right, that makes sense why it wouldn’t work using “//” on all the variables as per Vonasi’s tip.

I wrote:

To optimise variables in a strategy REM them out by typing // in front of them where their value is set and then click the spanner shown in my image and then enter the variable name and assign the start and finish quantities and steps you want to optimize over. Add multiple variables to do several at the same time – up to a limit.

I’m not sure where exactly it says in there to // out every variable in the strategy and then not bother to enter them in the optimize window and then wonder why the strategy does not work any more. I think it is more down to your interpretation of the help that is being offered to you rather than the quality of the help on offer.

Bard

BardParticipant

Master

Right! Thanks @nicolas,

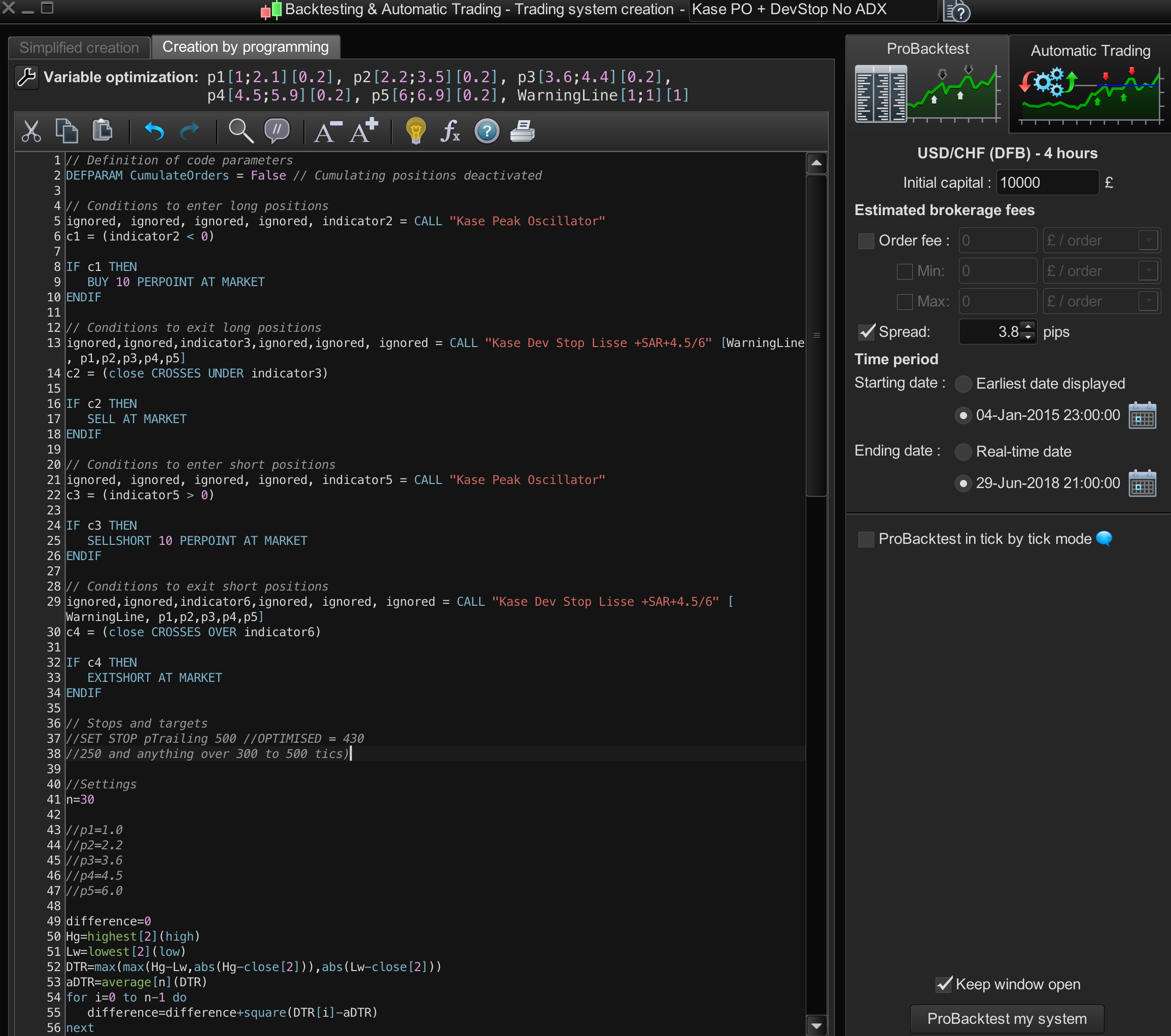

I’ve had to add the WarningLine as a variable to get it to work, yet… I think I’m setting up this Optimisation experiment up incorrectly?

