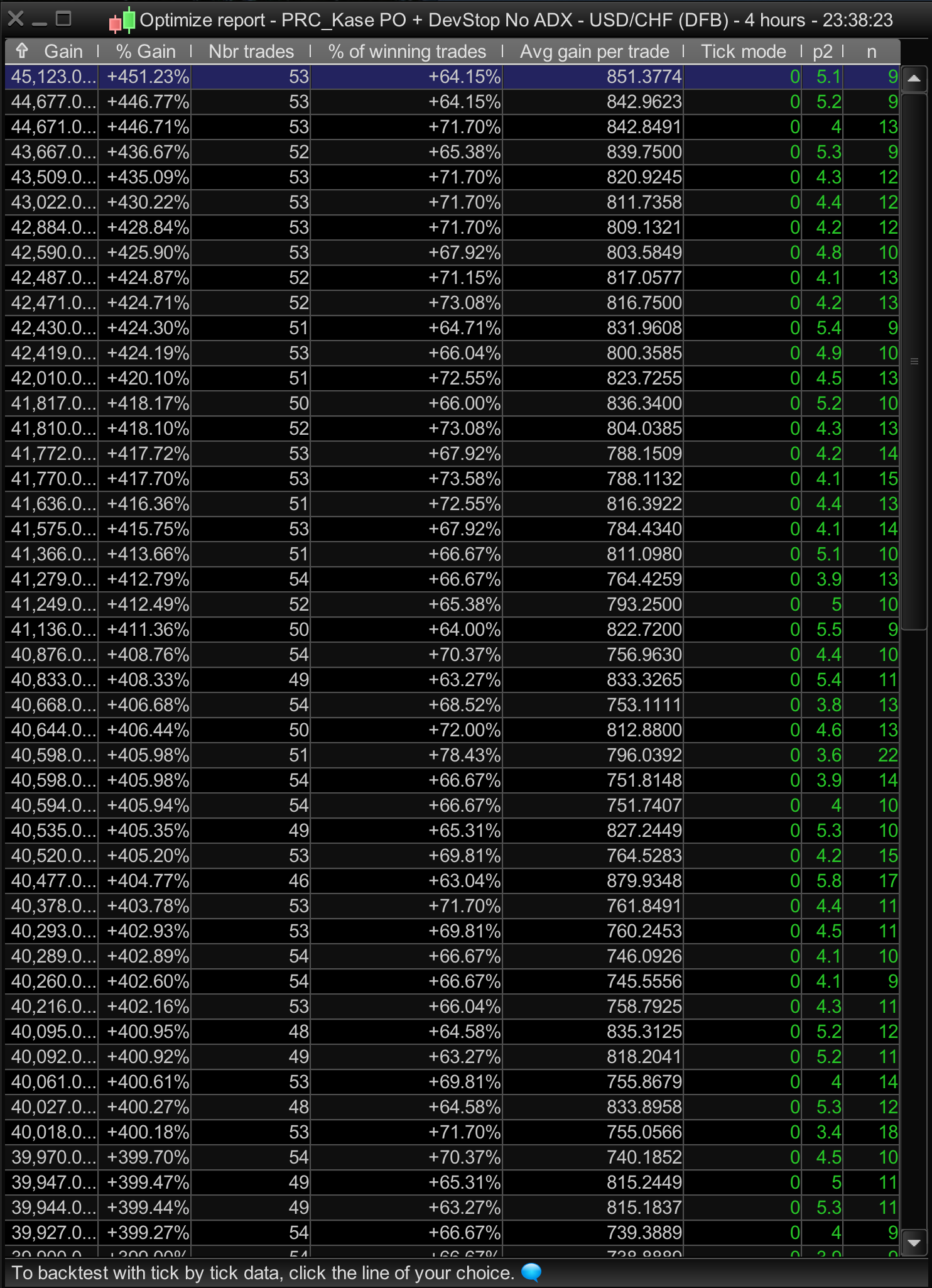

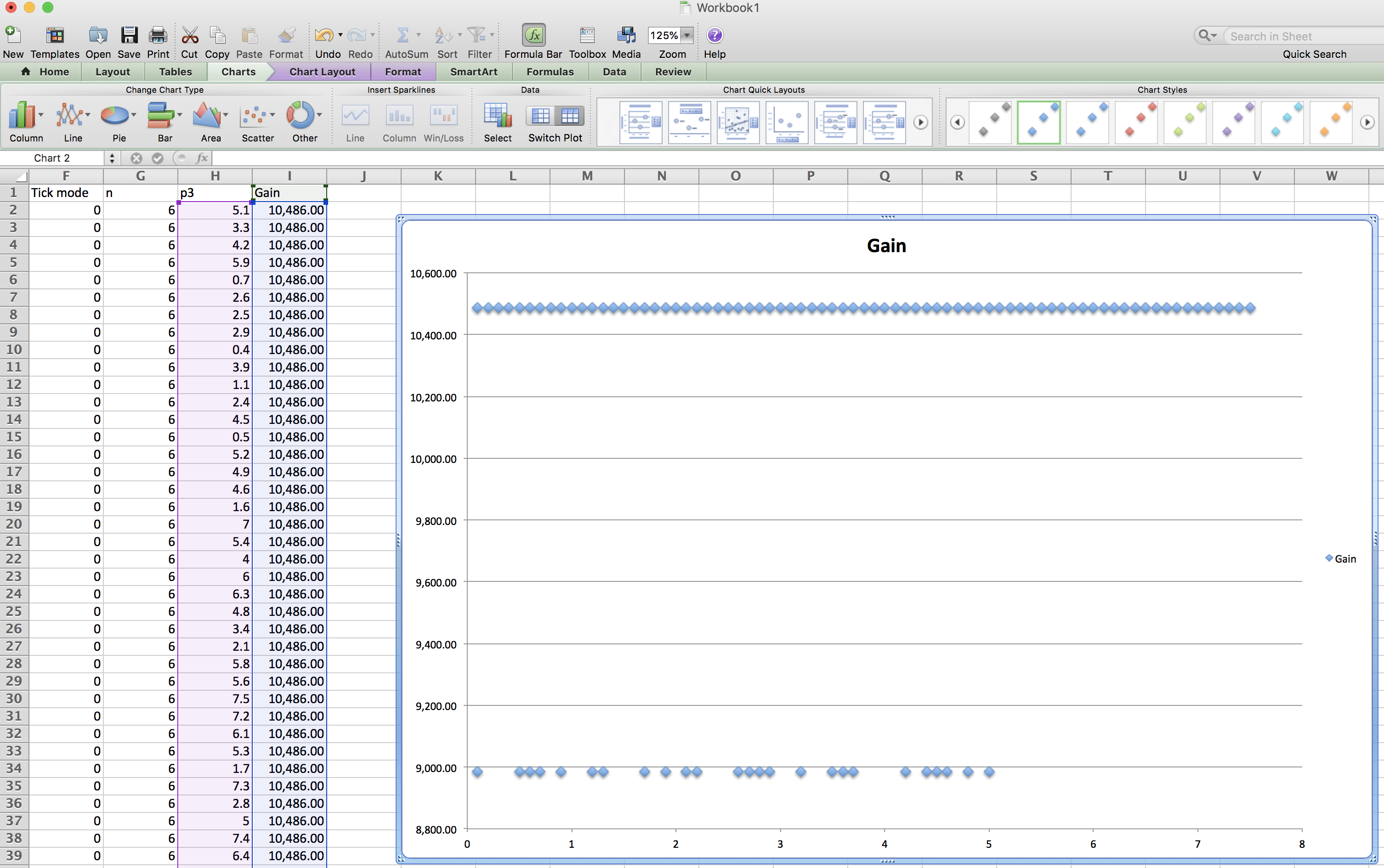

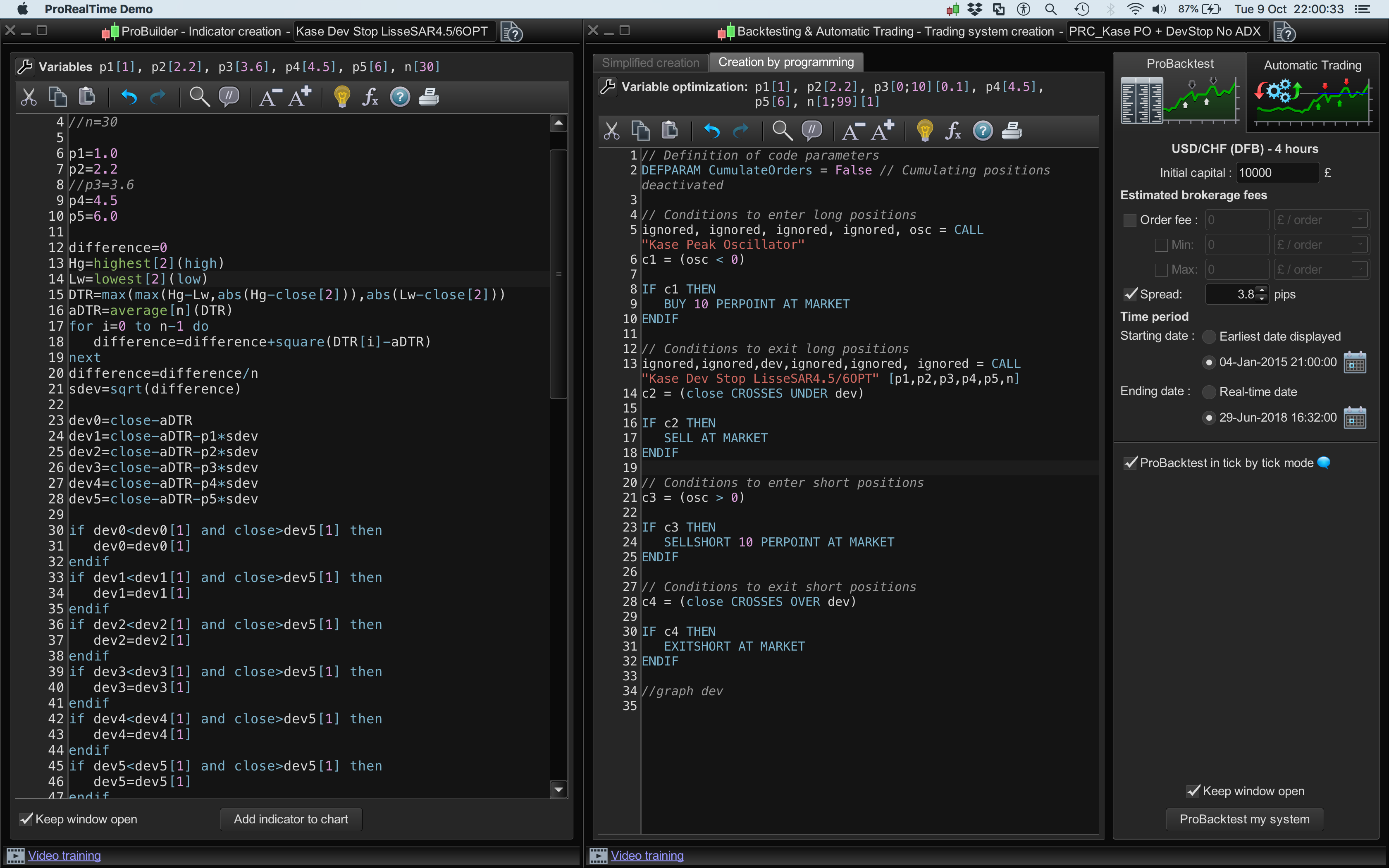

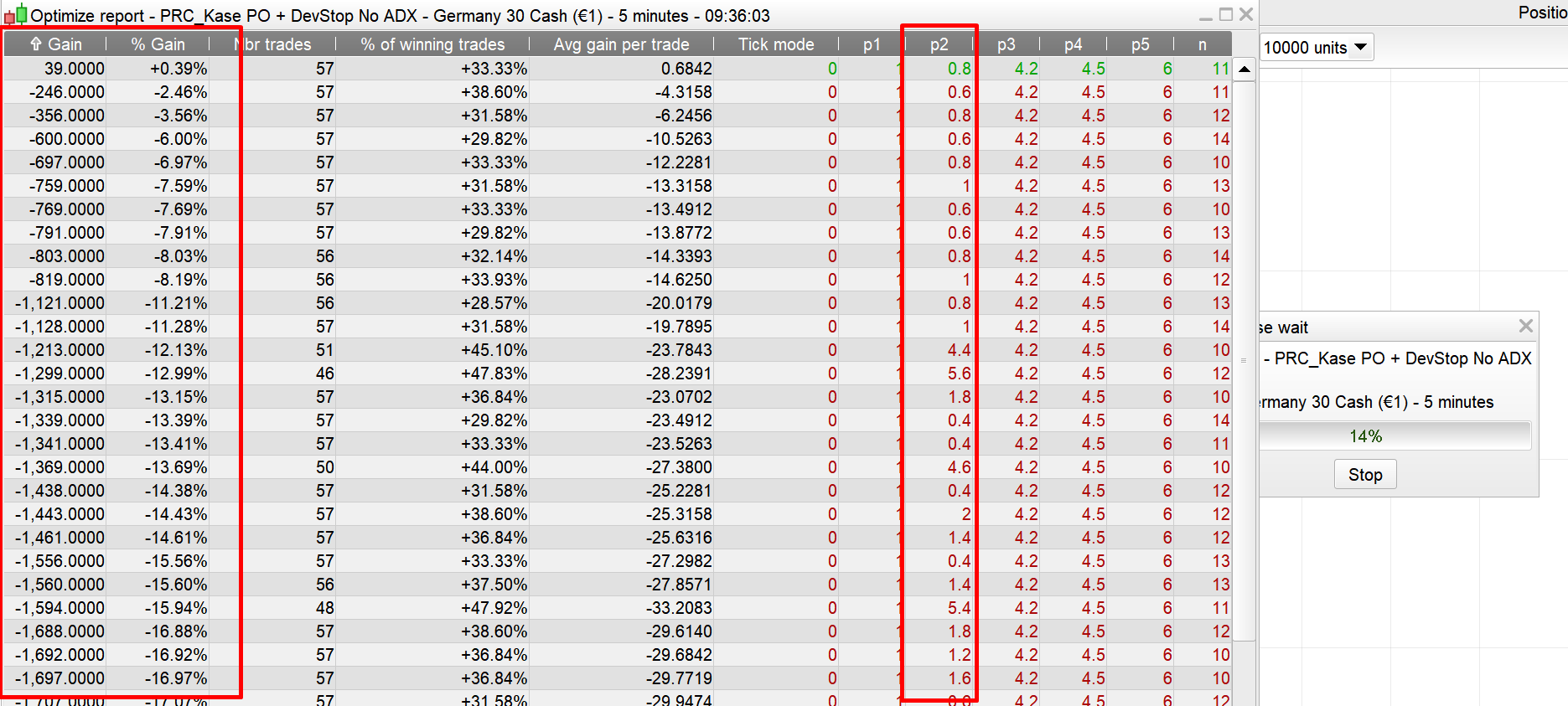

Hi @nicolas, I’ve REM’d out all the p1 to p6 values in the indicator and the strategy code (where I’d also added the indicator code). It’s optimising but without profits when