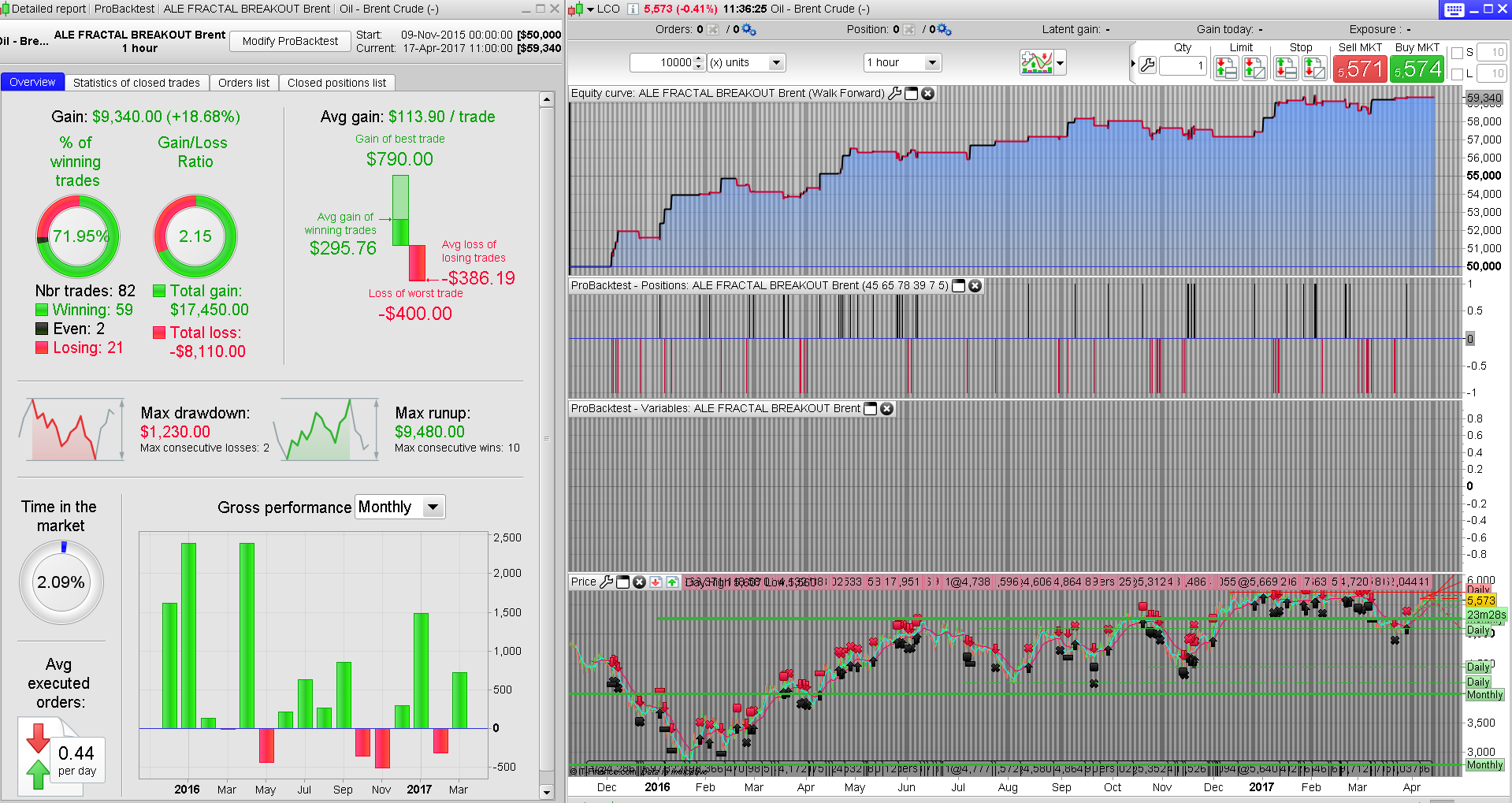

Yes I know that problem. I might have found another oppertunity i Brent Oil. But my data is limited, so first I used the large contract- not the mini to get the most backtrack data. But still its only from nov 2015. perhaps someone could take a look in a 200000 sample platform. Here is the results.

