Hi Guys,

This is my first attempt at a trading system based on Ichimoku, including some trend indicators, slope indicators and trailing stops & a bit of magic 😉 etc ..

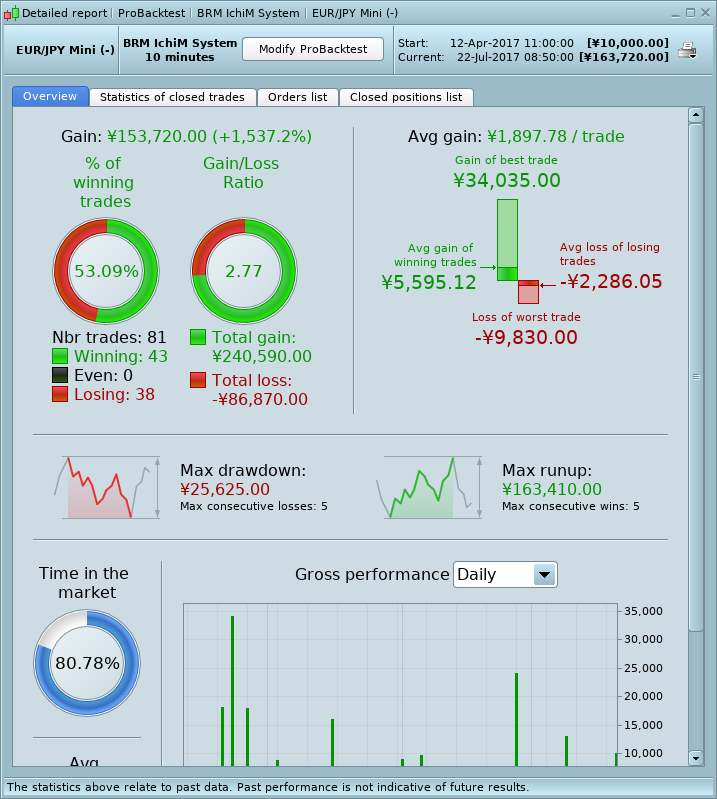

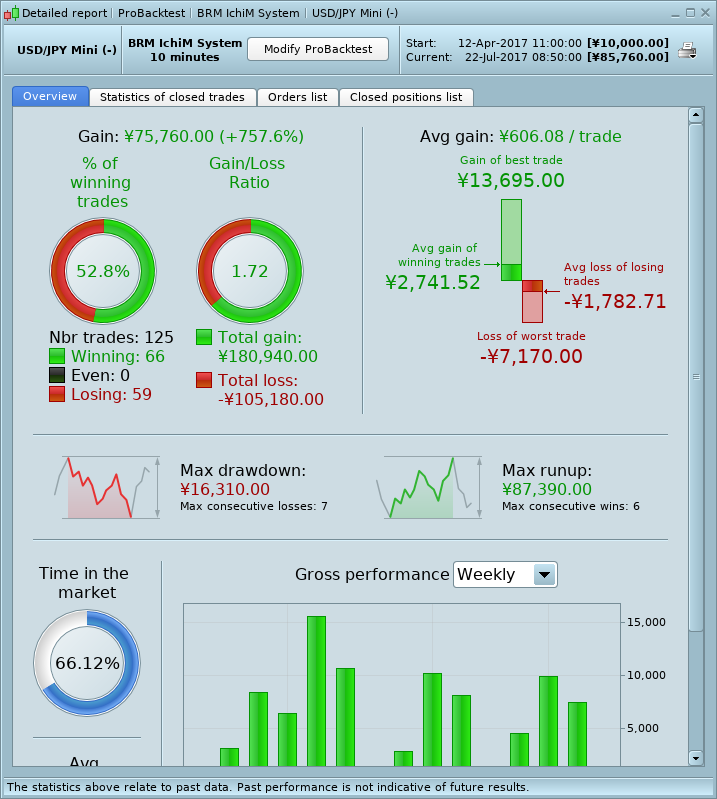

The system is optimized for $ or Pound/Yen and most work well. (The profit over 3 months {10,000 ticks} is from 800%[worse] to 1600%[best] ), see attached pictures and equity graph.

I don’t have a handle on if this is good or bad for my 1st attempt. I know the drawdown is higher than what I would like, but that could be managed with an overall initial stoploss at the expense of some profit.

What do you all think?

I have just started a couple of robots on my demo account to see what will happen, and will report back.

A question: Can someone explain how the forward testing works? I don’t understand the % ratios between back/forward testing and their importance ..

Thanks,

Bernie

Looks good, if you put the code on here then I / others will run it on our platforms and let you know.

Are your results for running in Tick by Tick Mode?

Check this link out re Walk Forward …

https://www.prorealcode.com/blog/learning/prorealtime-walk-analysis-tool/

Hi, will do, but I want to get the code to a reasonable quality before I post it 🙂

Yes, the results are tick-by-tick .. and thanks for the link.

