Time in the market is an important factor – often it is good to give a trade time to achieve what you expect but increased time on the market can also be increased risk exposure. I got thinking about this and decided to write some code to vary the exposure to risk as a strategy trades and came up with the following that I post here just in case it is of interest to anyone. It is not a complete strategy – you have to enter your own long and short entry conditions to make it work! I created it around an end of day strategy idea but it should work on other time frames. In the following description I refer to ‘days’ but you might want to think in candles for other time frames.

The idea is that you can set a maximum number of days that you want a trade to stay open (minD) and then get out as soon as a candle closes in profit or time runs out as you reach the maximum number of days. If it is a profitable trade then the exposure time for the next trade is increased by one day. This continues up to a maximum number of days which is maxD. If a trade is a losing trade then the number of days is reset back to minD.

There is also an averaging down part of the code which can be turned on or off by setting ‘AverageDown’ to 1 or 0. With this turned on if we are in a trade already and it is losing and entry conditions are true again then an extra position is opened. Normally this would be a dangerous game but our maximum days allowed in the market allows us to reduce our potential risk as we can only lose as much as a market would normally move from our average price in our maximum allowed number of days (we hope!).

There is also ‘PositionSizing’ that can be turned on or off too. With it on the first position is opened at whatever we set ‘StartPositionSize’ at and then if we average down the size of the next trade is increased based on however many days is our current maximum allowed. Be warned that turning PositionSizing on can be very scary for your bank account!

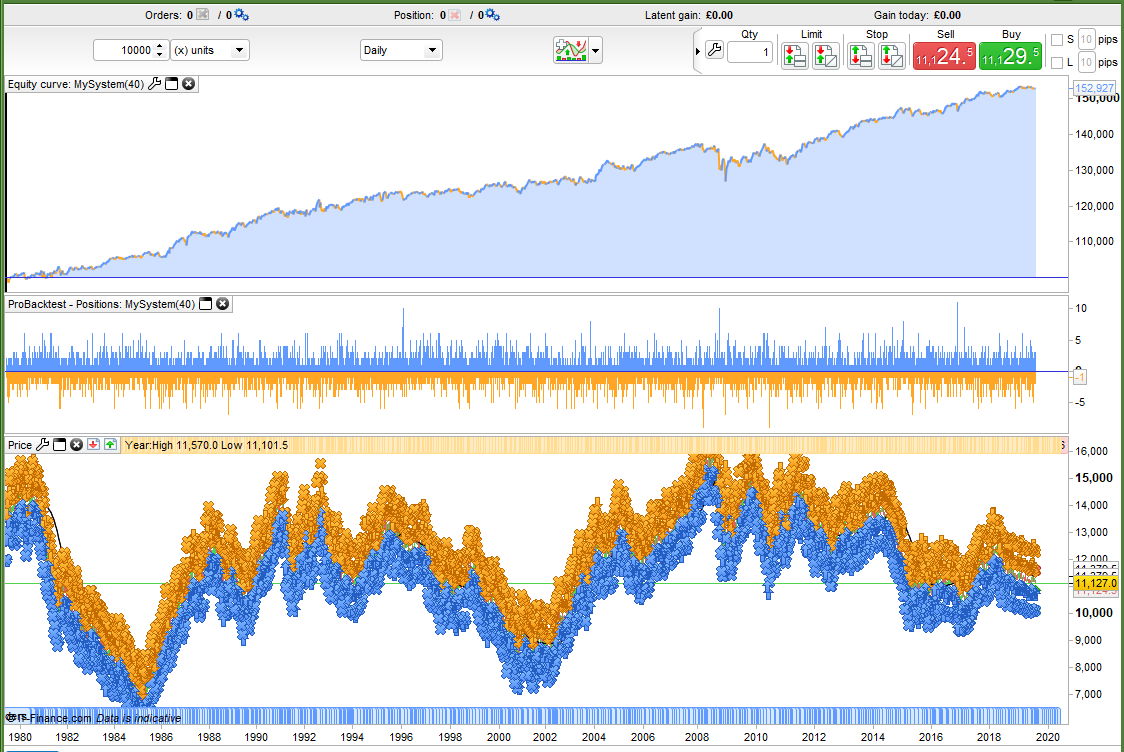

With a very simple set of price action entry conditions and position sizing turned off I was able to get the attached equity curve in the first image on EURUSD Daily with minD of 2 and maxD of 6.

