Hi Guys,

A little bit of time to test new ideas and analyze with Excel to select parameters

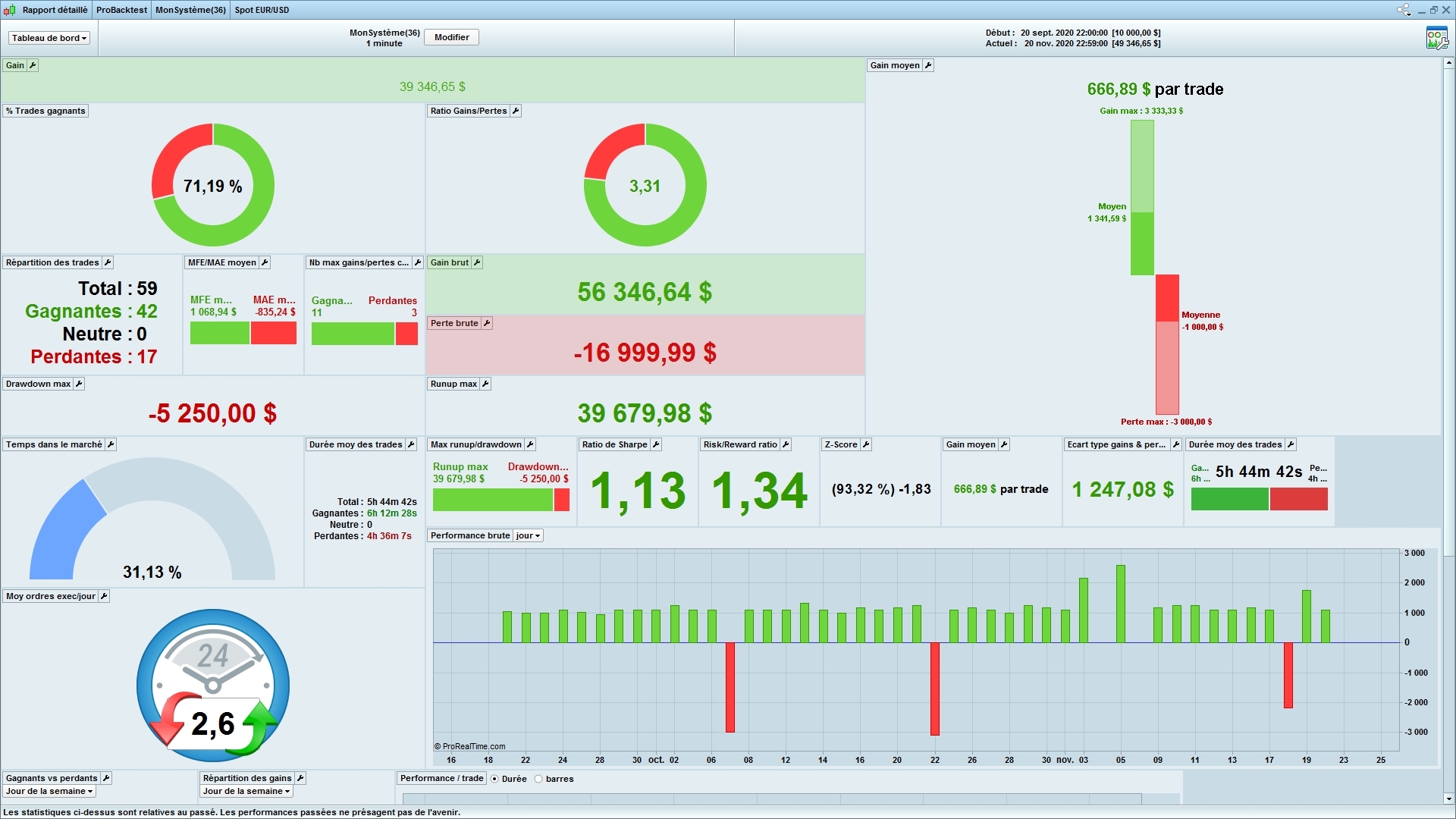

EUR/USD on 1 mn

The signal is very simple and very Donkey

c1 = (Dclose(0) > Dopen(0))

c3 = (Dclose(0) < Dopen(0))

First for call, second for short

With a trailing stop for Money management

Very small code and only 2 variables as usual

Win/loss 71.19 % Sharpe ratio 1.13 not excellent but not bad with a so donkey signal, but very bad standard deviation on gain

The goal is to be positive = win money at the end of this week

Let’s go for OOS results and have a nice week

thanked this post

Hello ZILLIQ,

I look carefully at your various comments on prorealcode.