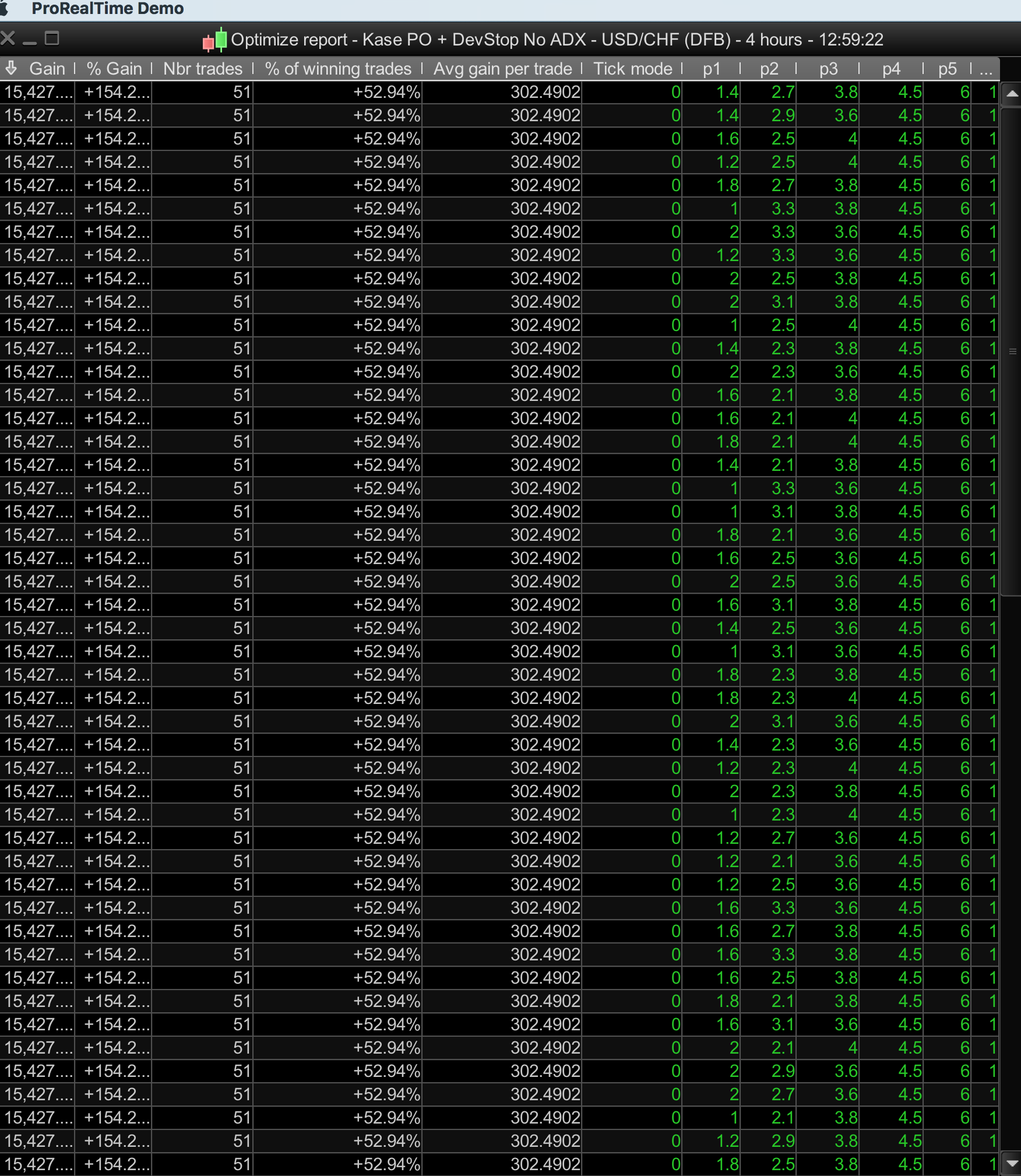

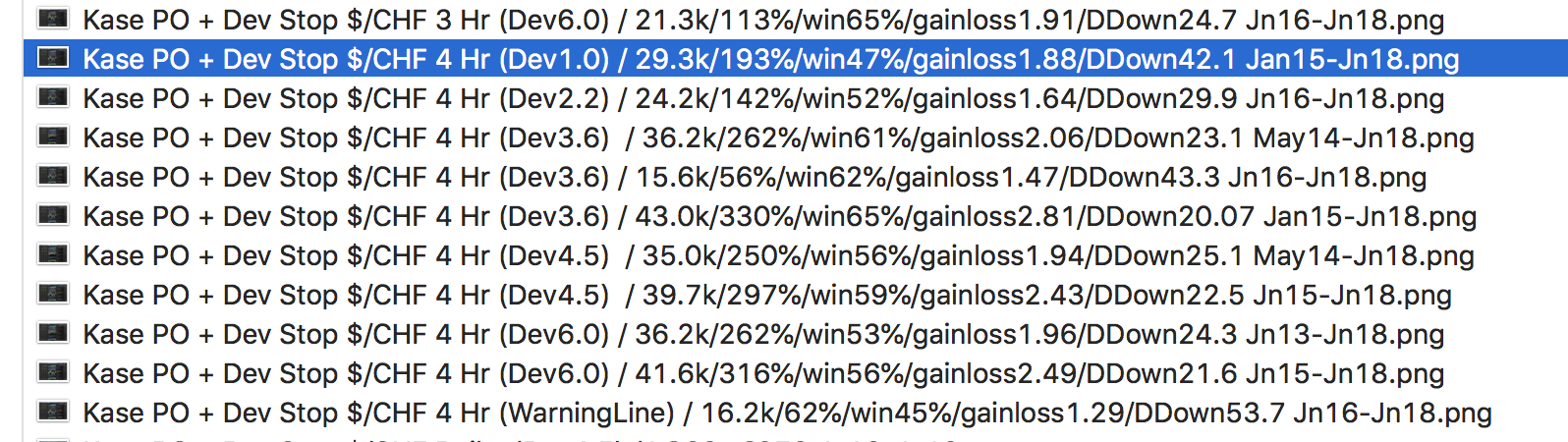

Different p1, p2, p3, p4, p5 (std deviations: 1.0, 2.2, 3.6, 4.5, 6.0) values do give different profit results when the p-values are manually set and tested “by hand.”

Although this optimisation runs perfectly well now, it still results in an identical £15.4k profit.. no matter what optimised p value is produced?

