@alco

Considering that I have other strategies I have shared the capital and devoted to this 400 euro.

In eur / usd does not work because when placing the order put +2 points above and -1 below, in the currency pairs move around 0’00001, ie, if the eur / usd puts close In 1’05123, when placing the order in +2, you are putting it in 3.05123, something that will never touch. In currency pairs you have to move with decimals.

en eur/usd no funciona porque al poner la orden la pones +2 puntos por encima y -1 por debajo, en los pares de divisas se mueven en torno a 0’00001, es decir, que si el eur/usd pone cierra en 1’05123, al poner la orden en +2, la estas poniendo en 3,05123, algo que nunca llegará a tocar. en los pares de divisas tienes q moverte con decimales.

Maybe we could use 1 hour bar candle and enter at the breakout of max or min of the last ten bars. What do you think?

Hi Guys

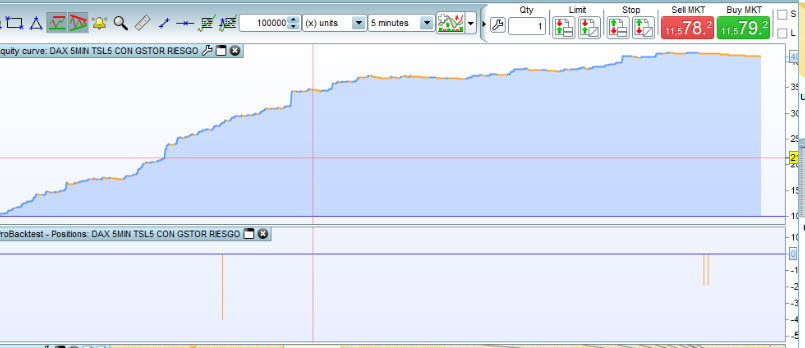

When I run Algo 5MIN TSL5 CON GSTOR RIESGO with tick-tick OFF I get zerobars, big profits, few losses and 40K overall profit (Capture 1 & 2 attached) .

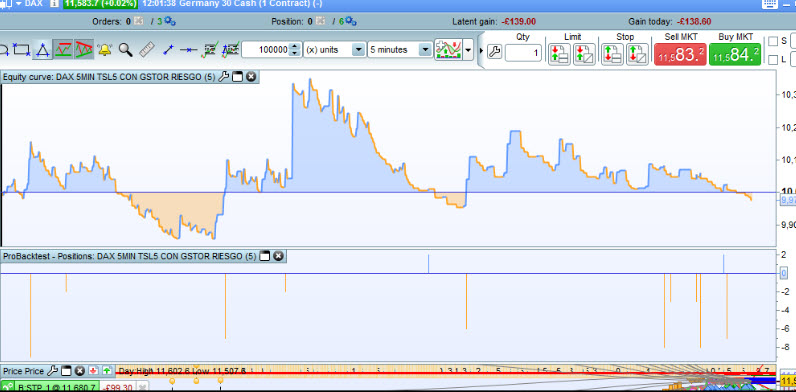

When I run Algo 5MIN TSL5 CON GSTOR RIESGO with tick-tick backtest ON I get zerobars, small profits, lots of small losses and £200 overall loss ((Capture 3 & 4 attached).

Are you sure you are using tick-tick optimise backtest correctly?

GraHal

Correction to above 1st paragraph should read … 30k overall profit

GraHal

Hi GraHal, Do you live in England, have you changed the time of entry? There is an hour less than in Spain.

