Hello everyone, I appeal especially to the more experienced, I think you have to work on the code to improve it and not waste energy on other time-frame. we must still improve and work on indexes and commodities. this and my thoughts to succeed as soon as possible. thanks and good luck to all.

Miguel

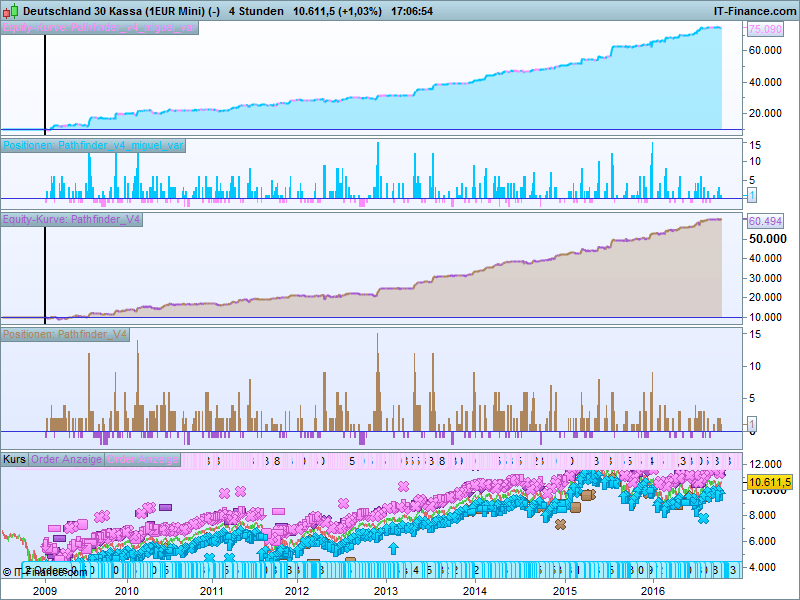

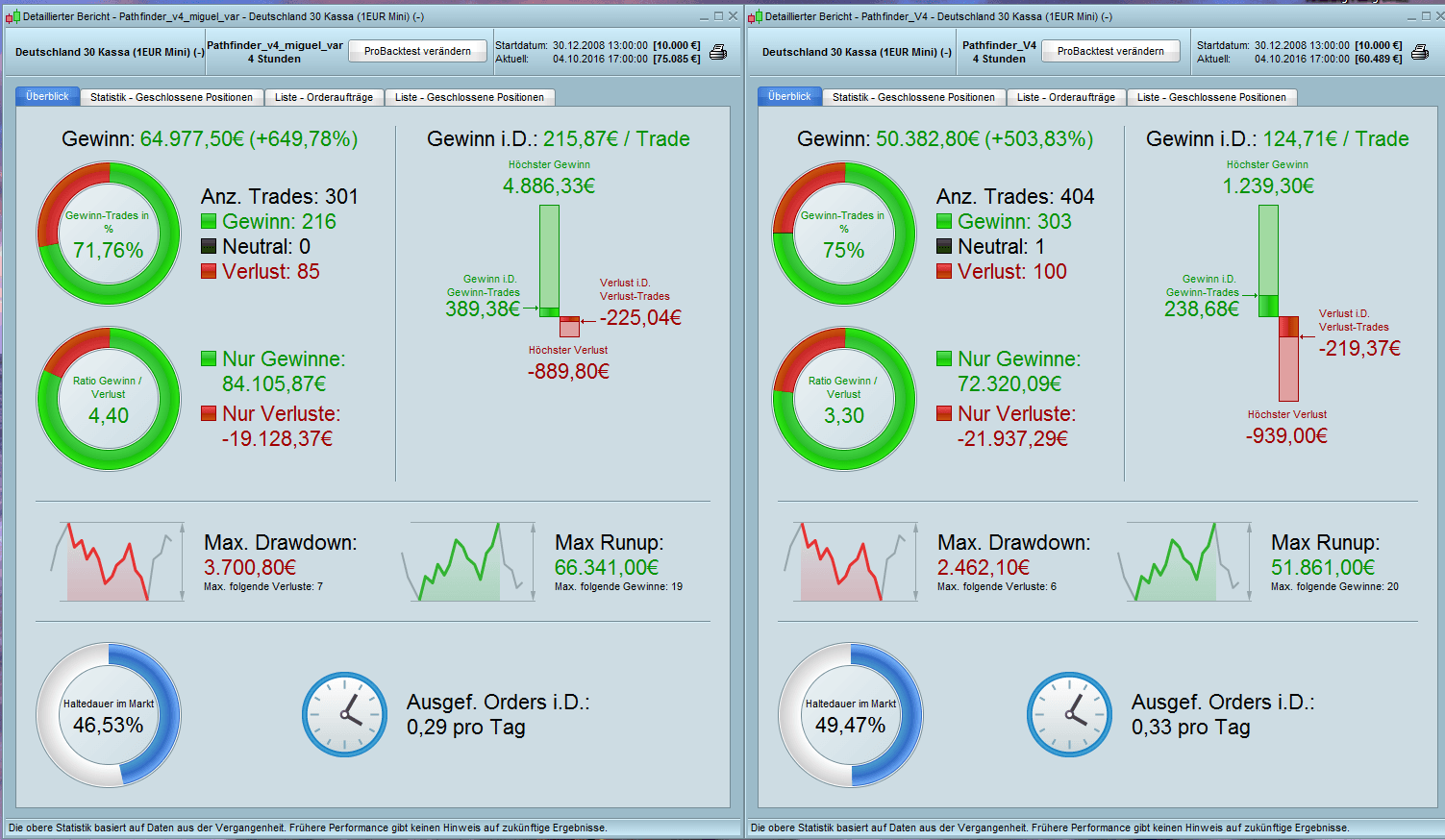

I like Reiners Version better because of the smaller Drawdown, but I tried to change his Version into one with variable StopLoss7Take Profit Levels for each Buy/Sell condition.

Maybe somebody is able to finde a combination of limit/sell percentages which will reduce the drawdown.

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 4 - avoid reopen of intraday positions in same direction (from Miguel)

// Instrument: DAX mini 4H, 8-22 CET, 2 points spread, account size 10.000 Euro

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000 // define intraday trading window

ONCE startTime = 80000

ONCE endTime = 220000 // define instrument signalline with help of multiple smoothed av-erages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 3 // define filter parameter

ONCE periodLongMA = 300

ONCE periodShortMA = 50 // define position and money man-agement parameter

ONCE positionSize = 1

ONCE maxPositionSizeLong = 15

ONCE maxPositionSizeShort = 10

ONCE stoppLossL1 = 3 // in %

ONCE stoppLossL2 = 5.5 // in %

ONCE stoppLossL3 = 5.5 // in %

ONCE stoppLossL4 = 5.5 // in %

ONCE stoppLossS1 = 2.5 // in %

ONCE stoppLossS2 = 5.5 // in %

ONCE takeProfitL1 = 5 // in %

ONCE takeProfitL2 = 9.5 // in %

ONCE takeProfitL3 = 8 // in %

ONCE takeProfitL4 = 6.25 // in %

ONCE takeProfitS1 = 2.5 // in %

ONCE takeProfitS2 = 2.25 // in %

ONCE maxCandlesLongWithProfit = 15 // take long profit latest after 15 candles

ONCE maxCandlesShortWithProfit = 13 // take short profit latest after 13 candles

