Ok.. I’ve had a similar issue on another instrument but had some values as low as 3 in the smoothK/smoothD variables. I increased them above 5 and optimised again, haven’t had an issue again yet but it does not fire as often as say the DJI algo. I’d be curious if you increase those to a min of 5 if you continue getting the same error.. I was suspecting that area to be my lines of code failing.. as obviously this can only occur in the code where a division is carried out where the denominator is getting quite small in comparison to the numerator… unless I have missed something elsewhere.

Brent but realized I had to scrap it because of constant zero division error.

Didn’t experience this before. Thanks for sharing.

@christofferrydberg, in any case, I suspect more on this few lines,

MinRSIa = lowest[lengthStocha](myrsia)

MaxRSIa = highest[lengthStocha](myrsia)

StochRSIa = (myRSIa-MinRSIa) / (MaxRSIa-MinRSIa)

I noticed you set the lengthStocha to be 3. In case the market very low volatility, and RSI doesn’t move for 3 bars, then you might result a zero for MaxRSIa-MinRSIa

Maybe you can protect it by something like this,

myRSIa = RSI[lengthRSIa](close)

MinRSIa = lowest[lengthStocha](myrsia)

MaxRSIa = highest[lengthStocha](myrsia)

IF MaxRSIa = MinRSIa THEN

c23 = 0

c24 = 0

ELSE

StochRSIa = (myRSIa-MinRSIa) / (MaxRSIa-MinRSIa)

Ka = average[smoothKa](stochrsia)*100

Da = average[smoothDa](Ka)

c23 = Ka>Da

c24 = Ka<Da

ENDIF

If you really interested to confirm this issue, then you can check the time stamp when the issue is reported to you. Put the indicator on chart, then pay attention to the time stamp so it narrow down your debugging range.

If not above issue, you can still do the same for other division function, by doing a graph of the division.

My version of the system (little changed from the V4a I copied from here) took a long on 1/10/2020 at 12:00:01 and was stopped out for a big loss on 2/10/2020 at 05:55:58. Today I ran the backtest to look at something else and discovered that the backtest does not take this trade and I cannot see why. Even if I copy the code from the live system into a new system and run it it doesn’t take the trade no matter how much I change the spread value (can’t think what else could account for it). Anyone else had this happen?

Hi Autostrategist, yes, unfortunately I experienced the same (currently running version DJ 5m 4.7.2a).

Live entry on 1/10/20 12:00:00 and stop loss hit 2/10/20 05:55:56 (UK times). Doesn’t show up on my backtest.

I’ve been running a version of this since 29 March 2020 and usually real results are very similar to backtest (although 2-3 June and 20 and 24 Aug I found were less good replication). So not just you, but not sure why it happened! Very grateful though for the sharing of this code, as still in profit over that period, despite this 🙂

I added a rounding up for the order sizes, to full numbers, just in case someone has problems orders smaller than 1.