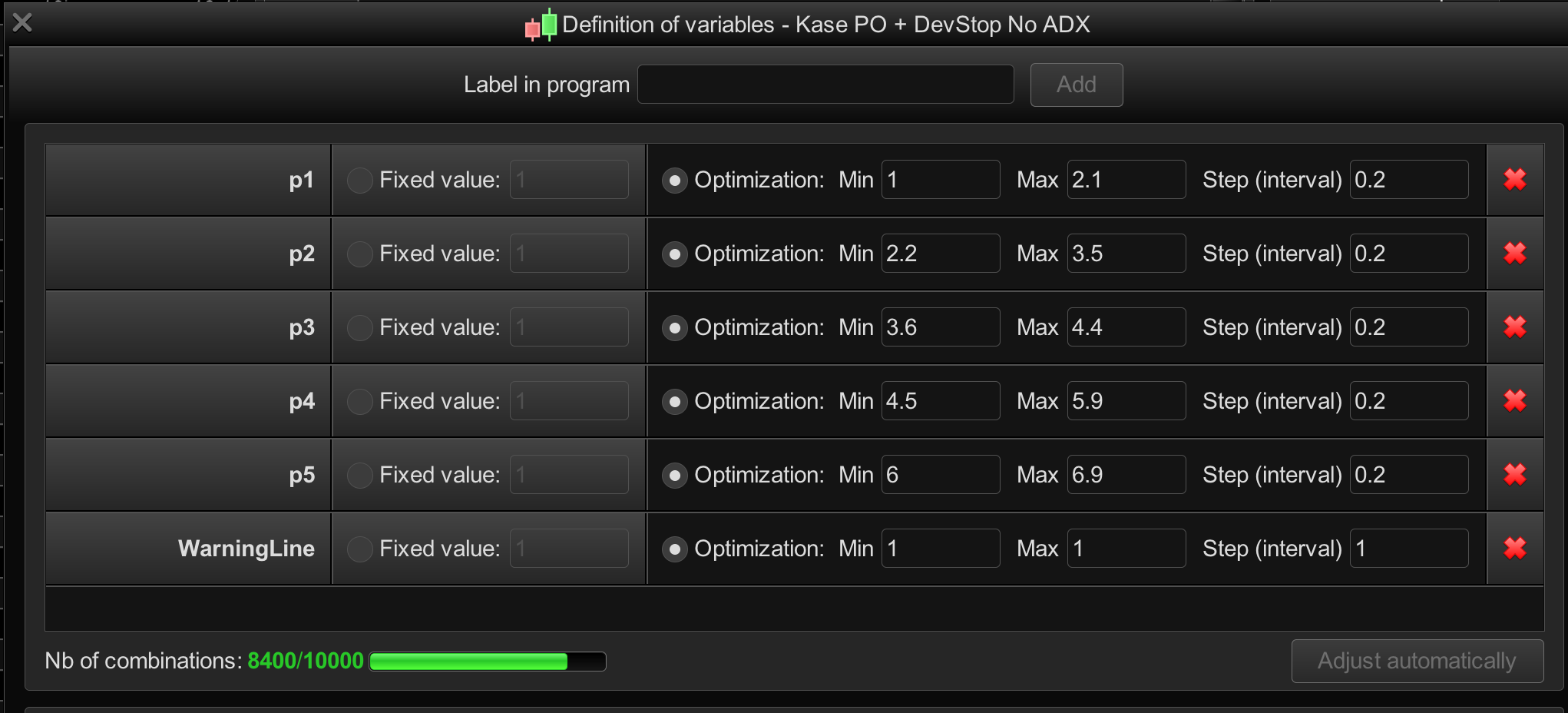

I thought that optimising values should be ranged so that:

p1 goes from 1 to 2.1 and

p2 from 2.2 to 3.5 and

p3 from 3.6 to 4.4 and

p4 from 4.5 to 5.9 and

p5 from 6.0 to 6.9)

but still it produces the same profit? Please see screenshot.