ONCE maxCandlesLongWithoutProfit = 30 // limit long loss latest after 30 candles

ONCE maxCandlesShortWithoutProfit = 25 // limit short loss latest after 25 candles

// define saisonal position multiplier >0 - long / <0 - short / 0 no trade

ONCE January = 2

ONCE February = 2

ONCE March = 2

ONCE April = 3

ONCE May = 2

ONCE June = 2

ONCE July = 3

ONCE August = -1

ONCE September = -2

ONCE October = 1

ONCE November = 3

ONCE December = 3

// calculate daily high/low

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// save position before trading window is open #Miguel

If Time < startTime then

startPositionLong = COUNTOFLONGSHARES

startPositionShort = COUNTOFSHORTSHARES

EndIF

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// filter criteria because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

// reduced position? #Miguel

reduceLongInTradingWindow = COUNTOFLONGSHARES < startPositionLong

reduceShortInTradingWindow = COUNTOFSHORTSHARES < startPositionShort

// saisonal pattern

IF CurrentMonth = 1 THEN

saisonalPatternMultiplier = January

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplier = February

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplier = March

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplier = April

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplier = May

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplier = June

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplier = July

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplier = August

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplier = September

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplier = October

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplier = November

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplier = December

ENDIF

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER dailyLow

// long entry (L1)

