The indicators when applied to Indices would be using the bars from all the 24 hours to calculate (including the hours when no global equity markets open), and not just the bars from the trade hours (or the trade hours + pre/post market hours). Is there anyway to fix or adjust this for an indicators AND for automatic trading signals?

As IG keep trading for 24 hours on markets, even if a specific market (+ its pre & post market, and its futures) are not being traded anywhere in globe. Would this be giving incorrect readings & incorrect long/short signals for a lot of indicators for any chart using a timeframe less than the daily?

This would especially be a problem for Asian Markets, for example if we think of the Nikkei (TSE), or the Hang Seng (HKEX) there is 4 to 5 hours of no global equities market open before their respective markets open. The TSE opens at 0900am Tokyo Time, and its pre-market index futures only opens 15 minutes prior to that at 0845am. Meaning from US markets closing to TSE index futures opening in pre-markets there is 3 hours 45 minutes of no global equity markets open. The Hang Seng then opens later on, which does get about 1 hour of Tokyo and Australia markets trading for its calculations, but still those markets is in no way reflective of China’s current markets conditions though? This might only be an issue for IG users as i don’t see my futures or indices charts showing bars outside of open markets on other platforms charts i use.

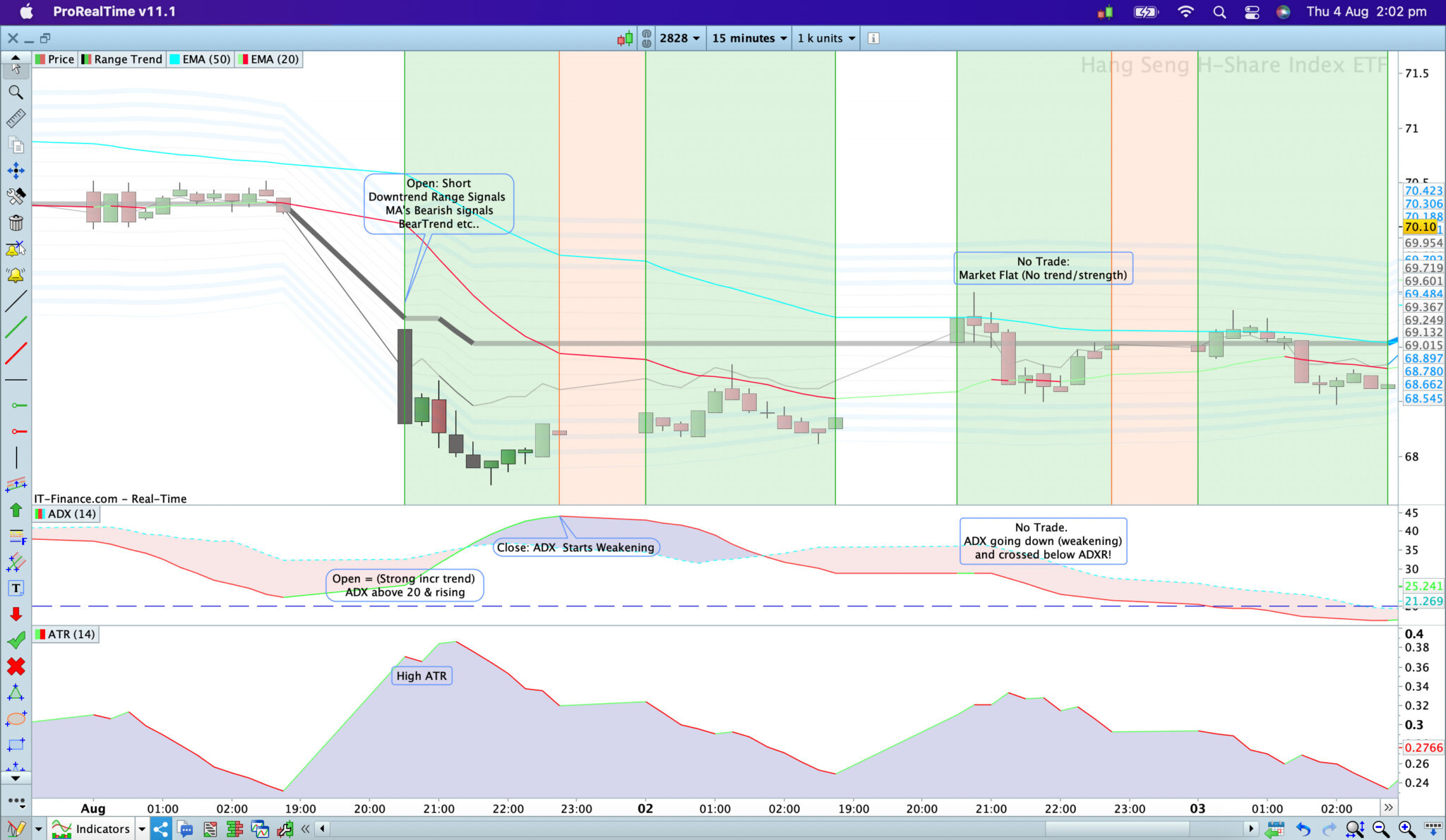

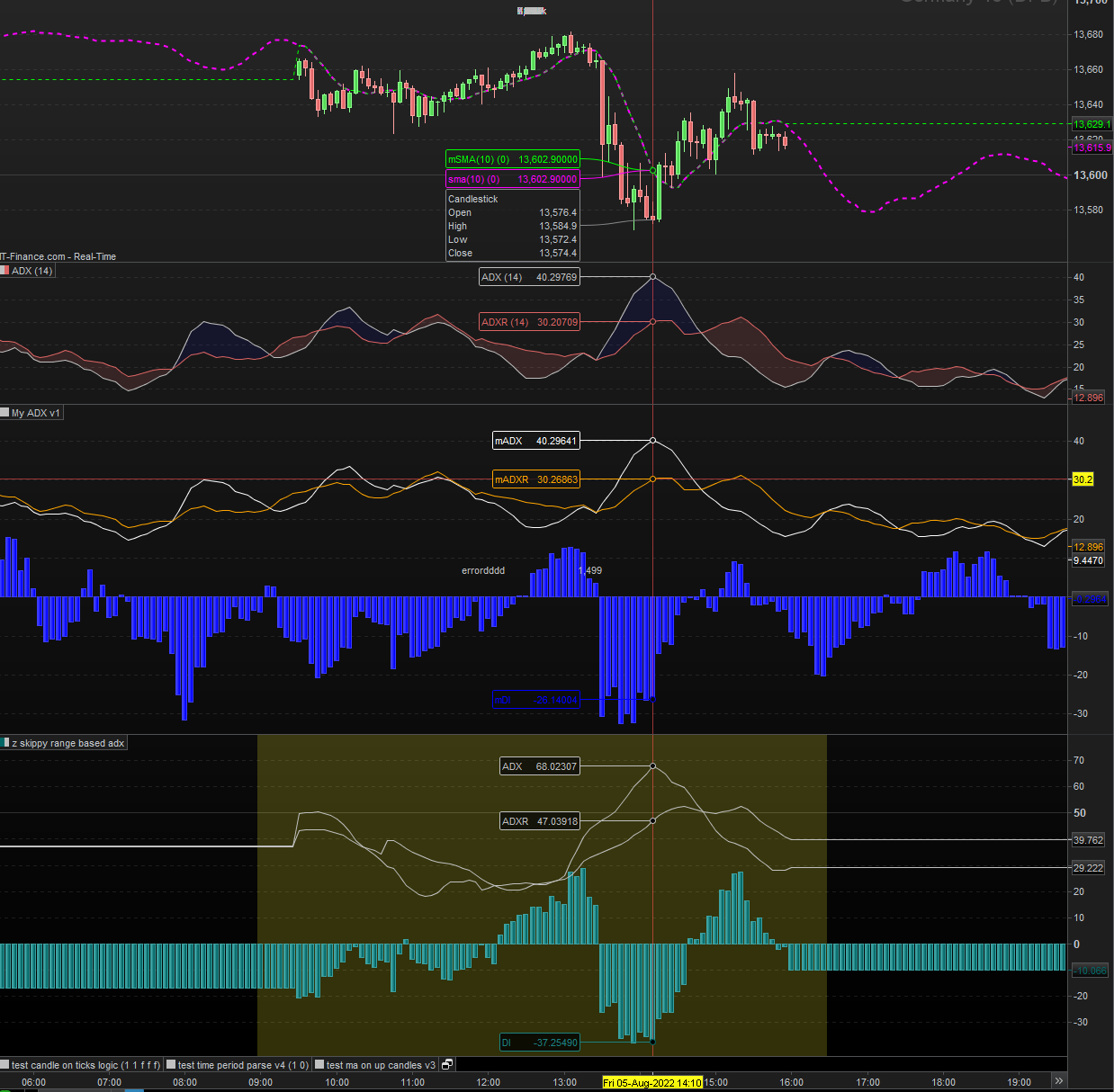

