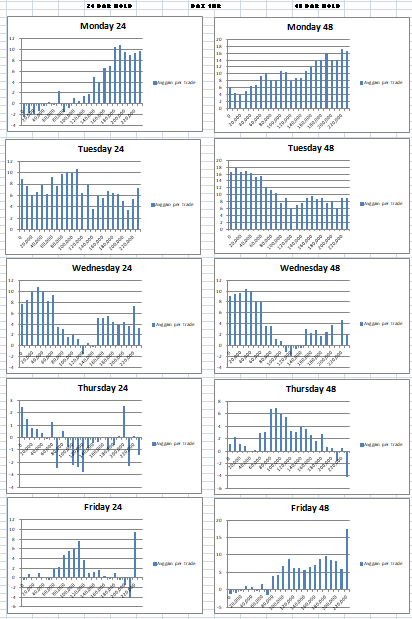

I decided that just holding for one hour did not really tell us much about investor behaviour so I ran the following code with varying length of holding before closing. The results are interesting. I have attached an Excel spread sheet of the 24 bar and 48 bar hold results on the DAX.

D is the variable 1 to 5 to represent Monday to Friday and T is the variable for time 000000 to 230000 step 010000. TradeLength is the number of bars to hold before selling.

Obviously run it on the 1HR chart.

DefParam CumulateOrders = false

IF OpenDayofweek = D and OpenTime = T then

buy 1 contract at market

Endif

If OnMarket and BarIndex - TradeIndex >= TradeLength THEN

sell at market

Endif

Analysing the 48 bar hold it seems that the beginning of the week is a better time to buy and then things start tailing off as the week progresses. Interestingly late on Friday is a good time to buy and hold for 48 bars. That kind of reminds me of Warren Buffett’s theory of buying when others are getting out!

Everyone knows that some times are better than others to trade but it is interesting to see it in graphical format.

It would be great if those with more time could run tests on other markets and over longer or different holding periods and post the results on here.

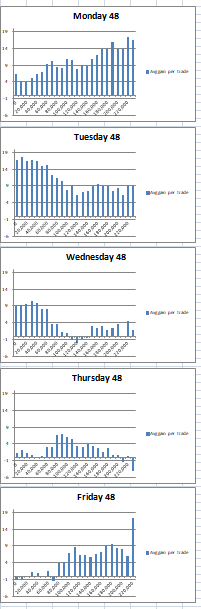

Trade DAX on short term time scales from Monday through Thursday between 9 and 10 am. And on Friday afternoon, after market opening in US. This is pretty regular.

My 48 hour buy, hold and then sell test would indicate that that is not far off the mark although I am not sure that between 9 and 10 are necessarily the best times (maybe for very short term trades but not 48 hour ones). Wednesday lunchtime through to Friday lunchtime appears to be a very good time to walk away from trading the DAX long and go and do something better. Now that is a very simple filter to add to any DAX strategy that does not hold for longer than 48 hours. It should give an edge if the DAX continues to have similar daily characteristics in the future.

The Friday afternoon thing interests me. I guess it is good to buy when others are closing their positions for the weekend and so price is dropping and giving good value and then everybody wants to buy them all back from you on Monday.