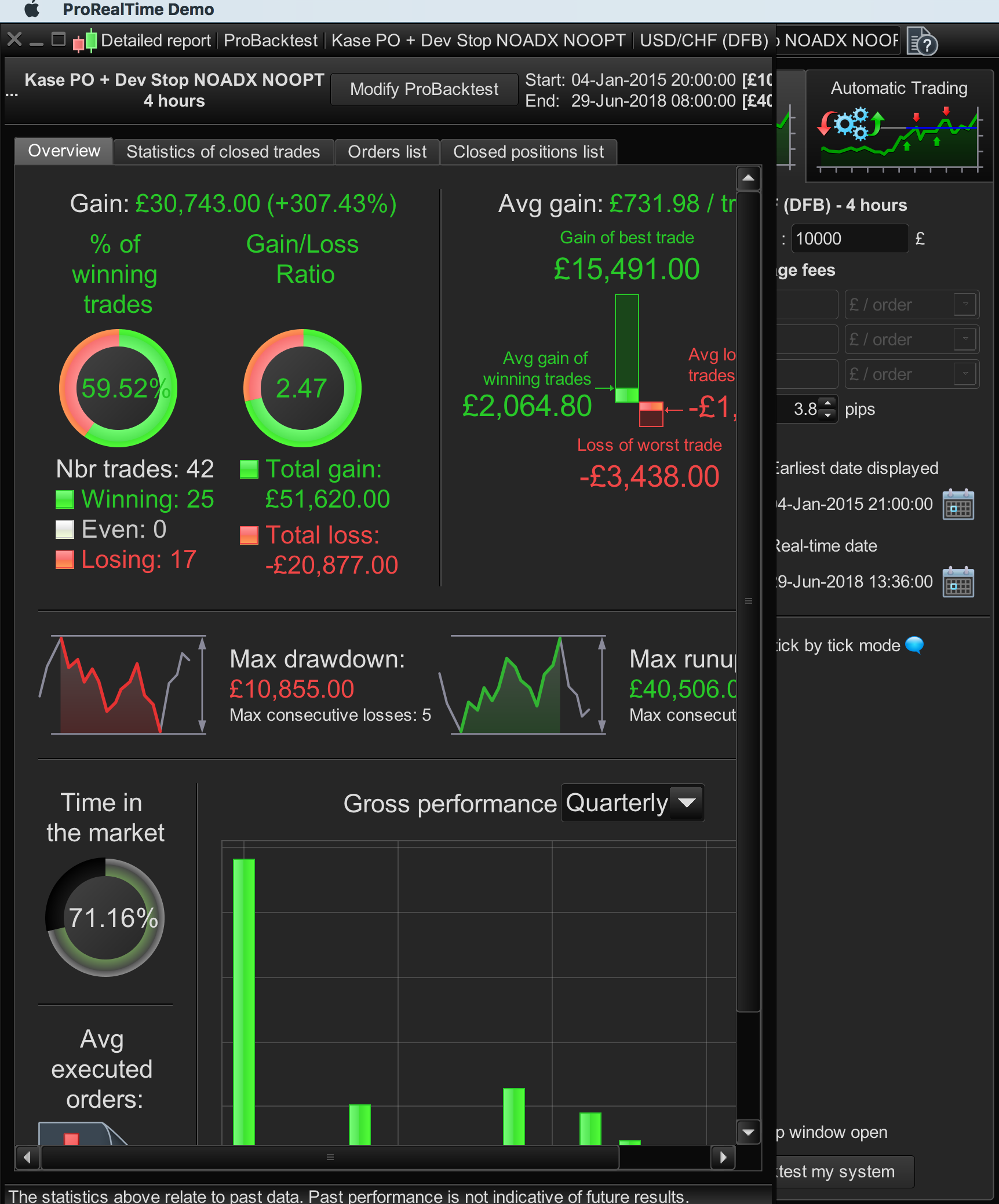

Profit using Dev Stop 4.5 also posted as a screenshot.