IF l1 AND not reduceLongInTradingWindow THEN // cumulate orders for long trades #Miguel

IF saisonalPatternMultiplier > 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stoppLossL1

takeProfit = takeProfitL1

ENDIF

// long entry (L2)

IF l2 AND not reduceLongInTradingWindow THEN // cumulate orders for long trades #Miguel

IF saisonalPatternMultiplier > 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stoppLossL2

takeProfit = takeProfitL2

ENDIF

// long entry (L3)

IF ( (l3 AND f2) AND not reduceLongInTradingWindow ) THEN // cumulate orders for long trades #Miguel

IF saisonalPatternMultiplier > 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stoppLossL3

takeProfit = takeProfitL3

ENDIF

// long entry (L4)

IF ( l4 AND not reduceLongInTradingWindow ) THEN // cumulate orders for long trades #Miguel

IF saisonalPatternMultiplier > 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stoppLossL4

takeProfit = takeProfitL4

ENDIF

// short entry (S1)

IF NOT SHORTONMARKET AND (s1 AND f3) AND not reduceShortInTradingWindow THEN // no cumulation for short trades #Miguel

IF saisonalPatternMultiplier < 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stoppLossS1

takeProfit = takeProfitS1

ENDIF

// short entry (S2)

IF NOT SHORTONMARKET AND (s2 AND f1) AND not reduceShortInTradingWindow THEN // no cumulation for short trades #Miguel

IF saisonalPatternMultiplier < 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stoppLossS2

takeProfit = takeProfitS2

ENDIF

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

Someone requested trailing stop and breakeven functionality for Pathfinder. Several tests with the DAX didn’t show significant improvement of the performance. The existing framework seems to be well balanced.

Here is the code to play around:

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 5 Beta 1 - with traling stop

// Instrument: DAX mini 4H, 8-22 CET, 2 points spread, account size 10.000 Euro

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 80000

ONCE endTime = 220000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 3

// define filter parameter

ONCE periodLongMA = 300

ONCE periodShortMA = 50

// define position and money management parameter

ONCE positionSize = 1

ONCE maxPositionSizeLong = 15

ONCE maxPositionSizeShort = 10

ONCE stopLossLong = 5.5 // in %

ONCE stopLossShort = 3.5 // in %

ONCE takeProfitLong = 2.75 // in %

ONCE takeProfitShort = 1.75 // in %

ONCE trailingStart = 1.75 // in %

ONCE trailingStep = 0.2 // in %

ONCE maxCandlesLongWithProfit = 15 // take long profit latest after 15 candles

ONCE maxCandlesShortWithProfit = 13 // take short profit latest after 13 candles

ONCE maxCandlesLongWithoutProfit = 30 // limit long loss latest after 30 candles 30

ONCE maxCandlesShortWithoutProfit = 13 // limit short loss latest after 13 candles

// define saisonal position multiplier >0 - long / <0 - short / 0 no trade

ONCE January = 2

ONCE February = 2

ONCE March = 2

ONCE April = 3

ONCE May = 2

ONCE June = 2

ONCE July = 3

ONCE August = -1

ONCE September = -2

ONCE October = 1

ONCE November = 3

ONCE December = 3

// calculate daily high/low (include sunday values if available)

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// save position before trading window is open

If Time < startTime then

startPositionLong = COUNTOFLONGSHARES

startPositionShort = COUNTOFSHORTSHARES

EndIF

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// set saisonal pattern

IF CurrentMonth = 1 THEN

saisonalPatternMultiplier = January

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplier = February

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplier = March

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplier = April

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplier = May

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplier = June

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplier = July

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplier = August

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplier = September

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplier = October

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplier = November

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplier = December

ENDIF

// define trading filters

// 1. use fast and slow averages as filter because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

// 2. check if position already reduced in trading window as additonal filter criteria

alreadyReducedLongPosition = COUNTOFLONGSHARES < startPositionLong

alreadyReducedShortPosition = COUNTOFSHORTSHARES < startPositionShort

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER dailyLow

// long entry with order cumulation

IF ( (l1 OR l4 OR l2 OR (l3 AND f2)) AND NOT alreadyReducedLongPosition) THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier > 0 THEN