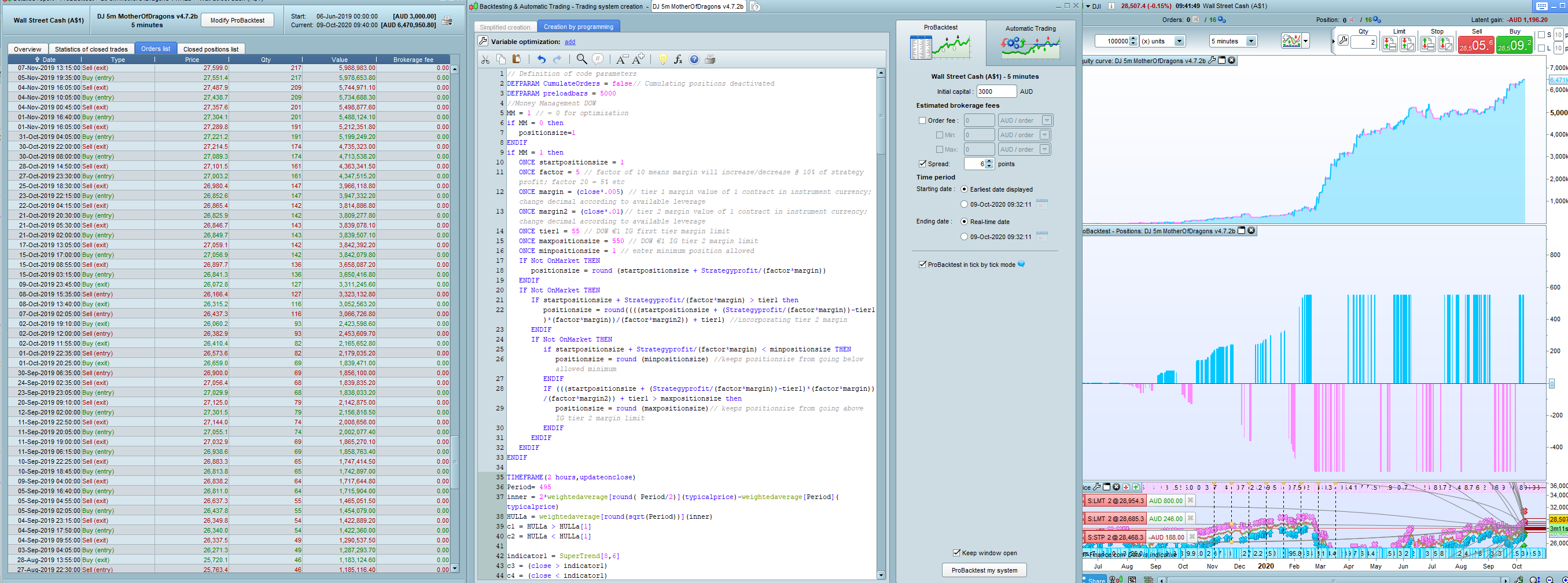

///Definition of code parameters

DEFPARAM CumulateOrders = false// Cumulating positions deactivated

DEFPARAM preloadbars = 5000

//Money Management DOW

MM = 1 // = 0 for optimization

if MM = 0 then

positionsize=1

ENDIF

if MM = 1 then

ONCE startpositionsize = 1

ONCE factor = 5 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE margin = (close*.005) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.01)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 55 // DOW €1 IG first tier margin limit

ONCE maxpositionsize = 550 // DOW €1 IG tier 2 margin limit

ONCE minpositionsize = 1 // enter minimum position allowed

IF Not OnMarket THEN

positionsize = round (startpositionsize + Strategyprofit/(factor*margin))//rounding up

ENDIF

IF Not OnMarket THEN

IF startpositionsize + Strategyprofit/(factor*margin) > tier1 then

positionsize = round((((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1) //incorporating tier 2 margin

ENDIF

IF Not OnMarket THEN

if startpositionsize + Strategyprofit/(factor*margin) < minpositionsize THEN

positionsize = round (minpositionsize) //keeps positionsize from going below allowed minimum

ENDIF

IF (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 > maxpositionsize then

positionsize = round (maxpositionsize)// keeps positionsize from going above IG tier 2 margin limit

ENDIF

ENDIF

ENDIF

ENDIF

TIMEFRAME(2 hours,updateonclose)

Period= 495

inner = 2*weightedaverage[round( Period/2)](typicalprice)-weightedaverage[Period](typicalprice)

HULLa = weightedaverage[round(sqrt(Period))](inner)

c1 = HULLa > HULLa[1]

c2 = HULLa < HULLa[1]

indicator1 = SuperTrend[8,6]

c3 = (close > indicator1)

c4 = (close < indicator1)

ma = average[60,3](close)

c11 = ma > ma[1]

c12 = ma < ma[1]

//Stochastic RSI | indicator

lengthRSI = 15 //RSI period

lengthStoch = 9 //Stochastic period

smoothK = 10 //Smooth signal of stochastic RSI

smoothD = 5 //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K = average[smoothK](stochrsi)*100

