As I posted many times, this is the solution fullness = abs((Dclose(0)-Dopen(0))/(Dhigh(0)-Dlow(0)+0.00001)

It’s a solution, I prefer something which can’t yield division by zero. I don’t think it’s likely to create any weird results either. I bet your solution works too with the underlying primitives, altough without the exact knowledge of how they work it still looks like possibly erroneous code.

abs((Dclose(0)-Dopen(0))/(Dhigh(0)-Dlow(0)+0.00001) cant yield to a division by zero as High -Low is bounded to zero, so high +low + 0,0000001 is strictly positive

Yes, they can’t yield negative numbers, which is obvious had I thought about what the function returns 🙂

Abz

AbzParticipant

Veteran

Despair , i have the premium version now and there is actually data all the way back to 2009 on 15 min , it is crude oil and not brent oil. 🙂

Which contract are you using?

I’m running Juans version live but have had it stopped since it seems to want to set stops too tightly with regards to my spread on Swedish IG. I’ve modified it to see if it’ll work better, I guess there’s always a risk if you’re moving it close to the current level with the spread set by the broker.

I’ve also been running the original code both optimized (and probably naively curve fitted) as well as the origianl code without great success both live/test. The trailing stop version seems to be more promising in the near future. Sadly I’ve lost most of the history on both accounts due to the division by zero error as well tweaking the code and restarting it and throwing away the results.

Anyone who’s been running the original code live and has had good returns?

AbzParticipant

Veteran

Despair: in the plattform it is ticker QMXXXX

OK, I don’t have this symbol. At which broker are you? I’m with IG through PRT.

How do the results with 200k bars look like?

AbzParticipant

Veteran

Despair: This symbols is on the pro realtime platform if you register trough there site. You can get a 14 days trail with this data. however there is something strange the strategy tested on IG crude oil does not produce the same result tested on QMXXXX oil price. The price looks the same.