@bmentink I am also looking forward to your code. Have been spending quite some time myself trading and developing ichimoku strategies with very promising results thus far. Will assist in improving it where I can.

Thanks @bmentik, how things are going with your system so far? Let us know how we can help you.

Hi All,

It is going well at the moment, I will post the code in the next few days after I have tidied it up with comments etc. Also, I want to have it running for at least a few days on my demo account so I can post those results too. (It is one thing to do back/forward testing/optimizing, but running live is the real test ..)

Currently it has been running for a couple of days and it has added 55,000 yen to my account (well, the equivelent of account $ anyway, only using 5 mini position), so looking promising … but early days.

@nicolas I do have a question regarding forward testing you could help with. Just wondering when the optimization runs on each segment, why does it end up using different optimizations for each segment. I would have thought it would make more sense to optimize the 1st segment, then carry those numbers through to testing the remaining segments with the same optimization values. After all, we can’t change optimization on the fly … well, unless we actively do that every few months, does anyone do that? With the current system, you can only realy choose the segment that has the best efficient close to 50% and use those numbers …

I think my system is good at getting into the right trade, but probably could be better at exit. I will leave you guys to comment on that when I post the code.

Cheers,

Bernie

Hmm sorry, I’m tired repeating the same thing again and again 🙂 You can refer to the FAQ I made in the blog section of the website.

Oooh OK, let’s explain it again!

Using the same optimisation values over the whole OOS periods has no sense at all. The WFA only help you studying what would have happened in real life with your optimized values with the help of splitting the history into 2 different section: the In Sample period (where/when you optimize the values) and the Out Of Sample period (where/when they are tested). Because the tool has the ability to repeat this test X times over the whole history, just use it, but it is up to you to make 1,2,3,10 or even 20 times the optimisation to know precisely when your strategy benefit for being re-optimized (after 1 week, 2 months, a quarter, etc.) = default is 5 times (but it doesn’t mean it is written in the marble that 5 times is enough).

I hope it is even more clear now for you 🙂

Ok, I’ll concider my self told off!!

In my defence I have only been on the site a total of a couple of days compared to you all, I hav’nt had a chance to read ALL the blog, yet many of the posts in the forum …. Nicolas, in case you did not realize, I am very new here …. so please don’t yell at me .. some of us havn’t been here long enough to make 5300 replies 😉

.. just to add. The blog was not clear, that is why I asked, I thought that was what the forums were for.

I understand the single back/forward test, but if you have multiple segments all giving ok efficiency figures, all with different optimizations, how do you select which one to use? Maybe I am just thick or something ..

Sorry for being rude. Too much work and not enough rest. I’m sorry my blog article is not clear 🙁

but if you have multiple segments all giving ok efficiency figures, all with different optimizations, how do you select which one to use?

None of them. They are only there to figured out how the strategy would have operate in the past with these values. So if you decide to launch the strategy for real (because the WFA seems good for you), you already know on how much time you need to optimize the strategy (same as a single In Sample period). This way you should expect the strategy to be as good as an OOS period of your WFA.

Hi bmentink

You say … Maybe I am just thick or something … quite the opposite as I have exactly same thoughts as you (and I know I’m not thick! 🙂 ) in your post #41755 and #41762 .

You say … unless we actively optimise every few months, does anyone do that? … yes that can be a useful option if WF optimised values are significantly different for successive In Sample periods, but still with WF % > 50 for Out of Sample periods.

I still haven’t come to a definite ‘formula’ for use of Walk Forward, I don’t think there is / ever will be? I often end up going forward with the modal value (most recurrent, but you knew that! 🙂 ) for optimised variables.

Your questions would be useful to prompt discussion on the ‘Walk Forward Thread’ (Mmm can’t find it, sorry, maybe later … it could do with being a ‘sticky’?).

Anyway, just sharing a few thoughts and I didn’t want you to feel alone in your thoughts re WF

GraHal

PS (This is Nicolas website and he ends up answering well over 80% (?) of questions and doing loads and loads of behind the scenes work also, I don’t know how he keeps going?)

I didn’t realise for my first week or two on this site as it’s not so obvious? Maybe the Nicolas Avatar should be above the ‘Welcome To ProRealCode’ on the Home / landing page? Just an idea I’ve had for ages and here seems a good place to say it?

Hope I didn’t offense @bmentink, I should have used more smileys 🙂 😉 😀 🙂

@nicolas No problem, no offence and your Blog is excellent, it is mostly me coming to grips with a new concept (WF is new to me in trading), I understand more now. But I need to put more time aside to read it all. I very much appreciate the time you give to help others like me.

@grahal Thanks for the feedback, your thought on how to use the WF results are pretty much what I was thinking.

I am just going to finish up some more WF testing on some of the parameters I am using, then I will post the code up to this point for you guys to play with. Probably tonight when I get home from work.