D = average[smoothD](K)

c13 = K>D

c14 = K<D

TIMEFRAME(30 minutes,updateonclose)

indicator5 = Average[2](typicalPrice)

indicator6 = Average[7](typicalPrice)

c15 = (indicator5 > indicator6)

c16 = (indicator5 < indicator6)

TIMEFRAME(15 minutes,updateonclose)

indicator2 = Average[4](typicalPrice)

indicator3 = Average[8](typicalPrice)

c7 = (indicator2 > indicator3)

c8 = (indicator2 < indicator3)

Periodc= 23

innerc = 2*weightedaverage[round( Periodc/2)](typicalprice)-weightedaverage[Periodc](typicalprice)

HULLc = weightedaverage[round(sqrt(Periodc))](innerc)

c9 = HULLc > HULLc[1]

c10 = HULLc < HULLc[1]

TIMEFRAME(10 minutes)

indicator1a = SuperTrend[2,7]

c19 = (close > indicator1a)

c20 = (close < indicator1a)

TIMEFRAME(5 minutes)

//Stochastic RSI | indicator

lengthRSIa = 3 //RSI period

lengthStocha = 6 //Stochastic period

smoothKa = 9 //Smooth signal of stochastic RSI

smoothDa = 3 //Smooth signal of smoothed stochastic RSI

myRSIa = RSI[lengthRSIa](close)

MinRSIa = lowest[lengthStocha](myrsia)

MaxRSIa = highest[lengthStocha](myrsia)

StochRSIa = (myRSIa-MinRSIa) / (MaxRSIa-MinRSIa)

Ka = average[smoothKa](stochrsia)*100

Da = average[smoothDa](Ka)

c23 = Ka>Da

c24 = Ka<Da

ma3 = average[15,3](close)

c21 = ma3 > ma3[1]

c22 = ma3 < ma3[1]

Periodb= 15

innerb = 2*weightedaverage[round( Periodb/2)](typicalprice)-weightedaverage[Periodb](typicalprice)

HULLb = weightedaverage[round(sqrt(Periodb))](innerb)

c5 = HULLb > HULLb[1]and HULLb[1]<HULLb[2]

c6 = HULLb < HULLb[1]and HULLb[1]>HULLb[2]

// Conditions to enter long positions

IF dhigh(0)-high<250 and c1 AND C3 AND C5 and c7 and c9 and c11 and c13 and c15 and c19 and c21 and c23 THEN

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS 1.5

SET TARGET %PROFIT 2.4

ENDIF

// Conditions to enter short positions

IF low-dlow(0)<700 and c2 AND C4 AND C6 and c8 and c10 and c12 and c14 and c16 and c20 and c22 and c24 THEN

SELLSHORT positionsize CONTRACT AT MARKET

SET STOP %LOSS 1.5

SET TARGET %PROFIT 2.2

ENDIF

//================== exit in profit

if longonmarket and C6 and c8 and close>positionprice then

sell at market

endif

If shortonmarket and C5 and c7 and close<positionprice then

exitshort at market

endif

//==============exit at loss

if longonmarket AND c2 and c6 and close<positionprice then

sell at market

endif

If shortonmarket and c1 and c5 and close>positionprice then

exitshort at market

endif

//%trailing stop function

trailingPercent = .26

stepPercent = .014

if onmarket then

trailingstart = tradeprice(1)*(trailingpercent/100) //trailing will start @trailingstart points profit

trailingstep = tradeprice(1)*(stepPercent/100) //% step to move the stoploss

endif

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart THEN

newSL = tradeprice(1)+trailingstep

ENDIF

//next moves

IF newSL>0 AND close-newSL>trailingstep THEN

newSL = newSL+trailingstep

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart THEN

newSL = tradeprice(1)-trailingstep

ENDIF

//next moves

IF newSL>0 AND newSL-close>trailingstep THEN

newSL = newSL-trailingstep

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

//************************************************************************

IF longonmarket and barindex-tradeindex>1800 and close<positionprice then

sell at market

endif

IF shortonmarket and barindex-tradeindex>610 and close>positionprice then

exitshort at market

endif

//=============================================

if longonmarket and abs(open-close)<1 and high[1]>high and close>positionprice and high-close>10then

sell at market

endif

if shortonmarket and abs(open-close)<1 and low[1]>low and close-low>13 and close<positionprice then

exitshort at market

endif

//===================================

myrsiM5=rsi[14](close)

