See attachment which also contains the text fr better readability.

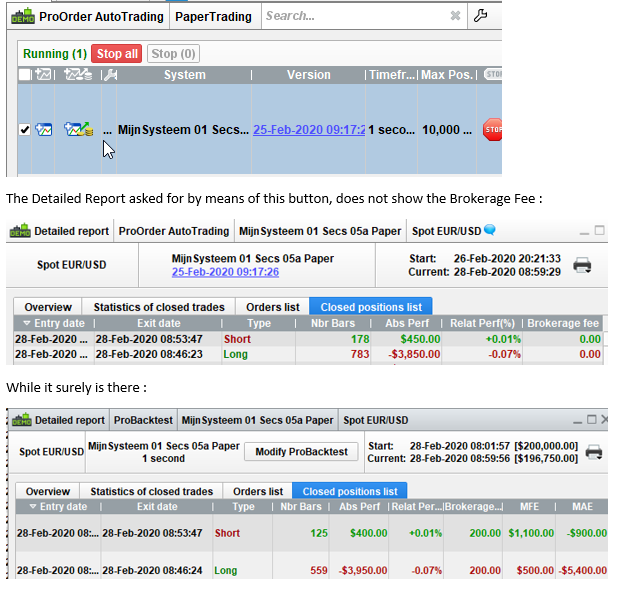

So notice that this is the running Strategy in the Paper environment against the Backtesting of the same Strategy in the same Paper environment.

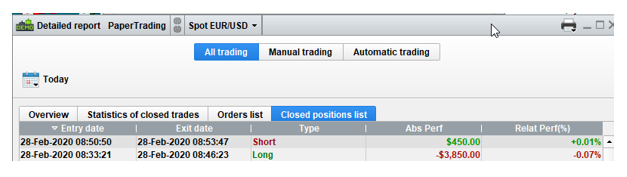

Similary, the Detailed Report of Paper Trading, does not show (or uses) the Brokerage Fee at all. See 2nd attachment.

Internal issue #021.

If the broker commission is 0 in the paper trading window, why do you think it does really exist?

Nicolas, if I understand your question correctly … because I pay for that in reality ?

This is not IG you know, this is IB. We pay commission there.

If you mean something else, please let me know.

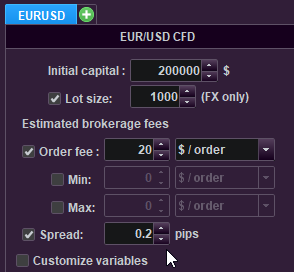

Anyway, the commission is crucial. You saw that in my last post in the other topic. OK, in the 2nd attachment the same screenshot (20 with commission vs 80 without). Multiply that with 100 orders and see how much off it will be. 🙁

So are you expecting brokerage fee (paid by you to IB) to be taken account of in PRT (in backtests and paper trading / Forward Test) without you entering a figure for brokerage fee into PRT?

without you entering a figure for brokerage fee into PRT?

Haha, of course not. But where to enter the figure ??