profits were achieved manually adjusting the Dev Stops values using std deviations of 1 to 6…

(I’ve put all the p values in bold)

To clarify, is the Kase Dev Stop code being called from the code where I’d added the indicator into the strategy, or from the actual PRT indicator code when I first added the indicator originally?

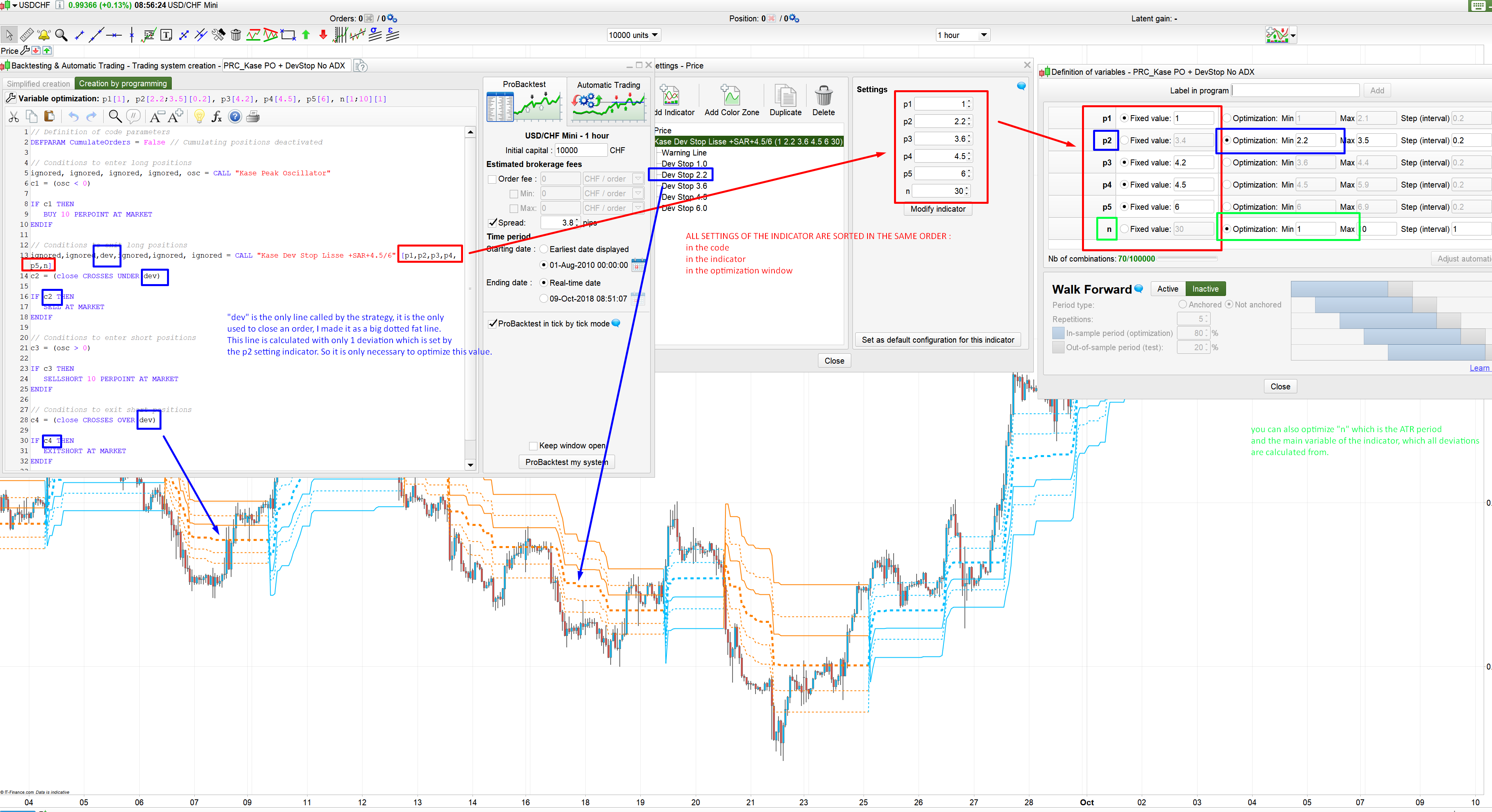

I see that the Kase Dev Stop indicator name in the strategy actually includes the p values in square brackets – I’m assuming this maybe where the issue is, but am unsure how to add strategy variable optimsation values (via the spanner) without the strategies indicator name being modified and including those p values?

