hello

just a question.

Why did you put a stop trailing in a strategy of 1 mn.(the must of case) when we know that the trailing moove every 5 mn (timeframe)?

TAKE CARE

with the backtest, it”s not reality even with v10.3 tick by tick.

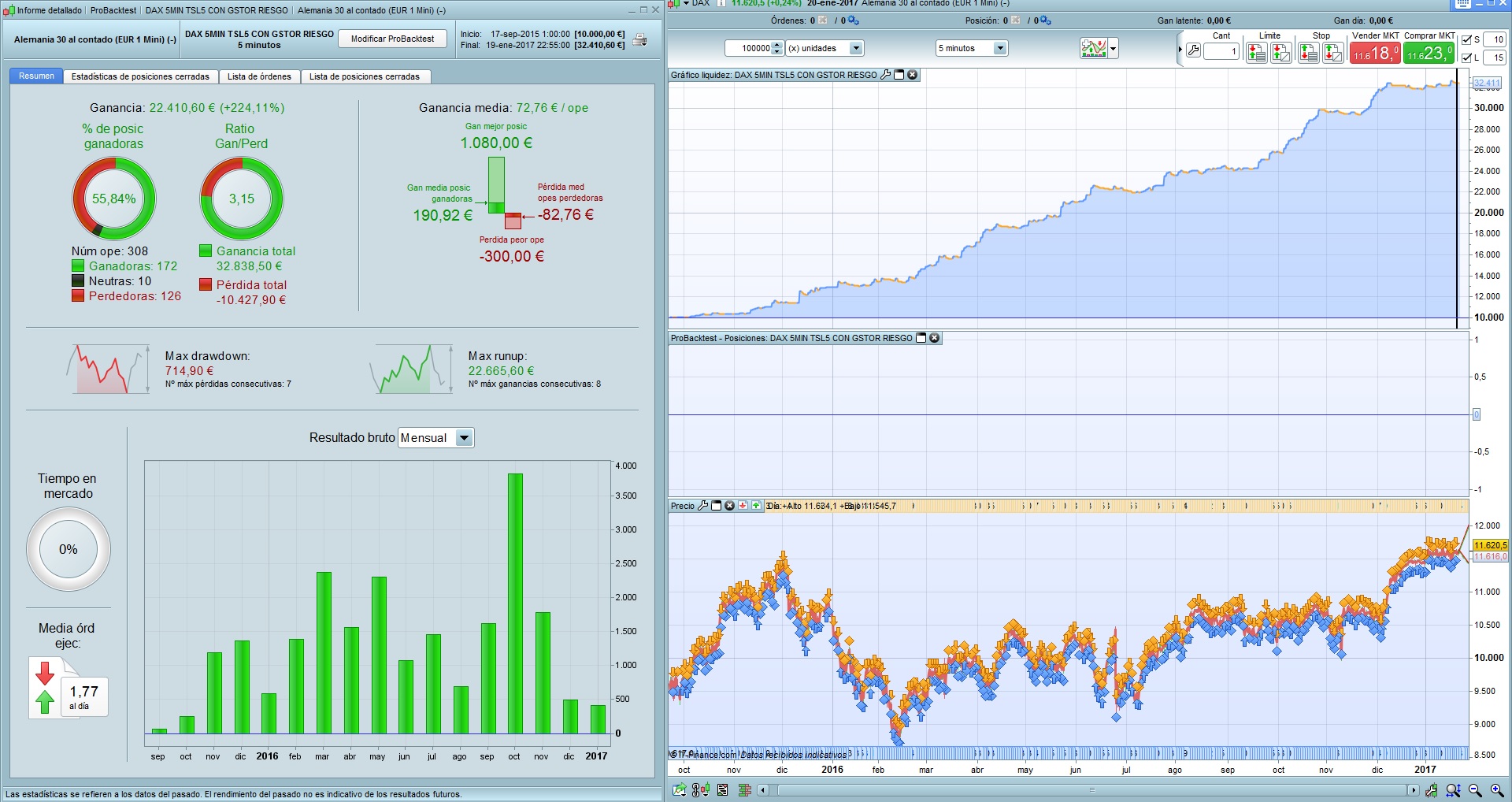

exemple the 20 january.backtest v10.3 tick by tick give a win about 258.50 euros and rhe reality it’s a lost 5 points.it’s the case of “0 BAR”.

I prefer to stay with the original version..5-10

t-y

An example:

At 600 euros profit, it uses 10 contracts.

We can lose 10 contracts * 5 points = 50 euros

8.4% of profits.

But if we have 15,000 euros profit, it uses 38 contracts.

We can lose 38 * 5 = 190 euros

A 1.26% of profits.