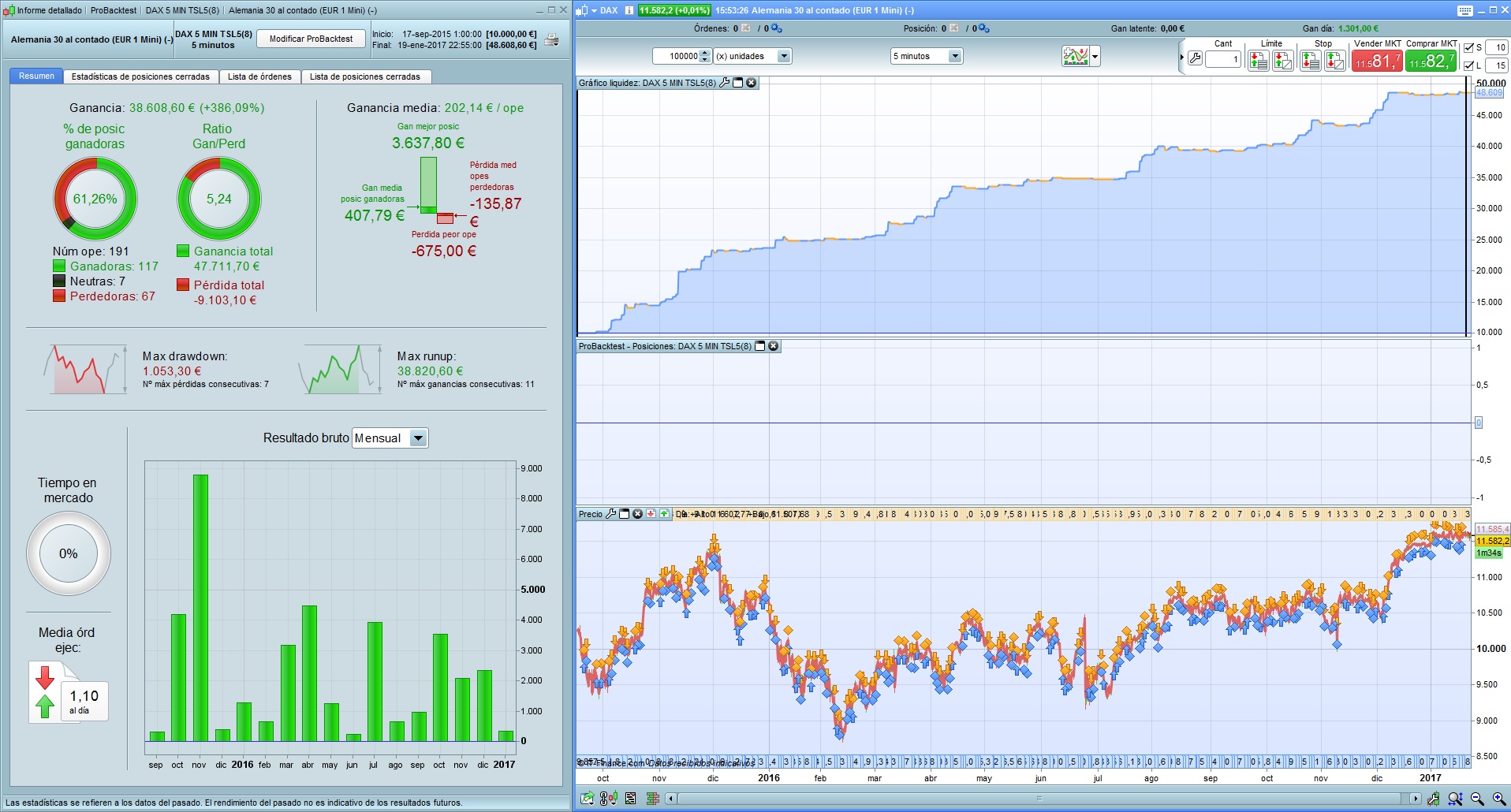

Hi guys, I have decided to try a new thing, to see that days of the week fail more and what days more correct.

For them I have done 5 different backtest, one for each day of the week, and as you can see in the attachments on Friday it fails a lot, and Thursdays are not very good either.

The last two catches with the program only operating from Monday to Wednesday and the other from Monday to Thursday, I decide to exclude Friday because it is the day that most fails.

I can not attach all the captures, these are here Monday, Tuesday, Wednesday and Thursday.

