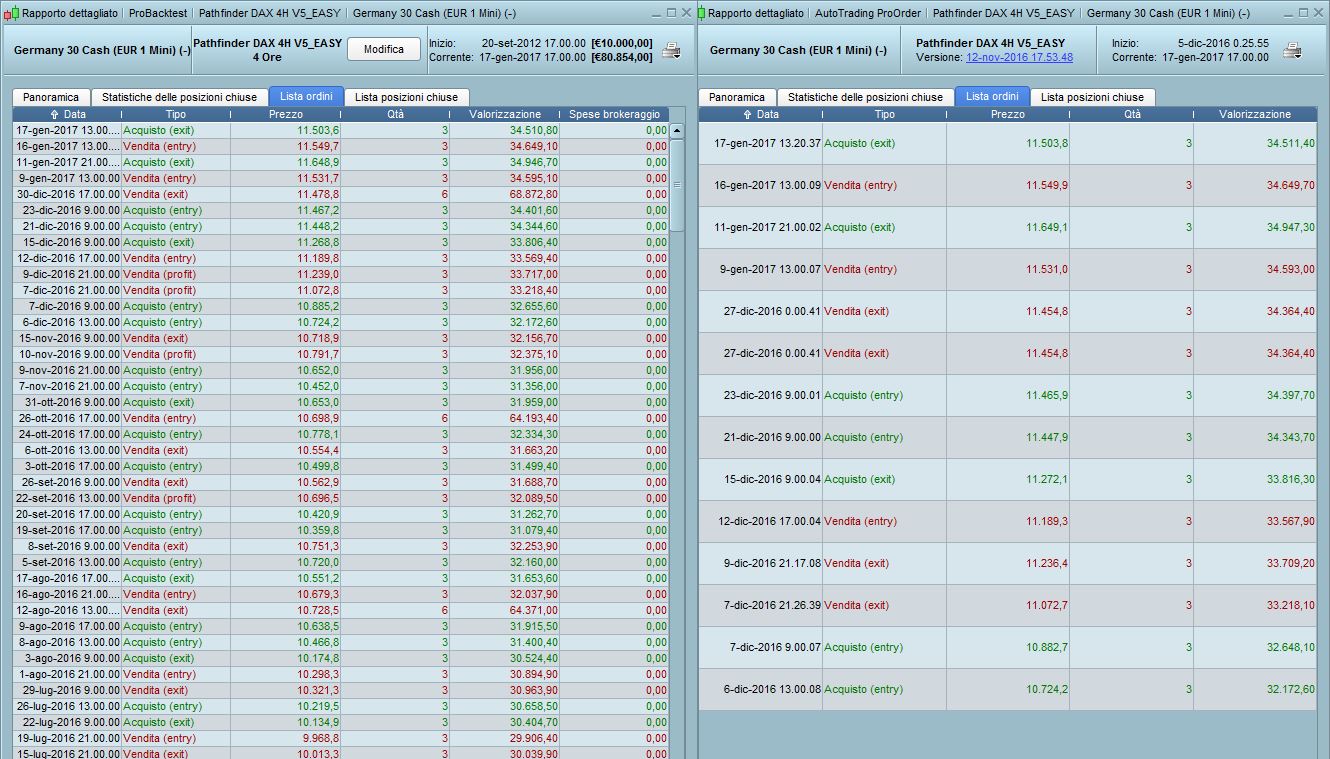

I’m testing a modified version of pathfinder since 6.12.2016, I’ve call it Pathfinder DAX 4H V5B2_EASY. it is not the best like V6, so you can continue to use v6 version, but I want to tell you that this morning it had closed a short position by tailing stop!..

Please check the attached picture, and the code above to check the short position of january=1 and the triling stop of v6!!