On this reasoning, if (as attached image) Hang Seng for example (14) on 15 minutes, start calculation 4.5 hours prior at New York time = 1600 (At market close) = calculations made up mostly of no global equities markets open. Now any calculations on more bar would be taking in futures movement (out of Hong Kong market hours) which is mostly related to USA and Europe markets conditions and not the Hong Kong markets. If used a (14) on a 1 hour chart, means we starting calculation 14 hours earlier, which also means after the Hong Kong markets closed.

- ADX(14) = calculates strength and movement relative to a period with no strength, and minimal trading occurring. So wouldn’t it make the start of trade almost everyday appear to be up-trending on the chart?

- Volume Calculations for detecting a trend (eg. Change in volumes, Oscillations, On-Balance Volume etc..) would all be suggesting a spike during trade hours, or a movement above average, or a movement upwards during trade hours relative to volumes occurring (none or minimal) during non-trade hours?

- Moving Averages, Ranges etc..: this (as you can see in the picture) would also be moving up and down with the out of market trades. So for example at the moment the USA markets have been performing well (for Longs), so generally all the indices futures follow them up during the USA market; but the HK market been more bearish / downwards moving. As such what happens is these averages and ranges moving upwards over the non-trade times, but then ‘relative’ to USA market times fall, so get Downtrends or Bearish/Short signals occurring at the start of the HK market even if the market doesn’t have any trend or is actually up (relative to itself). As is the case, you can see here, HK actually opened up from it’s yesterday close (in green), and was a relative flat market (relative to itself).

