When you ran WF tests, which variables did you optimize? Maybe a stupid question but I’m not familiar which all the ichimoku theory.

Hi,

As mentioned in my post “They all need optimization of the stop level and the slope threshhold. (see comments in code)”

They are up the top of the code in the variable section, It is the following

SlopeThreshold = 2.5 // From back/forward testing optimization

TGL = 30 // also from back/forward testing, note TGL and TGS the same,

Cheers

PS: You will have different values, I was playing with them,

NOTE: These variables I am optimizing are nothing to do with Ichimoku, just the EMA Slope threshhold and the Stop level.

So only slope and trailing distance, I see. And you run this on 10min chart, correct?

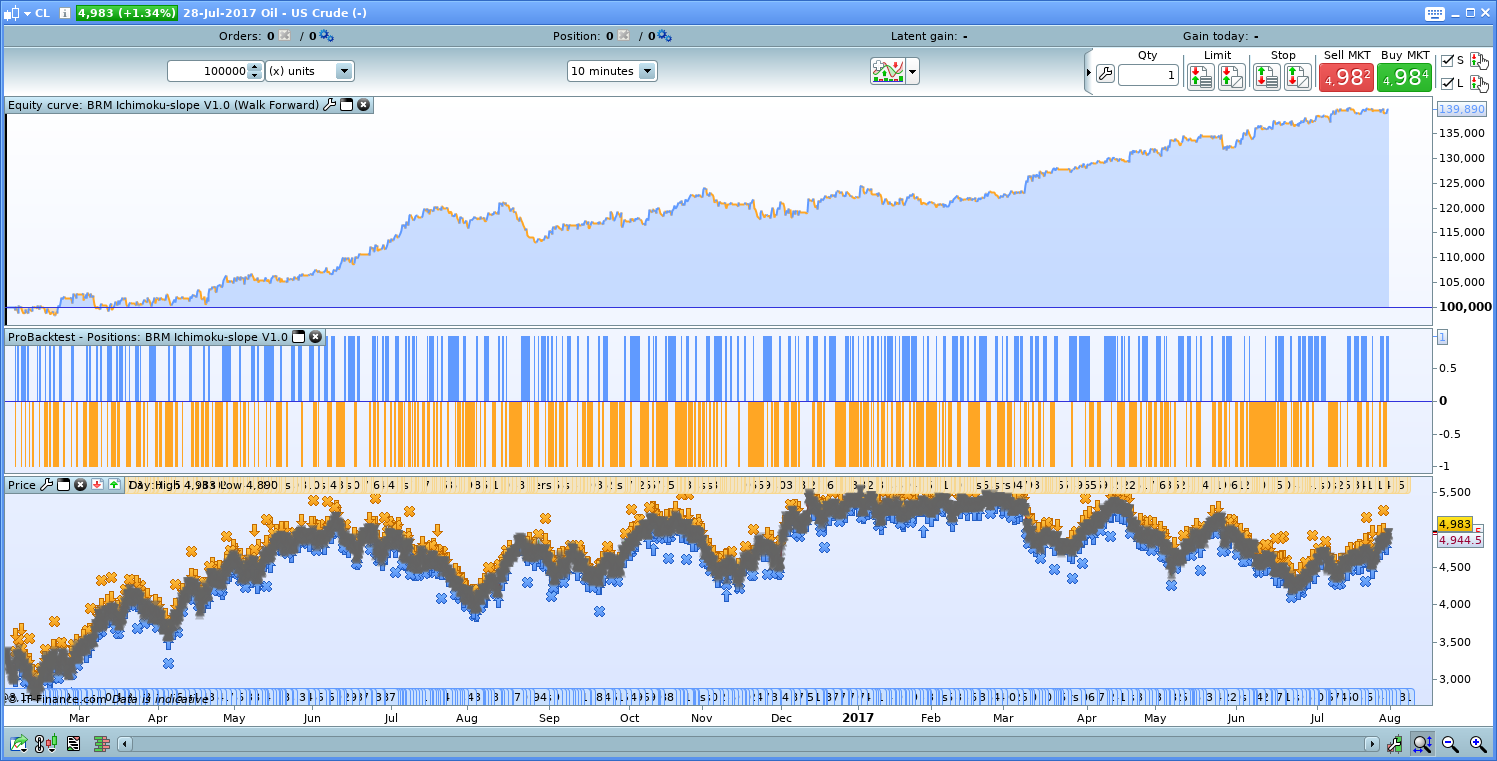

So far I find promising results for CL (oil) with the version you posted. The Yen pairs don’t give so good results but the version you uploaded is maybe optimized for CL and has to be adapted to the pairs?

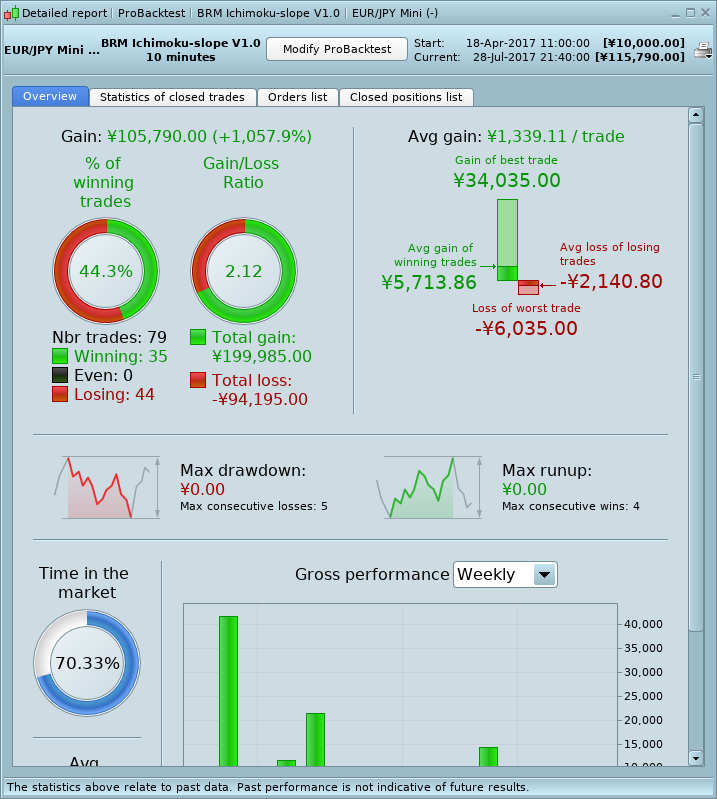

The trading system I posted works well on EUR/YEN mini, 10min 10000 units, make sure it has at least 10,000 yen capital to start as there is a bit of drawdown, I get the following with the code.

I am off to bed, talk tomorrow ..