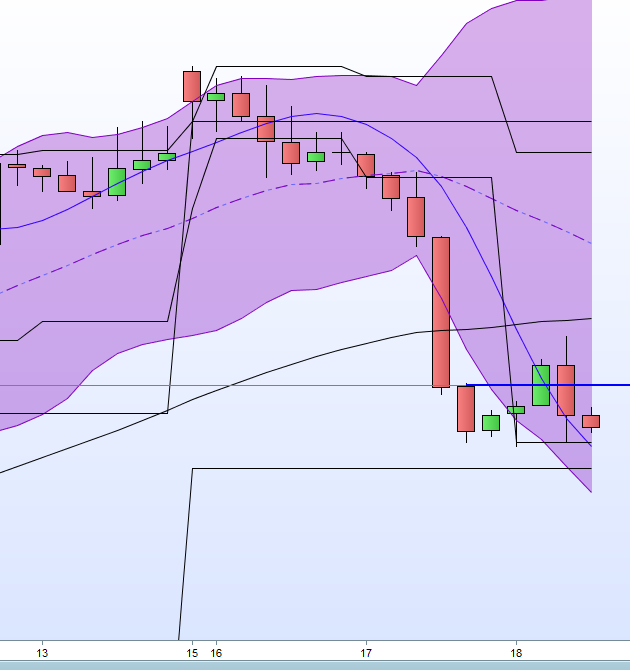

FTSE 4Hr (Long) closed today at 7238.7 for a loss.

FTSE 4Hr short opened shortly after at 7239.2 and currently running.

Hello

I have same trades in live account for FTSE (Long and then short)

But if I run the backtest, there is only the short one..The long (with the loss..) is not there..

Alco

AlcoParticipant

Senior

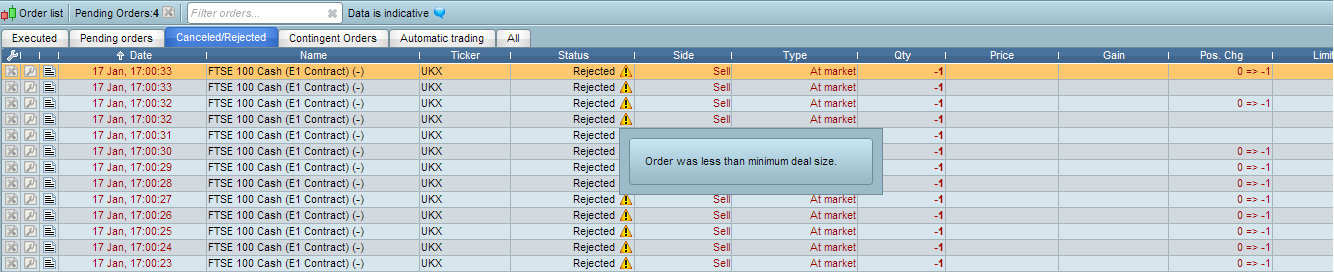

I had a problem yesterday with FTSE v5b2 version.

It gave a lot of rejected orders. It gave an error -> The minimum order size was 2 for ftse. The orders where rejected at 17:00. System was automatically stopped.

So I thought the multiplier was 1 for this period. But when I looked back at the code it has 2 or >.

This was the code I was using.

//-------------------------------------------------------------------------

// Main code : Pathfinder FTSE 4H V5B2

//-------------------------------------------------------------------------

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 5 Beta 2

// Instrument: FTSE mini 4H, 9-22 CET, 2 points spread, account size 10.000 Euro

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 90000

ONCE endTime = 210000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 7

// define filter parameter

ONCE periodLongMA = 230

ONCE periodShortMA = 10

// define position and money management parameter

ONCE positionSize = 1

Capital = 10000

Risk = 5 // in %

equity = Capital + StrategyProfit

maxRisk = round(equity * Risk / 100)

ONCE stopLossLong = 4 // in %

ONCE stopLossShort = 2.75 // in %

ONCE takeProfitLong = 3 // in %

ONCE takeProfitShort = 2 // in %

maxPositionSizeLong = MAX(15, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

maxPositionSizeShort = MAX(5, abs(round(maxRisk / (close * stopLossShort / 100) / PointValue) * pipsize))

ONCE trailingStartLong = 1.75 // in %

ONCE trailingStartShort = 0.75 // in %

ONCE trailingStepLong = 0.2 // in %

ONCE trailingStepShort = 0.3 // in %

ONCE maxCandlesLongWithProfit = 40 // take long profit latest after 40 candles

ONCE maxCandlesShortWithProfit = 30 // take short profit latest after 30 candles

ONCE maxCandlesLongWithoutProfit = 40 // limit long loss latest after 40 candles 30