Cheers,

Hi Guys,

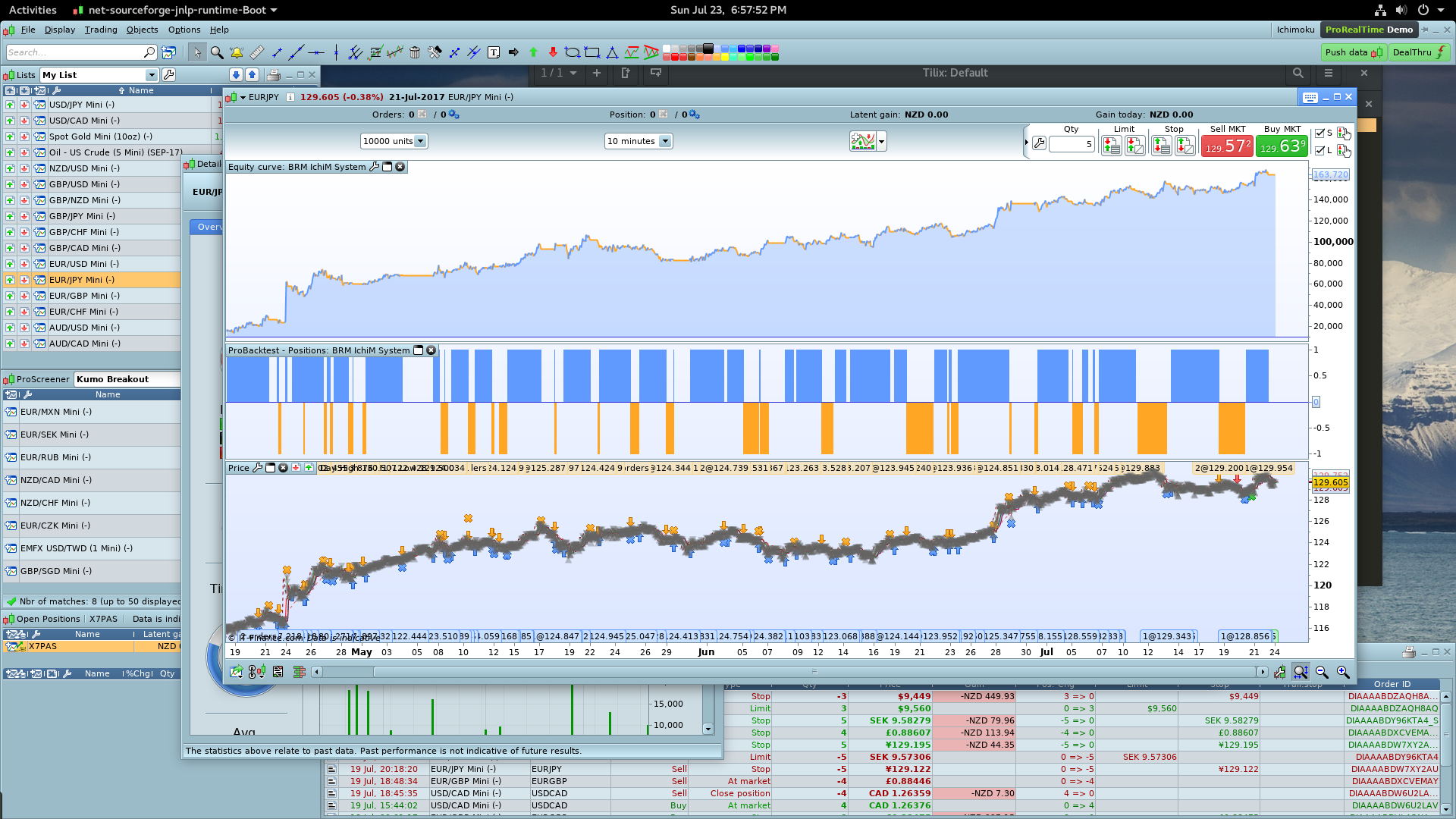

Well as promised, attached is my Ichimoku-slope trading system, hope it is worthy of this forum.

This system is based on the Ichimoku Kumo breakout, with the additional enhancements.

- The Chikou San is used as well to determine the underlying trend and to make sure we are trading with the trend. More profitable with it.

- The Linear Regression Slope of a 2 period DEMA is used to only enter the trade if we have enough volatility. It made a huge jump up in profitability.

- Trailing stops are used.

The trading system is best used on yen currency pairs, the best being EUR/YEN and GBP/YEN, the USD/YEN is not good in the WF test. US Crude Oil also works, I havn’t tried others. They all need optimization of the stop level and the slope threshhold. (see comments in code)

I have been running two optimized bot’s, one on the EUR/YEN and also on the GBP/YEN for the last few days with good results. (gain of over 100,000 yen)

Deficiencies:

- It needs a better trailing stop, as too much money is given back. I suggest a Fractal based trailing stop would be better.

- There needs to be a better initial stop to protect from market reversal immediately after getting in the market and before the trailing stop starts.

Any help with addressing the above would be good. Let me know what you all think.

Enjoy!

I will have a closer look at this one under the weekend and try to improve the issues you mentioned. Thanks for sharing.