Hello, I created this thread after the contribution of Juan Salas.

Juan, can you please post here your results and your code?

Many thanks!

Hi Francesco,

Thanks. I am attaching the code:

//crude oil 15 min strategy

DEFPARAM cumulateOrders = False

// Dias de la semana

IF DayOfWeek = 0 OR Dayofweek = 6 THEN

tradeok = 0

ELSE

tradeok = 1

ENDIF

// Friday 22:00 Close ALL operations.

IF DayOfWeek = 5 AND time = 220000 THEN

SELL AT MARKET

EXITSHORT AT MARKET

ENDIF

Fridaynight = Dayofweek = 5 AND time>220000

//parameter definition

period = 6

fastav = average[4](close)

slowav = average[50](close)

maoscillator = fastav-slowav

fullness = (Dclose(0)-Dopen(0))/abs(Dhigh(0)-Dlow(0))

avfullness = summation[period](fullness)/period

avfullnessthreshold = 0.38

enrojoalcista= (tradeprice(1)-close)>35*pipsize

enrojobajista= (close-tradeprice(1))>35*pipsize

cl = maoscillator>0

cl = cl and avfullness < -avfullnessthreshold

cs = maoscillator<0

cs = cs and avfullness > avfullnessthreshold

// Largos

IF NOT ONMARKET AND cl AND tradeok=1 AND NOT Fridaynight THEN

BUY 1 CONTRACT AT MARKET

ENDIF

// Cortos

IF NOT ONMARKET AND cs AND tradeok=1 AND NOT Fridaynight THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

// Salida Largos

IF LONGONMARKET AND enrojoalcista AND (open-close)>=30*pipsize AND open>close THEN

SELL AT MARKET

ENDIF

// Salida cortos

IF SHORTONMARKET AND enrojobajista AND (close-open)>=30*pipsize AND open<close THEN

EXITSHORT AT MARKET

ENDIF

////trailing stop function

trailingstart = 25 //trailing will start @trailinstart points profit

trailingstep = 30 //trailing step to move the "stoploss"

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 and tradeok=1 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

