Dear all

I have elaborated a little over an idea originally posted in the forum by Bjoern posted as True Range Breakout EUR/USD.

I applied to the Dax with the additional feature of switching from a breackout to a mean reversion strategy depending on some optimized value of the ADX indicator.

The strategy is a breackout strategy when the adx is above a certain value and a mean reverting strategy when ADX value is below that same value.

I have optimized it on several time frame and the results look quite promising, it would be great if someone think of a better way of discriminate between range trading vs trending phases. I have used the popular ADX indicator, but I am sure there are more efficient way to look at phase transictions in market.

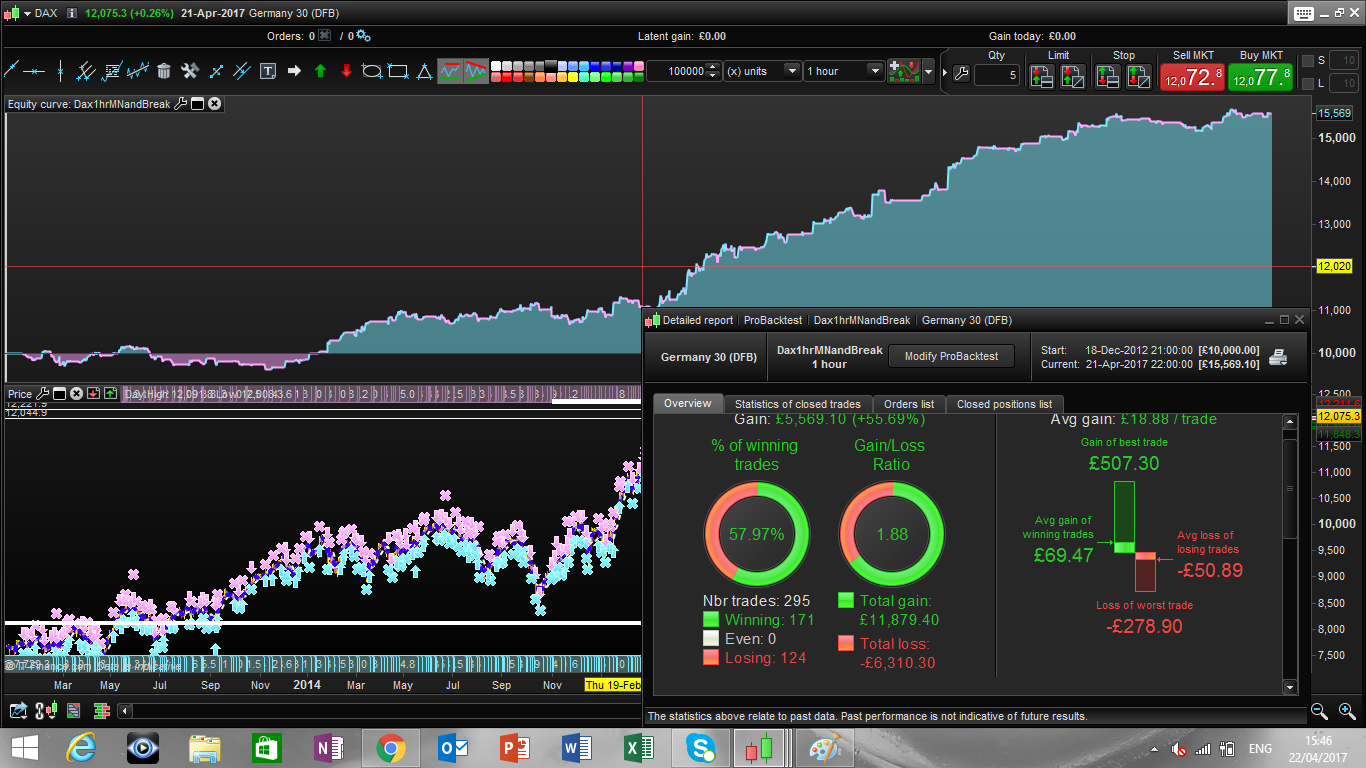

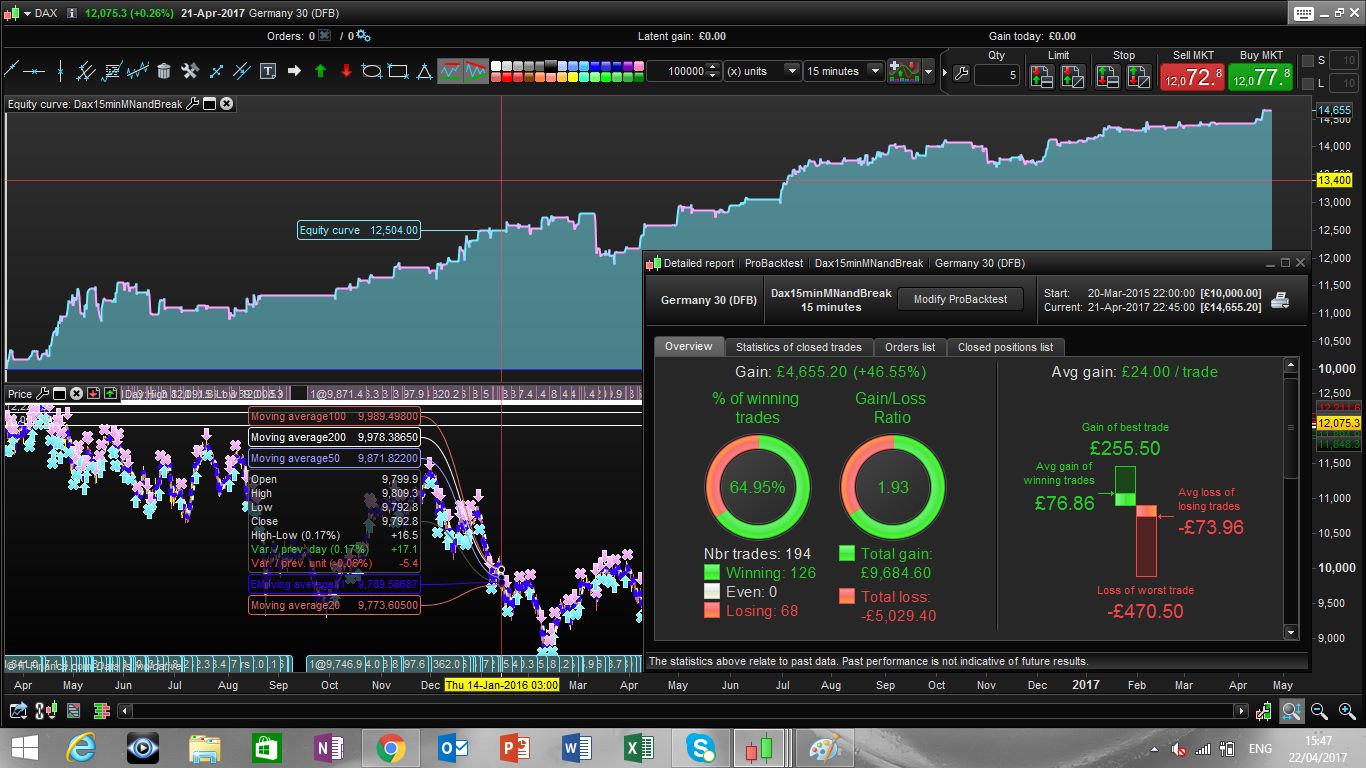

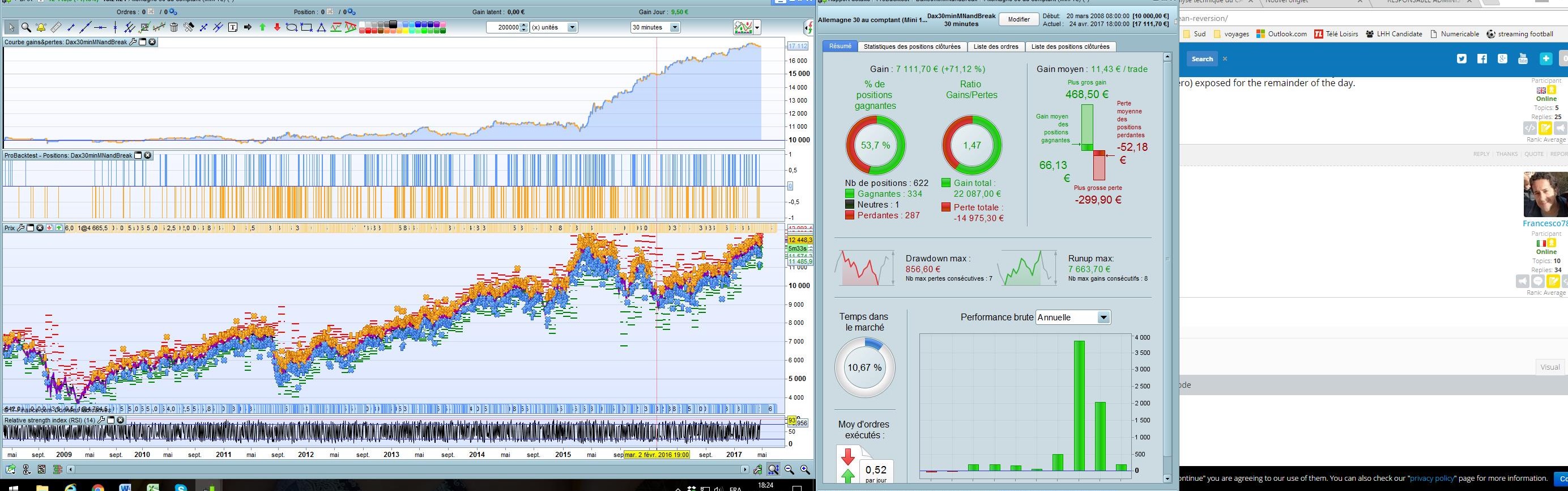

The results for different time frames are attached, together with the 30minutes code.

Best Regards

Francesco

reb

rebParticipant

Master

Hi Francesco

Your strat seems very interesting. I see 2 points about it :

- For the moment there isn’t any SL which can be a bit risky

- although the strat is active between 8 and 21h, you put a spread of 1pt. It inflates the results a bit. During 8 and 9 / 17h30 and 21, the stread by IG is 2pts