//Brent Oil(LOC) - IG MARKET

// TIME FRAME 1H

// PROBACKTEST TICK by TICK - 100.000 bars

// SPREAD 1 point

// Elsborgtrading

// WF: not ancored- 5 Rep, in sample 70%, OOS 30% optimized in times of two pairs

// 1 pair

//Period of fractal level: CP= 40 to 50, 1 point

//Stop loss by Donchian channel: DC = 65 to 80

//2nd Pair

//Trailing Stop long: TGL = 5 to 15 , 1 point

//Trailing Stop Short: TGS= 5 to 15 , 1 point

//3rd pair

//TP 60 to 80 , 1 point

//SL 30 to 45 , 1 point

DEFPARAM CumulateOrders = false

Reinvest=0

if reinvest then

Capital = 50000

Risk = 1//0.1//in % pr position

StopLoss = 39//7//10 // Could be our variable X

REM Calculate contracts

equity = Capital + StrategyProfit

maxrisk = round(equity*(Risk/100))

MAXpositionsize=5000

MINpositionsize=1

Positionsize= MAX(MINpositionsize,MIN(MAXpositionsize,abs(round((maxrisk/StopLoss)))))//*Pointsize))))

else

Positionsize=1

StopLoss = 39

Endif

///BILL WILLIAM FRACTAL INDICATOR

//CP=PERIOD

CP=45

if close[cp] >= highest[2*cp+1](close) then

LH = 1

else

LH=0

endif

if close[cp] <= lowest[2*cp+1](close) then

LL= -1

else

LL=0

endif

if LH=1 then

HIL = close[cp]

endif

if LL = -1 then

LOL=close[cp]

endif

//LONG and SHORT CONDITIONS

//Positionsize=1

if (time >=100000 and time < 230000) then

C1 = (close CROSSES OVER HIL)

D1 = (close CROSSES UNDER LOL)

IF c1 and not shortonmarket THEN

BUY positionsize CONTRACT AT MARKET

ENDIF

IF D1 and not longonmarket THEN

SELLSHORT positionsize CONTRACT AT MARKET

ENDIF

ENDIF

//TRAILING STOP

TGL =14

TGS=5

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

// DONCHIAN STOP

DC=65

e= Highest[DC](high)

f=Lowest[DC](low)

if longonmarket then

laststop = f[1]

endif

if shortonmarket then

laststop = e[1]

endif

if onmarket then

sell at laststop stop

exitshort at laststop stop

endif

set target pprofit 78//TP//30

set stop ploss stoploss//*pointsize

//graph equity COLOURED(0,0,0) AS "equity"//black

//graph (((tradeprice-(tradeprice-((tradeprice*stoploss)/100)))*positionsize*pointvalue*100)/(equity))*100 COLOURED(0,0,0) AS "MAXRISK"

//graph (positionsize*stoploss/equity)*100 COLOURED(0,0,0) AS "MAXRISK"

graph (stoploss*positionsize/(equity+capital))*100 COLOURED(255,255,255) AS "MAXRISK"//Aqua

//Graph HIL COLOURED(0,200,0) AS "BREAKOUT LEVEL LONG"//HIL COLOURED(200,0,0) AS "BREAKOUT LEVEL SHORT"

Hi!

Tested it in 200k but didnt get so much more data. Full contract was the same data as you.?

Regards

Henrik

snippet for modulation of contract

n = 1+(ROUND((strategyprofit)/7500))