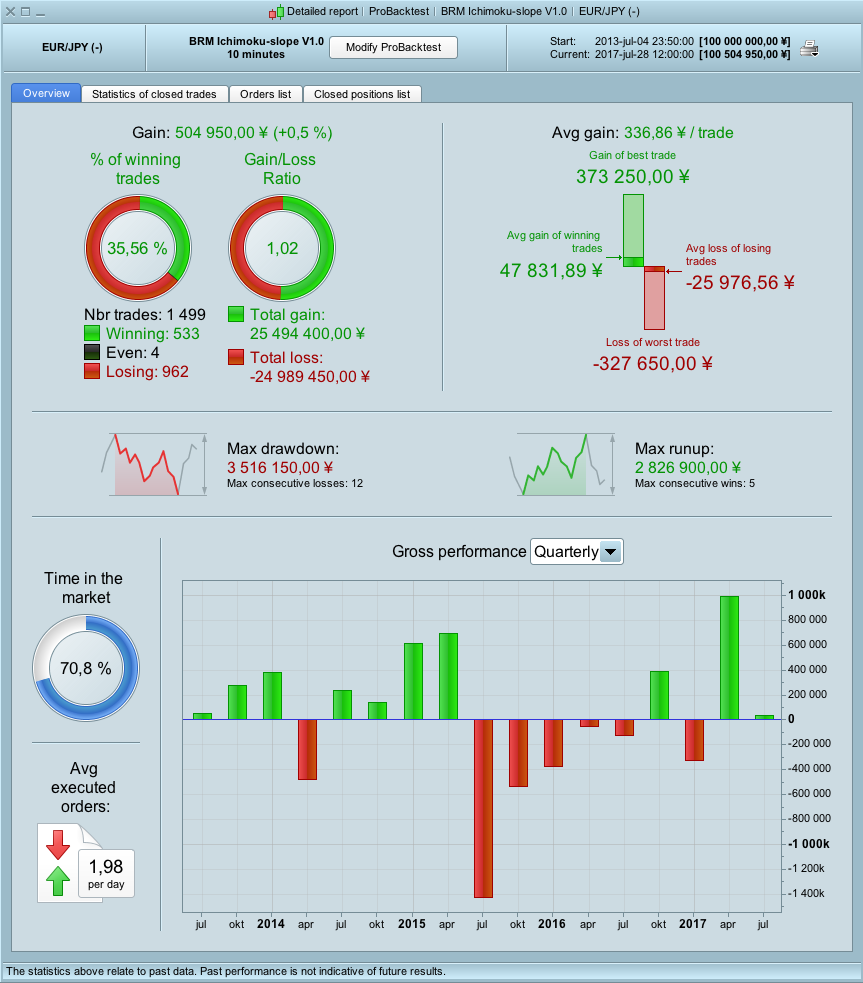

There we have the problem. You tested only on 10000 bars which is in 10min bars not much time. See the backtest with 200K bars for EUR/JPY with 1.5 pips spread.

Anyway for CL the test is fine even with 200K bars. 🙂 I will try to adapt other securities during the weekend. I have not so much time today.

@bmentink thank you for posting your very well structured and commented code.

I think like @despair pointed out it is important to at least make use of the bars you have available when optimizing (i.e. 100k).

I see you kept to the basics of the Ichimoku strategy. Have you ever looked into Ichimoku Number and wave theory?

Those are very important factors to consider when trading the Ichimoku strategy. You can find some nice resources on it here:

https://2ndskiesforex.com/trading-strategies/forex-strategies/ichimoku-price-theory-an-introduction/

https://2ndskiesforex.com/trading-strategies/forex-strategies/ichimoku-wave-theory-an-introduction/

https://2ndskiesforex.com/trading-strategies/forex-strategies/ichimoku-number-theory-an-introduction/

I will have a look at your code in more detail over the weekend.

I have found in my own time developing Ichimoku that ADX volitility checks and RSI divergence checks also really help sieving out the false signals.

