@Zilliq what’s your usual stop loss on your strategies?

I use a stop loss or stop trailing

The number of pip of stop loss/stop trailing is determined by the backtest

Bye

The number of pip of stop loss/stop trailing is determined by the backtest

Edit: The number of pip of stop loss/stop trailing is determined curvefitted by the backtest.

Sorry Zilliq but I just couldn’t help myself…. it must be the thought of the taste of all those donkey sausages!

A stop loss is just another strategy variable and a trailing stop loss is just a whole bunch of variables. Each and every one needs analysing and robustness testing to make sure they are not a curve fit. We think our strategies only have two variables when in fact they have perhaps at least six if we use stops, take profits and trailing stops.

Right I use only one variable for Money management ( stop ploss var, or stop ptrailing var and so on..)

It’s like a game with 3 pieces, and you put them where you want to. Me I put one on Money management and I don’t want to have more that 3-4 variables in algos (I never succed If I remember to have a good algo with just one variable)

We can try not to use a piece on Money Management = no stop for example but with crossing average …It’s just maths

We can always say that if we use close and not close[1] it’s like a variable but like that all is variable and can explain why the more complex a code is the less correlation on OOS we will have

Bye

with “algo” – do you mean entry variables? In which case, if you say that you only have 2 variables, that is 2 variables for entry positions, but you may have more variables within the trailing stop loss code, i.e. ‘money management’, and possibly other variables elsewhere in the code? For me a variable is any data set that can be changed, and if changed it will affect the strategy outcome / or backtest.

R

I use a stop loss or stop trailing

The number of pip of stop loss/stop trailing is determined by the backtest

Bye

The reason I asked is when you make money on your live demo strategies you seem to make a consistent profit, but when you loose it’s quite big. I was wondering what your stop loss is in relation to your profit target – it seems to be small profit target vs your stop loss and a high win rate, but I might be wrong.

Hi @eckaw

Algo is algorithm

In general

Only one variable for signal=entry position

One variable for market structure

One variable for Money management (sometimes we can trick to not have stop loss)

The loss is determine by Money management. The more you can lose, the more you can win. Not a real problem if you have a high win rate. You should always look at your ratio win/loss (Always>2)

The term money management seems to be being used incorrectly here.

Money management is the adjustment of position size based on perceived risk or the adjustment of position size to protect capital or the adjustment of position size to try to increase gains as capital increases. Money management has nothing to do with stops and targets unless you are adjusting position size based on them because your risk of winning/losing changes depending on stop and target distances.

When back testing and forward testing it is always better to remove any money management unless it is risk based position sizing as it is just another variable that can make you think a strategy is better than it really is.

“..unless you are adjusting position size based on them…”

This is what I do 😉 (Mix VanTharp/Vince Method)

So you are calculating stop and target prices and then calculating what position size to use based on the risk/reward? There is more than just simple risk/reward based on target compared to stop in each trade we take. Some will have more probability of success than others which needs to be quantified before deciding on position size – this is where the curve fitting starts as we can only look at historical performance to decide the probability of success over failure.

If your position size is purely adjusted because for example our target is 1 and our stop is 2 then no amount of money management can save a strategy from failure because spread will always skew things slightly against us as soon as we open a trade.

Life Goes on ..