every 7500 € it adds a contract …. of course you could modify it

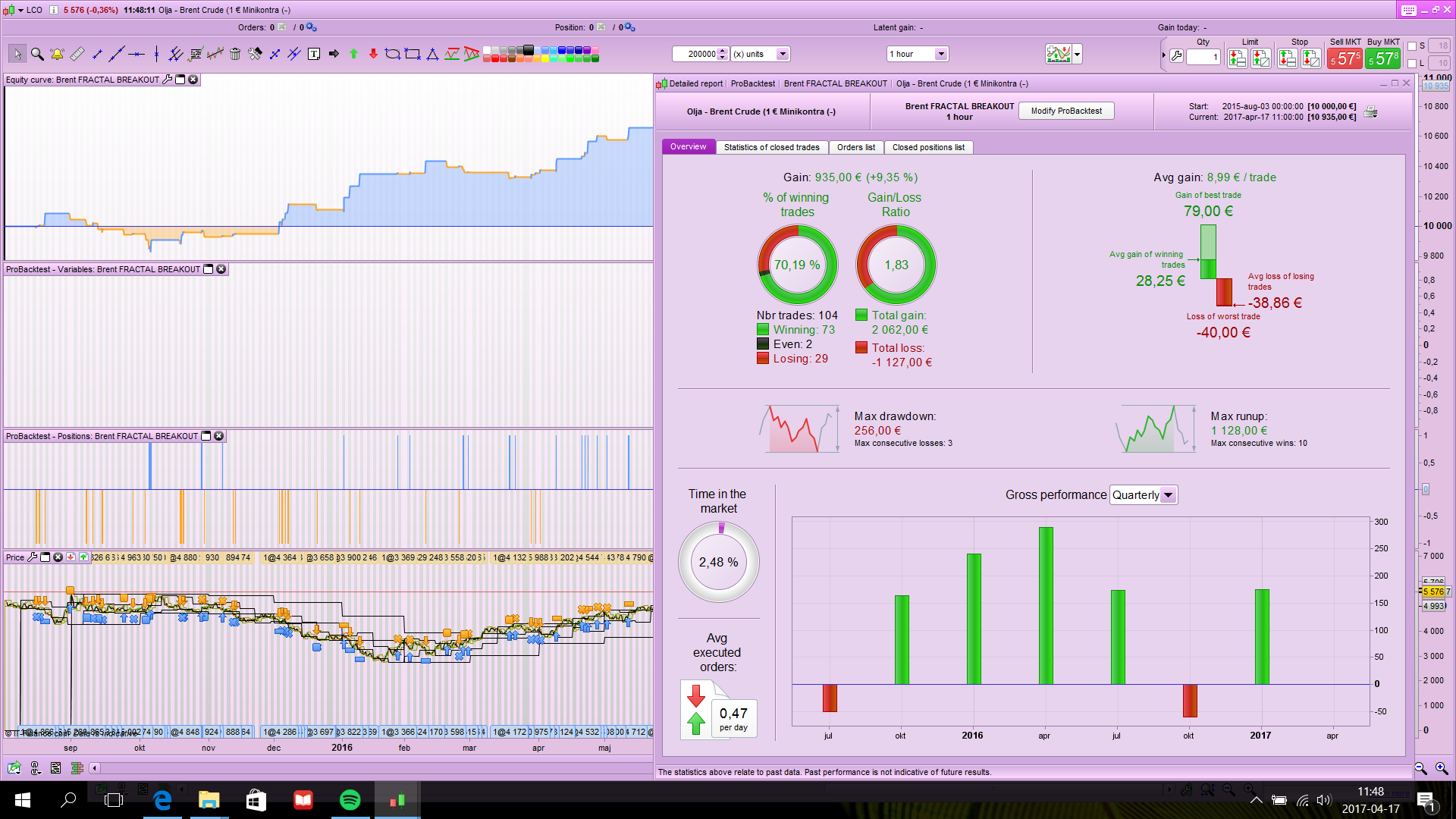

Hi Henrik you are using 1£ mini contract- but that should be the same. I was hoping for more years. it’s not statistically enough to rely on 1,5 years. sadly.

adds 1 contract every 2500 € and has max of 6 contracts .

Positionsize=1+(min (6,(ROUND((strategyprofit)/2500))))

FYI, it is now possible to have lots with decimal with IG. It is no longer needed to round up the contracts calculation.