//************************************************************************

//set target pprofit 30

set stop ploss 90

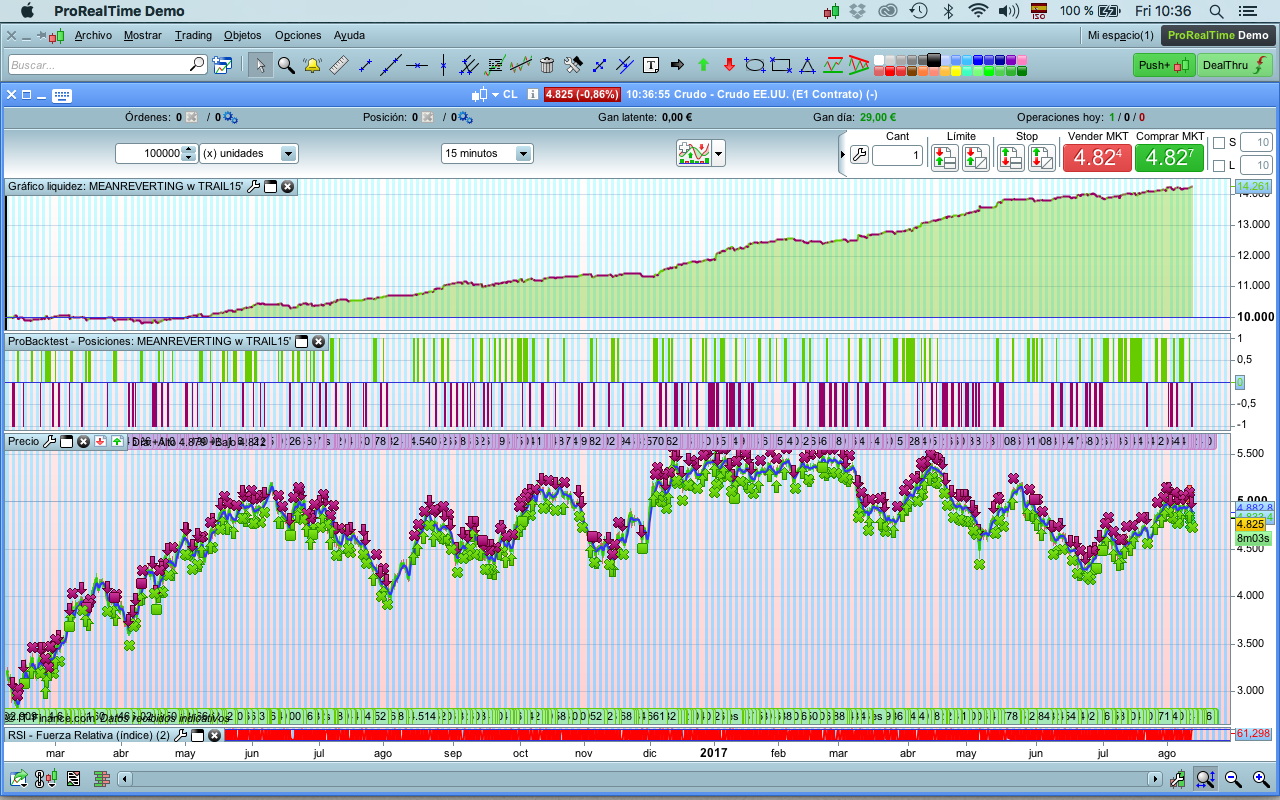

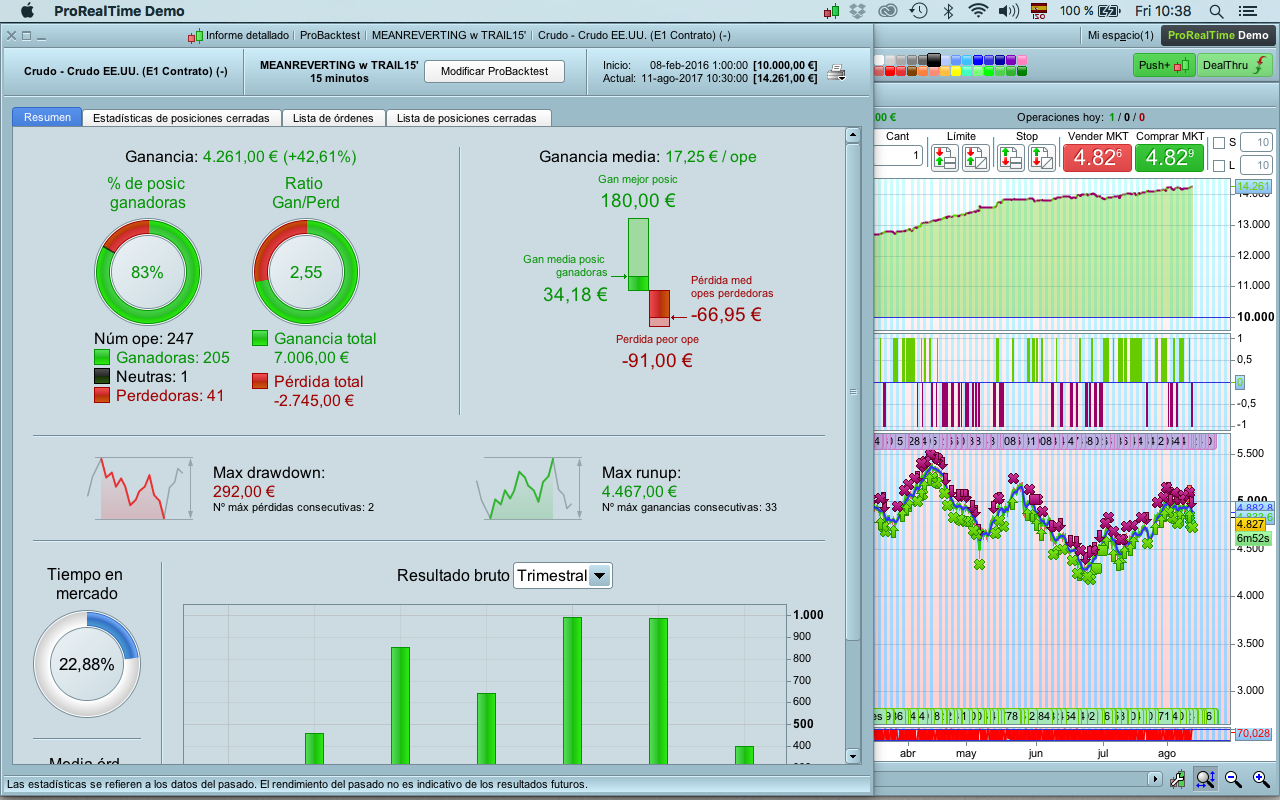

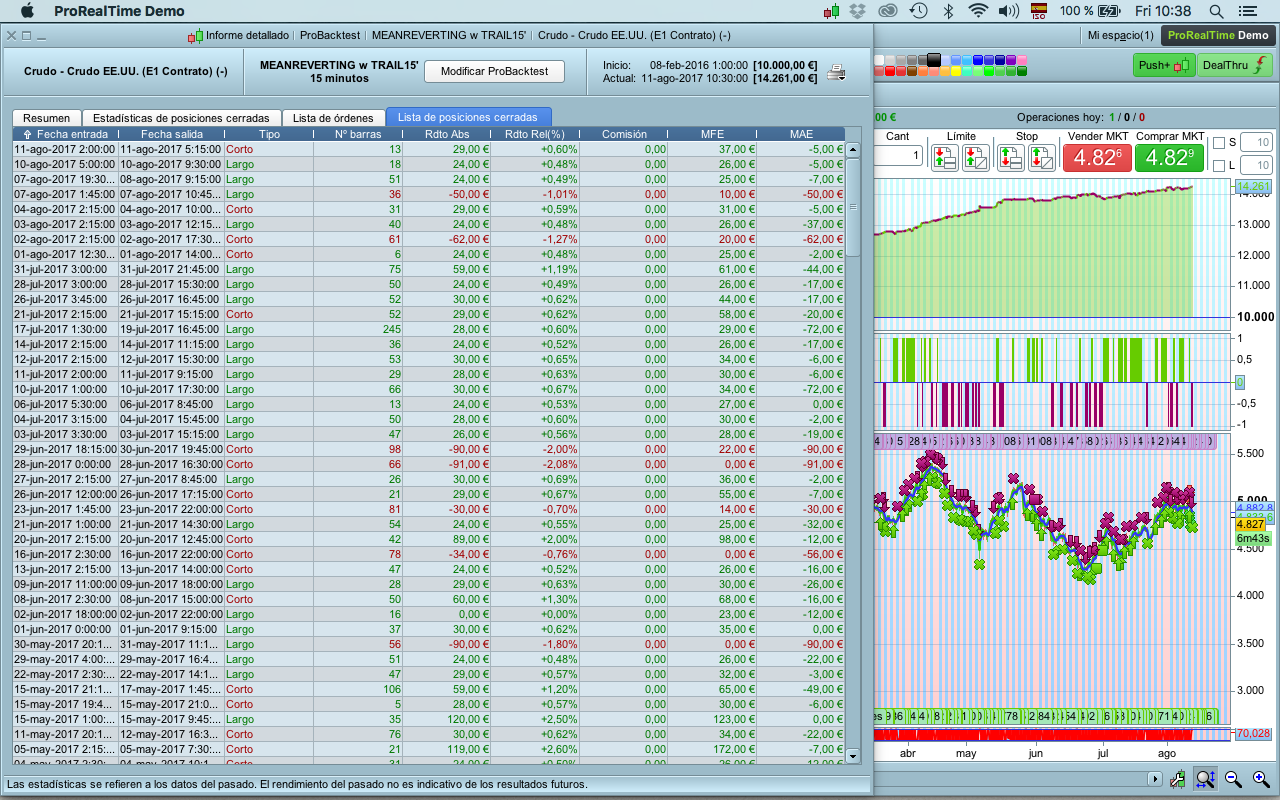

I am also attaching pics of my backtest:

As you can see in the code, the parameters trailingstart: 25 and trailingstep: 30 determine the following:

Trailing start is the first profit locked. Once 25 is secure, the trailing will be securing profits after every 30 pips (trailing step). You can play with these two parameters and decide which one fits you better.

