Yep, given that these had simple fixed point take profits/stop losses there would have been something seriously wrong in PRT if the backtests did not match live. Both positions closed in profit early morning which was good to see. Need a few weeks of trades to see if the strategy is performing well though.

I am working on testing some short strategies in future, too many are focused on longs at the moment and it results in slightly biased outcomes as the market has been bullish for 8 yrs.

I may be wrong, but I think that in the case of a bear market, if the conditions that mark the indicators are produced, it is very likely that he will be able to touch the 50 take points equally. In one of the strongest and prolonged falls of the last years, in August of 2011, I see that the system 3 remains reliable. In addition to the bearish period from 2008 to 2009 also ends with benefits, then slower so we speak of the volume. Anyway, I am also working on developing a sales system that works. To see if we are lucky and find it soon. a greeting!

Great stuff, look forward to coming up with something that works. I have tried it simplistically with long and short using similar parameters on other strategies but even though some work the draws are simply too large. If you recall, we tested System 3 earlier with both Long+Short trades and that produced positive results but the draws were much worse than Long on its own.

I agree, there is a short system that could work equally as the long but I have a feeling that the parameters may need to be adjusted slightly between them. In my experience, indices go down a lot quicker than they go up (on average) because panic sets in etc so maybe we have to incorporate volatility indicators (eg like the VIX) and ATR to help identify the downward acceleration and take advantage.

The 1-4H system 3 took positions in both Dax and Cac today with the exits just occurred:

Dax open long @ 11,838.1 exit @ 11,888.4

Cac open long @ 4,859.8 exit @ 4889.8

Excellent news, has been winning for two weeks. I tried to use take and stop in%, to adjust wn every moment at the price we are in, but it is not as effective.

Lyny

LynyParticipant

Junior

@Raul, i try the Dax 1-4h system and it has been recently winning for 2 weeks. But recently Dax keep going up a lot, therefore, still need to test when Dax starts turning down. So far, it looks promise.

Hello lyny, yes, that was talking manel and I, despite having tested the robot over 10 years, much of it have been with the price going up. In spite of it, in its code, it has indicators like MACD, crossing of means and that the price is above another movable average exponential, reason why, the weeks or months that this in fall the price should not operate.

Hi Lyny – yes, we have tested it across market cycles (10yrs+) and as Raul says, apart from 1/2 wrong trades usually taken at the beginning/end of a downturn, the system just sits on the sidelines for the main part. Hence any trades taken during this period should have a lower impact on the overall results. We did develop a long+short system (see previous posts) but felt that the draw was too high to consider taking forward.

Raul – yes, I messed around with % levels on the System 3 but couldn’t find something attractive either.

