Impressive to see MOD get better and better and that people share their findings!

@nonetheless

-Why do you choose to divide the NAS version into a separate L and S algo? (worse results in a combined one or just for testing out values and combine later?)

-Is there a reason that the NAS version is based on v4, not v5? (I saw that you wrote that v5 should be a good template when testing on other markets)

-Ever tried any of the versions of MOD on forex? (I guess there has to be some changes made to make it even work)

Thanks in advance, Oboe

Paul

PaulParticipant

Master

mmm probably it was easier using only this row

condbuy=c1 and c3 and c5 and c7 and c9 and c11 and c13 and c15 and c19 and c21 and c23

condsell=c2 and c4 and c6 and c8 and c10 and c12 and c14 and c16 and c20 and c22 and c24

and keeping the reset conditions to 1. Something to check.

Thanks Paul, not entirely sure if i get it (cuz I’m a bit simple) but I’ll play around with it at the weekend. 👍

@OboeOpt, yes the Nasdaq being so much more volatile it benefited enormously from splitting the code into long and short. The Dow not so much so I left it as one.

NAS v4 and DJ v5 are the same structure, the Dow has just gone through more iterations, so diff number.

Personally I’ve never had much joy with forex so no idea if that would work… you should have a go!

Hello, I have create my topic for my preferite strategy…if you want to aid me !!! Thanks

LUNCH_BIAS_DAX

@volpiemanuele

Do not double post. Ask your question or state something only once and only in one forum. All double posts will be deleted anyway so posting the same question multiple times will just be wasting your own time and will not get you an answer any quicker. Double posting just creates confusion in the forums

Thank you 🙂

@robertogozzi Thanks….just wanted to share It’ s all clear.

@BobOgden

My DJI 5.1 also went short (live on forward testing demo) with the attached parameters.

I have another account where it went short on the back test at the same time but it did not take it on the LIVE demo.

I’ve seen this happen a number of times before and investigated it with IG & PRT. They state that the demo accounts are not entirely accurate and reflective of market action so that there will be discrepancies from time to time.

I’ll also note that I have had this happen on a LIVE $$ account where the trade was taken and it should not have been. I’m currently disputing it with PRT who have admitted fault and I’m in the process of getting the lost funds back.

It is important that we keep PRT and IG honest always and dispute and discrepancies we see collectively. This is the only way they will be motivated to improve the accuracy of the system.

The moral of the story here is that PRT and IG don’t entirely have this sorted out yet and you will see anomalies on both Demo and Live accounts that can not be explained.

My theory is that PRT has a resource limit on the number of cycles it will run against demo accounts and therefore some trades will be taken and others won’t.

More concerning for me is the inaccuracy on the LIVE accounts.

Thanks to all the contributors here,

May I ask those based in Europe or elsewhere do you change the time frame in PRT to New York time zone when loading the DJI code?

Or should I be doing this differently please?

Thanks Saint

the DJ MoD runs 24hrs a day, you don’t need to do anything to your time settings.

The NAS version takes a 1hr break between 23:00 and midnight GMT, so you should adjust the Ctime values for whatever that equates to down under. It should adjust automatically for US daylight saving.

Thanks for sharing all these codes, that is amazing!