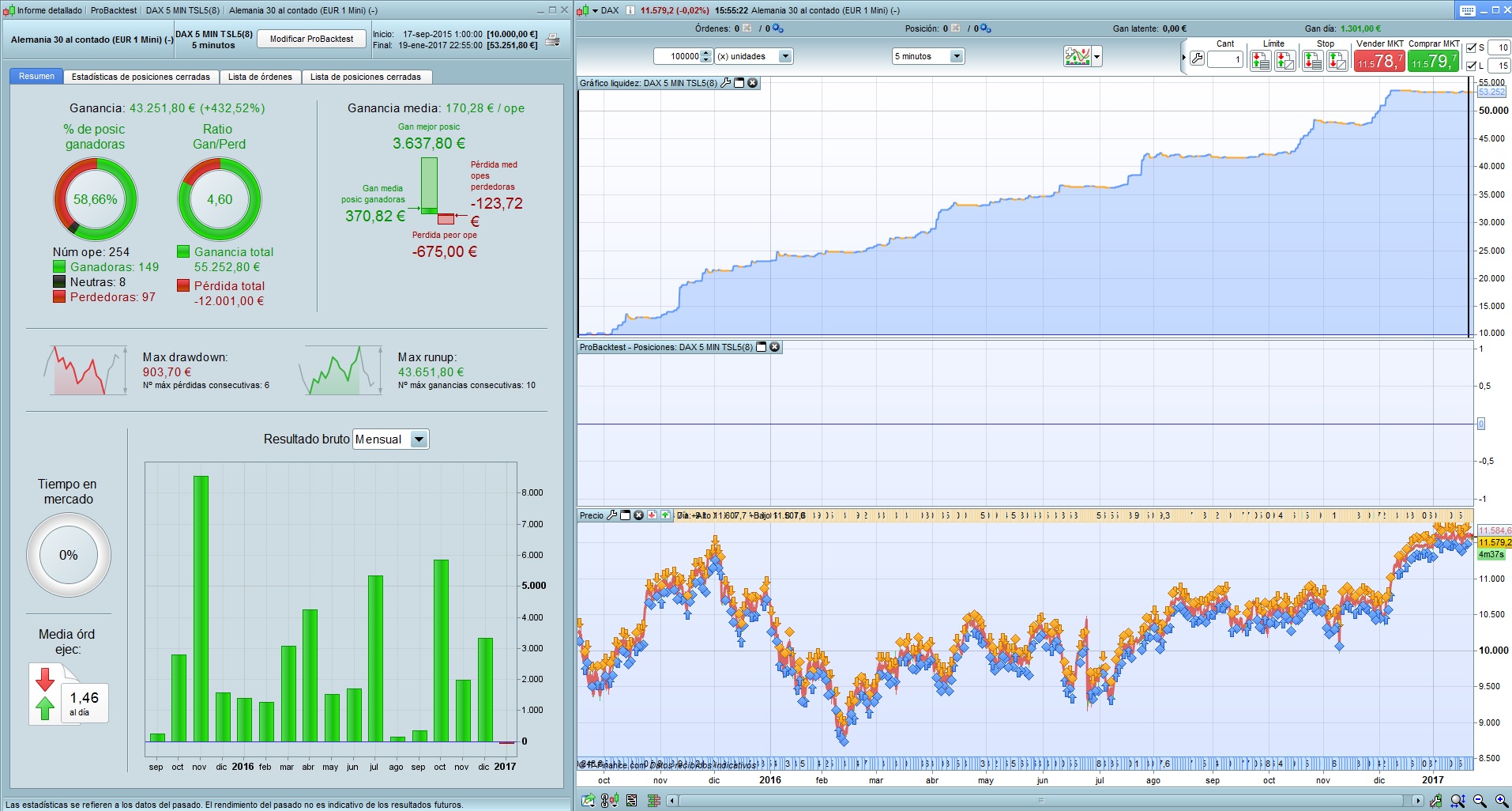

These catches are from Friday, and from the backtest from Monday to Wednesday and from Monday to Thursday

Nice Raul. Wold you like to post the code with the best profit?

Hi,

In demo today positive result on Wall Street cash….tonight I share the strategy for this instrument. I think to share my analisys of day trading that Raoul said. Yesterday I start this work that I think to finish tonigh. Tanks

Hi guys

I’ve been busy with my 1 year-old being sick and at home today. I see that there has been a lot of talk over the weekend and a few different versions of the code. I haven’t had chance to read and digest everything so I will be looking at an older version of the code. As I mentioned on Friday I had a very quick look at the Dow (5 min and also 10 min out of interest).

Product: Mini DJ30 Full0317 Future

5min: 200,000 bars goes back to April 2014.

10min: goes back to Sept 2012. I have tested from 2 Jan 2013.

I’ve had to be a bit more aggressive with the lot sizing to get reasonable returns which I think is OK with the Dow rather than the Dax. In particular I start off with 5 lots. Also increase order size by 3. I haven’t used the cool risk management / sizing toolthat is a new bit of code I have seen (I’m not sure I would use this in practice anyway as I think I would prefer to manually control this (other than the increase +3 or reducing /2) considering market volatility, performance of different strategies…etc). I’m also not using the ptrailing as we know that it is not reliable in live trading on IG so I therefore don’t want to test this. I’m keeping it simple still with fixed stop and target. I’m sure there are better results to be had out there.

Code for the 5 min is below. The code for 10 min bars is exactly the same just with different times.

I attach the results. Any comments welcome. As I said I have looked at this only very quickly but early results are promising.

I’m probably going to run both simultaneously in demo to compare.