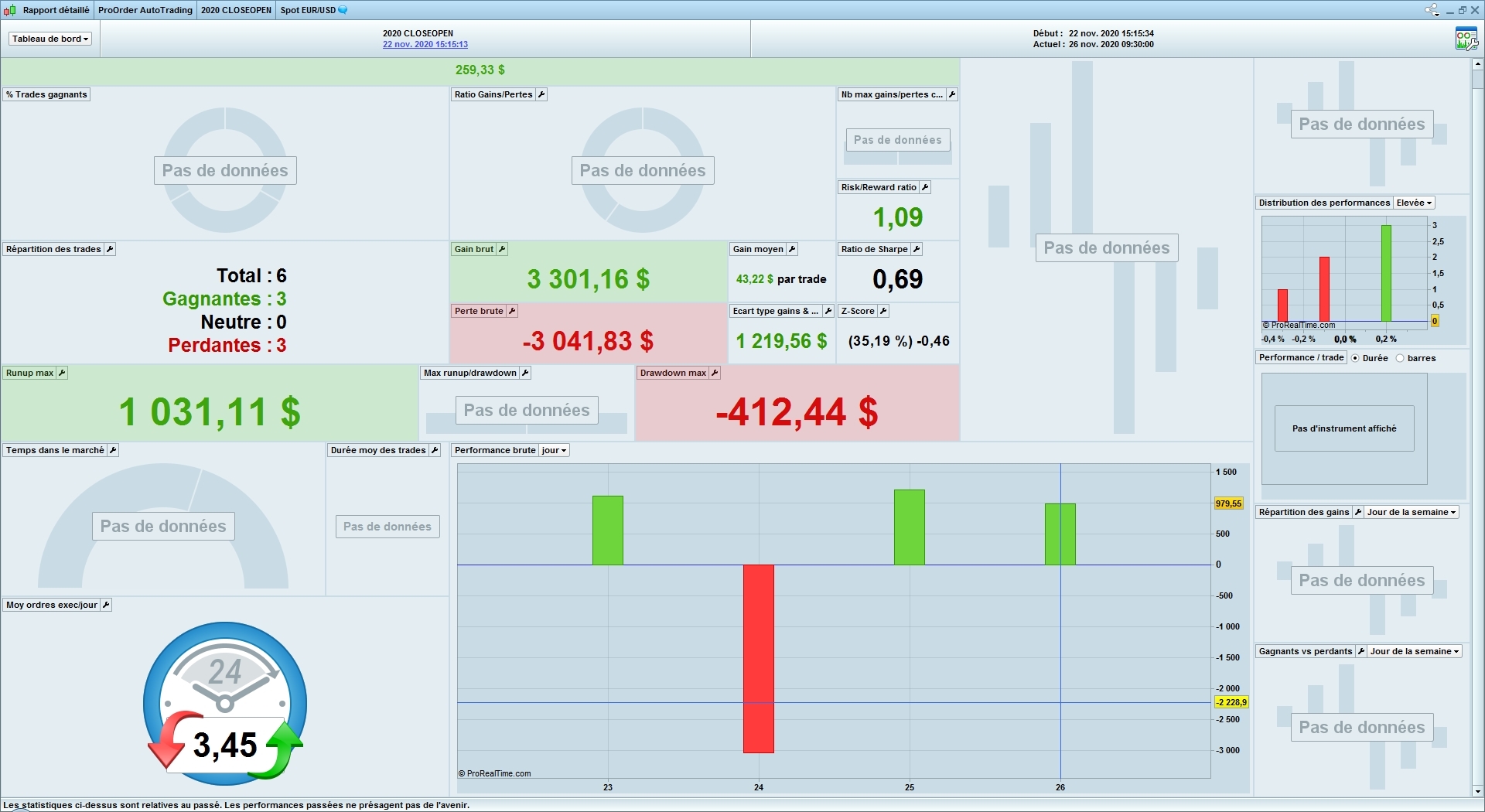

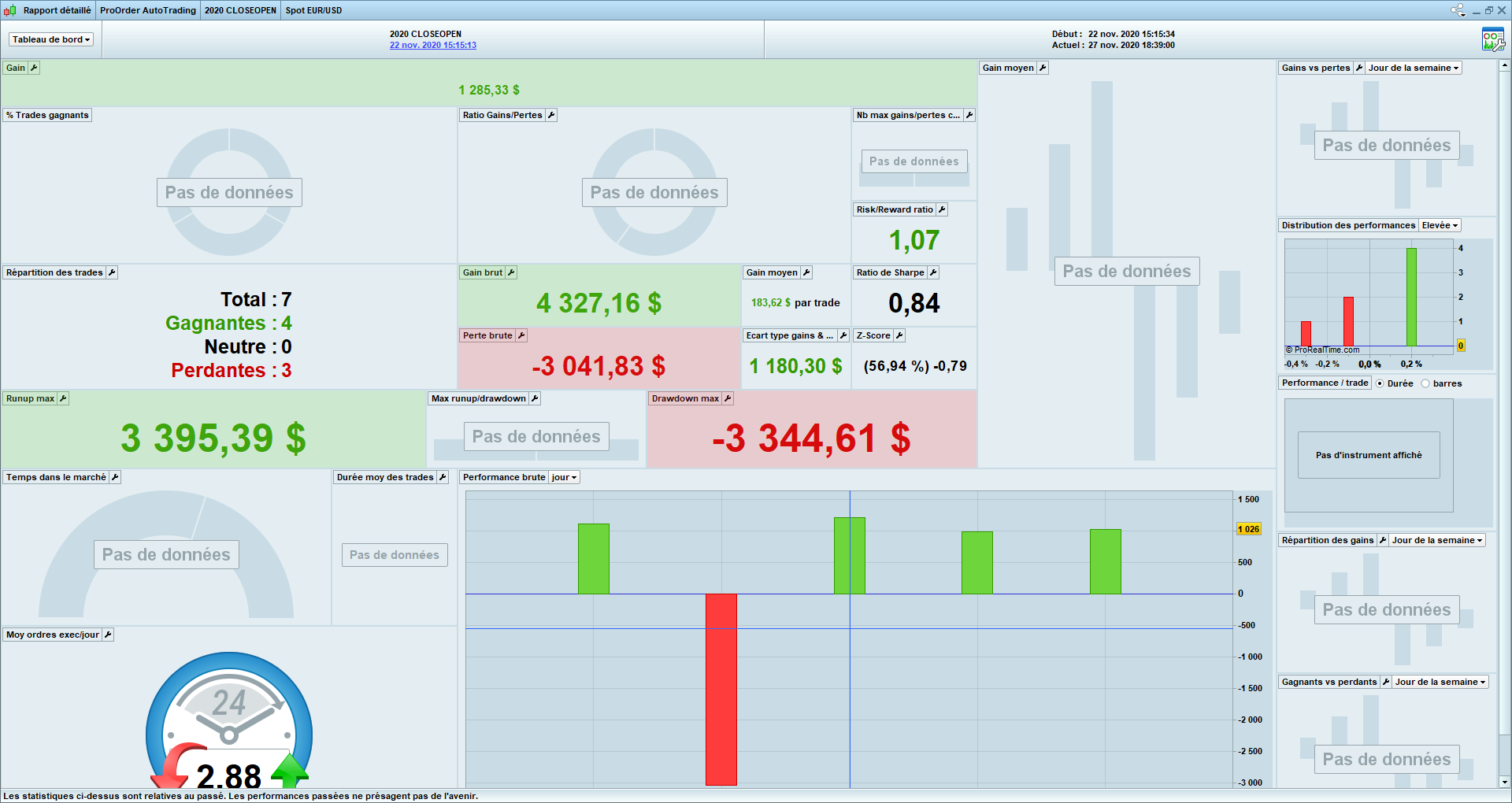

+12 % after one week

We will see what happen next week (To remember the IS/OOS backtest should be work/reevaluate after 2 weeks)

happy week-end

please show how many contracts

3000 as before?

No if I remember 1000-1500 but not really important

Just need to be enough for spread, slippage …

What has number of contracts got to do with spread and slippage?