//

if myrsiM5<30 and barindex-tradeindex>1 and longonmarket and close>positionprice then

sell at market

endif

if myrsiM5>70 and barindex-tradeindex>1 and shortonmarket and close<positionprice then

exitshort at market

endif

// --------- US DAY LIGHT SAVINGS MONTHS ---------------- //

mar = month = 3 // MONTH START

nov = month = 11 // MONTH END

IF (month > 3 AND month < 11) OR (mar AND day>14) OR (mar AND day-dayofweek>7) OR (nov AND day<=dayofweek AND day<7) THEN

USDLS=010000

ELSE

USDLS=0

ENDIF

once openStrongLong = 0

once openStrongShort = 0

if (time <= 223000 - USDLS and time >= 050000 - USDLS) then

openStrongLong = 0

openStrongShort = 0

endif

//detect strong direction for market open

once rangeOK = 40

once tradeMin = 1500

IF (time >= 223500 - USDLS) AND (time <= 223500 + tradeMin - USDLS) AND ABS(close - open) > rangeOK THEN

IF close > open and close > open[1] THEN

openStrongLong = 1

openStrongShort = 0

ENDIF

IF close < open and close < open[1] THEN

openStrongLong = 0

openStrongShort = 1

ENDIF

ENDIF

once bollperiod = 20

once bollMAType = 1

once s = 2

bollMA = average[bollperiod, bollMAType](close)

STDDEV = STD[bollperiod]

bollUP = bollMA + s * STDDEV

bollDOWN = bollMA - s * STDDEV

IF bollUP = bollDOWN THEN

bollPercent = 50

ELSE

bollPercent = 100 * (close - bollDOWN) / (bollUP - bollDOWN)

ENDIF

once trendPeriod = 70

once trendPeriodResume = 30

once trendGap = 3

once trendResumeGap = 6

if not onmarket then

fullySupported = 0

fullyResisteded = 0

endif

//Market supported in the wrong direction

IF shortonmarket AND fullySupported = 0 AND summation[trendPeriod](bollPercent > 50) >= trendPeriod - trendGap THEN

fullySupported = 1

ENDIF

//Market pull back but continue to be supported

IF shortonmarket AND fullySupported = 1 AND bollPercent[trendPeriodResume + 1] < 0 AND summation[trendPeriodResume](bollPercent > 50) >= trendPeriodResume - trendResumeGap THEN

exitshort at market

ENDIF

//Market resisted in wrong direction

IF longonmarket AND fullyResisteded = 0 AND summation[trendPeriod](bollPercent < 50) >= trendPeriod - trendGap THEN

fullyResisteded = 1

ENDIF

//Market pull back but continue to be resisted

IF longonmarket AND fullyResisteded = 1 AND bollPercent[trendPeriodResume + 1] > 100 AND summation[trendPeriodResume](bollPercent < 50) >= trendPeriodResume - trendResumeGap THEN

sell at market

ENDIF

//

//Started real wrong direction

once strongTrend = 60

once strongPeriod = 8

once strongTrendGap = 2

IF shortonmarket and openStrongLong and barindex - tradeindex < 12 and summation[strongPeriod](bollPercent > strongTrend) = strongPeriod - strongTrendGap then

exitshort at market

ENDIF

IF longonmarket and openStrongShort and barindex - tradeindex < 12 and summation[strongPeriod](bollPercent < 100 - strongTrend) = strongPeriod - strongTrendGap then

sell at market

ENDIF

I have tried to run Mother of dragons v4.5 live for a while. The only Changes I have made is my own optimization of the values. Time after time the algo is stopped because “division by zero”.

Is there a general way to eliminate that or how do a newbie in PRT coding proceed to fix this?

hi, which version do you suggest to me to trade in real ? I’m interested on NQ, DJ and DAX.