I’m not going to be around for the rest of the day. Catch you guys tomorrow.

// Definition of parameters

DEFPARAM CumulateOrders = false // No accumulation of orders

// Position is closed at 9:00 p.m., local market time (London).

DEFPARAM FlatAfter =205900

Once Ordersize=1

// Start time (calculation at end of 143000 bar)

StartTime = 143500

// Only 1 position per day

EndTime = 143900

// Max orders & risk multiplier

//Margin = 60

//Lottfree = 0

//OrderSize = max(1,1+ROUND((strategyprofit-lottfree)/Margin))

//Ordersize=min(35,Ordersize)

If Ordersize > 35 THEN

Ordersize = 35

Endif

n=1

// Conditions for analysis

If Time >= StartTime and time <= EndTime THEN

If not onmarket then

c1 = open < close-2*pointsize

c2= open > close-1*pointsize

IF PositionPerf(1) < 0 THEN

OrderSize = OrderSize/2 // -2

ELSIF PositionPerf(1)> 0 THEN

OrderSize =OrderSize+3

Endif

Ordersize=max(Ordersize,5)

// Conditions to enter positions

IF c1 THEN

buy Ordersize*n contract AT close+2 stop

endif

IF c2 THEN

sellshort Ordersize*n contract AT close-1 stop

Endif

Endif

Endif

//Stops & target

SET STOP ploss 6 //5 3

SET TARGET pPROFIT 14 //10 12

jonjon, I hope your son gets better soon

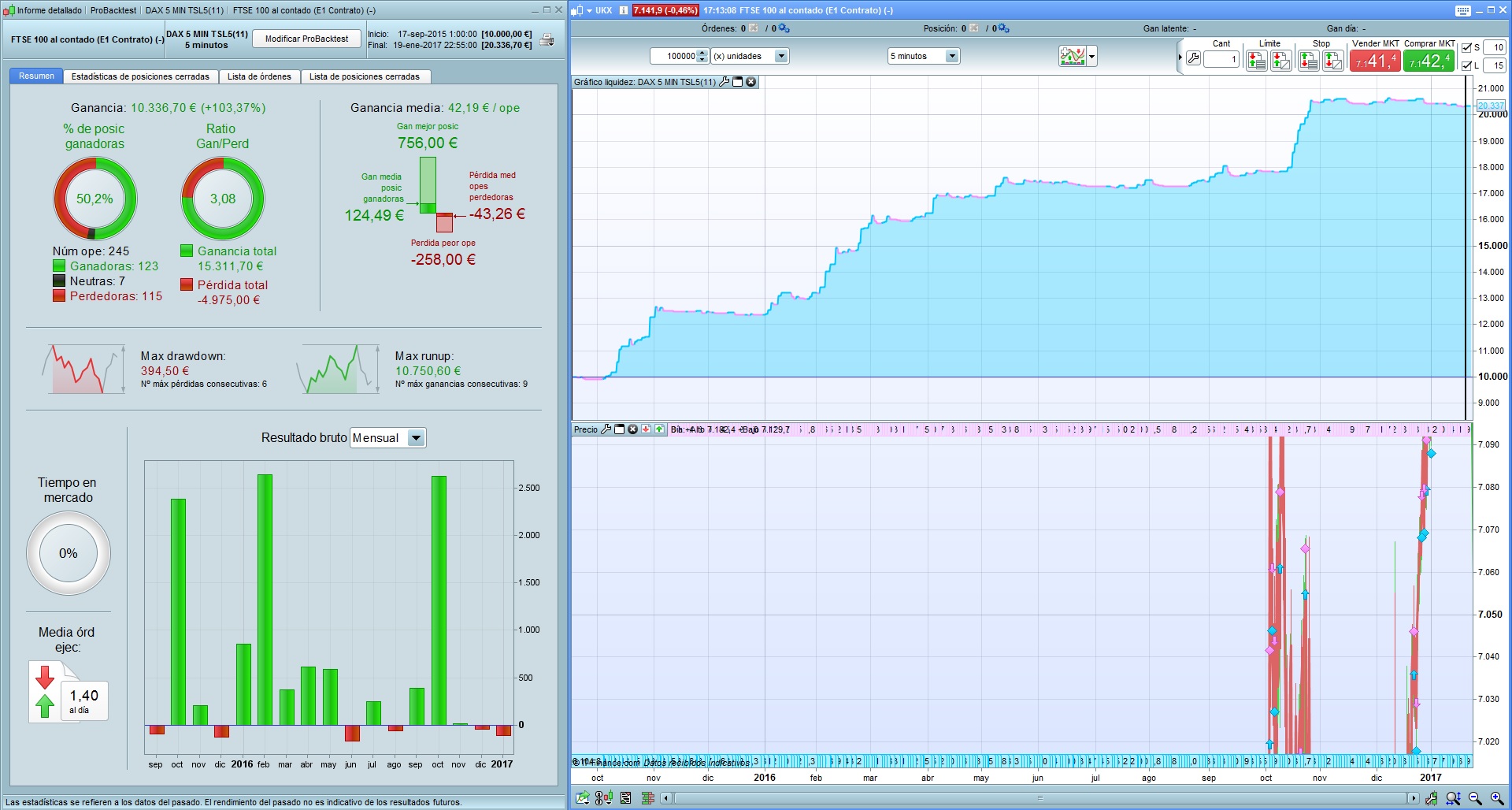

This is the backtest adapted for the FSTE 100,It is not as good as in the DAX, although it is quite positive, I find it very attractive, it needs to be touched up a bit

// Definición de los parámetros del código

DEFPARAM CumulateOrders = false // Acumulación de posiciones desactivada

DEFPARAM FlatAfter =173000

once ordersize=1

HoraEntradaLimite = 090600

HoraInicio = 090500

if Ordersize>40 then

Ordersize=30

endif

if dayofweek=1 then

daytrading=1

endif

if dayofweek=2 then

daytrading=1

endif

if dayofweek=3 then

daytrading=1

endif

if dayofweek=4 then

daytrading=1

endif

if dayofweek=5 then

daytrading=0

endif

n=3

if Time >= HoraInicio and time <= HoraEntradaLimite and daytrading= 1 then

c1 = open < close-2

if not onmarket then

IF c1 THEN

IF PositionPerf(1) < 0 THEN

OrderSize = OrderSize/2

if ordersize<1 then

ordersize=1

ENDIF