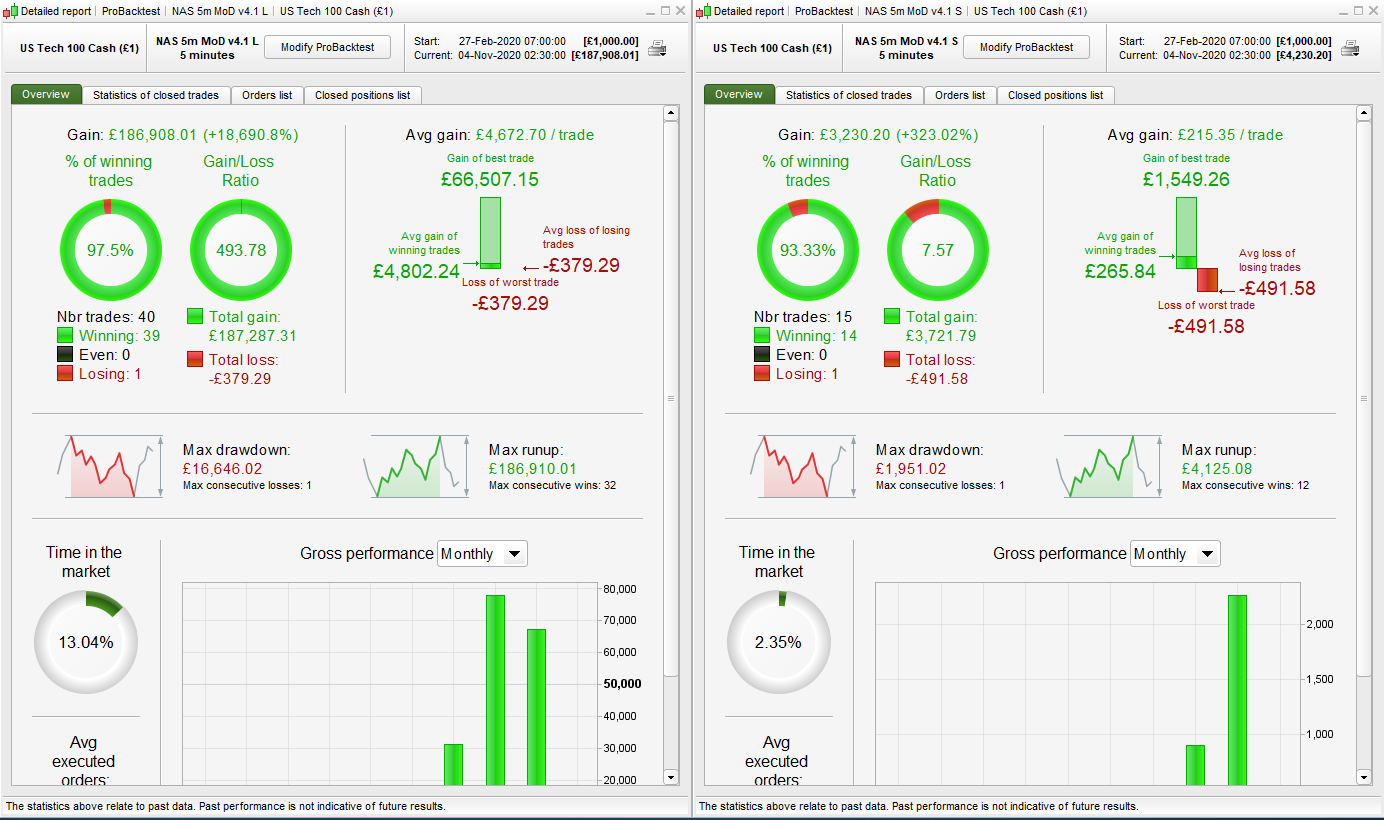

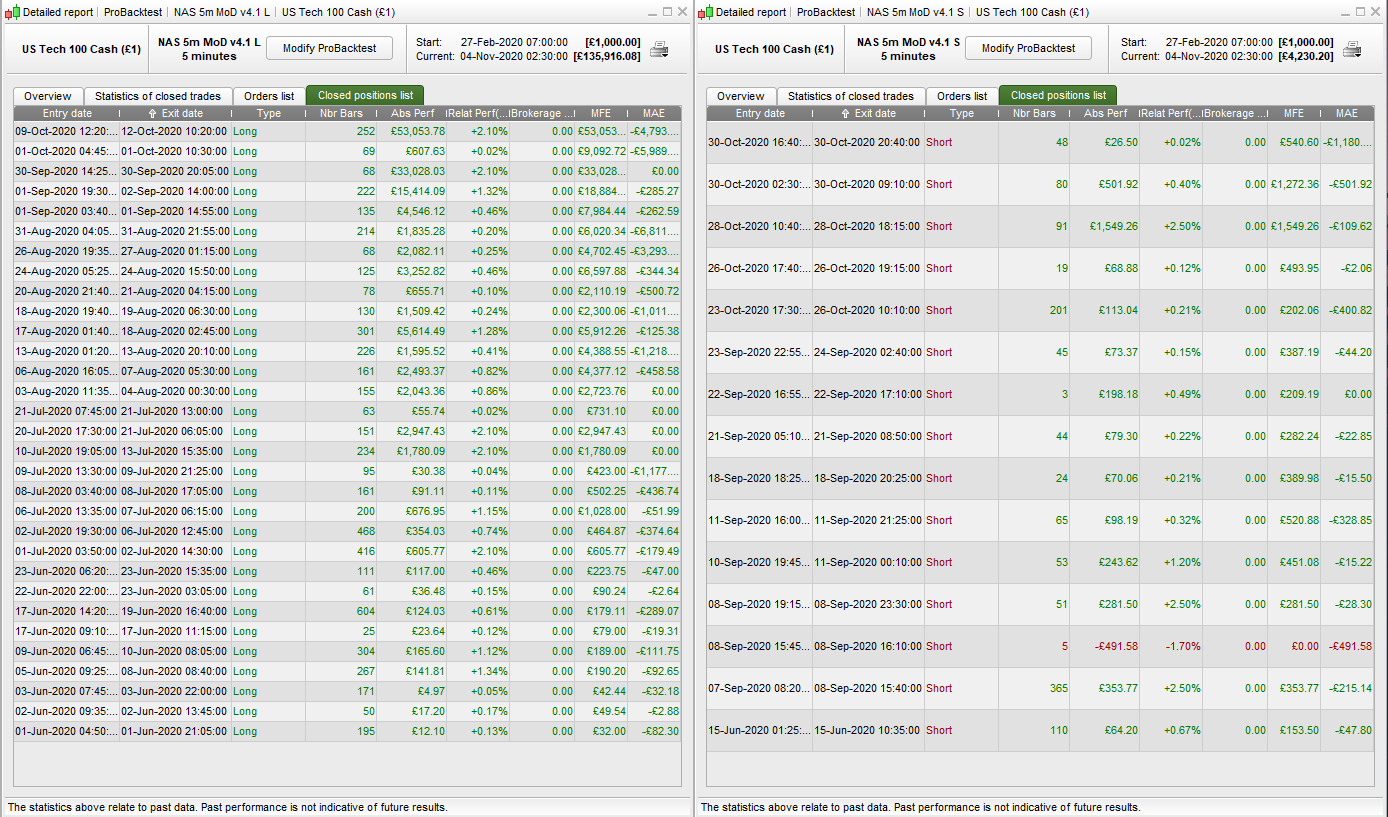

I tested NAS version both Long and Short and I am getting weird results, see attached, I could not explain where the problem is coming from, if you have any idea…Thanks

I expect that you have MM switched on for the long version but not for the short.

Thanks again to all the contributors on this amazing topic.

Anyone running the NAS 5m MoD v4.1 S here ? I launched it without MM (MM=0 & positionsize=1), and it took a position on Nov 3rd, at 06:00:00 UTC, which hit stoploss at 15:15:27 UTC. However, this doesn’t appear in the backtest.

I reached PRT out, and I am now waiting for their answer.

I read that @BobOgden had a similar issue a few days ago with the DJ version.

Hi @nonetheless,

Thank you for sharing this code. I have looked at and I’m trying to re-optimize and adapt the code on many different markets; DAX, US500, NDQ, etc.

The problem I’m experiencing is that after optimizing the H2 and M15/M30 timeframes, the backtest actually looks good enough to start, and if I try to add / optimize the conditions on the 5 minute timeframe, it only makes the result worse.

When optimizing the higher timeframe I look for many trades and high WF. I can have around 400 trades after High and Middle TF optimization, with a 1.6pf when starting to optimize the M5-timeframe.

Whichever values I choose for M5 it only makes the results worse.

If I’m optimizing more boldly I could have a backtest with around 250 trades with a 3pf (still without the m5-timeframe).