Thanks again,

// Conditions to exit long positions

ignored,ignored,indicator3,ignored,ignored, ignored = CALL "Kase Dev Stop Lisse +SAR+4.5/6" [WarningLine, p1,p2,p3,p4,p5]

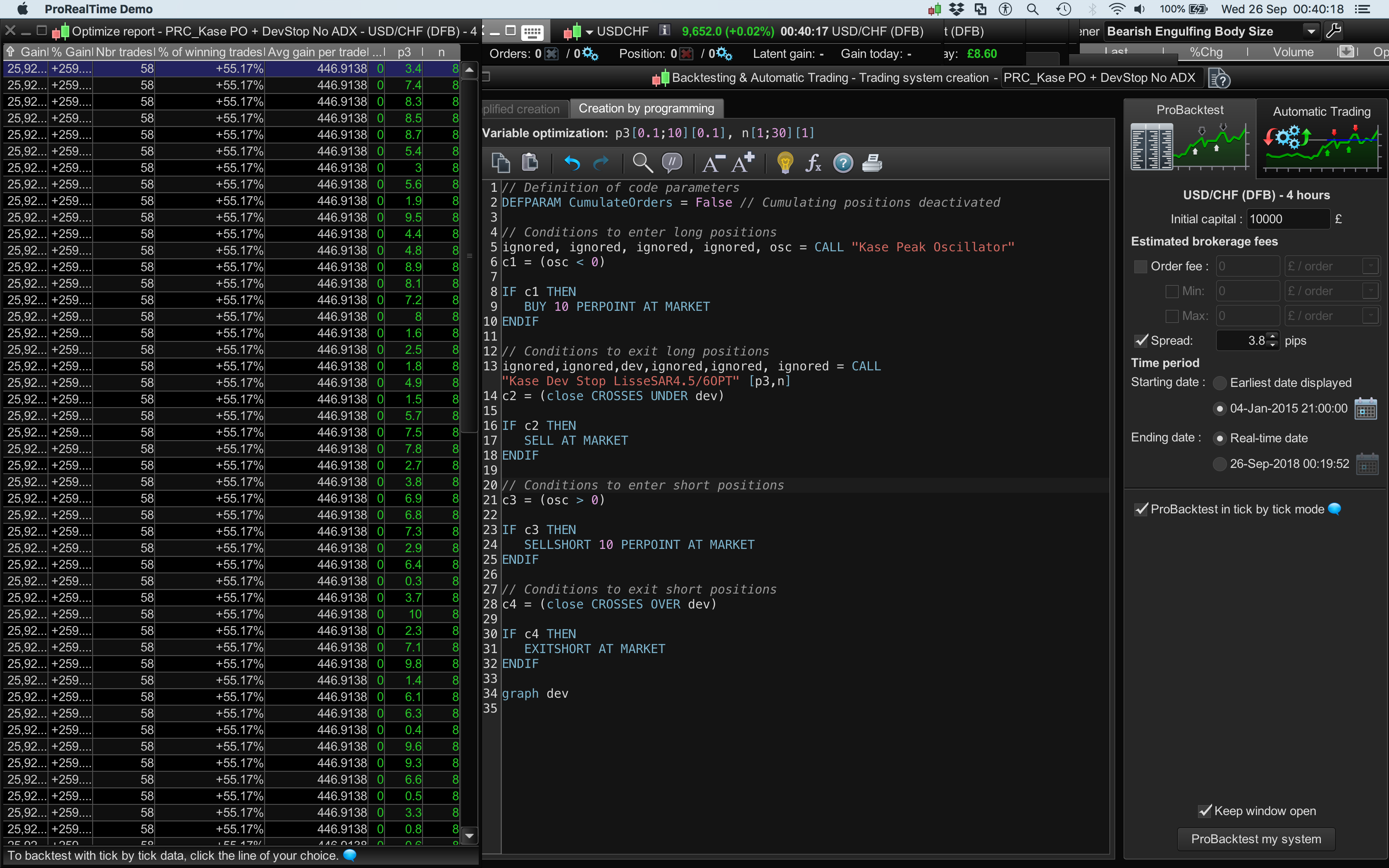

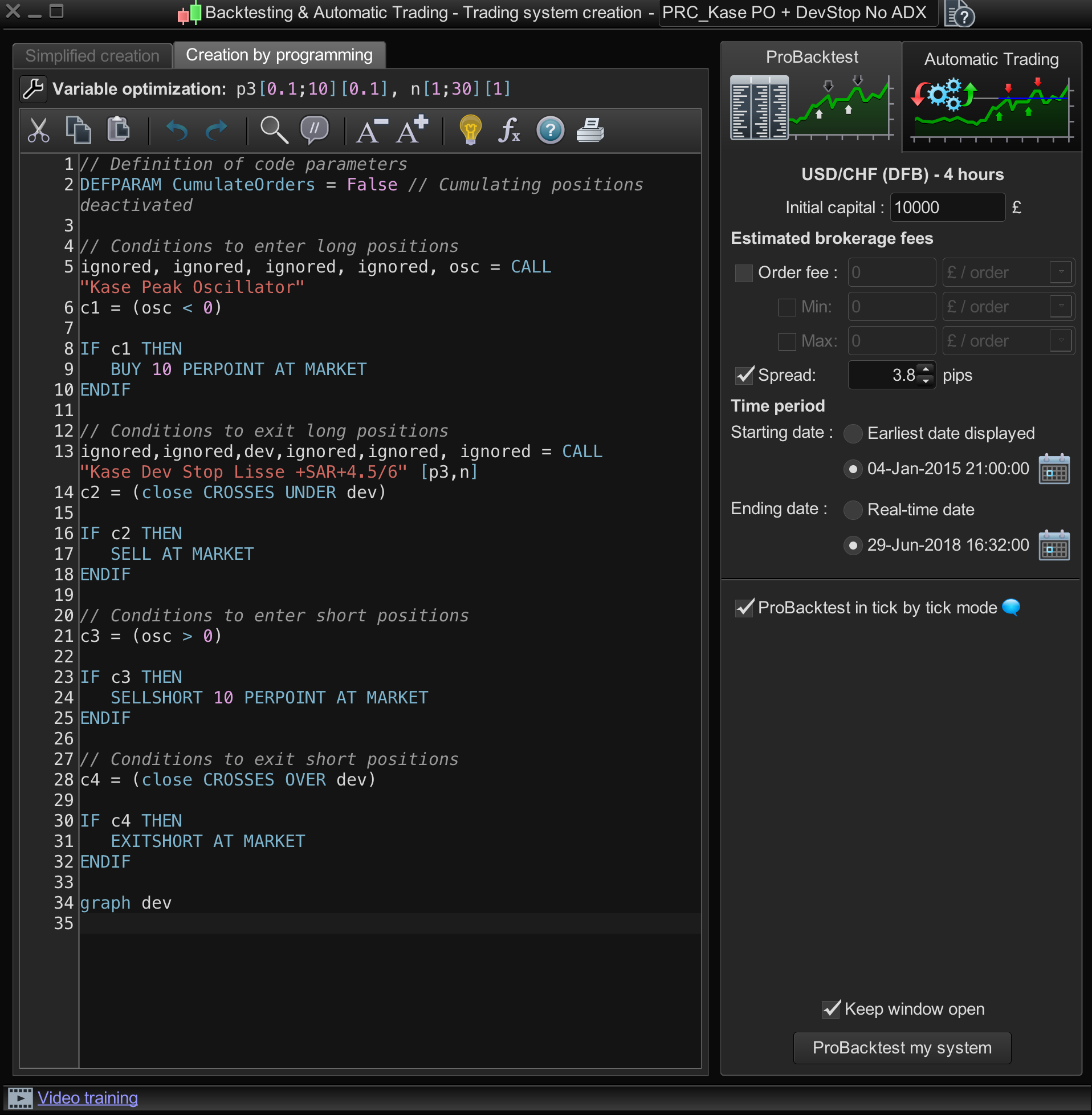

Strategy Code:

// Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

// Conditions to enter long positions

ignored, ignored, ignored, ignored, indicator2 = CALL "Kase Peak Oscillator"

c1 = (indicator2 < 0)

IF c1 THEN

BUY 10 PERPOINT AT MARKET

ENDIF

// Conditions to exit long positions

ignored,ignored,indicator3,ignored,ignored, ignored = CALL "Kase Dev Stop Lisse +SAR+4.5/6" [WarningLine, p1,p2,p3,p4,p5]

c2 = (close CROSSES UNDER indicator3)

IF c2 THEN

SELL AT MARKET

ENDIF

// Conditions to enter short positions

ignored, ignored, ignored, ignored, indicator5 = CALL "Kase Peak Oscillator"

c3 = (indicator5 > 0)

IF c3 THEN

SELLSHORT 10 PERPOINT AT MARKET

ENDIF

// Conditions to exit short positions

ignored,ignored,indicator6,ignored, ignored, ignored = CALL "Kase Dev Stop Lisse +SAR+4.5/6" [WarningLine, p1,p2,p3,p4,p5]

c4 = (close CROSSES OVER indicator6)

IF c4 THEN

EXITSHORT AT MARKET

ENDIF

// Stops and targets

//SET STOP pTrailing 500 //OPTIMISED = 430

//250 and anything over 300 to 500 tics)