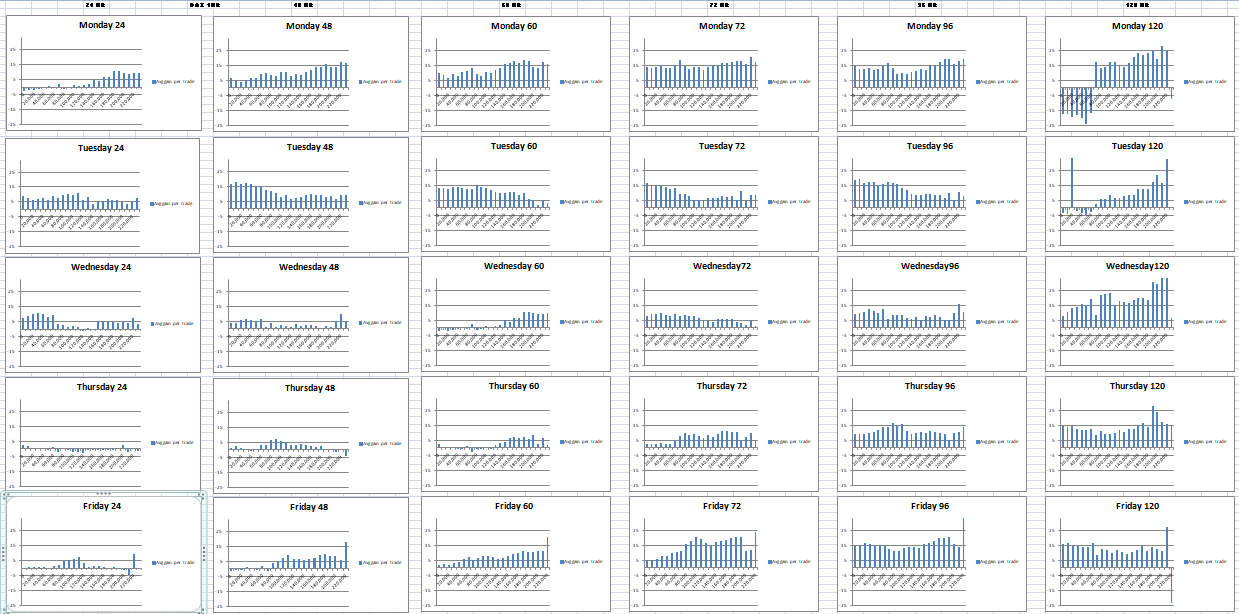

I did a little more testing on buying, holding for a period and selling on the DAX 1HR to try to establish when are good times of the week to buy. The results are once again quite interesting.

Image attached for results covering holding for 24,48,60,72,96 and 120HR and Excel spreadsheet also attached.

It definitely seems to show the benefit of longer holding over short term profit taking and also highlights times of the week when it is clearly a good time to buy and good time not to.

Hello dear ones.

I haven’t been here for a while, but what do my blind eyes see?

You have taken up the thought of me and followed and worked on it here. Thank you very much indeed!

I need to read and understand what you’ve done, and then I’ll come back.

But one thing seems to be certain, investor behavior is different from time to time.

Thank you very much indeed!

But one thing seems to be certain, investor behavior is different from time to time.

No problem JohnScher. I’ve not had much time to continue with it myself recently either.