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry without order cumulation

IF NOT SHORTONMARKET AND ( (s1 AND f3) OR (s2 AND f1) ) AND NOT alreadyReducedShortPosition THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier < 0 THEN

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

IF LONGONMARKET THEN

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

ELSIF SHORTONMARKET THEN

posProfit = (((positionprice - close) * pointvalue) * countofposition) / pipsize

ENDIF

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

//trailing stop function

trailingStartInPoints = tradeprice(1) * trailingStart / 100

trailingStepInPoints = tradeprice(1) * trailingstep / 100

//reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL = 0 AND close - tradeprice(1) >= trailingStartInPoints * pipsize THEN

newSL = tradeprice(1) + trailingStepInPoints * pipsize

ENDIF

//next moves

IF newSL > 0 AND close - newSL >= trailingStepInPoints * pipsize THEN

newSL = newSL + trailingStepInPoints * pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL = 0 AND tradeprice(1) - close >= trailingStartInPoints * pipsize THEN

newSL = tradeprice(1) - trailingStepInPoints * pipsize

ENDIF

//next moves

IF newSL > 0 AND newSL - close >= trailingStepInPoints * pipsize THEN

newSL = newSL - trailingStepInPoints * pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL > 0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

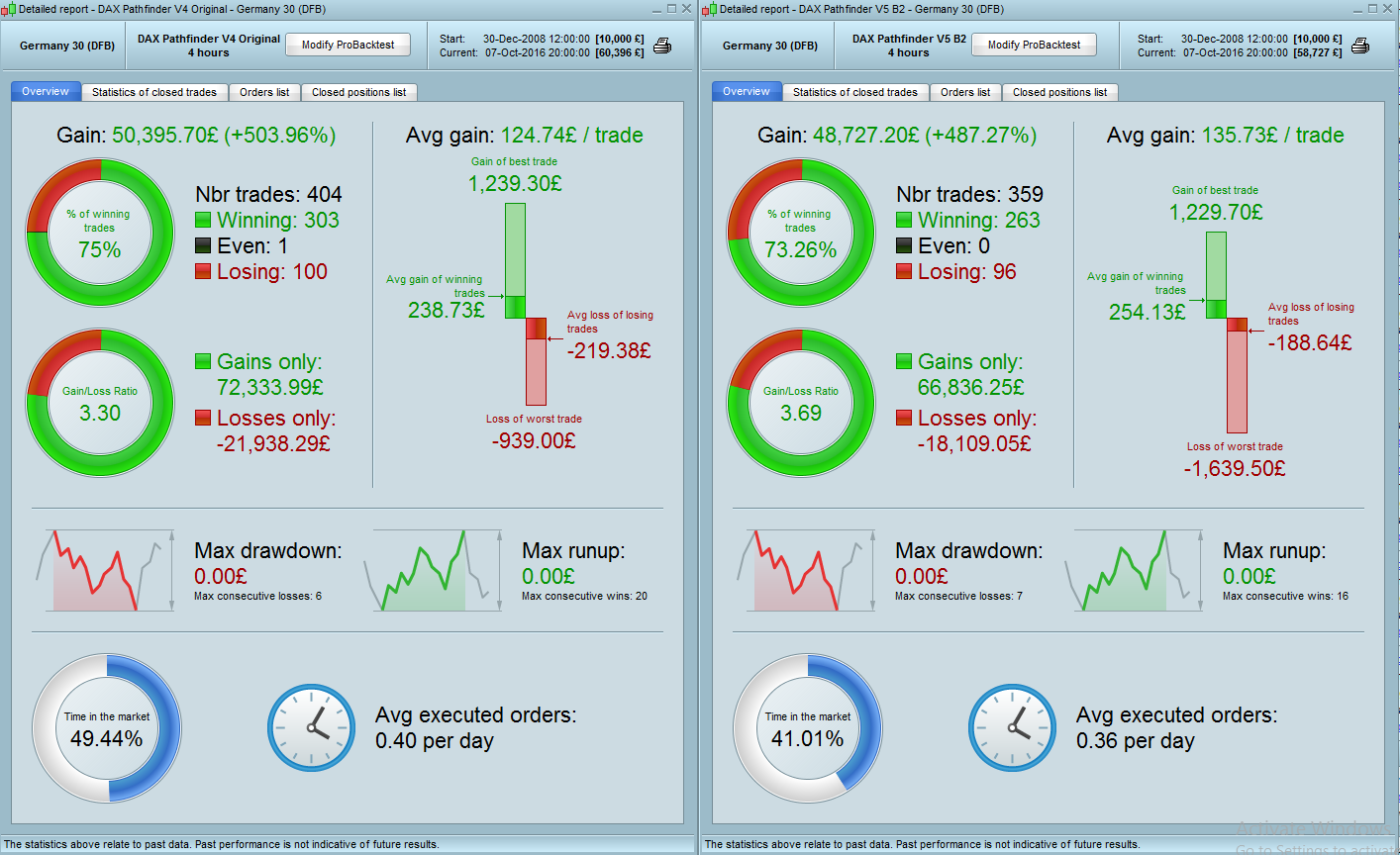

Maybe it is just a few single trades with high profit that make the difference, but see for yourselfs.

Flowsen ,

I checked in backtest results, excellent performance but very aggressive and therefore more dangerous.

reb

rebParticipant

Master

Hi Reiner, hi all

Thanks for this strategy and all your improvements.

Don’t you think that MaxPositionSize is a bit agressive and risky ? 15 mini with 10 000 Eur capital, you can kill your account in 3 or 4 days (for the Dax in average ,there is day move of 150pts between highest and lowest)

A newbie interested by easy money , will probably take your code without any understanding of all the details of Pathinder.

A reduction of MaxPositionSize or a more consequent capital as proposal would be safer for most of the viewers.

After for these who want to take more risks, they will do it knowingly.

Regards,

Reb

My 2 cents about max position sizing : adjust it with max “Average Daily Range” from X lookback days.

rebParticipant

Master

Hi Reiner, Hi all

To go beyond my previous post, I have just tested the strat (version 4 – miguel) since mai 2006:

The strat is negative until dec 2012, with a maximal loss of -14 000 eur. If you used a 10 000 eur capital , your account is dead.