Do not you think it would be better to take less risk in the beginning?

Hi larouedegann.

Actually, to me live on Friday I was left at 0 euros the operation, it depends on the speed of execution of the platform, on the backtest it has won. I believe that in the long term it is more useful to use trailing since if you lose, you lose 5 equal, but to win you can win more than 10. you have to keep in mind that it will not always be as fast as this Friday. Another option is the last one I sent that is to change the take by 5 and the stop by 10, in reverse that at the beginning

@Raul

Sorry if you already explained it somewhere else, but why do the c1 and c2 conditions are different? 1 or 2 points differences between Open/Close should be the same isn’t it? Or did I miss something here?

Good question nicolas, I tried to optimize it and I got the best result. In case the first bar of 5 minutes is positive, puts a purchase order 2 points above the closing, and in the case that is negative, puts a purchase operation 1 point below the closing. I have tried different configurations, but the best comes out. You can try to put +2 and -2 or +1 or -1

CN

CNParticipant

Senior

@everyone

So which strategy is the best optimized for livetrading from all of them posted?

@CN

There are several versions, that depends on the risk that each one wants to assume, all are based on the same inputs and outputs, the only thing that changes is the way to add or subtract contracts. Except one you change the by 5 and the stop by 10. The attached:

@Raul

hi,

your opinion it’s correct but in thsi I prefer use my version that start with 0ne lot. If you see in my strategy there is a variable called “Lottfree” that now is equal to 0. If the strategy makes money and for example reach 2250 I can valorized it with -2250 and I can change the version and I can value to use your version in order to minimized the risk like you have said. In this moment for me is important to start with 1 lot.

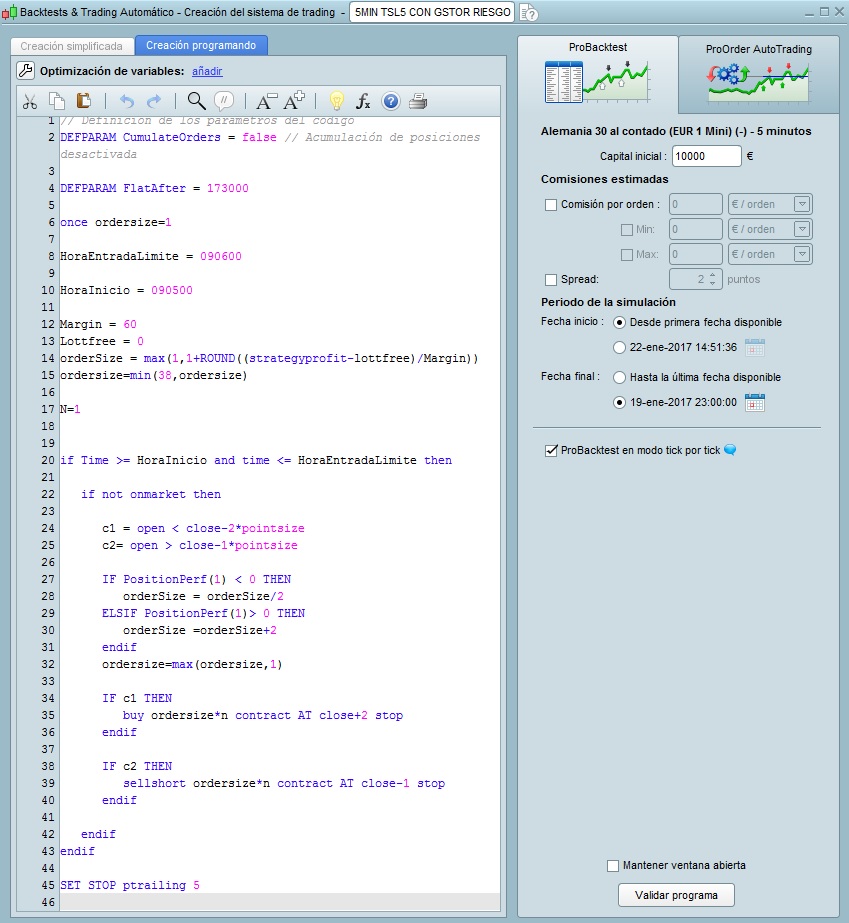

I’m starting tomorrow with the version below.

// Definición de los parámetros del código

DEFPARAM CumulateOrders = false // Acumulación de posiciones desactivada

// La posición se cierra a las 17:29 p.m. si no toca ni stop ni take.