“Always a small code (the more complex your code, the more curefit you will do, the worse OOS results you will have), never more than 3-4 parameters (same reaosns) and so on … Always the same advice. should look at some results like in the photo on an algo i am currently working on which is in my incubator (OOS demo for 10 days) ”

To summarize :

– Small time on the market,

– A sharpe ratio greater than 1.5-2

– a positive gain-loss spread but the lowest to have a regular curve.

– a gain per trade <the average gain

– RISK / REWARD> 1

Is that it? Is that enough to test the robustness of a strategy? On your side, when you have a strategy on IG that does not work on Ib, is it a source of over-optimization or the strategy must be readjusted to adapt to the flow of interactive broker?

All in all a good start to your DONKEY algo with only 2 variables. Good luck 😉

A +

Hello ZILLIQ,

I look carefully at your various comments on prorealcode.

“Always a small code (the more complex your code, the more curefit you will do, the worse OOS results you will have), never more than 3-4 parameters (same reaosns) and so on … Always the same advice. should look at some results like in the photo on an algo i am currently working on which is in my incubator (OOS demo for 10 days) ”

To summarize :

– Small time on the market,

– A sharpe ratio greater than 1.5-2

– a positive gain-loss spread but the lowest to have a regular curve.

– a gain per trade <the average gain

– RISK / REWARD> 1

Is that it? Is that enough to test the robustness of a strategy? On your side, when you have a strategy on IG that does not work on Ib, is it a source of over-optimization or the strategy must be readjusted to adapt to the flow of interactive broker?

All in all a good start to your DONKEY algo with only 2 variables. Good luck 😉

A +

Yes it is my point of view to “predict” the correlation IS/OOS whatever if it is IG, IB or others

I work actually with Excel to find some predictors because there is still some missing points on PRT