BardParticipant

Master

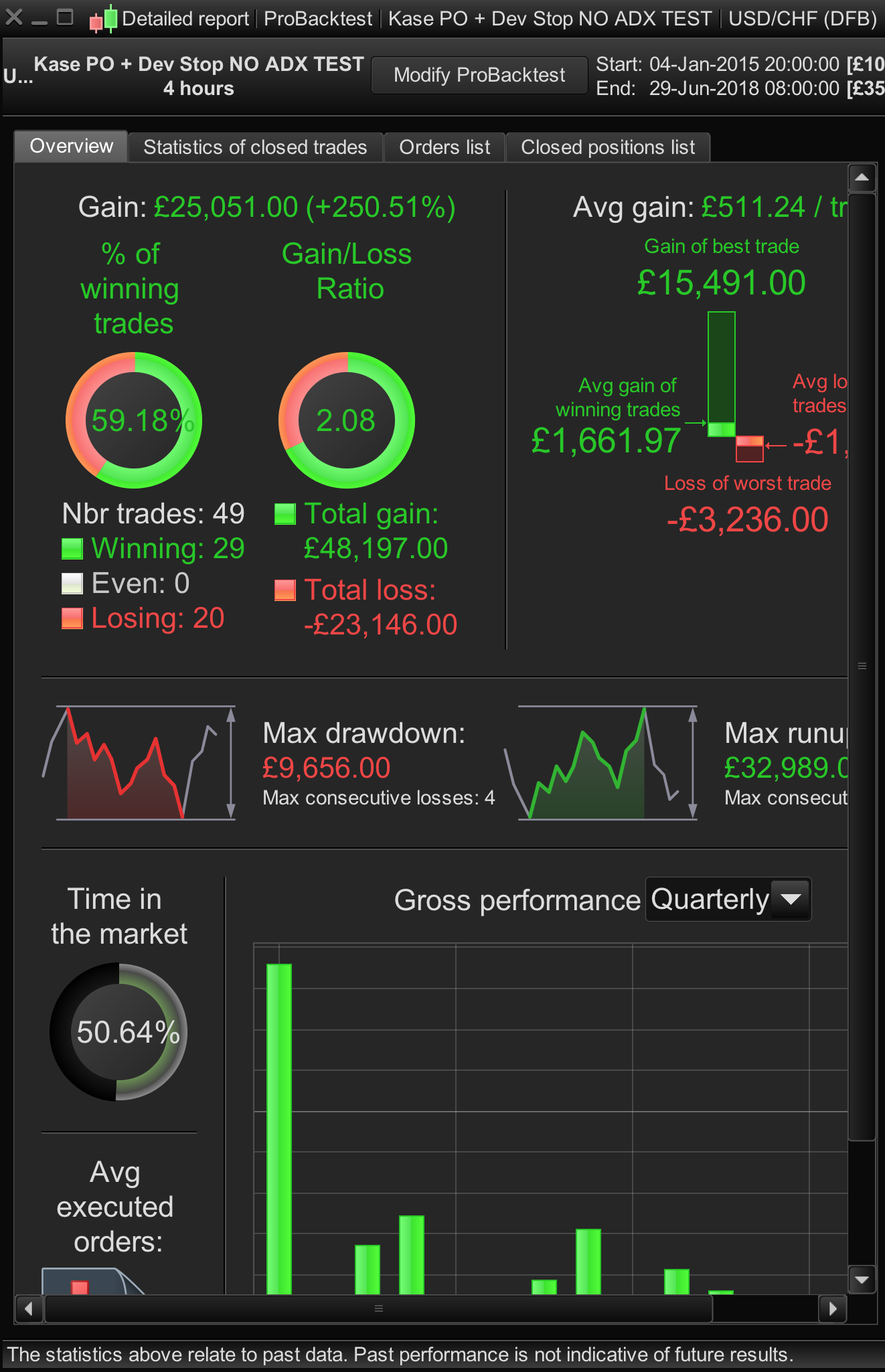

ps/ Sorry ignore second image with profit of £25,051.

It was meant to be this image using dev stop 4.5 and a profit of £30,743.

BardParticipant

Master

I haven’t “//” every variable. Line 121 onwards are commented out to allow it to work in strategy. I commented out the correct lines 44 to 48 as per your guidance but you generously assumed I know what I’m doing and would add the external variable definitions into the actual indicator itself and not just the strategy.

Sorry for my D’oh! moment (I seem to have a lot of them on this forum) and any aspersions upon your much appreciated help.

BardParticipant

Master

In a backtest manually placing the Dev Stop at 4.5 (standard deviations) of (double) TR the system makes £30,743.

Using optimisation it makes £15k.

Does anyone know what is causing this optimisation issue with Kase’s Dev Stop?

Cheers

Bard

BardParticipant

Master

Hi

I’m wondering how to set the right parameters for this Dev Stop optimisation?

I figure my post above (78696) is all wrong in terms of how I have given each p1, p2, etc, a range of values so it could be optimised — as per that screenshot in that post above. Ultimately I was hoping that I would just get one result. Eg, your Dev Stop needs to be set at 4,2 std deviations for example, to get the max profit. Do you have any idea how to set these parameters for an optimisation with the Dev Stop indicator @nicolas?

Many thanks,

Cheers

Bard

(The post above this one, just explains that the profit is higher when manually choosing a Dev Stop (4.5 std devs) than the optimisation run which has less profit and lots of different p values 😳)

In your previous post, results of optimization are all the same, it’s because you haven’t commented out the variables in your strategy. If the variables are declared in the code, they override the ones from the optimization window.