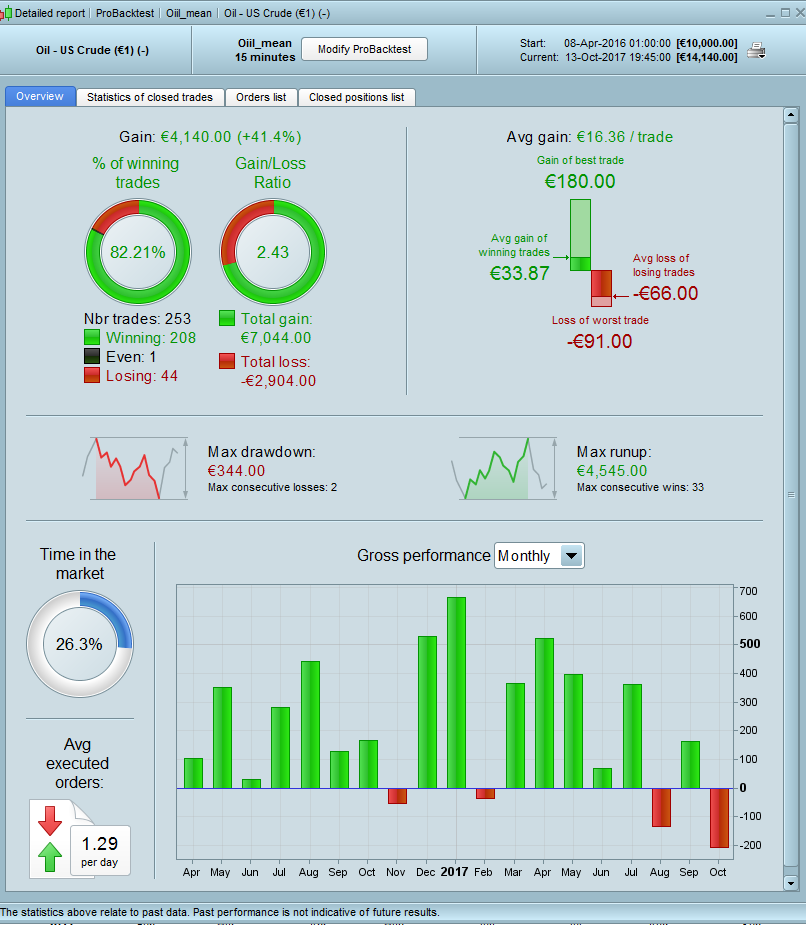

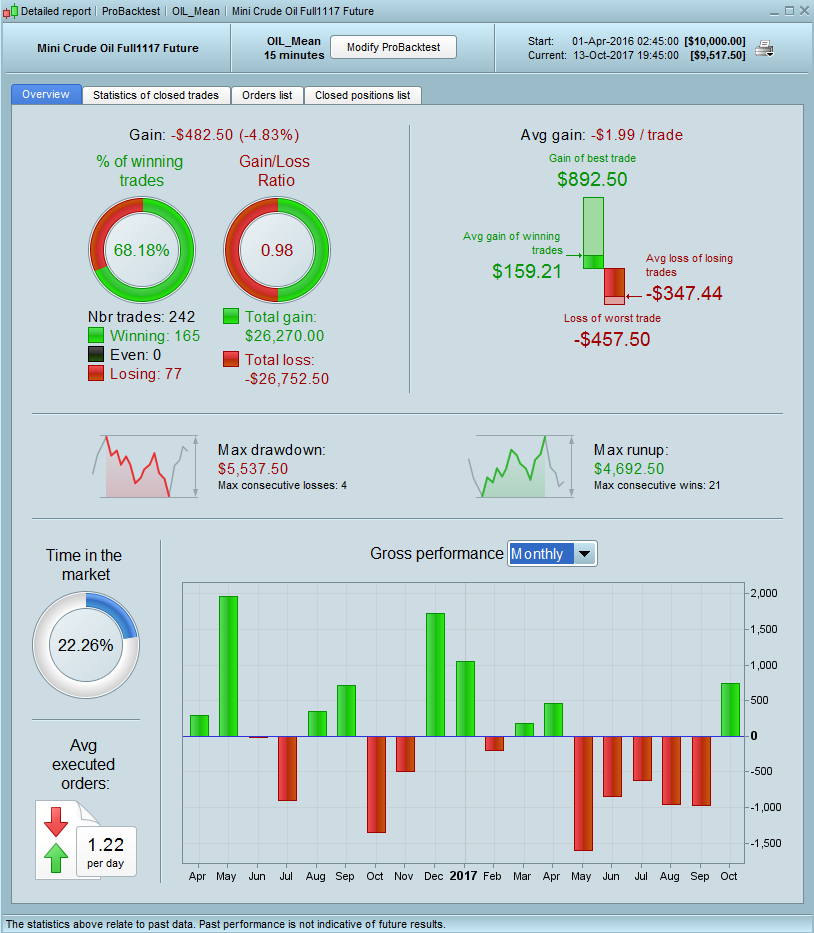

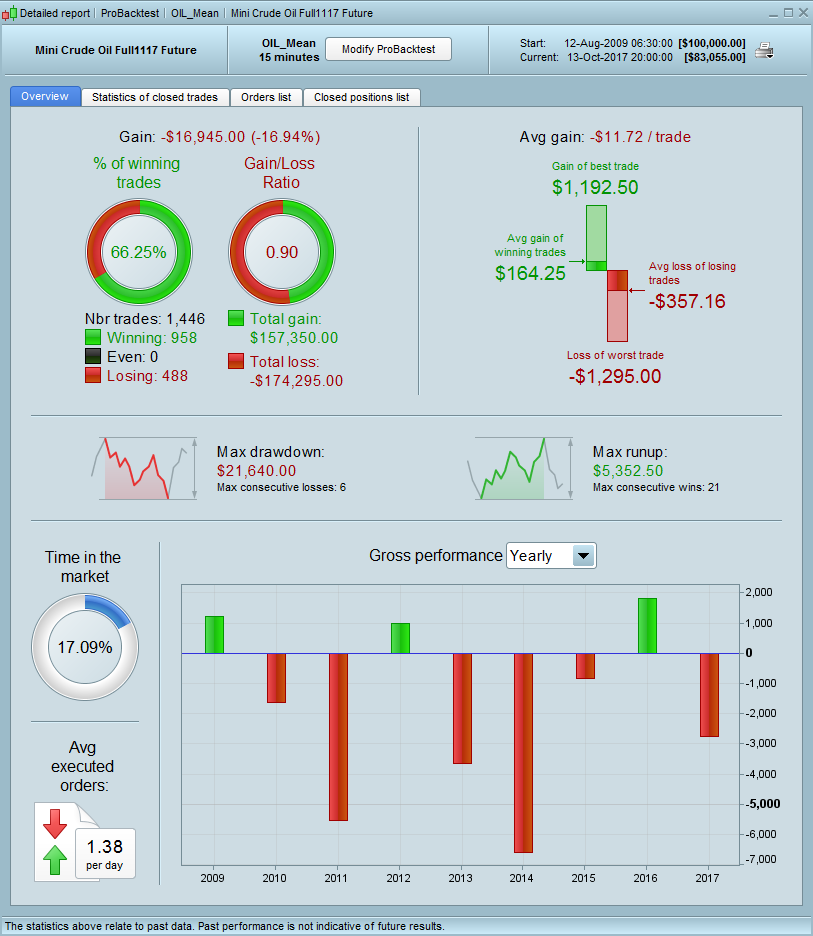

Francesco78: see attached screenshots for test on 200k bars.

1 mini crude oil contract is the same as 5 us – crude 1€ contracts on IG

Anyone have any idea how the result can be so different?

thanks, the results on the 200k are not on the same oil which I used in the post, do you have data with the same underlying?

thank you

AbzParticipant

Veteran

i think they are the same see pictures, however as mentioned in previous post the backtest is very different.

Don’t compare Futures contracts with CFD ones 🙂

Just wanted to add some info since I’ve been running the original system for a while, as well as the trailing stop suggestions done by Juan.

Firstly I’d like to show my change to the trailing stop code, which hopefully (I have to try “for real” on Monday) includes stop distance requirements.

The change is simple; you simply ensure you’ve got 6 pips to spare for SL-requirements. Might need to tweak this to 7-8 for slippage, but I’m not sure. I’m going to run this live.

The original code usually breaks quite quickly on successful trades on Swedish IG as it tries to set the SL way to close to the trade price.

//27-21

////trailing stop function

trailingstart = 27 //trailing will start @trailinstart points profit 25

trailingstep = 22 //trailing step to move the "stoploss" 30 21 & 9

slDistance = 6 // <--- to compensate for SL distance reqs emposed by the dealer.

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize+slDistance THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize+slDistance THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

I’d also like to say that the algo has performed admirably using Juan’s additions to it, the drawback seems to be limited and it’s managing to capture nice movements and take home the bacon, i.e. TP some 30-70p so far.

@stockdemon

Could you share the entire code?

Thanks

Attaching the code from PRT.

It can also be optimized for Brent with ok drawdown and performance. Just optimize the trailing start and stops (or don’t, you’ll most likely curve fit it). DAX is alright too, although the drawdown is a bit much. Not running the DAX version live. I’ve also had success in making it work theoretically for Nasdaq, and am trying it live. Drawdown is low, in theory.