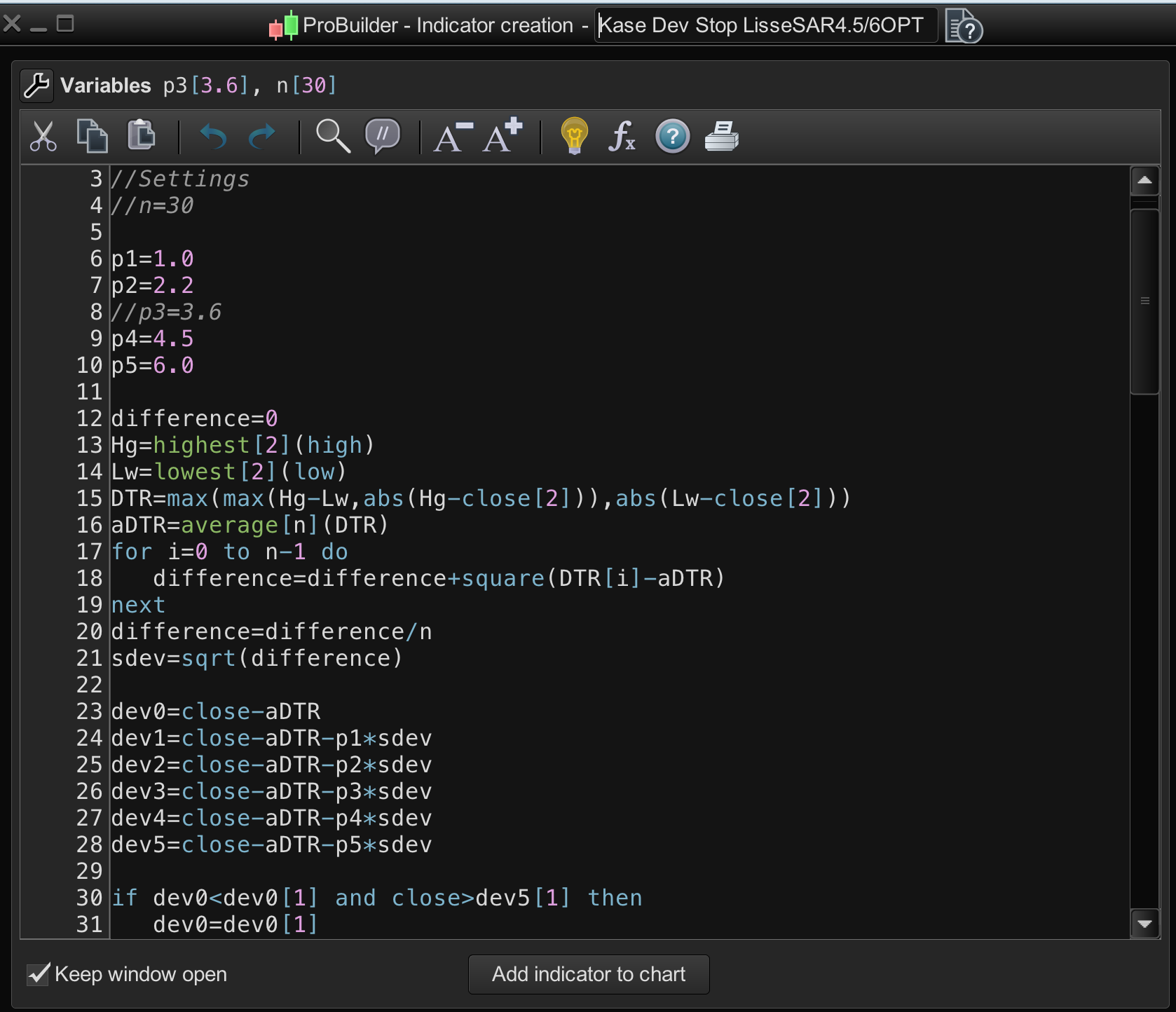

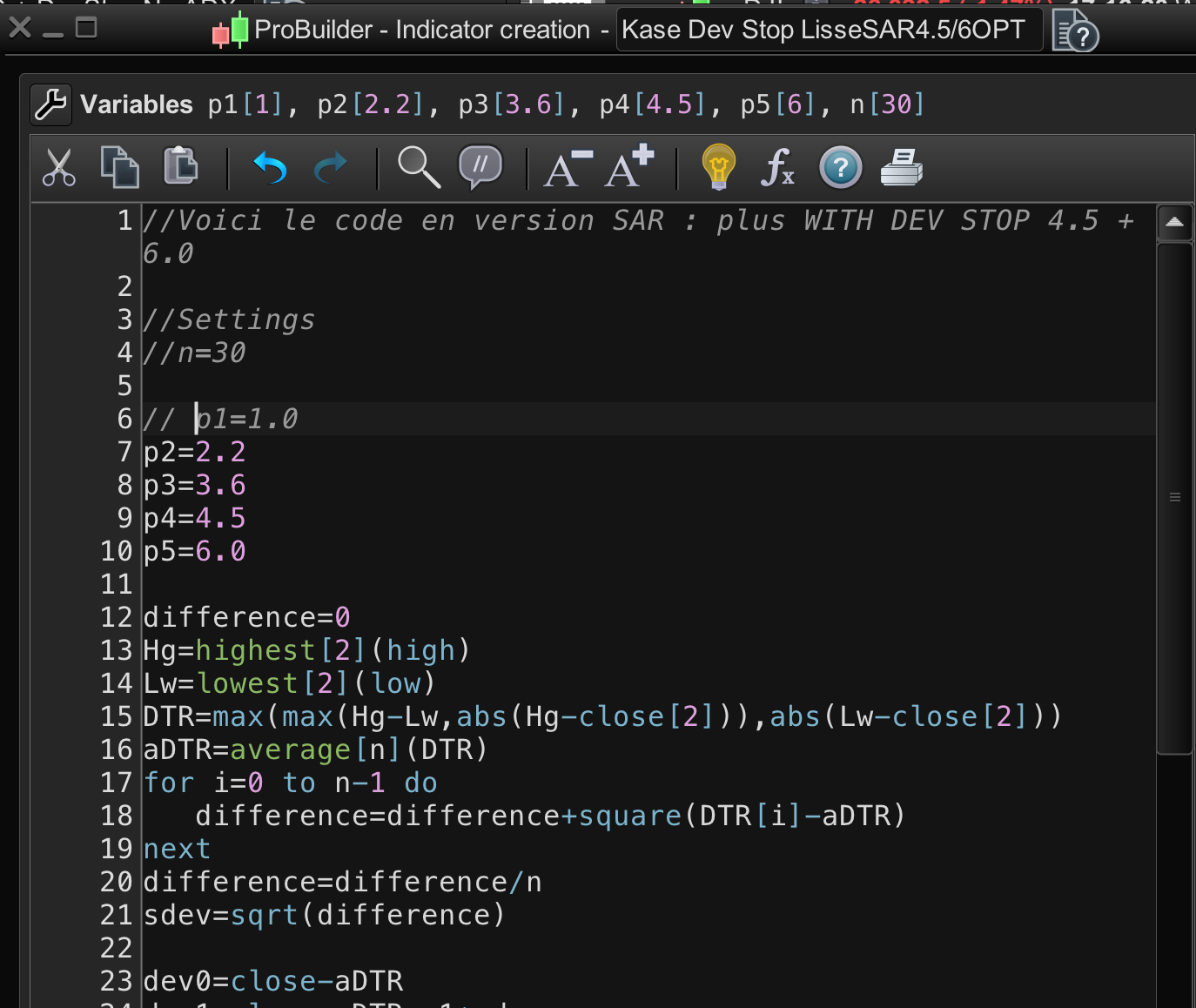

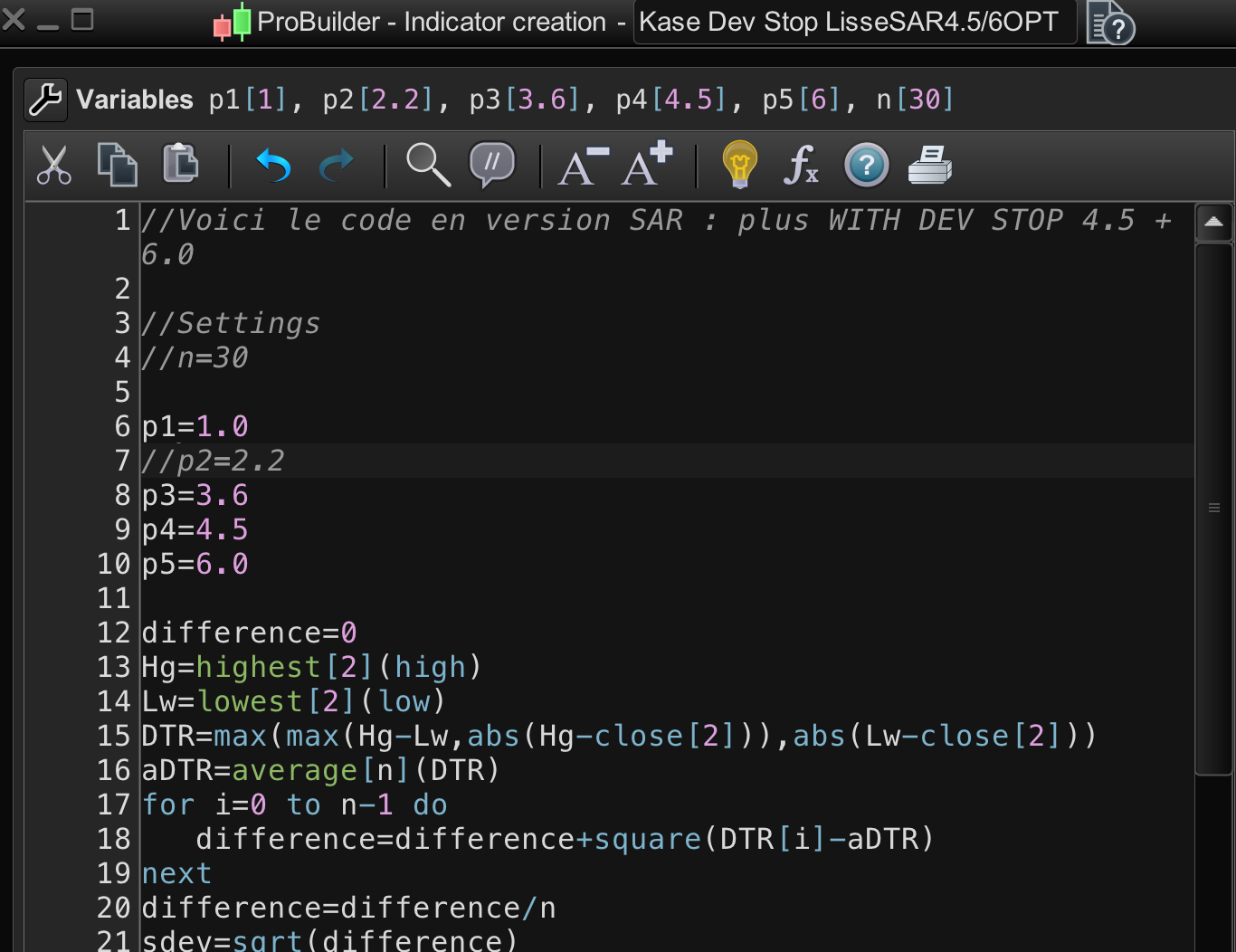

//Settings

n=30

//p1=1.0

//p2=2.2

//p3=3.6

//p4=4.5

//p5=6.0

difference=0

Hg=highest[2](high)

Lw=lowest[2](low)

DTR=max(max(Hg-Lw,abs(Hg-close[2])),abs(Lw-close[2]))

aDTR=average[n](DTR)

for i=0 to n-1 do

difference=difference+square(DTR[i]-aDTR)

next

difference=difference/n

//sdev=sqrt(difference)

dev0=close-aDTR

//dev1=close-aDTR-p1*sdev

//dev2=close-aDTR-p2*sdev

//dev3=close-aDTR-p3*sdev

//dev4=close-aDTR-p4*sdev

//dev5=close-aDTR-p5*sdev

if dev0<dev0[1] and close>dev5[1] then

dev0=dev0[1]

endif

if dev1<dev1[1] and close>dev5[1] then

dev1=dev1[1]

endif

if dev2<dev2[1] and close>dev5[1] then

dev2=dev2[1]

endif

if dev3<dev3[1] and close>dev5[1] then

dev3=dev3[1]

endif

if dev4<dev4[1] and close>dev5[1] then

dev4=dev4[1]

endif

if dev5<dev5[1] and close>dev5[1] then

dev5=dev5[1]

endif

dev6=close+aDTR

//dev7=close+aDTR+p1*sdev

//dev8=close+aDTR+p2*sdev

//dev9=close+aDTR+p3*sdev

//dev10=close+aDTR+p4*sdev

//dev11=close+aDTR+p5*sdev

if dev6>dev6[1] and close<dev11[1] then