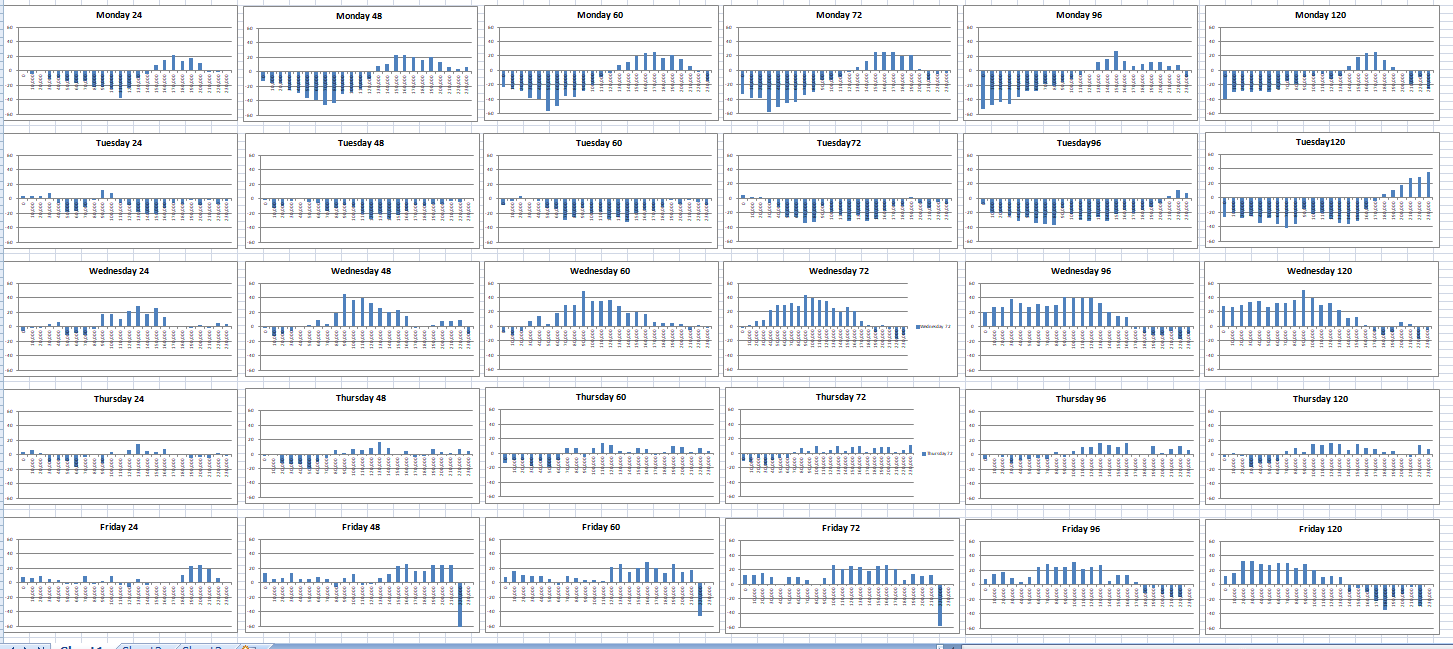

With the information provided in my analysis it would be very easy to write a strategy that makes fantastic profits over the backtest period but (and it is a big but) whether it would continue to in the future can only be confirmed by very long term forward testing.

Also I guess that the behaviour would be very different in a major market correction such as during the GFC period compared to a bullish up trending market – and as ever identifying when these periods start and end is another challenge altogether.

It might be worth breaking the historical data down in to these different periods and running analysis to compare. Unfortunately I am a bit short of time to do that at the moment.

At minimum as it is the info could add some sort of potential edge to any strategy that buys and holds for two to three days by limiting buying to only certain periods of the week that have proven to be more lucrative in the past.

Hello, Vonasi.

I was just had today a look at the results of the Hold and Buy. That looks good!

I’m grateful for the code you put in, too. Once again I lacked the most basic programming knowledge. I’ll take the code and put 2.3 filters under it. Maybe we’ll get even better results.

I also just remembered that one could perhaps also integrate the seasonal pattern from the Pathfinder system and test whether the holding period should be varied in the corresponding (half-) months for better back test results. What do you mean? Would that be a good approach?

I have not done any further testing on this idea but may look into it if I get some time. I’m not so sure about the Pathfinder seasonality idea and as with any longer term seasonality it can become very easy to fit a strategy to historic seasonality and then find it does not fit the future. The seasonality has to be very strong and very consistent to be considered I think.

I think that now that nearly five months has passed since I did the tests shown on here that it would be interesting to run them again over this new OOS period and see if they are the same – especially considering how the markets have been recently. I will try to do it if I can find time.

I ran the same tests on the OOS period that we now have from 15 February to 5 July 2018.

Here are the results:

[attachment file=75464]

The OOS period has shown benefits to trading on Monday afternoon, Wednesday morning and lunchtime and on Fridays. Tuesdays have been a very poor day to trade. Some of this is also similar in the IS test particularly the Monday afternoon and Friday comparison. I think that a longer OOS period is required for better comparison as the OOS data sample is still quite small.

Excel spread sheet also attached to more easily analyse.

[attachment file=”Hour of day OOS DAX 15Feb2018 5Jul2018.xlsx”]

Hello.

Thanks for the overview. I have flown through the overview but have not yet been able to evaluate it.

Instead, I created a program based on my low skills that achieves positive results in the backtest with the optimazingtool.

Here the code on example Wednesday

Defparam cumulateorders = false

TradingDay = Opendayofweek = 3

TradingTime = time = tin*10000

position = 1

// maincode

If TradingDay and TradingTime then

buy position contracts at market

Endif

IF Longonmarket and time= tout*10000 Then

sell at market

Endif

Set Target %profit tp

Optimized with the Optimazingtool the best results are achieved with

tin = 080000

tout = 070000

TP = 1.9

(I put in the SL as “insurance” at 2% after backtest.)