- Average True Range % or Volatility measures etc.. also these would all be suggesting things changes a lot at start of trades too.

Now so i did look at the Hang Seng 50 Indices compared to a random Hang Seng 50 ETF traded only during the HK market times (image 2), and i did indeed see there is a big difference in the signals. The ETF as only taking signals from HK markets which on this chart appears to be giving more correct signals for opening a SHORT based on a trend 2 days ago (on the 2nd of August) at start of trade and closing this about 8 bars later just before lunch as the trend weakens. The time period after this however, unlike the indices, it wouldn’t open any trade, as there was no spike up and then back down to give the start of trade downtrend on the 3rd, and the ADX was weakening (not increasing as was the indices), with other flat market signals unlike the indices. If anything the moving average was uptrend (green) at start of trade for the ETF = correct, vs red for the indices = incorrect. Meaning on the 3rd of August it was a lot more correctly giving the signals, compared to the indices chart.

As such is there any way i can be calculating the indicators for only the bars occurring trade hours of the market and ignoring calculating on the bars outside of market trade? For example [14] at market open means the 14 bars (during markets) before markets closed yesterday, and not the 14 bars (outside of markets) before market opened today. And code this for automatic strategies? So when doing an automatic strategy on the indices i’m getting correct signals (on volumes, trends etc..) related to its market ?