Since 2013, it is very positive (see attachement), but to earn this money, you need to have more than 15 000 eur at the beginning and to be very confident (you will loose 90% of your capital and you have to wait 6.5 years before earning some money).

Reb

Before August 2010 the results are not really significant, because between 22:00 and 08:00 there has been no pricing. So the calculation of the number of candles is not correct and probably the calculation of the averages as well.

I have created a new version. Pathfinder V5 Beta 2. The version is still beta because off the ongoing discussion regarding position sizing. Here are the changes:

- fixed a bug in the profit calculation for short positions (variable posProfit)

- introduce trailing stop mechanism based on percent values (idea from MichiM, based on Nicolas work found here in the blog)

- add a filter to reduce unprofitable intraday trades (idea from Miguel)

- introduce maximal position size calculation dependent on capital and risk settings (inspired by comments from Elsborgtrading and reb)

- modify some trading parameter because of the bug fixing

changes in detail for the DAX:

- new: trailingStartLong

- new: trailingStartShort

- new: trailingStepLong

- new: trailingStepShort

Here is the code for the DAX (backtest is attached):

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 5 Beta 2

// Instrument: DAX mini 4H, 8-22 CET, 2 points spread, account size 10.000 Euro

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 80000

ONCE endTime = 220000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 3

// define filter parameter

ONCE periodLongMA = 300

ONCE periodShortMA = 40

// define position and money management parameter

ONCE positionSize = 1

Capital = 10000

Risk = 2 // in %

equity = Capital + StrategyProfit

maxRisk = round(equity * Risk / 100)

ONCE stopLossLong = 5.5 // in %

ONCE stopLossShort = 3.5 // in %

ONCE takeProfitLong = 2.75 // in %

ONCE takeProfitShort = 2 // in %

maxPositionSizeLong = MAX(15, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

maxPositionSizeShort = MAX(5, abs(round(maxRisk / (close * stopLossShort / 100) / PointValue) * pipsize))

ONCE trailingStartLong = 1.75 // in %

ONCE trailingStartShort = 0.75 // in %

ONCE trailingStepLong = 0.2 // in %

ONCE trailingStepShort = 0.1 // in %

ONCE maxCandlesLongWithProfit = 16 // take long profit latest after 16 candles

ONCE maxCandlesShortWithProfit = 15 // take short profit latest after 15 candles

ONCE maxCandlesLongWithoutProfit = 30 // limit long loss latest after 30 candles

ONCE maxCandlesShortWithoutProfit = 13 // limit short loss latest after 13 candles