dev6=dev6[1]

endif

if dev7>dev7[1] and close<dev11[1] then

dev7=dev7[1]

endif

if dev8>dev8[1] and close<dev11[1] then

dev8=dev8[1]

endif

if dev9>dev9[1] and close<dev11[1] then

dev9=dev9[1]

endif

if dev10>dev10[1] and close<dev11[1] then

dev10=dev10[1]

endif

if dev11>dev11[1] and close<dev11[1] then

dev11=dev11[1]

endif

if close>dev11[1] then

//flag=-1

else

if close<dev5[1] then

//flag=1

endif

endif

//if flag=-1 then

//ind0=dev0

//ind1=dev1

//ind2=dev2

//ind3=dev3

//ind4=dev4

//ind5=dev5

//k=1

//r=0

//g=191

//b=255

//else

//ind0=dev6

//ind1=dev7

//ind2=dev8

//ind3=dev9

//ind4=dev10

//ind5=dev11

//k=-1

//r=255

//g=128

//b=0

//endif

//ORIG return ind0 COLOURED BY k,ind1 coloured by k,ind2 coloured by k,ind3 coloured by k//

//ORANGE AND LIGHT BLUE

//return ind0 coloured(r,g,b) style(dottedline,2) as "Warning Line", ind1 coloured(r,g,b) style(dottedline,2) as "Dev Stop 1.0", ind2 coloured(r,g,b) style(dottedline,2) as "Dev Stop 2.2", ind3 coloured(r,g,b) style(line,2) as "Dev Stop 3.6", ind4 coloured(r,g,b) style(dottedline,2) as "Dev Stop 4.5", ind5 coloured(r,g,b) style(line,2) as "Dev Stop 6.0"