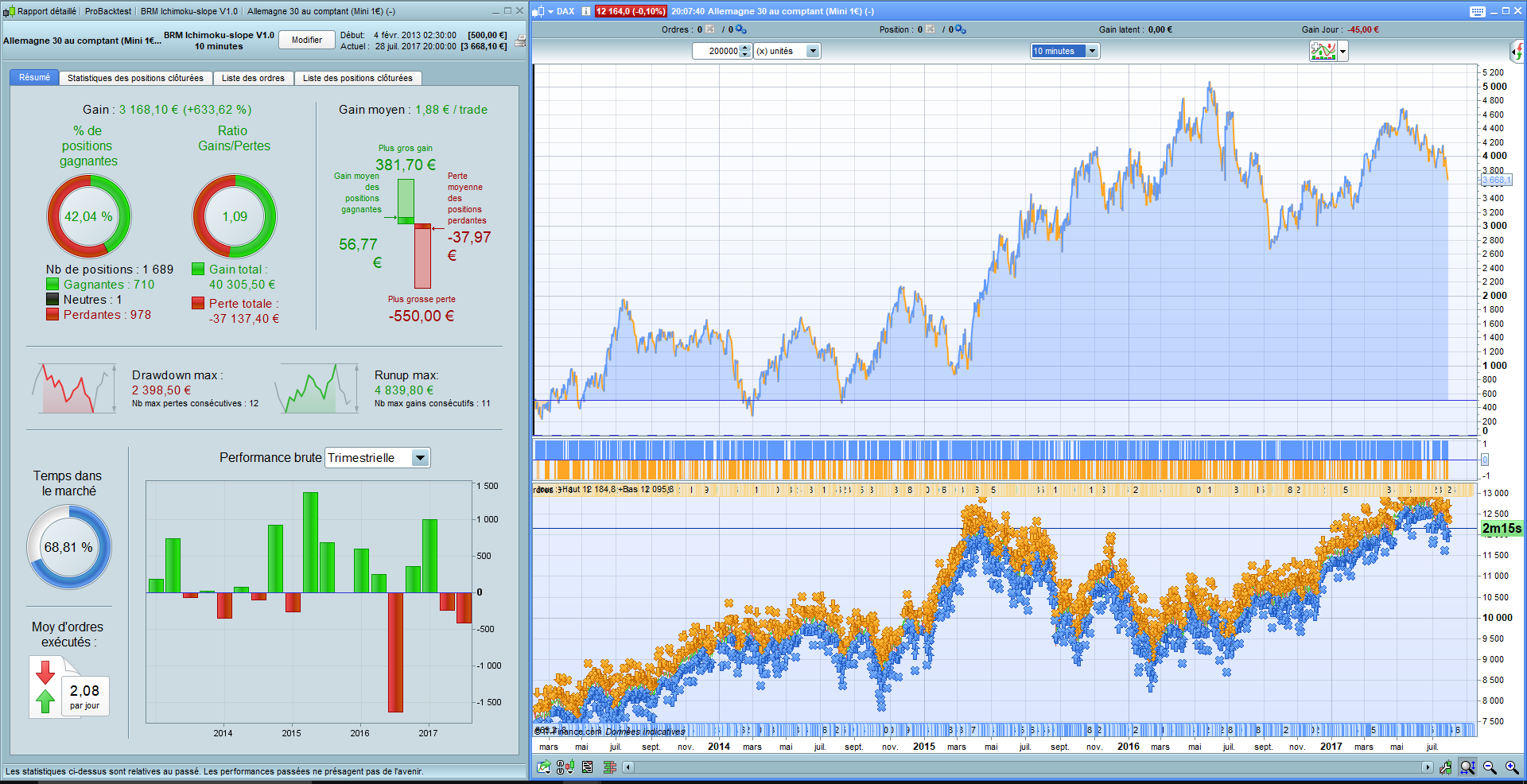

Hi, 3 pts spread for the Oil instrument, 1.5 for the DAX.

@despair I get your point. (I need to get a faster computer, WF takes forever on my machine testing back that far.)

@juanj Thanks for the kind words. Feel free to add any code that will weed out the false signals if you have time.