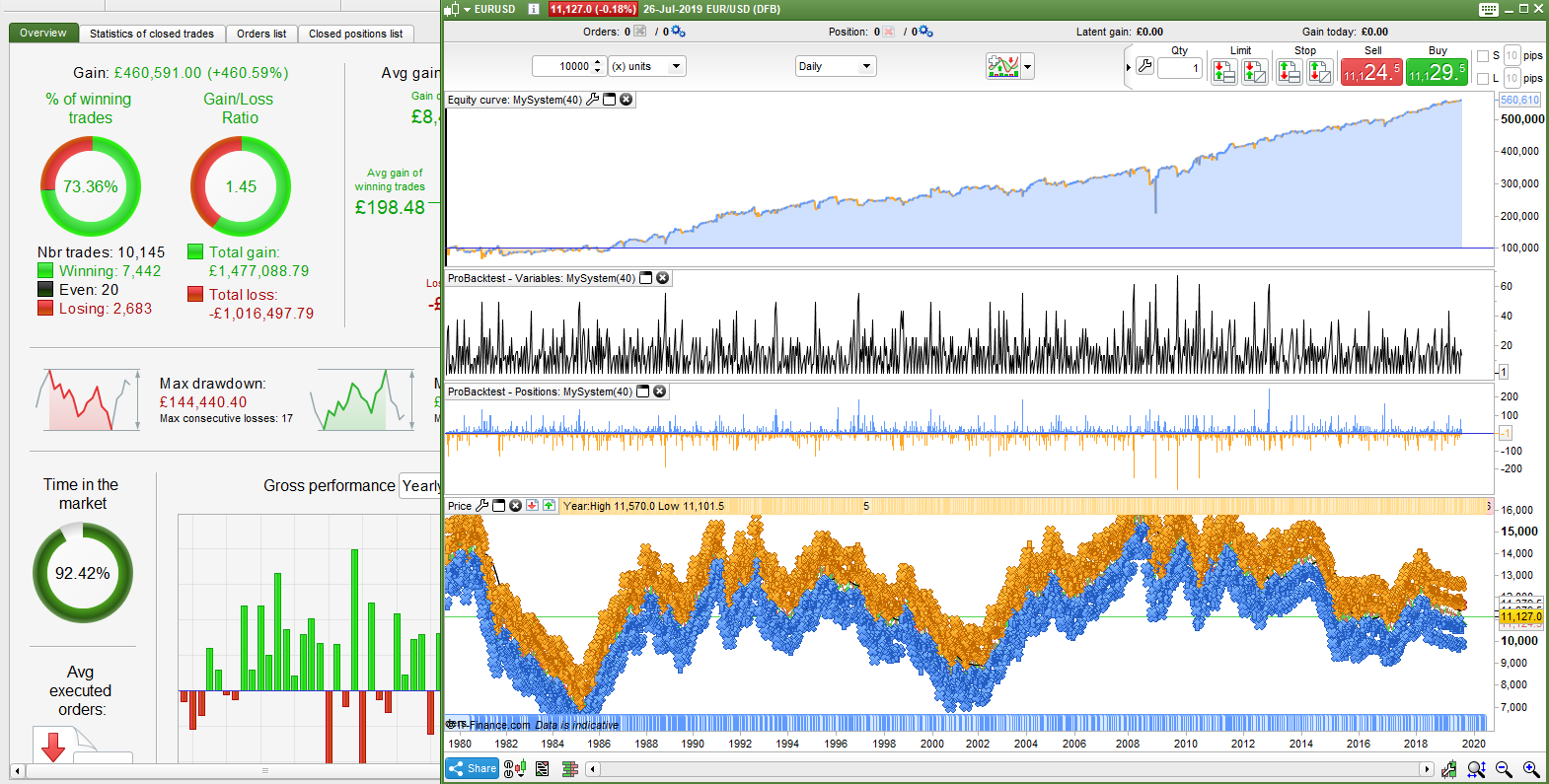

Please be aware that this was just an interesting experiment in the effects of adjusted market exposure based on trading performance and not a suggested way of going about trading – especially the averaging down with adjusted position sizing turned on – please see the very scary draw down in the second image as a warning!

Enter your own long and short conditions in lines 7 and 8.