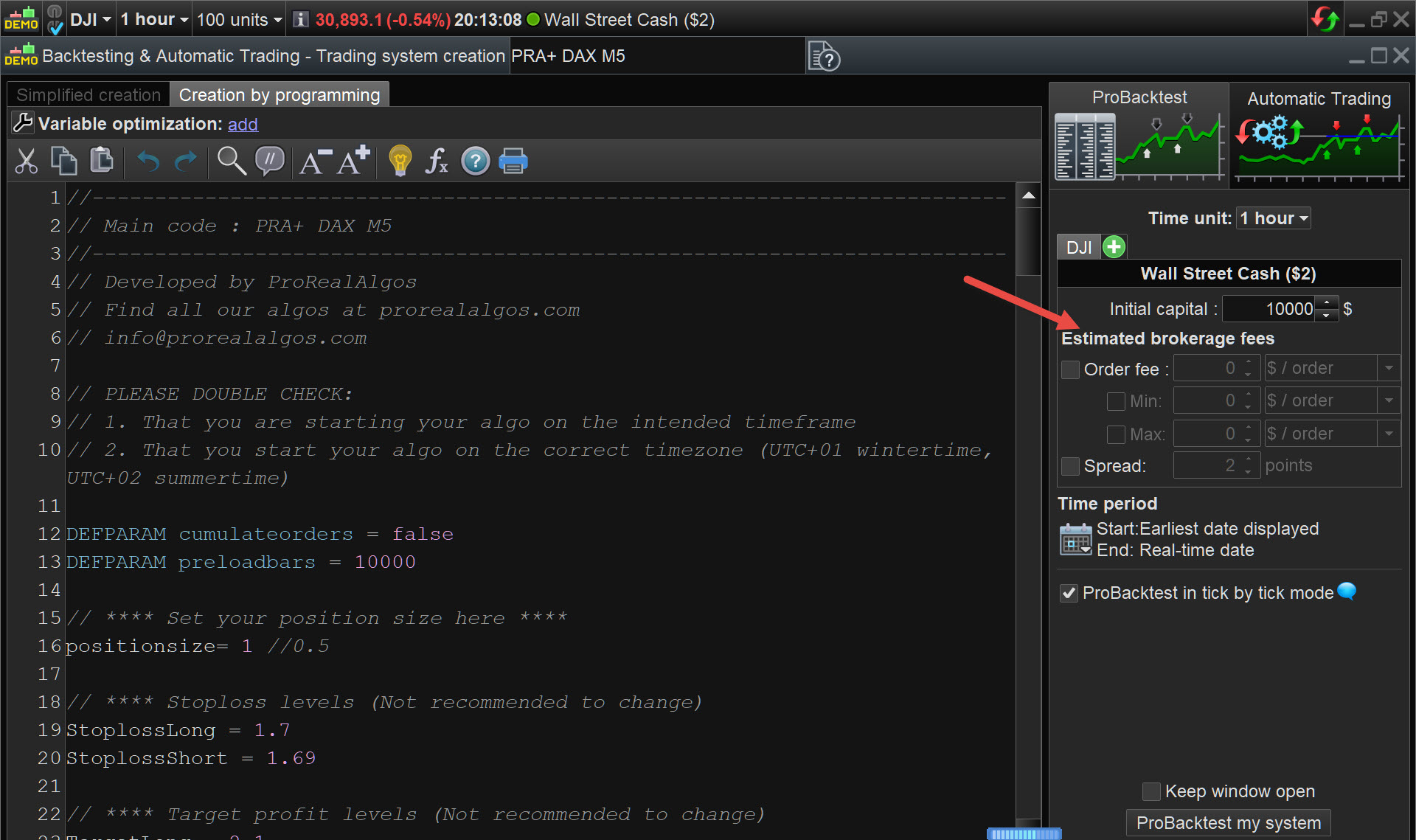

See attached

I know how confusing it is … but that is for ProBackTest. Not for Automatic Trading (by me referred to as Paper Trading – pls remember, real-live (real-life) Automatic Trading does not need simulation of Commission).

Plus

With you (IG) no Commission is in order (only Spread).

and

You people have no idea how complex it is to cover for these kind of things in Program Code, might my strategies try to be resilient in PRT-IB and PRT-IG at the same time. Hint : Market Place. 🙂

But also : keep on shooting because it is sooo easy to make mistakes by me on these matters. Thanks !

Thanks for above … now I understand.

Not perfect at all, but – to simulate slippage etc for Paper Trading / Demo Forward Test – I add an extra point onto my spread setting.

It would be lovely if the brokers would send account fee information to PRT to be used by them in their profit/loss calculations but they don’t.

Currently the only way to see how each strategy running live is truly performing including fees is to log into your brokers account and record the fees for each trade manually and deduct them off the PRT displayed results.

If you require accurate profit/loss information within an algo for the purpose of money management calculations and your broker has a fixed commission then you can just calculate your own ‘simulated’ profit/loss value by deducting the commission at each position size change from strategyprofit. With varying spread this is not going to be very accurate but allowing for some fixed spread value (different for different times of the day) will be better than using no simulated calculation at all.

So this bug is not really a bug but just a lack of fees data provided from brokers to external sources. Really this sort of complaint would be better directed at your broker either via their own forum if they have one or directly to them rather than in a PRT forum.

Not perfect at all, but – to simulate slippage etc for Paper Trading / Demo Forward Test – I add an extra point onto my spread setting.

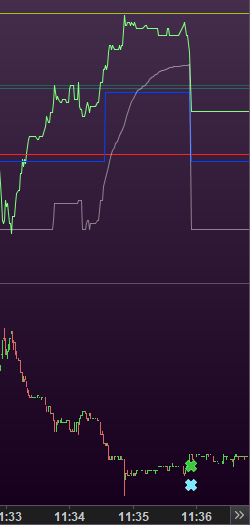

Yes, that is what I did too, in the past. These days I have a very different approach : causing PaperTrading to behave exactly the same as Backtesting (see attachment) – or maybe it is the other way around 🙂 – and next be able to trust the BackTesting which runs in real time. So a. that includes the Commission (or spread) all right and b. because the program code knows about the settings too, it all works consistently.

Ad b.: You’d sell above the spread or Commission loss.

I don’t want to confuse things in this topic unnecessarily, but there’s another bug regarding this. See 2nd attachment;

That spread can’t have more than 1 decimal, while this is most certainly not enough to mimic reality. So might PRT read up till this post anyway …

If we in-code must simulate the spread in order (this is crucial for PRT-IG, less for PRT-IB) *and* you see me simulate my own PaperTrading in BackTest, then with 1 decimal this won’t work out. Btw, I saw someone (a moderator) tell me the other day that you can’t know the real spread … well, IMO you can. Just look at what you lost after entering the order. Of course this is at the entering of the order only (at the exit you will be too late – haha). That aside, if we can’t have this more precise, we also can’t simulate PaperTrading by means of BackTesting (yes, that is the proper sequence).

So all is related a little …

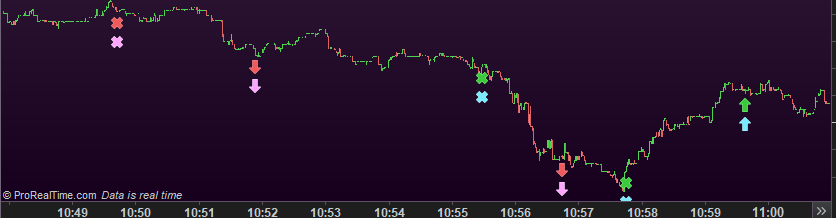

… and if I can’t simulate properly, my graphing will also be worthless (graphing which can’t be done in PaperTrading nor in real AutoTrading). See 3rd attachment.

Am I exaggerating things ? no man, this is $. 🙂