have a nice day

Zilliq

Hi Guys,

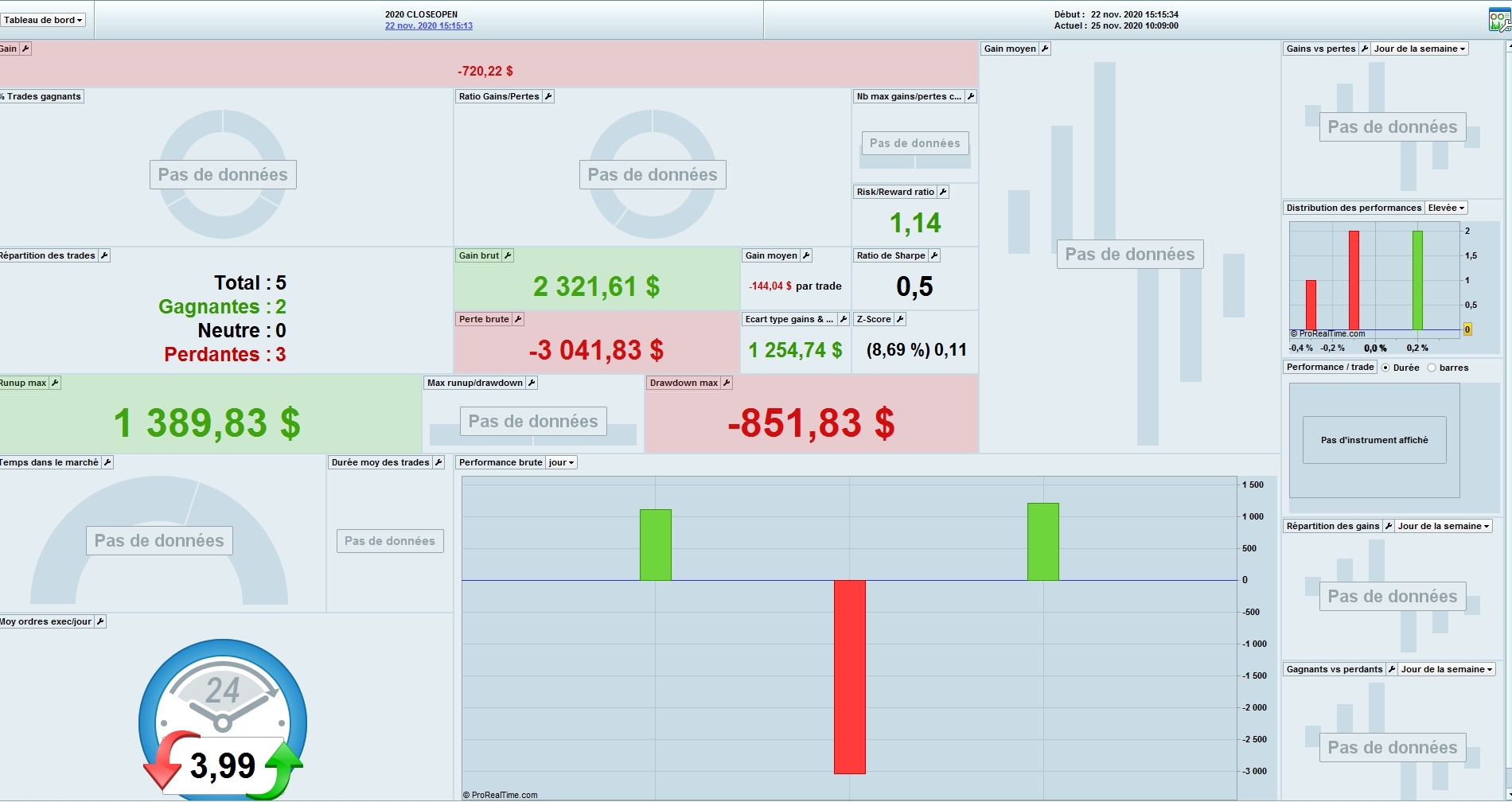

Ouch, big big fall yesterday on EUR/USD !!!

1/ It’s why we need Stop loss or stop trailing

2/ Very good for further backtest who will include this “artefact”

3/ Why we need to haave algo on different markets not connected

this little “artefact” cant/wont/will not make future strategies better in any way. one single event cant forsee another crash like that one.

so what are you trying to say?

Yes it can in some way

This “crash” is included in the data of the backtest like range/trend phase and so OOS will be better

The more phase/crash and so on..; you have, the better it is

In other way if you do a backtest with only trend phase up or down, at the first range phase you will lose in OOS and vice versa

In other way, more market structure you have in your historic, better it is

Bye

if one event is important to you in creating algos, i would say you are curvefitting

if one event is important to you in creating algos, i would say you are curvefitting

No @snuckle

Many events are curvefitting in some way

But one event is a bless 😉

Life goes on …

….except for the three legged donkey that will now end up in the sausage factory.

LOL, you’re right Vonasi 🙂

But to win we need to accept to lose, that’s life

Have a nice day

i don’t believe it. Impossible to have a good strategy with so few variables. (2…)

This topic is interesting but it just pure fantasy. In the theoretical concept ok, but one or the other one can give bad results or not.

moreover, be very little on the market with high timeframe (M15 for example) (in order to have a big historic) does not give good results

Hi @MAKSIDE

It’s not fantasy and not even theory because quite all algos I code have only 2 or 3 variables (with some tricks, for example on MACD a, 2*a for variables), not more for all reasons I already said

And of course you can give very good result with small time in market (As all pros write on books)