I hope it can be useful. I already mentioned, but I am a big fan of your hammer-negated and mean-reverting, so I have taken the liberty to customised both codes.

I am trying to see if mean-reverting is adaptable to any other instruments (Indexes, Forex, etc).

Best,

Juan.

I am at the airport right now, so I will try to post (maybe this weekend, or beginning of next week) results and codes for the hammer-negated in other TFs.

Have a great weekend,

Juan

Hey guys, can anyone explain the logic behind the exit? Are you creating a target around 35 points? I’m referring to this part of the code:

// Salida Largos

IF LONGONMARKET AND enrojoalcista AND (open-close)>=30*pipsize AND open>close THEN

SELL AT MARKET

ENDIF

// Salida cortos

IF SHORTONMARKET AND enrojobajista AND (close-open)>=30*pipsize AND open<close THEN

EXITSHORT AT MARKET

ENDIF

@visctormork,

Hi, actually, the exit is defined by the trailing-start and trailing-step.

These two paragraphs in Spanish salida largos/Exit long and salida cortos=exit short are somehow something I thought it would help to mitigate the losses. I shouldn’t have labeled it as exit long/short.

In this sense, what I have tried to code is that because the Stop Loss is 90, I wanted to avoid to reach 90 in cases when is clear the operation is going to be negative. Example: when a LONG operation is losing by 35 points (enrojoalcista) and on top of that we see we have a long short candle of more than 30 pips, we sell at market. The market is showing a clear SHORT tendency, so why wait??. It is a little simple but it works in most of the cases. When operating in manual, if you see this clear short tendency, you would cut the losses. The same way, I wanted to create these two conditions to avoid reaching the stop loss of 90. In some cases, I am sure the operation would turn around and would close in positive, but are IMO the least.

I hope it clarify these two paragraphs,

Thanks,

Juan

P.S.- If any of you have tried this code in other values, it would be nice to share. I think Francesco did a wonderful job with hammer-negated and mean-reverting and we should try to explote these codes in other values and TFs.

