Hey here’s something I’ve thought about for a while, now seems a good time to do it?

Attached is a video of my 25 Systems on Forward Test on Spread Bet with all at Lot size 1 / £1 per point.

Be great if you could do the same, gives a good overall feel for results we are getting?

Ha no can do … file size too big to attach!

Shout up if you do want to see as no point me messing about (reducing file size etc) if not much interest generated!?

Im shouting , love to see it thanks

Hey here’s something I’ve thought about for a while, now seems a good time to do it?

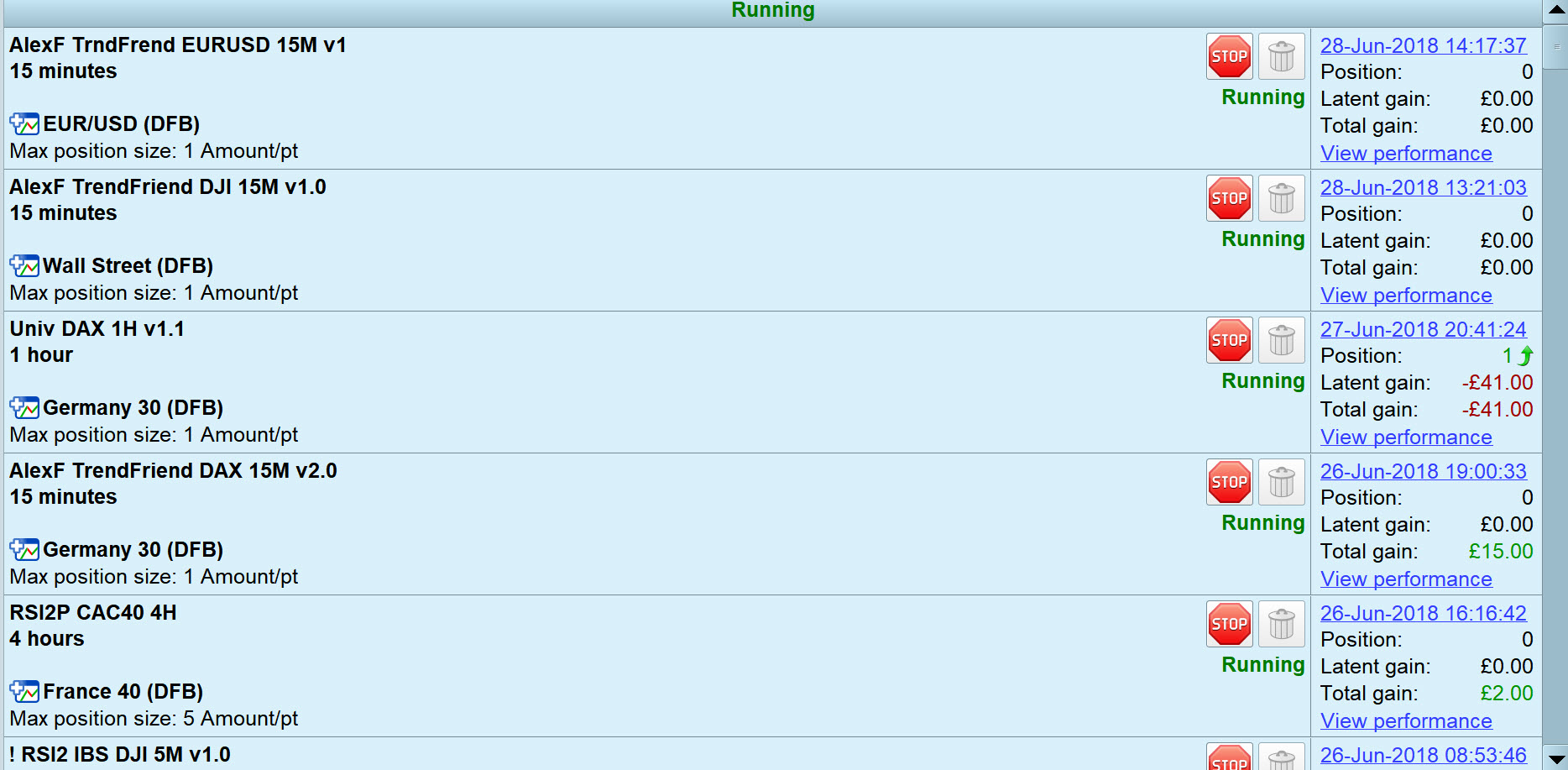

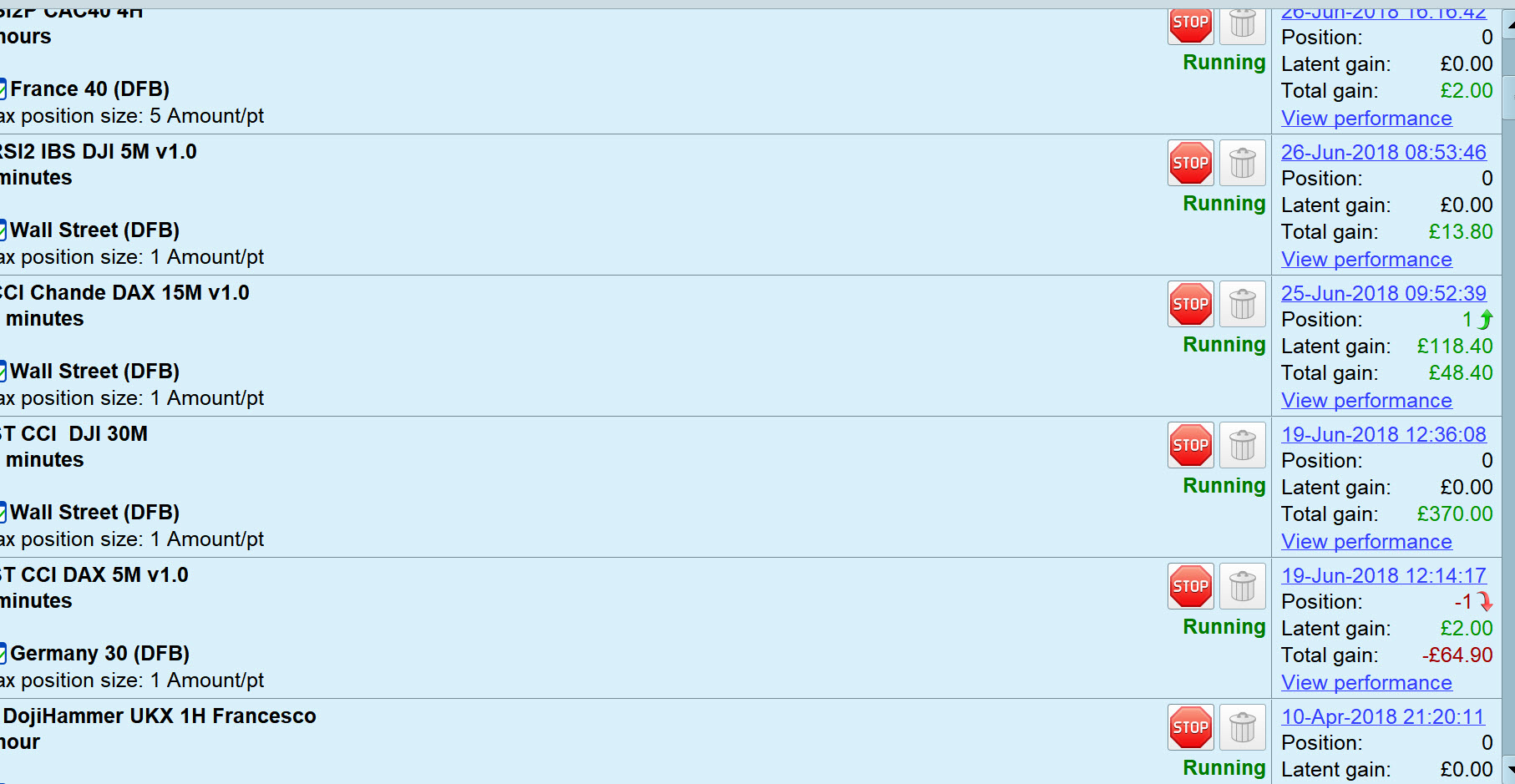