The optimization tool, in its current state, will always return the greatest profit, and should give one hundred results with different variables values. There is no one path to lead a perfect optimization, but you can save you a lot of time if you make WFA instead, to simulate Out Of Sample results with your optimized variables.

BardParticipant

Master

Yet I can see in the system code I did REM those lines out as per Vonasi and your advice, please see screenshot (i).

“There is no one path to lead a perfect optimization”

I was curious to see what the optimisation did on Currencies compared to Indices after Cynthia Kase said that you need to use a 4.5 Dev Stop sometime as the equities markets “tend to trade in a more erratic manner.” (And 3.6 std devs was meant to be the “get out now, no point of no return.” 🙄)

Please export the strategy as an .itf file so I can able to import it and test on my own.

BardParticipant

Master

Thanks @nicolas, I’ve drop-boxed the .itf file here:

https://www.dropbox.com/s/2pw644fommcr3jz/KasePO%2BDevStopNoADX.itf?dl=0

Cheers, have a great weekend.

Just exporting the strategy from your PRT platform and then adding the ITF file the same way that you would an image to your post makes it much easier for others to get access to it. 🙂

BardParticipant

Master

Hi @Nicolas, Wondering if you got a chance yet to look at the strategy to determine why it’s not optimising the Kase Dev Stops?

Cheers Bard

Because all settings in your indicator “Kase Dev Stop Lisse +SAR+4.5/6” = p1 to p5, are declared in the code between lines 6 to 10. So, they override the ones you are optimizing.

Delete them or comment them.

BardParticipant

Master

Thanks for clarifying that @nicolas, so even though the indicator code which was written out in the system was REM’d out, the actual original indicator wasn’t and that was what the system was using to optimise.