Hi Juan,

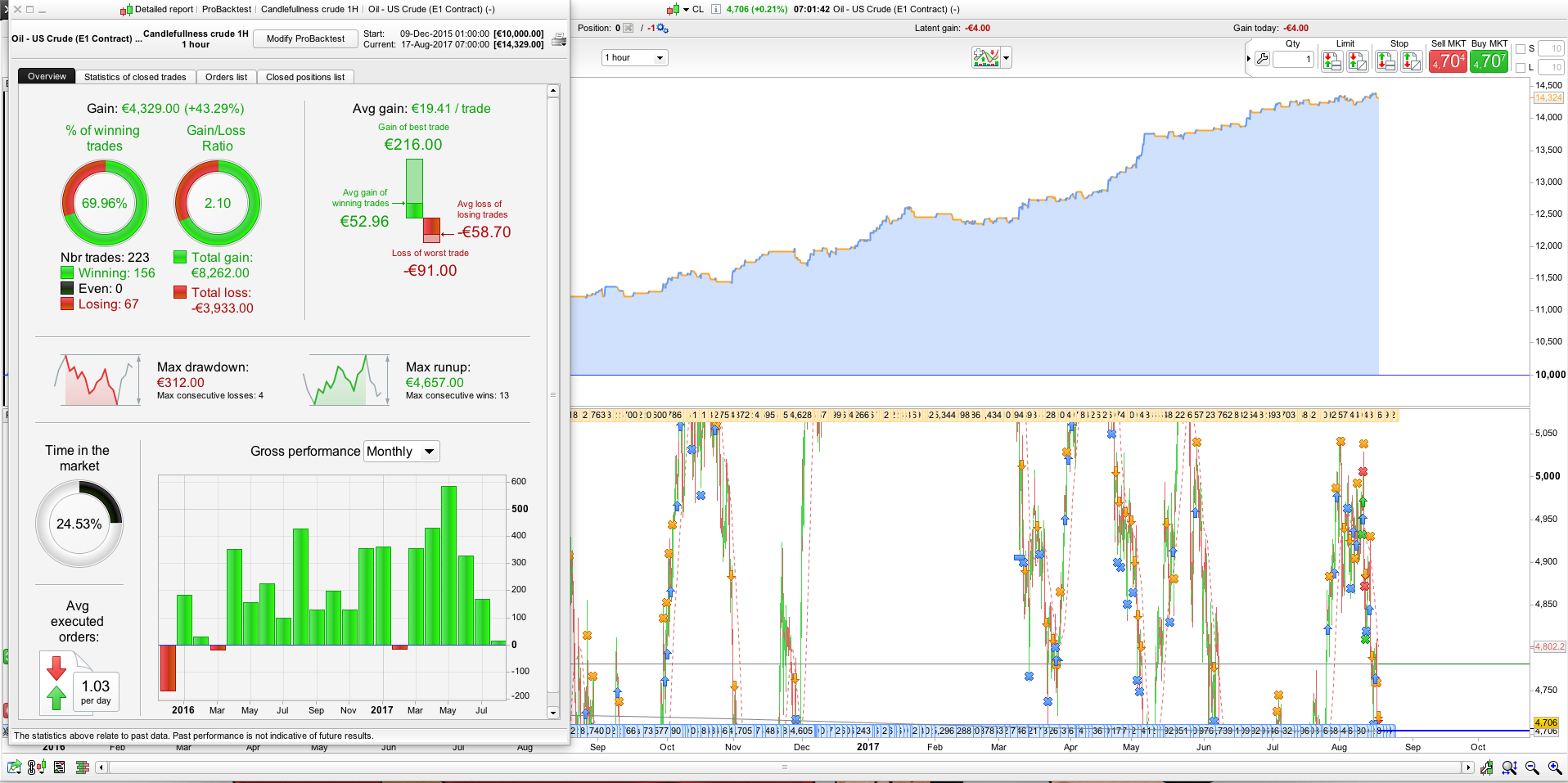

Thanks for your explanation. I think you have a great idea and I’ll try this section of code on other systems. With regards to this system I was a little bit bothered about the short history so I tried to see if the idea works on a higher timeframe just for some better confirmation. I have attached my version of the US Crude 1H. Please not that this backtest is curve fitted and should be adjusted before trying out live. It’s more to get an understanding if the idea works well. I would also like to point out that the return on this system (even if it’s not bad) is not as good as the one on 15 min.

It is so annoying that we have so little data for oil. There is plenty for several other raws but on Oil one has to go up to daily timeframe to get more data. 🙁

@Nicolas: I think something is wrong with the forum. I tried now several times to attach a file but it doesn’t show up and obviously Victor had the same problem. His file(s) don’t show.

Hi Victor,

Thanks. I will try on US Crude 1h and will see the results. In any case thanks for Francesco’s and your understanding. I just got into PRC three months ago and learning everyday from all of you guys.

BTW, I am seeing the expressions “curve fitted” a lot, and although I know is about the equity curve, I don’t know exactly the meaning of the expression when it comes to the performance of the EC. Any explanation would be greatly appreciated.

Thanks,

Juan

Hi Juan,

Thanks for your contribution.

Curve fitting is a very big issue when developing strategies. In short it is adding too many rules to your code to make the backtest look better and better. Think of the extrem. You could code a strategy that specifies for every trades of the past exactly when it should be opened and closed. You could easily construct a backtest with 100% winning trades. But this strategy obviously has zero predictive power and putting it live would most likely only lose money.

Hi Despair,

Thanks for the explanation. I am afraid that I did what you said with some of the strategies, and when I put them on DEMO I noticed some discrepancies with the performance of my previous backtest, so I thought that I have adapted the code to create a clean curve on the backtest. You just confirmed my original idea, but I had no idea that it was labeled with the expression “curve fitted”. Besides the name, it is good to know that when working on strategies and adapting other systems is not about constructing the perfect curve.

Thanks,

Juan

Curve fitting is the probably the nb. 1 reason why realtime trading results differ from the backtest. The best we can da right now is utilizing WFA. I made a post not long ago labeled “WFA – Am I doing it right?” (post # 42252). This is a very short description of the way I think with my current knowledge one should optimize a strategy.