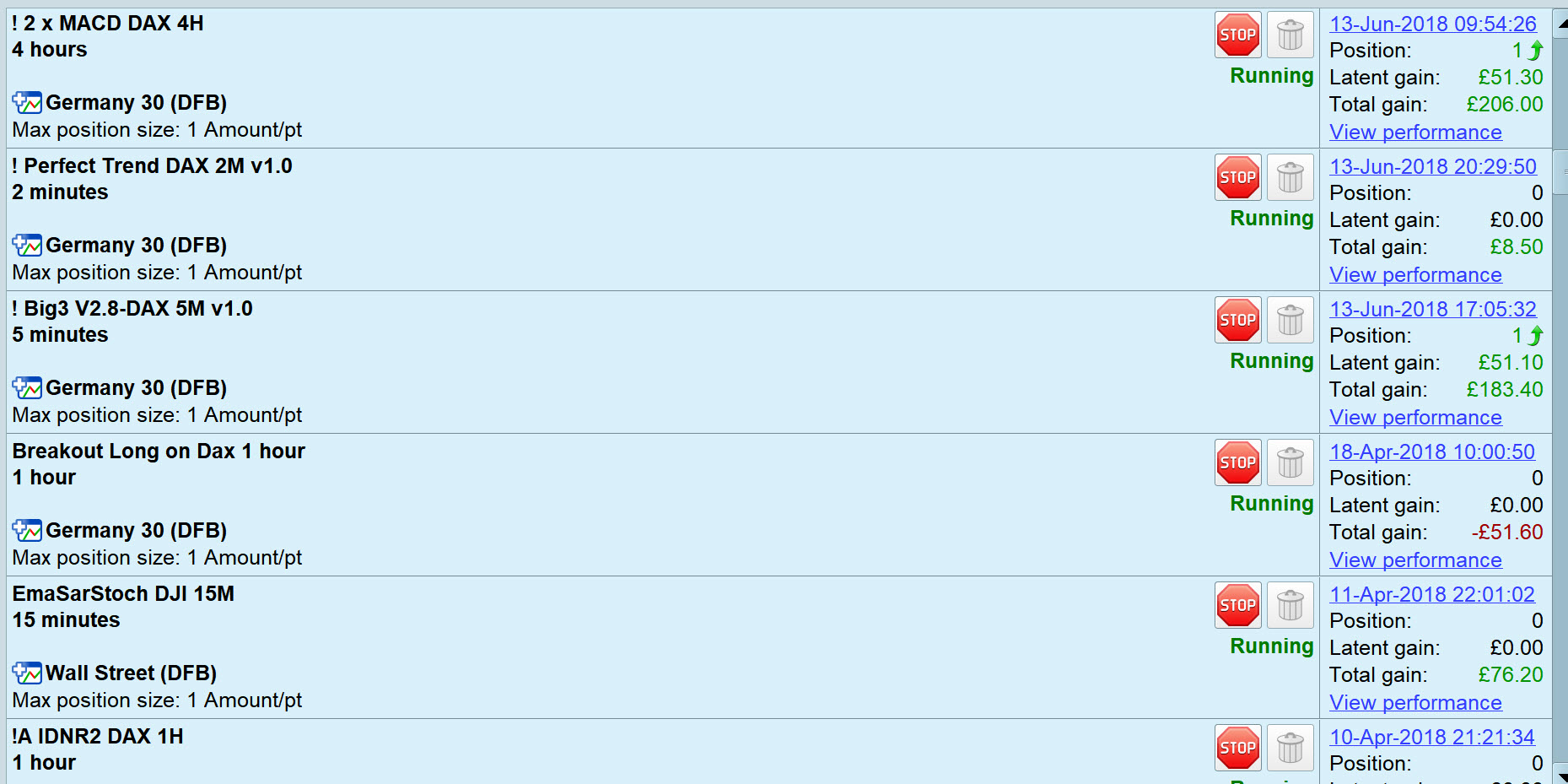

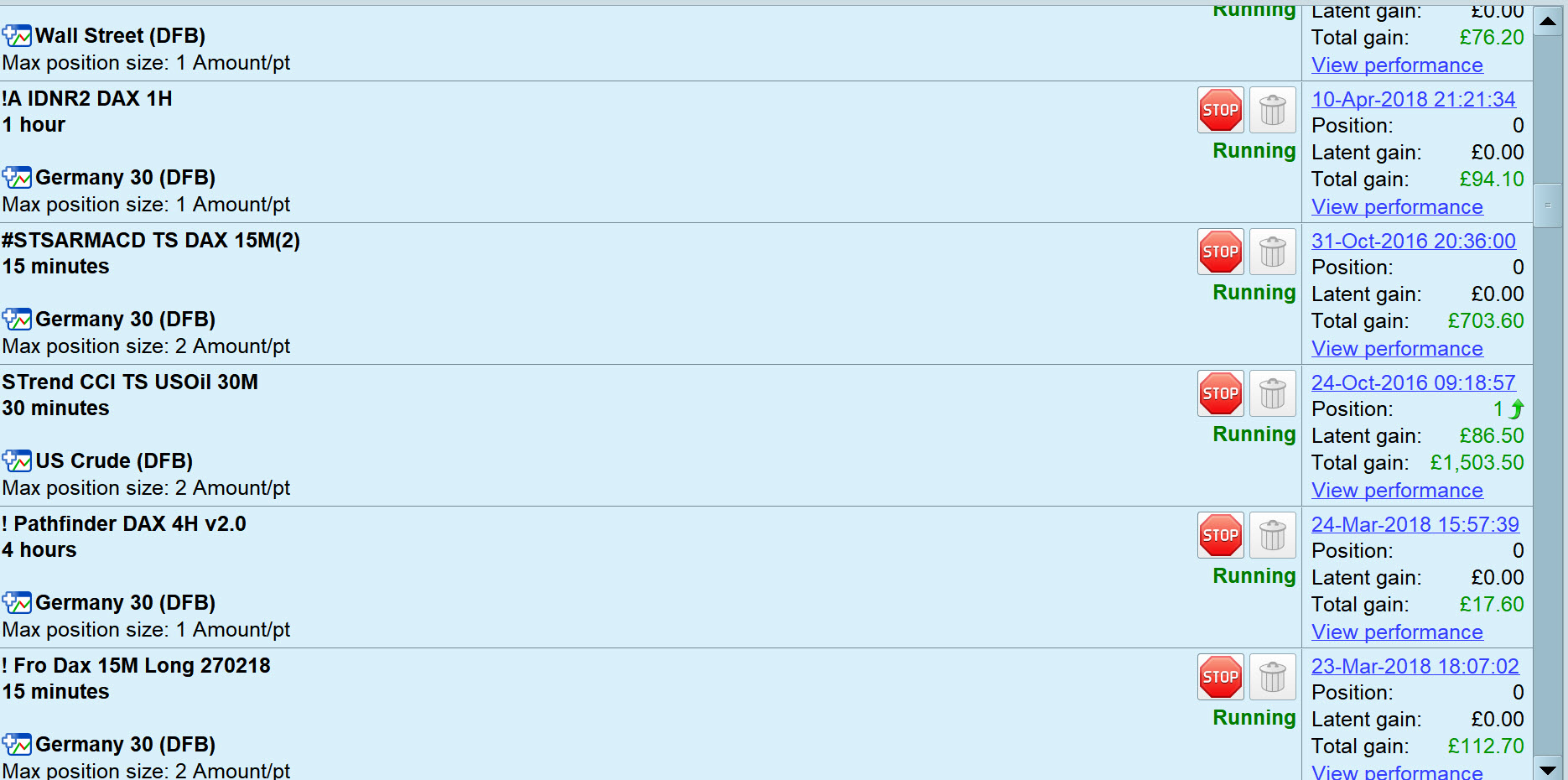

Attached are screen shots of my 25 Systems on Forward Test on Spread Bet with all at Lot size 1 / £1 per point.