DEFPARAM FlatAfter =173000

once ordersize=1

HoraEntradaLimite = 090600

HoraInicio = 090500

Margin = 60

Lottfree = 0

orderSize = max(1,1+ROUND((strategyprofit-lottfree)/Margin))

ordersize=min(38,ordersize)

n=1

if Time >= HoraInicio and time <= HoraEntradaLimite then

if not onmarket then

c1 = open < close-2*pointsize

c2= open > close-1*pointsize

IF c1 THEN

buy ordersize*n contract AT close+2 stop

endif

IF c2 THEN

sellshort ordersize*n contract AT close-1 stop

endif

endif

endif

SET STOP ptrailing 5

CNParticipant

Senior

@Raul,

Thanks for the explanation! What are the diff on the strats posted?

@volpiemanuele

Ok, had not taken into account the lottfree variable. Let’s see if there’s any luck and we’ll chain some winning days soon!

@CN

The first is the “original”, has a trailing stop of 5 points and accumulates contracts as you hit and divide between 2 if it fails.

The second, has the risk manager @volpiemanuele and also the same summation as the first, that is, has 2 variables for which adds and subtracts contracts.

The third, only has the risk manager @volpiemanuele.

The fourth changes the trailing by a normal stop, stop 10 and take 5, the number of hits improves considerably, but the ratio wins / lost worsens.

It is missing that @jonjon try with 200,000 bars the latter.

Hi Guys

Please forgive me if I am missing something here (as usual :)) I ran the SL5 CON GSTOR RIESGO Algo (see list of 4 Algos above) and with tick-tick backtest OFF … I got numerous zerobars and results showed + £34K PROFIT over 100,000 bars on DAX 5 Min TF.

Run same Algo over 100,000 5M bars with tick-tick backtest ON and I get Minus / – £2K LOSS. Also the equity curve rarely even gets above my starting capital … see attached.

The second equity curve shown on attached is the most recent pasted version above run with 1 Lot … similar results.

Feel free to say … you’ve f****d up big style Gra … what you should be doing is this …. ??

Thanks

GraHal

Hi GraHal,

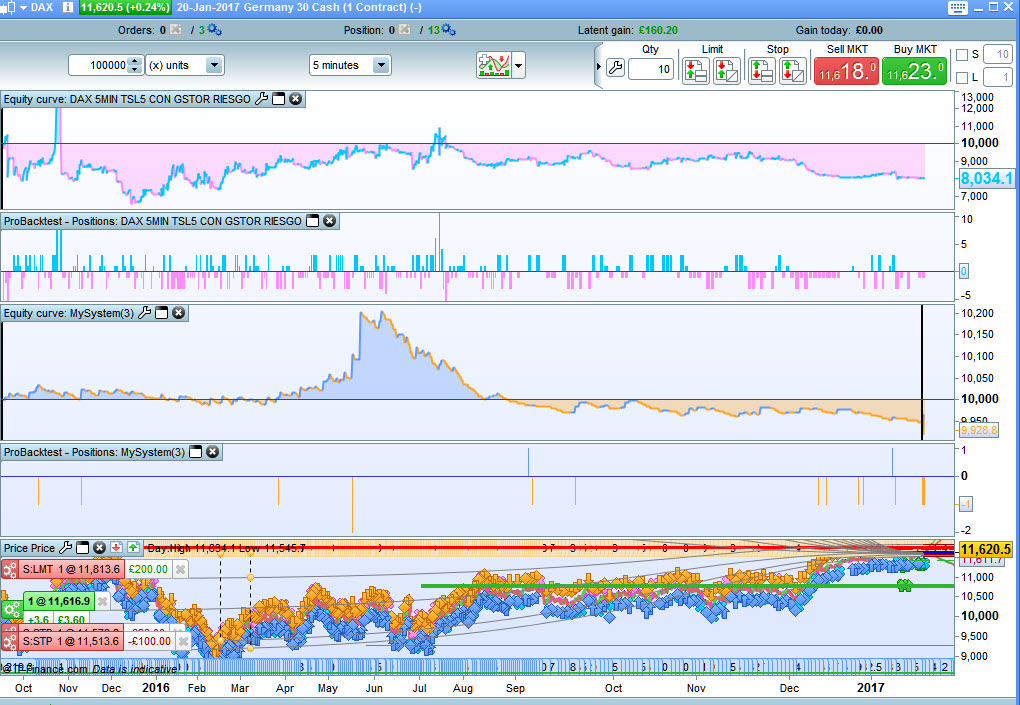

Something has to fail you, attached the backtest tick by tick and spread 1. (photos 1 and 2)

I see you have many positions open for a long time, something is wrong there. (Photo3) on my backtest close at the moment (foto4)

Alco

AlcoParticipant

Senior

@GraHal

Maybe you need to change the time. We have 1 hour difference.