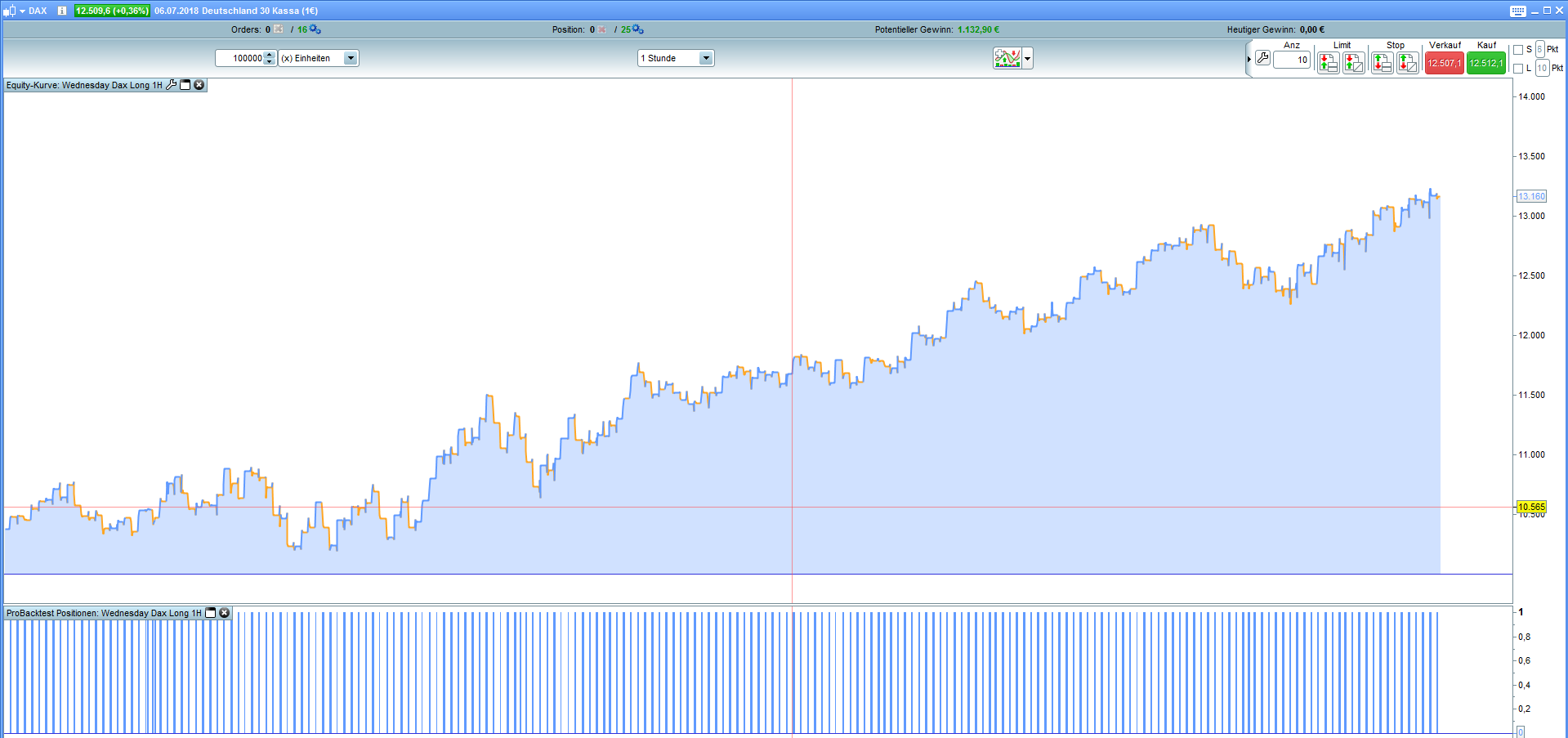

With a spread of 2 and 100,000 bar test I get to 3,160., see attached.

Is it possible for you, do you have time (?) to check my result?

Somehow, I don’t trust the good result.

the complete code, here

Defparam cumulateorders = false

TradingDay = Opendayofweek = 3

TradingTime = time = 080000

position = 1

// maincode

If TradingDay and TradingTime then

buy position contracts at market

Endif

IF Longonmarket and time= 070000 Then

sell at market

Endif

Set Stop %Loss 2 // as insurance

Set Target %profit 1.9

If only it were that easy! I am guessing that you are on a different trading clock tome (I use GMT +1) but this is what I get using time in as 070000 and time out of 060000.