I ‘ll post a 200K backtest tonight or tom

Reb

Thank you Nicolas,

Reb: Regarding SL I agree they can be set in order to reduce the risk but I decided to avoid SL and Take profit because

- the condition to be flat at the end of every trading day is already a good risk mitigant

- the back test worsen if I add sl and tp and furthermore will be dependant of 2 more variables, since there are already many variables to be settled through optimization I wanted to limit the risk of overfitting.

- I have listened to an interview with the trader Tomas Nesnidal https://www.youtube.com/watch?v=X424q0Dv_0g. Apparently his main focus are breakout strategies and he said that in his experience is generally better to set exit strategy at the end of the day than set SL

Regarding the spreads you are absolutely right.

Many thanks for your comments and for your help with the 200k backtest

A wide stoploss to avoid flash crash would probably reassure a lot of people. In France and I think in England too, now when you open a new trading account, you can’t add any order on market without any stoploss.

Hi! Have you tried this strategy on any forex pairs?

Hello Victor, It works for EUR/USD, I tried USD JPY and GBP USD but no luck for those, would be great if someone could find other suitable currency pair

Regards

Francesc

I agree with Nicolas. Always use SL- if it breaks your strategy then widen it. It will save you on flash crashes or any other unforeseen marked changes. And again It will also in the end shows your RR and you can decide if it actually a good strategy in the future and not only in back test. A MM is also available to be implemented is SL is set.

We still are waiting for guaranteed SL in PRT so we can be even more secure.

Cheers Kasper

Maz

MazParticipant

Veteran

In production environment I would rarely have the same bot look for longs and shorts. If a strategy looks for both longs and shorts it is divided into a long and short sub-version. In the case of this system it would solve the stop-loss problem.

Whilst the long version might go long and stay long during a crash, the short version would have found a short entry soon after increase of downward momentum. So overall you would have been market-neutral (net-zero) exposed for the remainder of the day.

All the best,

Maz

Thanks Maz, I see what you mean and it sounds very clever.

Thanks a lot Reb!

Looks like is a specific strategy for the last couple of years..

Francesco

HI All

Awesome strategy really like it. Just one question is the minimum contract size for dax not 2 on the IG network?

Thank you StantonR, glad that you liked it! No here where I trade (italy) the minimum size is 1 per point…