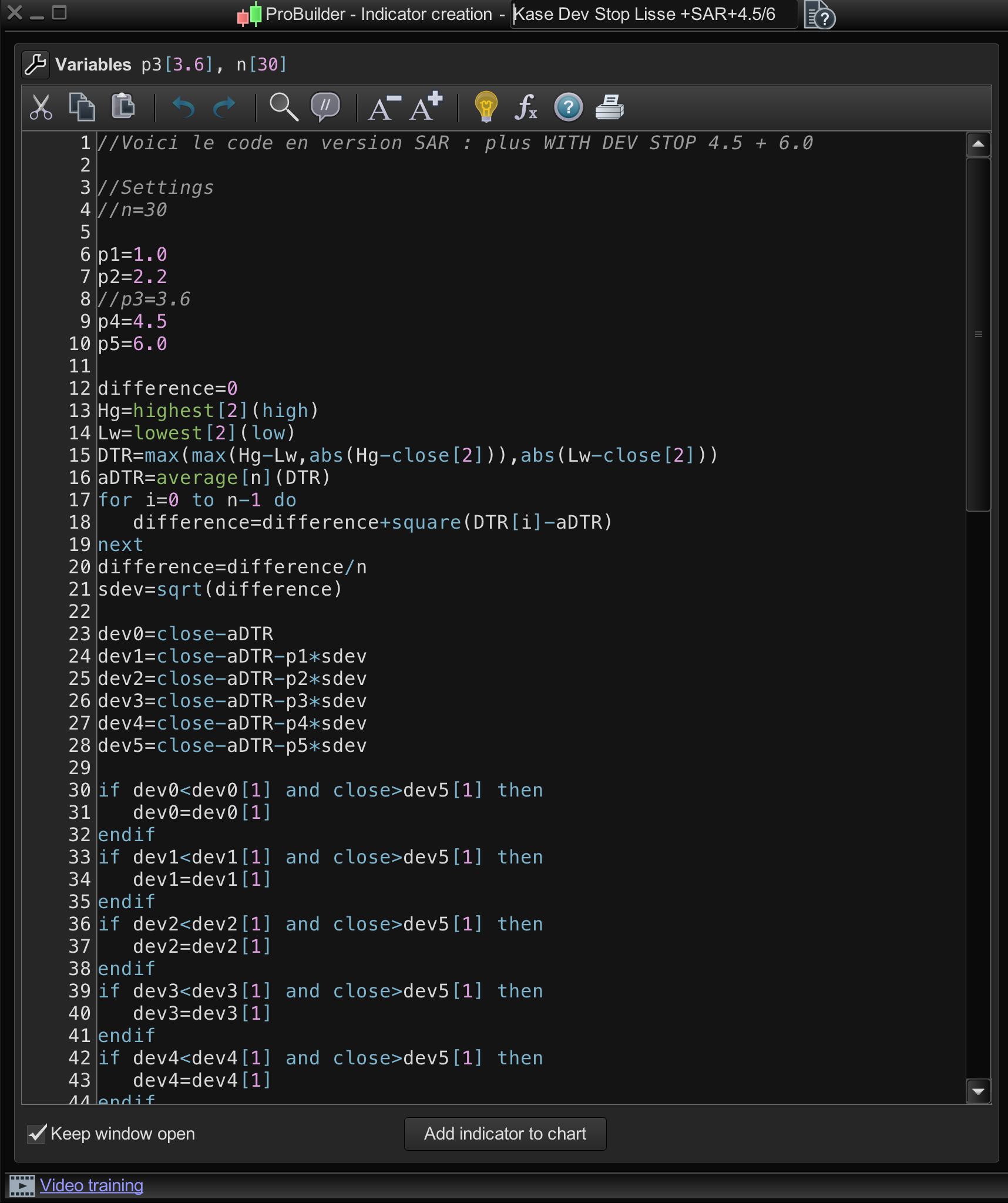

Indicator Code:

//Settings

n=30

//p1=1.0

//p2=2.2

//p3=3.6

//p4=4.5

//p5=6.0

difference=0

Hg=highest[2](high)

Lw=lowest[2](low)

DTR=max(max(Hg-Lw,abs(Hg-close[2])),abs(Lw-close[2]))

aDTR=average[n](DTR)

for i=0 to n-1 do

difference=difference+square(DTR[i]-aDTR)

next

difference=difference/n

sdev=sqrt(difference)

dev0=close-aDTR

//dev1=close-aDTR-p1*sdev

//dev2=close-aDTR-p2*sdev

//dev3=close-aDTR-p3*sdev

//dev4=close-aDTR-p4*sdev

//dev5=close-aDTR-p5*sdev

if dev0<dev0[1] and close>dev5[1] then

dev0=dev0[1]

endif

if dev1<dev1[1] and close>dev5[1] then

dev1=dev1[1]

endif

if dev2<dev2[1] and close>dev5[1] then

dev2=dev2[1]

endif

if dev3<dev3[1] and close>dev5[1] then

dev3=dev3[1]

endif

if dev4<dev4[1] and close>dev5[1] then

dev4=dev4[1]

endif

if dev5<dev5[1] and close>dev5[1] then

dev5=dev5[1]

endif

dev6=close+aDTR

//dev7=close+aDTR+p1*sdev

//dev8=close+aDTR+p2*sdev

//dev9=close+aDTR+p3*sdev

//dev10=close+aDTR+p4*sdev

//dev11=close+aDTR+p5*sdev

if dev6>dev6[1] and close<dev11[1] then

dev6=dev6[1]

endif

if dev7>dev7[1] and close<dev11[1] then

dev7=dev7[1]

endif

if dev8>dev8[1] and close<dev11[1] then

dev8=dev8[1]

endif

if dev9>dev9[1] and close<dev11[1] then

dev9=dev9[1]

endif

if dev10>dev10[1] and close<dev11[1] then

dev10=dev10[1]

endif

if dev11>dev11[1] and close<dev11[1] then

dev11=dev11[1]

endif

if close>dev11[1] then

flag=-1

else

if close<dev5[1] then

flag=1

endif

endif

if flag=-1 then

ind0=dev0

ind1=dev1

ind2=dev2

ind3=dev3

ind4=dev4

ind5=dev5

//k=1

r=0

g=191

b=255

else

ind0=dev6

ind1=dev7

ind2=dev8

ind3=dev9

ind4=dev10

ind5=dev11

//k=-1

r=255

g=128

b=0

endif

//ORIG return ind0 COLOURED BY k,ind1 coloured by k,ind2 coloured by k,ind3 coloured by k//

//ORANGE AND LIGHT BLUE

return ind0 coloured(r,g,b) style(dottedline,2) as "Warning Line", ind1 coloured(r,g,b) style(dottedline,2) as "Dev Stop 1.0", ind2 coloured(r,g,b) style(dottedline,2) as "Dev Stop 2.2", ind3 coloured(r,g,b) style(line,2) as "Dev Stop 3.6", ind4 coloured(r,g,b) style(dottedline,2) as "Dev Stop 4.5", ind5 coloured(r,g,b) style(line,2) as "Dev Stop 6.0"