[attachment file=75535]

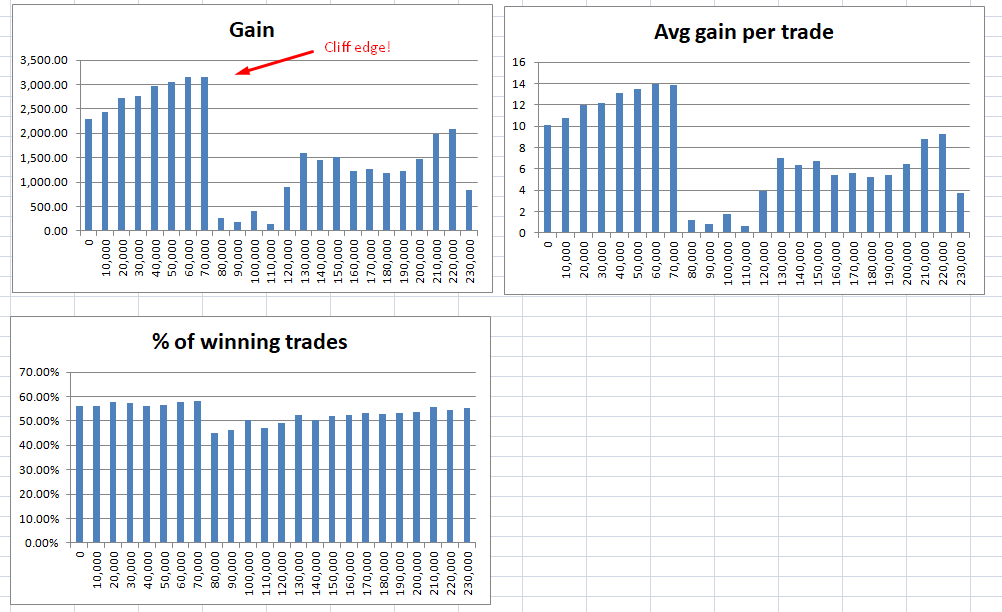

Which looks lovely but if you plot charts of the times either side of the exit time then you get this:

[attachment file=75536]

Which shows your trade standing near a cliff edge. Just a handful of minutes in the wrong direction and your strategy is suddenly rubbish.

I’m afraid that it is pure data mining of the last 100K bars. Yes it has worked in the past but there is no logical reason why it should work in the future. I think time has a place in a strategy but it has to be linked to an overall picture. For example you want to buy a position this week as price is good value and you know that historically prices are lower on a Friday afternoon as every one is off-loading for the weekend so you wait till Friday afternoon to get a hopefully even better price. Just buying and selling based on time is the road to the poor house IMHO. The stop loss and take profit offer no insurance as at any time entering the market based on just time you have 50% chance of being right and 50% chance of being wrong. The SL and TP levels swing this slightly towards being right more often but the losses are bigger than the wins so this takes it back to 50/50 and then the spread makes sure that you will lose money.

When you say data mining, I think I know what you’re talking about. Occasionally one reads again and again of problems, which do not agree results of the Backtestes with the results acting in the demo and/or also live version.

As far as I have noticed, this problem runs through all CFD brokers offering MT4 or other platforms.

We will only be able to solve this problem for ourselves if we find a broker who provides reliable valid data, who provides data that goes back a long way and who also offers automatic trading, last and last but not least, an easy-to-learn programming language for creating the programs.

Then maybe, we’ll experience less failures.

I will continue to pursue the time-based trading approach. I’ll keep you informed.

And many thanks for testing the results. They match so far, which surprises me a little. Thank you.

Translated with http://www.DeepL.com/Translator

Data mining has nothing to do with the data feed or broker or platform. It is about making results fit the past data – basically curve fitting.

You could look back and say I should have bought a certain index every year except years where the last two numbers are divisible by 8 and then you’d get a nice equity curve – this does not mean that the next year that comes along that is divisible by eight will be one to avoid – it just means that you have dug through the historical data and kept the gems and thrown away the rubbish. Hence ‘data mining’.