I’m thinking that my process is wrong? Maybe one should not optimize the H2 tf without having any M5-conditions at all?

I really don’t see how your process goes to produce your results. How do you find the M5-values?

When optimizing for a new instrument I use 80/20 WF x 1. This gives about 6 months OOS.

I start at the top and do 1 indicator at a time, leaving the TS, SL and TP for last. Then I do it over again at least twice. It’s v time consuming.

I tried to do the SP500 recently but the oos was so bad that I gave up. DAX might be worth it.

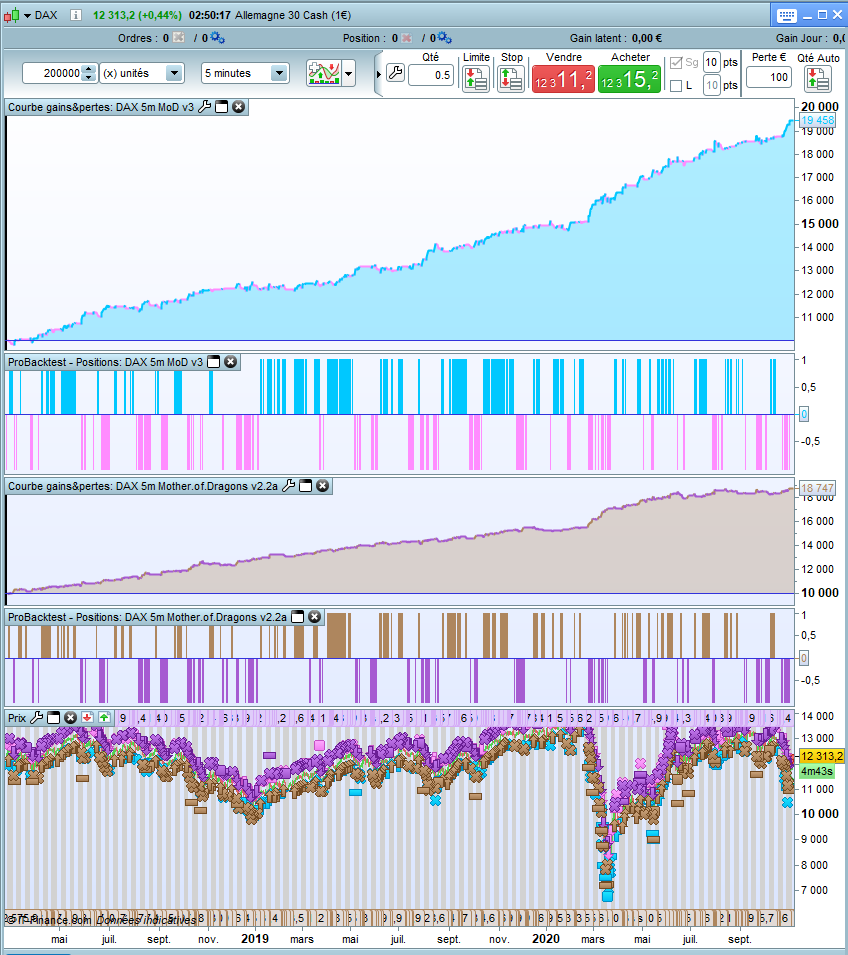

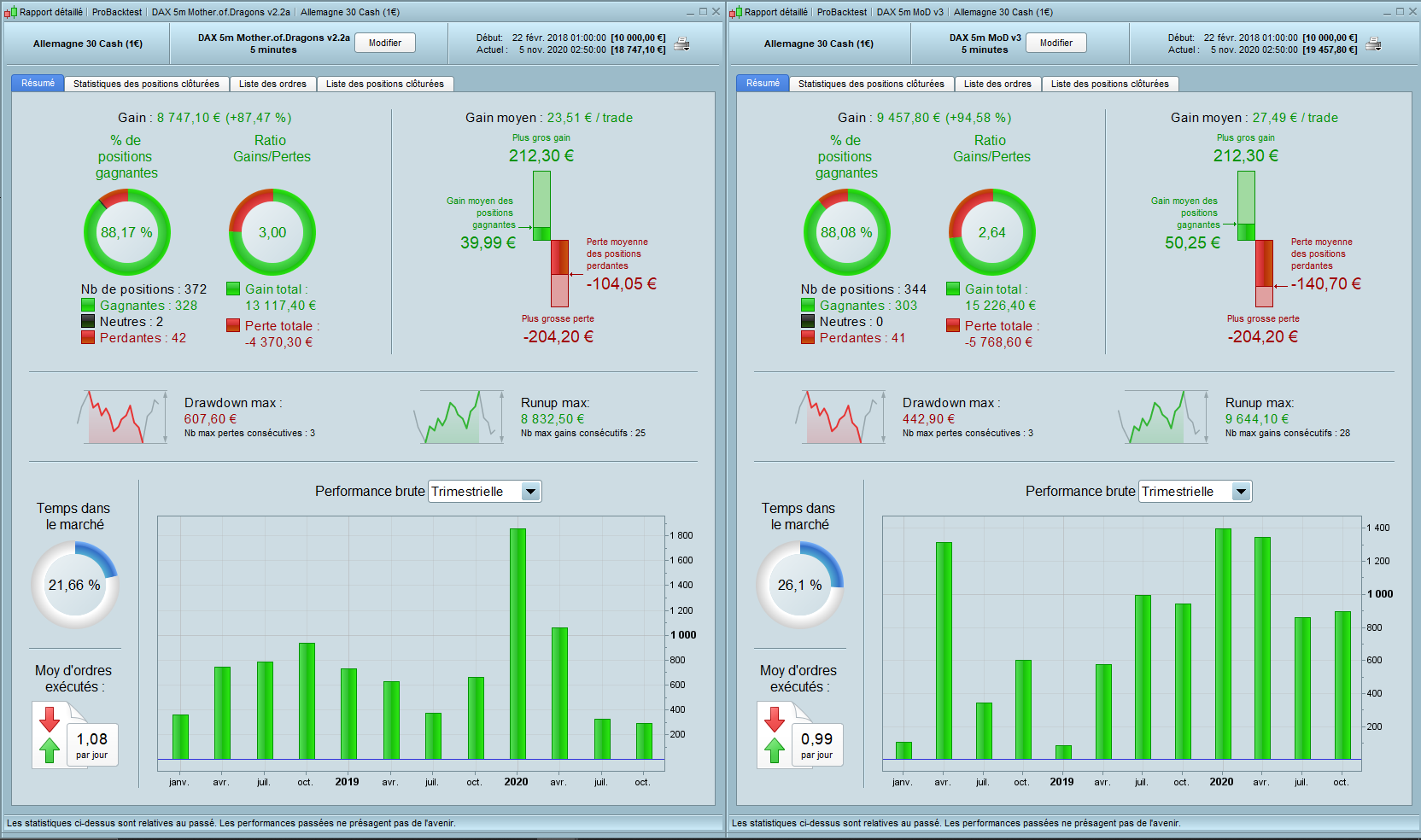

I reoptimised the DJ v5.1 for the Dax, see attached

Not a big amelioration, but, better on the lastest data and less drawdown on the total period. The v2.2a version looks still good. Some variables don’t change this much. Sometimes it can be a good thing to run the same strategy with different parameters like in thise case. We got pretty much the same strategy, but with different parameters and one with the lastest data optimisation, no wf and 200k. Supposed to perform better for this period.

I gave a little eye for a S&P version but looks like this strategy is not supposed to perform on, take care with overfitting for this one. At the moment i’m looking at FTSE, maybe something is possible… Gonna give tests on others but it is very long, more than 2 days.

The best way to do it it’s to slash your variables range and to execute many optimisation windows of a limited number of possibility, like 1000. You can have an eye one more than 1000 results and select variables who give a sense, not just max gain. But i optimise like this only on MoD, because she already proven she win. Don’t optimise like this on strategy you are not sure, or do it on 100k and confirm on 200k.