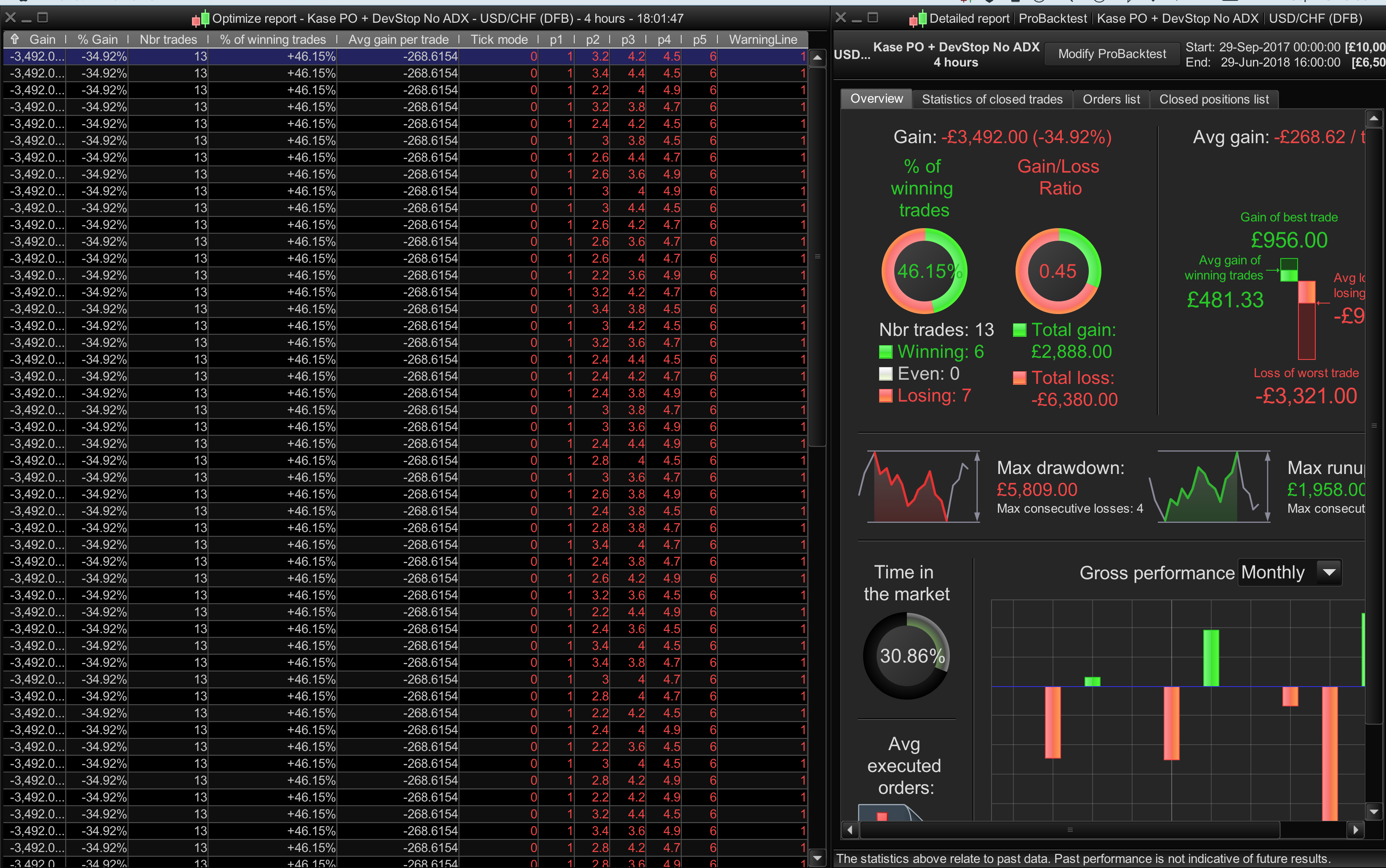

Okay, so in the past I’ve done manual backtests from Dev Stop 1.0 to Dev Stop 6.0, and got profits on all of them for the 4 hour Swissy… but apparently not when running an optimisation just now?

Pls see optimisation loss image and a screenshot of the profitable results.

I’ve attached the itf strategy here too.

I guess I must be setting up the optimisation wrong? (I added a screen of those parameter too).

Cheers for any insights, be good to finally nail this optimisation!

BardParticipant

Master