// define saisonal position multiplier >0 - long / <0 - short / 0 no trade

ONCE January = 2

ONCE February = 2

ONCE March = 2

ONCE April = 3

ONCE May = 2

ONCE June = 2

ONCE July = 3

ONCE August = -1

ONCE September = -2

ONCE October = 1

ONCE November = 3

ONCE December = 3

// calculate daily high/low (include sunday values if available)

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// save position before trading window is open

If Time < startTime then

startPositionLong = COUNTOFLONGSHARES

startPositionShort = COUNTOFSHORTSHARES

EndIF

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// set saisonal pattern

IF CurrentMonth = 1 THEN

saisonalPatternMultiplier = January

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplier = February

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplier = March

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplier = April

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplier = May

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplier = June

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplier = July

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplier = August

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplier = September

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplier = October

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplier = November

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplier = December

ENDIF

// define trading filters

// 1. use fast and slow averages as filter because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

// 2. check if position already reduced in trading window as additonal filter criteria

alreadyReducedLongPosition = COUNTOFLONGSHARES < startPositionLong

alreadyReducedShortPosition = COUNTOFSHORTSHARES < startPositionShort

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER dailyLow

// long entry with order cumulation

IF ( (l1 OR l4 OR l2 OR (l3 AND f2)) AND NOT alreadyReducedLongPosition) THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier > 0 THEN

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry without order cumulation

IF NOT SHORTONMARKET AND ( (s1 AND f3) OR (s2 AND f1) ) AND NOT alreadyReducedShortPosition THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier < 0 THEN

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

IF LONGONMARKET THEN

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

ELSIF SHORTONMARKET THEN

posProfit = (((positionprice - close) * pointvalue) * countofposition) / pipsize

ENDIF

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

// trailing stop function

trailingStartLongInPoints = tradeprice(1) * trailingStartLong / 100

trailingStartShortInPoints = tradeprice(1) * trailingStartShort / 100

trailingStepLongInPoints = tradeprice(1) * trailingStepLong / 100

trailingStepShortInPoints = tradeprice(1) * trailingStepShort / 100

// reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

ENDIF

// manage long positions

IF LONGONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND close - tradeprice(1) >= trailingStartLongInPoints * pipsize THEN

newSL = tradeprice(1) + trailingStepLongInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND close - newSL >= trailingStepLongInPoints * pipsize THEN

newSL = newSL + trailingStepLongInPoints * pipsize

ENDIF

ENDIF

// manage short positions

IF SHORTONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND tradeprice(1) - close >= trailingStartShortInPoints * pipsize THEN

newSL = tradeprice(1) - trailingStepShortInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND newSL - close >= trailingStepShortInPoints * pipsize THEN

newSL = newSL - trailingStepShortInPoints * pipsize

ENDIF

ENDIF

// stop order to exit the positions

IF newSL > 0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

// superordinate stop and take profit

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

Hi reb,

Thanks for your contributions, I appreciate your review. You are absolutely right, 15 “naked” DAX mini contracts are too much for an 10k account. Please be aware that Pathfinder cumulated the position size only in very strong trends especially on the long side. The “signalline” has to crossed over the daily high (add pos), the weekly (add pos) and the monthly (add pos). When this extremly bullish scenario happens Pathfinder go “all in” and cumulate aggressiv the position. With the last trade the others are already in profit. This behavior is one of the booster of Pathfinder and the backtest showed since 2009 that the system were never in trouble with this logic.

I have added few lines of code in the last beta version to test the performance depending on risk and capital settings. I attached two backtests with 10k, 2% risk and at least 1 contract and 10k, 2% and at least 5 contracts to show how important it is to give Pathfinder enough room for cumulation.

I can’t judge your backtest before 2009 but I believe that the data conditions are not comparable. Any idea, review or improvement from your side is welcome.

regards

Reiner

Unfortunately, I can’t attach the both files. Here is the first, 10k, 2% risk and at least 1 contract

and here is the second attachment, 10k account, 2% risk and at least 5 possible contracts

Hey Reiner, Great work progressing an already great bit of code.

Thought you might like to see these. Not sure how relevant data from 2009 is for you but thought it was worth while posting…

Annoyingly, max runup/drawdown is not working for me sometimes at the moment.