AverageDown = 1 //0=Off 1=On Turn on or off averaging down

PositionSizing = 0 //0=Off 1=On Turn on or off position sizing

StartPositionSize = 1 //Starting Position Size

mind = 2 //Minimum candles on market

maxd = 6 //Maximum candles on market

LongConditions = (Your Long Conditions)

ShortConditions = (Your Short Conditions)

once d = mind

//exit if in profit

if longonmarket and close > positionprice then

sell at market

d = min(d + 1,maxd)//extend time allowed in market after a win

endif

if shortonmarket and close < positionprice then

exitshort at market

d = min(d + 1,maxd)//extend time allowed in market after a win

endif

//exit if time is up

if longonmarket and barindex - startindex = d then

sell at market

endif

if shortonmarket and barindex - startindex = d then

exitshort at market

endif

//Reset time allowed on market to minimum after a loss

if strategyprofit < strategyprofit[1] then

d = mind

endif

//Buy first long position

if not longonmarket and LongConditions then

positionsize = StartPositionSize

buy positionsize contract at market

startindex = barindex

endif

//Buy extra long position if in a loss and conditions met again

if longonmarket and LongConditions and close < positionprice and averagedown then

if positionsizing then

positionsize = positionsize + (startpositionsize * d)

endif

buy positionsize contract at market

endif

//Buy first short position

if not shortonmarket and ShortConditions then

positionsize = StartPositionSize

sellshort positionsize contract at market

startindex = barindex

endif

//Buy extra short position if in a loss and conditions met again

if shortonmarket and ShortConditions and close > positionprice and averagedown then

if positionsizing then

positionsize = positionsize + (startpositionsize * d)

endif

sellshort positionsize contract at market

endif

graph positionsize

Link to above added to below with the Comment ,,,

Concept more than a working strategy

Snippet Link Library

Paul

PaulParticipant

Master

Hi Vonasi, interesting code and perhaps it could be used on the vectorial dax strategy.

That strategy has a few issues, like

- long costly exposure in the market

- signals in the same direction are are ignored as long there is no exit criteria matched

Trying to understand the code I’am focussing on the second paragraph.

It’s also modified because the days had to be counted and not the bars on a 5min TF.

To the entry conditions I ‘ve add startday=0

// display days in market

if displaydim then

if (not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket))) then

count=0

endif

if not ( dayofweek=1 and hour <= 1) then

if onmarket then

if openday <> openday[1] then

count = count + 1

endif

endif

endif

graph count

endif

once testV=1

if testV then

//pp=(positionperf*100) (already in code above)

mind = 0 //Minimum days on market (counting days; first day is 0)

maxd = 6 //Maximum days on market

once d = mind

//exit if in profit

if count>0 and pp>1 then

if longonmarket then

sell at market

d = min(count+1,maxd) //extend time allowed in market after a win

endif

if shortonmarket then

exitshort at market

d = min(count+1,maxd) //extend time allowed in market after a win

endif

endif

//exit if time is up

if count>0 then

if longonmarket and count - startday = d then

sell at market

endif

if shortonmarket and count - startday = d then

exitshort at market

endif

endif

//Reset time allowed on market to minimum after a loss

if strategyprofit < strategyprofit[1] then

d = mind

endif

endif

Also changed positionprice to a positionperformance, otherwise it would get out too often. Hope its correctly coded, got to check it some more and try to expand it.

I’ve not really been following the Vectorial DAX in close detail so it is difficult for me to comment on this addition to it without going back over an awfully large number of posts to understand it all!

My first thought was why over complicate things. 1 day is 288 * 5 minute candles so when a trade is opened and you want to give it a minimum number of days on the market then just set minD to a multiple of 288 and maxD to a multiple of 288.

You would also need to change the line that increases the time in the market to add 288 candles on instead of just 1 candle:

d = min(d + 288,maxd)//extend time allowed in market after a win

Here is a stripped down version with the averaging down and position sizing removed and a step variable added for increasing the time in the market. Settings are for a 5 minute chart with minD of 2 days and MaxD of 6 days.

Not tested.

minD = 576 //Minimum candles on market

maxD = 1728 //Maximum candles on market

Dstep = 288

LongConditions = (Your Long Conditions)

ShortConditions = (Your Short Conditions)

once d = mind

//exit if in profit

if longonmarket and close > positionprice then

sell at market

d = min(d + Dstep,maxd)//extend time allowed in market after a win

endif

if shortonmarket and close < positionprice then

exitshort at market

d = min(d + Dstep,maxd)//extend time allowed in market after a win

endif

//exit if time is up

if longonmarket and barindex - startindex = d then

sell at market

endif

if shortonmarket and barindex - startindex = d then

exitshort at market

endif

//Reset time allowed on market to minimum after a loss

if strategyprofit < strategyprofit[1] then

d = mind

endif

//Buy first long position

if not longonmarket and LongConditions then

buy positionsize contract at market

startindex = barindex

endif

//Buy first short position

if not shortonmarket and ShortConditions then

sellshort positionsize contract at market

startindex = barindex

endif