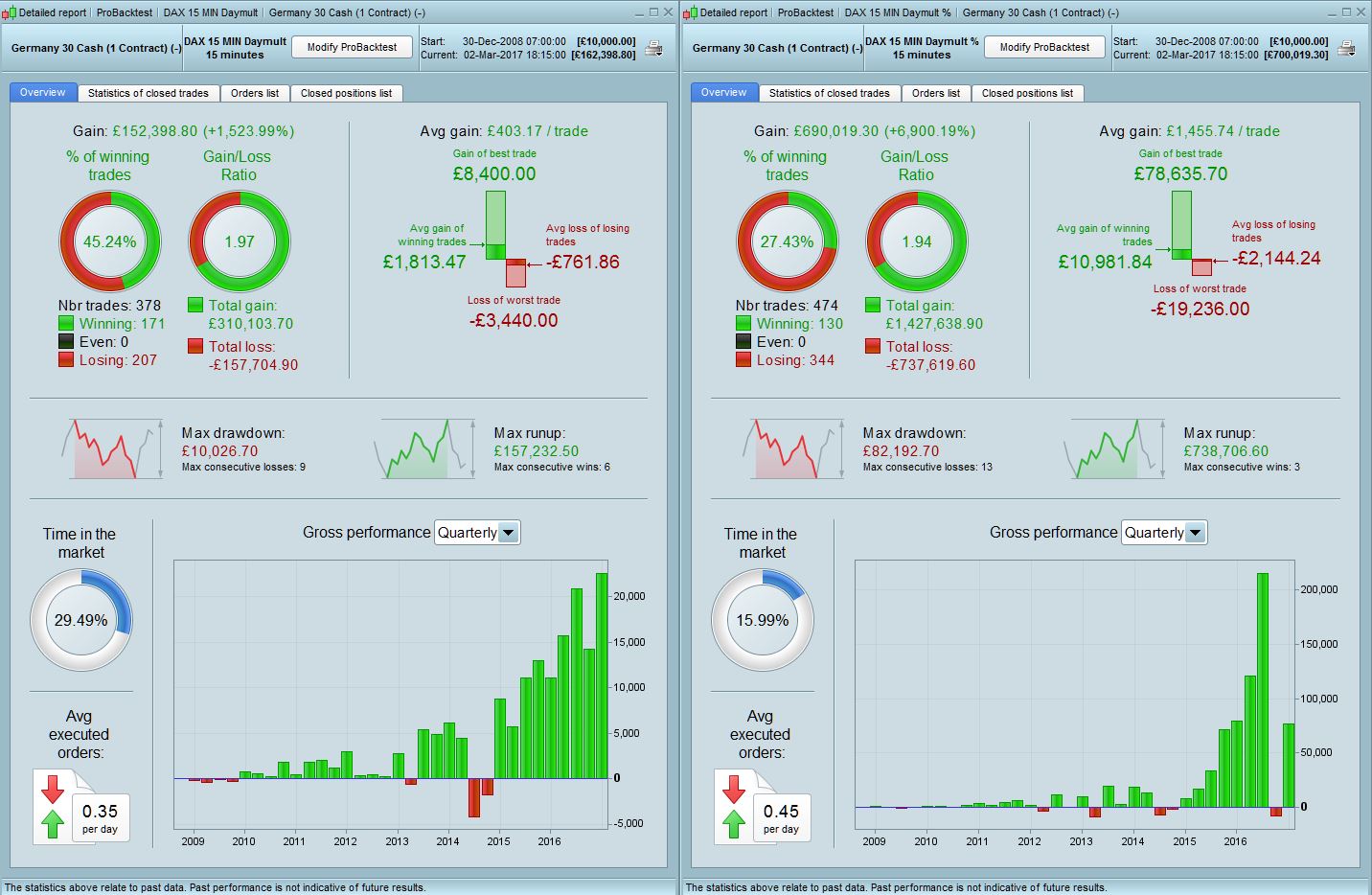

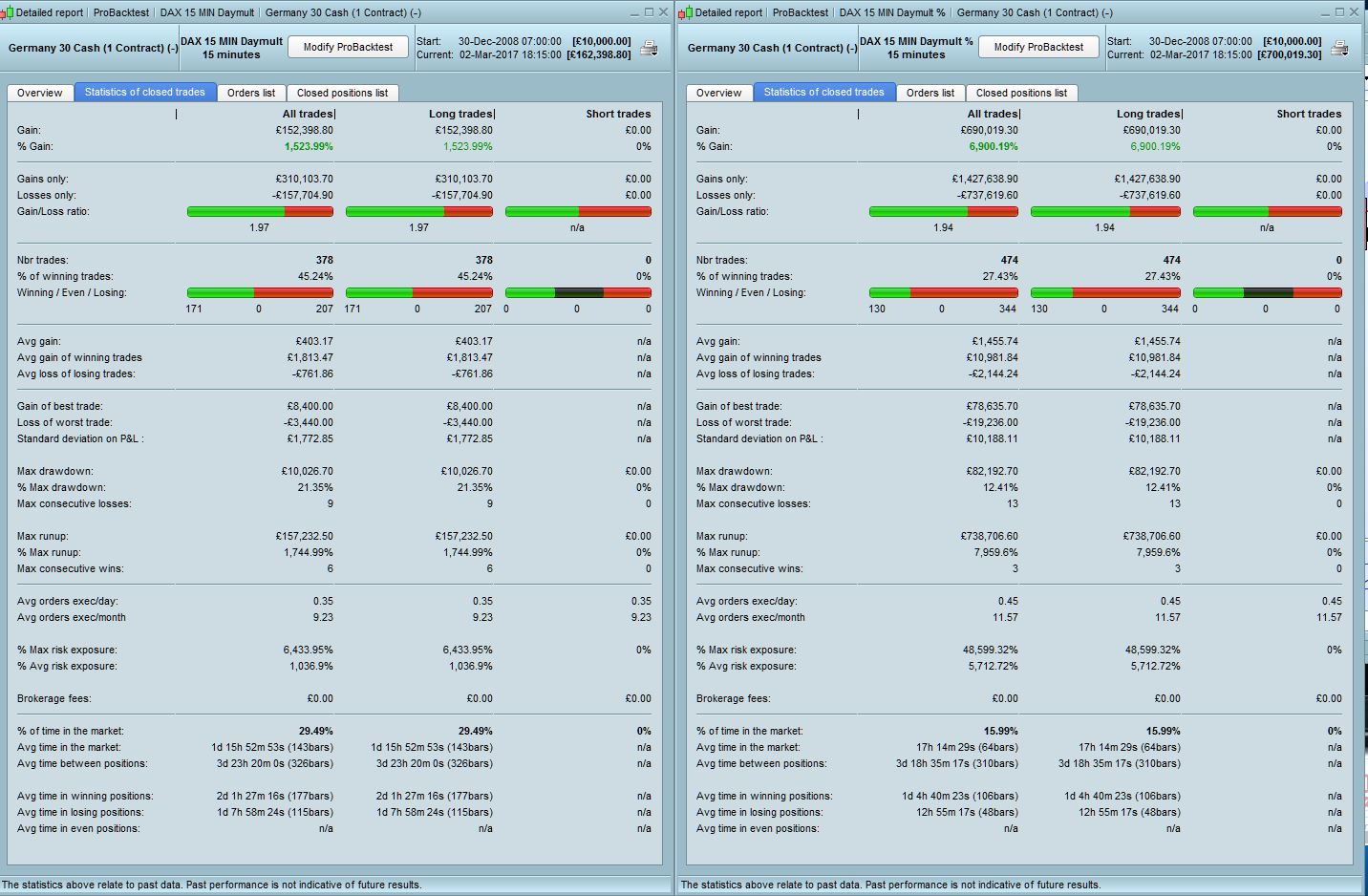

However, with regards to the 15m Daymult system, I put in a simple % based on the 100 period ema. 0.4% stop loss and 1.6% take profit – ie simple 1:4 ratio. Here are the results (note the scale on the RHS when viewing the curve). A few things we need to consider:

1)We would of course never be happy taking 400+ per point exposure to the Dax, the results are more of principle than what risk we would take in reality. We need to find a way of limiting the position size to say (100 max) but not lose too much in results. At the same time maybe create a smoother equity curve.

2) However, we don’t want to limit the position size too much at the beginning as its manageable and we need it to build up equity We can have a separate position management system that is only triggered when size gets to say 50per point (around year 4 according to backtest).

2)Using a % based system reduces the draw by almost half to around 12% which is actually pretty good considering it takes into account a large single loss of £19k.

3) The average time in market is again more than halved (64 bars vs 143 bars) which is helpful for reducing financing costs

4) The use of a % based on a ema average price could be changed – perhaps utilise other variables such as ATR, yesterdays price etc etc

Let me know your thoughts, many thanks.

DEFPARAM CumulateOrders = false

//DAX - 15M

sl=0.004*exponentialaverage[100]//80

tp=0.016*exponentialaverage[100]//150

p=18

d=20

m=1.5

Rg = 0.5

ONCE Januaryl = 1

ONCE Februaryl = 2

ONCE Marchl = 3

ONCE Aprill = 1

ONCE Mayl = 1

ONCE Junel = 2

ONCE Julyl = 3

ONCE Augustl = 1

ONCE Septemberl = 1

ONCE Octoberl = 1

ONCE Novemberl =2

ONCE Decemberl = 2

ONCE Monday = 2

ONCE Tuesday = 2

ONCE Wednesday = 1

Once Thursday = 1

Once Friday = 1

Once Saturday = 1

Once Sunday = 1

If Opendayofweek = 1 then

DayMult = Monday

ElsIf Opendayofweek = 2 then

DayMult = Tuesday

ElsIf Opendayofweek = 3 then

DayMult = Wednesday

ElsIf Opendayofweek = 4 then

DayMult = Thursday

ElsIf Opendayofweek = 5 then

DayMult = Friday

ElsIf Opendayofweek = 6 then

DayMult = Saturday

ElsIf Opendayofweek = 7 then

DayMult = Sunday

Endif

// saisonal pattern long position

IF CurrentMonth = 1 THEN

saisonalPatternMultiplierl = Januaryl

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplierl = Februaryl

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplierl = Marchl

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplierl = Aprill

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplierl = Mayl

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplierl = Junel

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplierl = Julyl

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplierl = Augustl

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplierl = Septemberl

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplierl = Octoberl

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplierl = Novemberl

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplierl = Decemberl

ENDIF

aMax = Highest[d](High)

aMin = Lowest[d](Low)

SupTnd = SuperTrend[m,p]

RngOk = (High-Low)/(aMax-aMin)<Rg

Equity = 10000+StrategyProfit

Risk = 0.015

n = Max(1,Equity*Risk/Sl/PipValue*SQRT(DayMult*saisonalPatternMultiplierl))//min(1,)

//n=1

cBuy = aMin[1]<aMin[2] And High<aMax[1] And Close>Open And RngOk And Close>SupTnd

If cBuy Then

Buy n Shares at Market

EndIf

SET STOP ploss sl

SET TARGET pPROFIT tp

CN

CNParticipant

Senior

Heya guys, checked back in here for the first time in a while, and WOW, amazing active thread.

What system is the one that would be a candidate for live-trading?

Thanks guys !

CNParticipant

Senior

Where can I find the .itf for dax 1-4 v3?

Hi CN – I would only be confident in the Dax and Cac 1-4H System 3 so far. The rest of the ones we tested in this thread have not produced better or less riskier results in my opinion. The Daymult % one above is currently being tested by me in Live and Demo so I will report on that when I have enough results.

However, given that even the System 3 code is still new, I would suggest amending the code and starting with a much lower risk just to make sure you gain confidence in the results after a few months of trades, you can then adjust and increase your risk thereafter.

Attached is the Dax 1-4H System 3 as requested. It should be run on 1H timeframe and please note that if you are in Europe you need to adjust the times in the code by +1hr. Enjoy !

CNParticipant

Senior

@Manel

nvm, saw that I didnt read your describtion in the first place

@ manel

please backtest with broker fees …..

dax mini 5 € : 5€ per contract

dax mini 1€ : 1€ per contract

thanks for all your work…

CNParticipant

Senior

Noticed that the backtest of daymult is 1pt. The robot opened a position this morning in the dax with the 5pts spread…

CORRECT me if I’m wrong. Does that not render the daymult robot non-profitable?