Be great if you could do the same, gives a good overall feel for results we are getting?

MODS

Please delete my post above mentioning a video

Thank You

GraHal

Here’s # 5 and 6 (# 1 to 4 above)

Ok so when starting aback testing strategy what do I include?

I need an entry based on indicators and what about exit is this on indicators or tp limit and stop loss what do I use?

Please delete my post above mentioning a video

Probably best just to leave it as Brisvegas has replied to it and the thread would get very confused!

Ha if we knew the answer, we’d all be millionaires!? 🙂

I just try anything and everything, but – and I think you may be same as me in this (?) – I try (but fail often! 🙂 ) not to get hung up on making a particular strategy work! By that I mean if I make enough changes / add more indicators / optimise enough then I can get anything to produce positive results, even spectacular results!

But will this highly optimised strategy stand the test of time??

Why not start it off on Demo Forward Test, go and get a coffee / a beer then start on another strategy altogether??

Indicators make more logical exits, but TP and SL can give you a quick and dirty feel for if the Strategy is worth spending more time on?

Thanks for posting those images GraHal. Wouldn’t it be lovely if as well as the running gain/loss and overall gain/loss the window also showed number of trades, average gain per trade and maybe max draw down, trades per day etc as otherwise just the gain totals tells us very little at a glance about how the strategy is really performing.

Maybe one for your wish list?

number of trades, average gain per trade and maybe max draw down, trades per day etc

Above are all on my Wish List and always have been as I have suggested to PRT by all the various means open to us. I was waiting until you post your Wish List as I’m sure you’ll have these on yours and then I can think of more things I have already suggested!? 🙂

I sooo wish we could see a roadmap for Version 11 and then we could rest our frustrated brains! Nicolas makes version 11 sound very very exciting!? 🙂

I was waiting until you post your Wish List as I’m sure you’ll have these on yours and then I can think of more things I have already suggested!?

I think the point of the survey is being missed slightly. You are not expected to think of things that someone else has not already listed. If your top five things are the same as mine then post them – it is a survey!

If your top five things are the same as mine then post them – it is a survey!

Ah yeah gotcha, makes more sense, else it could turn out to be a repeat of the other Thread where we have already listed loads.

It be worth mentioning above (if you haven’t already) on the Survey Thread as if I missed that subtlety then others might also??

It be worth mentioning above (if you haven’t already) on the Survey Thread as if I missed that subtlety then others might also??

Done before you even wrote that.

All I’m going to say is that if running a survey is this difficult I can see why recent political surveys keep getting it wrong!

I can also see why maybe I am not getting anywhere. I am using my entire 4 yrs of historical data as my in sample.

I think I should be selecting a 6 month period for in sample and then use that optimization on the other 3.5 yrs of data to see my system is still successful?

What I believe I am doing now is confusing the hell out of me and the computer with excess data calcs.

Amy I correct?

Yes, but maybe a 50% IS and then test over the other 50% OOS data may be better. The 50% OOS will be more representative than 6 months IS and 3.5 years OOS?

But having said above, I tend to BT / optimise over 10k bars and then do WF test over 25k, then 50k then 100k. If at the 25k bars stage the performance has gone to rats then I would probably make changes to the strategy / code then repeat at 25k bars etc.

Reason for the 25k, 50k, 100k bars is that I hate waiting for the optimiser to do it’s thing (esp over 100k bars!) so this is a way for minimal waste of my life! 🙂

So if I first test the waters on IS for 10k bars and then extend as per your recommendation that sounds like a plan.

When you say 10k bars that is static for either 15 min, 30 min or 4hr TF I hope?

I have to ask wouldn’t it get straight to the point if everyone tested over the 100k bars straight of the bat? I understand the computer make time to process this much data but aren’t we doing this anyway by using smaller increments to get to 100k evenutaully? My thoughts on this are say we back test for 10k bars and then 50k bars and then 100k bars we find a certain optimization – Wouldn’t doing 100k bars straight away cut straight to the point and show you the results that work best over the collective 100k bars without doing each sample size?