ALE

ALEModerator

Master

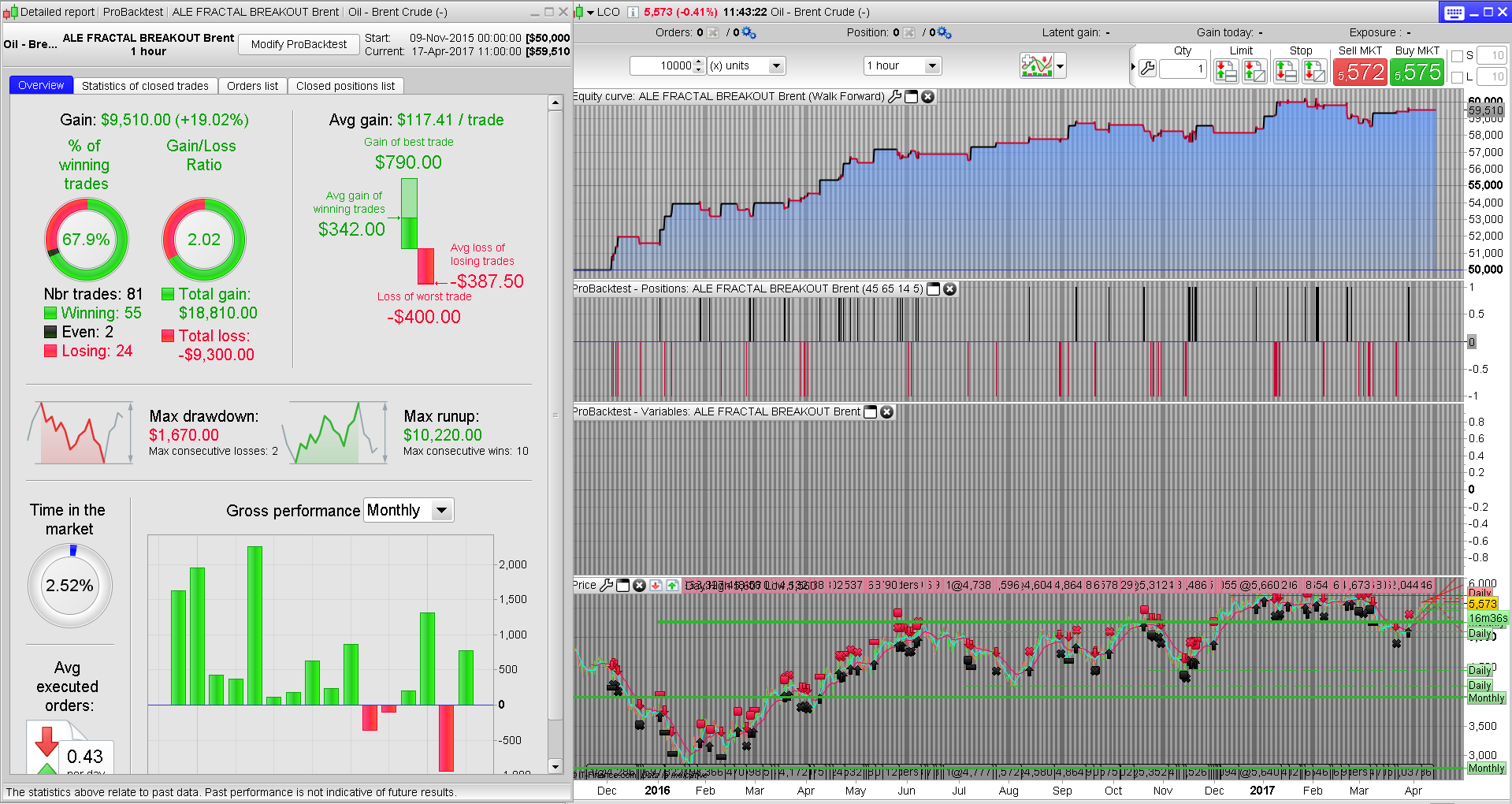

@Nicolas, Thanks, I’ve attached screenshot with a little explanation to test other pairs, please correct me if I missing something..

ALEModerator

Master

@Kasper, I’ll test your brent value soon with 200.000 bars WF

Thanks!

@Kasper, this is cash contrakt, dont more data with that contrakt. do you @ALE?

@Ale where’s the screenshot? 🙂

ALEModerator

Master

Henrik I’ll test it later, sorry!

forgot to attach… here it is.

Hi everyone!

Here is code for optimizing with WF on 100k data with ALEs numbers from first page.

Regards

Henrik

@Henrik, so to be clear this is the code that everyone should now use to make their optimizations?