ELSIF PositionPerf(1) > 0 THEN

OrderSize =OrderSize+5

if ordersize<1 then

ordersize=1

ENDIF

endif

buy ordersize*n contract AT close+2 stop

endif

c2= open > close-2

IF c2 THEN

iF PositionPerf(1) < 0 THEN

OrderSize = OrderSize/2

if ordersize<1 then

ordersize=1

ENDIF

ELSIF PositionPerf(1) > 0 THEN

OrderSize =OrderSize+5

if ordersize<1 then

ordersize=1

endif

ENDIF

sellshort ordersize*n contract AT close-1 stop

endif

endif

endif

SET STOP ptrailing 2

Could you be so kind to try this code on the dax? Remember that you have it at 25 euros per point, if it stays at 0 increase the initial money, thanks.

// Definición de los parámetros del código

DEFPARAM CumulateOrders = false // Acumulación de posiciones desactivada

DEFPARAM FlatAfter =173000

once ordersize=1

HoraEntradaLimite = 090600

HoraInicio = 090500

if Ordersize>40 then

Ordersize=30

endif

if dayofweek=1 then

daytrading=1

endif

if dayofweek=2 then

daytrading=1

endif

if dayofweek=3 then

daytrading=1

endif

if dayofweek=4 then

daytrading=1

endif

if dayofweek=5 then

daytrading=0

endif

n=1

if Time >= HoraInicio and time <= HoraEntradaLimite and daytrading= 1 then

c1 = open < close-2

if not onmarket then

IF c1 THEN

IF PositionPerf(1) < 0 THEN

OrderSize = OrderSize/2

if ordersize<1 then

ordersize=1

ENDIF

ELSIF PositionPerf(1) > 0 THEN

OrderSize =OrderSize+5

if ordersize<1 then

ordersize=1

ENDIF

endif

buy ordersize*n contract AT close+2 stop

endif

c2= open > close-1

IF c2 THEN

iF PositionPerf(1) < 0 THEN

OrderSize = OrderSize/2

if ordersize<1 then

ordersize=1

ENDIF

ELSIF PositionPerf(1) > 0 THEN

OrderSize =OrderSize+5

if ordersize<1 then

ordersize=1

endif

ENDIF

sellshort ordersize*n contract AT close-1 stop

endif

endif

endif

SET STOP ptrailing 5

The above message is for jonjon try it with 200,000 bars

Good evening.

You must respect the stop distances.

On Down Jones: stop minimun 9 points.

If you do not set the correct stop distance, warning.

The program is open without stop protection.

The distance of the stop and stop trailings is also different for the same index.