Thanks

@OboeOpt Might be stating the obvious but a division by zero error occurs when the variable to the right of the division operator i.e. ‘/’ is zero. Take this line from MOD code as an example (myRSIa–MinRSIa) / (MaxRSIa–MinRSIa), if ever the values to the right of the ‘/’ were to equal zero (not saying they can) then the error would occur. I have been running MOD and a DAX version for months without seeing this error. I have seen the error in the past with other systems and it is usually caused by a situation in the market that had not been accounted for like when the DJI was paused on limit up or down or a market is unusually quiet and fails to make one or more bars for a while etc. The only way to track it down is to work through all the possible divisions and see which one is causing the error.

@Andrew7

Normally I can figure out why a trade was taken even though I wasn’t expecting it e.g. a difference in the spread from live Versus backtest or insufficient backtest data for the moving average but in this case I couldn’t work it out so I raised the issue with PRT, see below:

The referenced strategy took a long on 1/10/2020 at 12:00:01 and exited at a loss on 2/10/2020 at 05:55:58. The backtest does not take this trade and I cannot see why. Can you explain please.

Concerned strategy: (required) : DJ 5m Mother of Dragons v4.9 – Wall Street (DFB) – 28-Jun-2020 16:51:22

To my amazement I got this response:

We have identified the problem you reported about your backtest and our technical team is currently working on a correction, which will be implemented as soon as possible. Please note that depending on the complexity of the correction needed, it may take up to several weeks for the problem to be corrected.

That errant trade cost me several hundred pounds but I don’t expect they will be compensating me 🙁 .

Mother of Dragons made in one week its 2 worst losses since Feb 2018. In both cases, it first closed one long position (in profit) and took again a long position a few minutes later.

Then this position would stay opened several hours / days until it hits stoploss. I was wondering whether it would be great to prevent the robot to open a new position if another one has been closed a few minutes ago.

What are your thoughts about that ?

thanked this post

You can use something like the below, I got this from one of the PRC gurus. It will force the strategy to wait N bars. However, the reality is that the returns are such that you sometimes just take the rough with the smooth, or you risk missing out on the next big move.

//Wait

ONCE Count = 0

ONCE MinCount = 5

IF (Not OnMarket AND OnMarket[1]) OR (StrategyProfit <> StrategyProfit[1]) THEN //check thare was a trade open the previous bar and not any longer....

Count = 1 //... to start counting periods (bars)

ELSE

Count = Count + 1 //increment Count at each new period (bar)

ENDIF

IF OnMarket THEN

Count = 0

ENDIF

You can use something like the below, I got this from one of the PRC gurus. It will force the strategy to wait N bars. However, the reality is that the returns are such that you sometimes just take the rough with the smooth, or you risk missing out on the next big move.

//Wait

ONCE Count = 0

ONCE MinCount = 5

IF (Not OnMarket AND OnMarket[1]) OR (StrategyProfit <> StrategyProfit[1]) THEN //check thare was a trade open the previous bar and not any longer….

Count = 1 //… to start counting periods (bars)

ELSE

Count = Count + 1 //increment Count at each new period (bar)

ENDIF

IF OnMarket THEN

Count = 0

ENDIF

//Wait

ONCE Count = 0

ONCE MinCount = 5

IF (Not OnMarket AND OnMarket[1]) OR (StrategyProfit <> StrategyProfit[1]) THEN //check thare was a trade open the previous bar and not any longer….

Count = 1 //… to start counting periods (bars)

ELSE

Count = Count + 1 //increment Count at each new period (bar)

ENDIF

IF OnMarket THEN

Count = 0

ENDIF

Thank you for your answer. I will look into it.

But I agree, with this code implemented, it could miss the next big move…

It’s worth noting, with elections in the US soon it’s worth de-risking for the next few weeks.

Hola he puesto lo que le dices a la Madre de Dragones y da un error en mincount. Can you help me please? I’m trying to learn, thank you very much

@

josef1604

In PRT unlike some other programming languages if a variable is declared it has to be used, either use Mincount or comment it out/delete it.