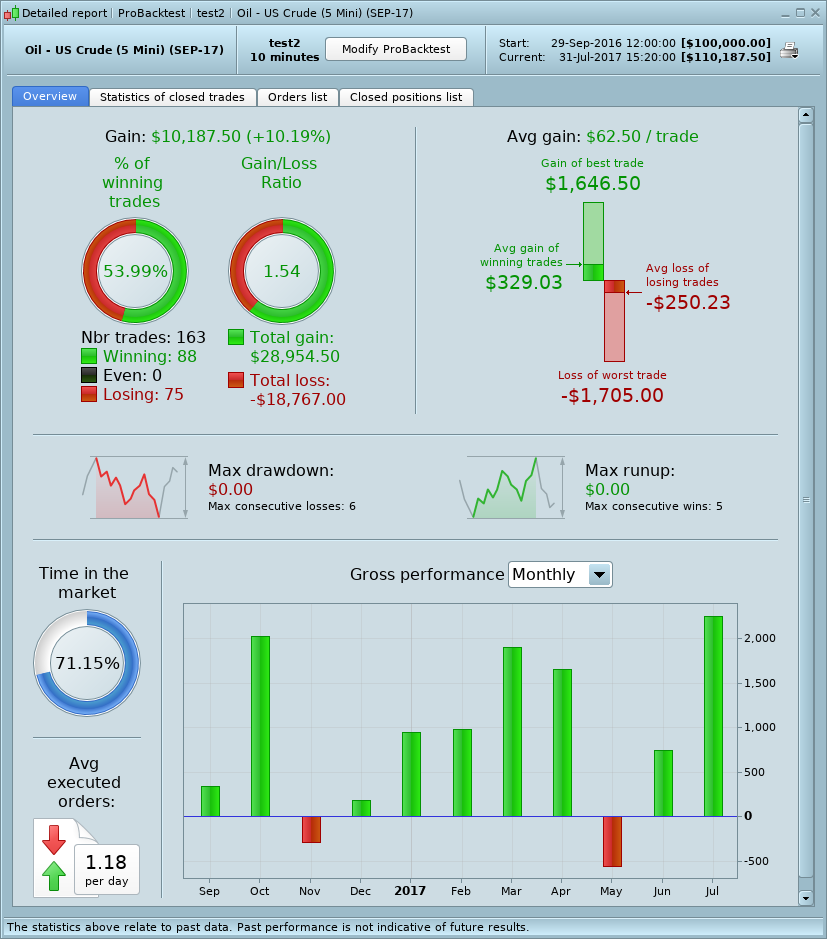

@despair I did an WF optimization on CL and got better results with 4.3 for slope and 36 for stoploss, check it out .. also WF efficiency 70%

Total gain over the period was 1298%

Very nice! As I said, CL looks promising. I will try to improve the code today and see what i can do.

I spend some time with your code today but the result got worse if you are unwilling (like me) to hold positions over the weekend. All my other changes were minor improvements. I will post if I find an interesting result.

@bmentink you can add the following addition to your code to your CL result;

// ------------------------------- Additional Criteria -----------------------------------

R = RSI[15](close) //RSI Period to determine momentum

If R > R[22] Then

If close < close[22] Then

BDIV = 1 //Possible Bearish Divergence Present

SDIV = 0

EndIf

EndIf

If R < R[22] Then

If close > close[22] Then

SDIV = 1 //Possible Bullish Divergence Present

BDIV = 0

EndIf

EndIf

AX = ADX[12] > 11

// ---------------------------------- Market Stuff --------------------------------------

if BOK=-1 and BDIV = 0 and AX then

sellshort NbrContracts contract at market

endif

if BOK=1 and SDIV = 0 and AX then

buy NbrContracts contract at market

endif

Also be aware that according to my knowledge Senkou-Span A and B should be formulated as:

SSpanA = (tenkansen+kijunsen)/2

SSpanB = (highest[52](high)+lowest[52](low))/2

Reason being that they are projected 26 periods ahead. By calculating them as you did (26 periods back) you discount a big part of the system.

SSpanA and SSpanB have 3 components to them if calculated as mentioned above.

- The leading edge (26 periods ahead) – SSpanA > SSpanB = Bullish and SSpanA < SSpanB = Bearish

- The current cloud (26 periods back from leading edge of cloud) – used to determine Kumo break.

- The trailing cloud (5 2 periods back from leading edge of cloud) – used to determine resistance (current close/chikou must be clear of the trailing cloud.

@juanj Many thanks for that. A couple of questions:

- Did you actually try my system with those modifications?

- Regarding the RSI and ADX parameters, did you optimize those to get to those values? If not, where did the numbers come from?

- Regarding SSpanA and B formula, I got those off the Forum, so maybe they are incorrect, I don’t know.

Anyway, I will try those mods out when I get home. Thanks again.

@juanj

I tried your additions to the code, but although the drawdown did decrease, the reduction of %profit was well down on what it was originally. I have attached output of latest. (the original profit was in the order of 39% on CL ..)

It would have been better if you had posted your code version and output of your testing, so we are on the same page.

EDIT: And adding the changes to SSpanA/B that you suggested, dropped %profit down further to 2%

Cheers,