ONCE maxCandlesShortWithoutProfit = 9 // limit short loss latest after 9 candles

// define saisonal position multiplier >0 - long / <0 - short / 0 no trade

ONCE January = 3

ONCE February = 3

ONCE March = 2

ONCE April = 2

ONCE May = 2

ONCE June = 2

ONCE July = 2

ONCE August = 3

ONCE September = -2

ONCE October = 2

ONCE November = 3

ONCE December = 2

// calculate daily high/low (include sunday values if available)

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// save position before trading window is open

If Time < startTime then

startPositionLong = COUNTOFLONGSHARES

startPositionShort = COUNTOFSHORTSHARES

EndIF

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// set saisonal pattern

IF CurrentMonth = 1 THEN

saisonalPatternMultiplier = January

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplier = February

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplier = March

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplier = April

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplier = May

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplier = June

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplier = July

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplier = August

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplier = September

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplier = October

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplier = November

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplier = December

ENDIF

// define trading filters

// 1. use fast and slow averages as filter because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

// 2. check if position already reduced in trading window as additonal filter criteria

alreadyReducedLongPosition = COUNTOFLONGSHARES < startPositionLong

alreadyReducedShortPosition = COUNTOFSHORTSHARES < startPositionShort

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER dailyLow

// long entry with order cumulation

IF ( (l1 OR l4 OR l2 OR (l3 AND f2)) AND NOT alreadyReducedLongPosition) THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier > 0 THEN

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry without order cumulation

IF ( (s1 AND f3) OR (s2 AND f1) ) AND NOT alreadyReducedShortPosition THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier < 0 THEN

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

IF LONGONMARKET THEN

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

ELSIF SHORTONMARKET THEN

posProfit = (((positionprice - close) * pointvalue) * countofposition) / pipsize

ENDIF

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

// trailing stop function

trailingStartLongInPoints = tradeprice(1) * trailingStartLong / 100

trailingStartShortInPoints = tradeprice(1) * trailingStartShort / 100

trailingStepLongInPoints = tradeprice(1) * trailingStepLong / 100

trailingStepShortInPoints = tradeprice(1) * trailingStepShort / 100

// reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

ENDIF

// manage long positions

IF LONGONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND close - tradeprice(1) >= trailingStartLongInPoints * pipsize THEN

newSL = tradeprice(1) + trailingStepLongInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND close - newSL >= trailingStepLongInPoints * pipsize THEN

newSL = newSL + trailingStepLongInPoints * pipsize

ENDIF

ENDIF

// manage short positions

IF SHORTONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND tradeprice(1) - close >= trailingStartShortInPoints * pipsize THEN

newSL = tradeprice(1) - trailingStepShortInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND newSL - close >= trailingStepShortInPoints * pipsize THEN

newSL = newSL - trailingStepShortInPoints * pipsize

ENDIF

ENDIF

// stop order to exit the positions

IF newSL > 0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

// superordinate stop and take profit

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

Could someone explain why it stopped?

Thanks,

Alco

@Alco

Use FTSE 100 CASH (-). Don’t use GBL_EUR. It worked for me.

AlcoParticipant

Senior

@mamio

i used ftse 100 cash €1 mini. So that shouldnt be the problem.

wp01

wp01Participant

Master

@Alco.

I see in your screen at pending orders: 4. Are these related to the FTSE 100?

Because it looks like it had conflicting orders.

In this link from PRT you can read when it is automaticly stopped.

https://tc.md.it-finance.com/IGIndex/conditions_of_execution_of_automatic_trading_systems.phtml?appletkey=0f4645986f0939c64351deb312e24d41707f01cf1289bab993e6d909593396a4&locale=en_GB

The minimum size is 1 for this contract, so that can not be the problem.

AlcoParticipant

Senior

@wp

No those 4 pending orders are not related to ftse.

(dutch) Wel raar, wanneer ik de muis op het driehoekje houd staat er dat er minimaal 2 contracten nodig zijn voor deze markt…. Heel vreemd.

wp01Participant

Master

@Alco

The quickest way how i check what the minimum contractsize is i go in IG tradingplatform to that CFD, i click on it and create an order or ticket and than you see in under “grootte” (also Dutch :-))

the minimum contracts. I tried to find it on the website from IG, unfortunate without luck.

When you click all the FTSE 100 you see that they all show one contract. But i see your screen. So that’s weird……

wp01Participant

Master

@Alco

But on the picture you show i can not read the last line, but it shows something like canceled 2 @ 7.545 at the same time.

So it does look like something is conflicting.