Give me a little time this afternoon and I will show you

Have a nice day

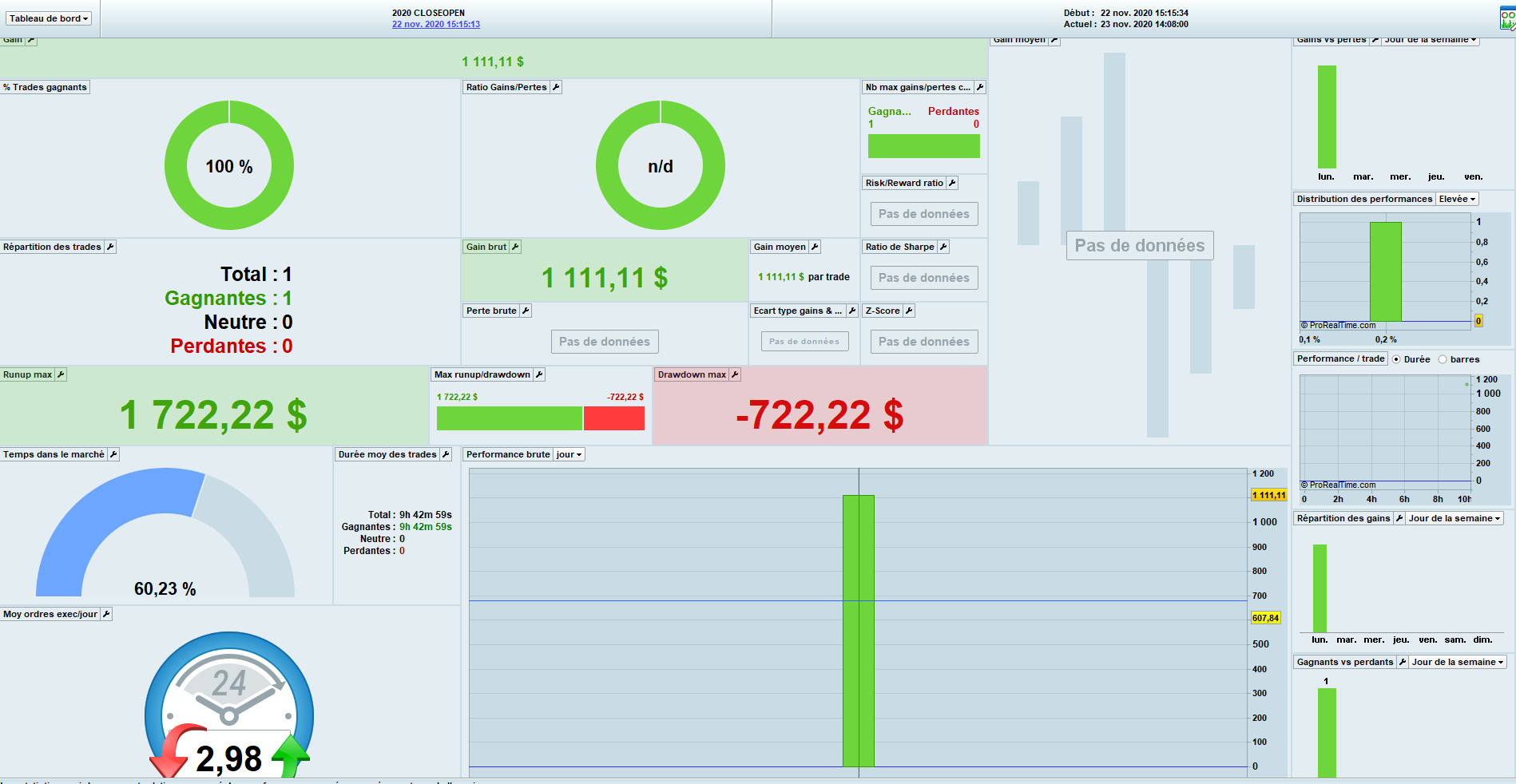

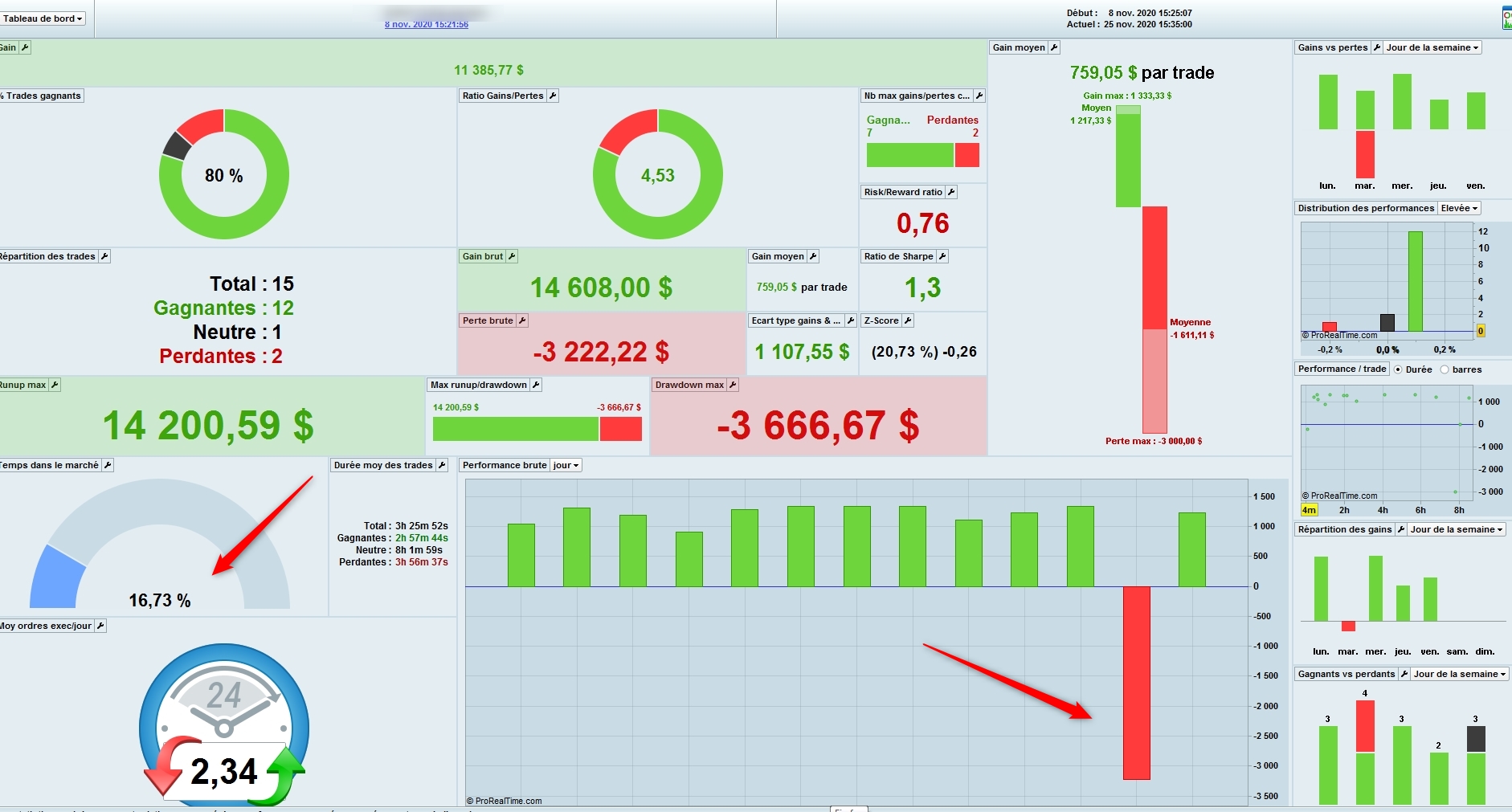

One example @MAKSIDE of my “incubator”

The purpose is to have Algo who works for 2 weeks and another backtest should be done (Because I do a kind of WF on 2 weeks on one pass Cf other post)

Whatever, on this algo as you see, it works very well since 2 weeks (OOS demo results), with 16 % on Market and only 3 variables

(We see the “accident” on EUR/USD from yesterday (0.1 down who is very rare and as Forrest Gump said “It happens” !)

The future objective is to put the “better algos” of the “Incubator” in the future V11 IG Version on Real

Have a nice day