Took the last code from this post: https://www.prorealcode.com/topic/5-min-mini1e-dax-spread-1/page/3/#post-21815

Modified the code to be lightweight with only useful code, don’t know if it’s the last version, but this kind of coding should be used in your future development, to gain some time while backtesting:

// Definición de los parámetros del código

DEFPARAM CumulateOrders = false // Acumulación de posiciones desactivada

DEFPARAM FlatAfter = 173000

once ordersize=1

HoraEntradaLimite = 090600

HoraInicio = 090500

Margin = 60

Lottfree = 0

orderSize = max(1,1+ROUND((strategyprofit-lottfree)/Margin))

ordersize=min(18,ordersize)

n=1

if Time >= HoraInicio and time <= HoraEntradaLimite then

if not onmarket then

c1 = open < close-2*pointsize

c2= open > close-1*pointsize

IF PositionPerf(1) < 0 THEN

OrderSize = OrderSize/2

ELSIF PositionPerf(1)> 0 THEN

OrderSize =OrderSize+2

endif

ordersize=max(ordersize,1)

IF c1 THEN

buy ordersize*n contract AT close+2 stop

endif

IF c2 THEN

sellshort ordersize*n contract AT close-1 stop

endif

endif

endif

SET STOP ptrailing 5

Alco

AlcoParticipant

Senior

@jonjon

Dow has a minimum 9 pip SL.

AlcoParticipant

Senior

@jonjon

Oh wait, sorry I got it wrong. It has a minimum 9 pip SL before opening. After opening it has a minimum of 6 pip SL.

@Alco. That sounds better. I’ll try getting the data. I actually trade the Dow anyway (I’m currently trading through X_Trader and chart through eSignal). The equivalent contract on PRT to what I trade is the Mini DJ30 Full0317 Future. Hopefully this is similar to the prices you get.

I’ll let you know how it goes.

BC

BCParticipant

Master

Hi Nicolas

Is it possible Live trade with “ptrailing” function with V10.2?

Thanks

@Bin

Yes of course, the reason why people are complaining about it, is about the lack of reliability into backtest in version pre 10.2 and the “0 bar” phenomena.

Hello guys,

First of all, Grandisimo trabajo Raul,

Next…

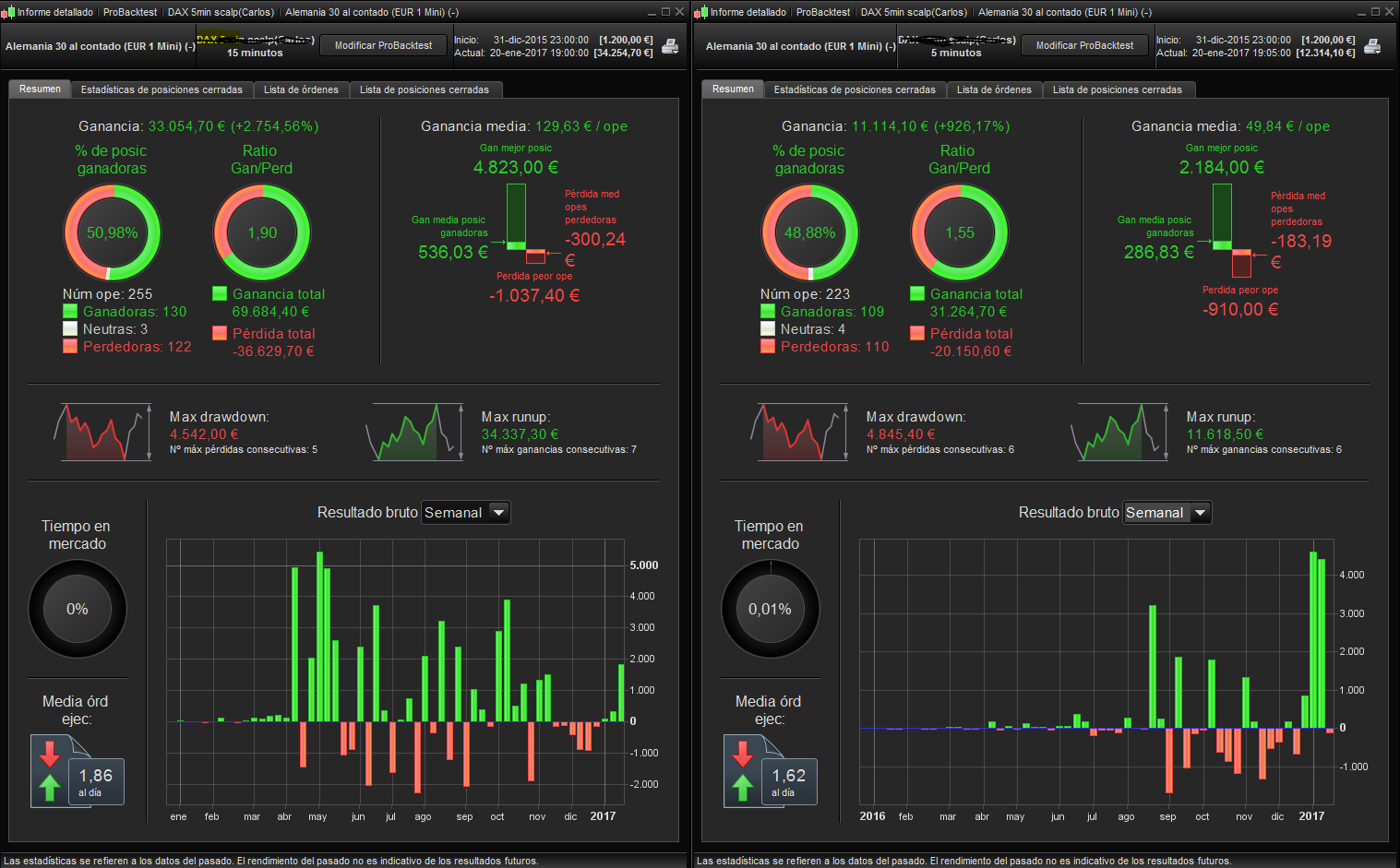

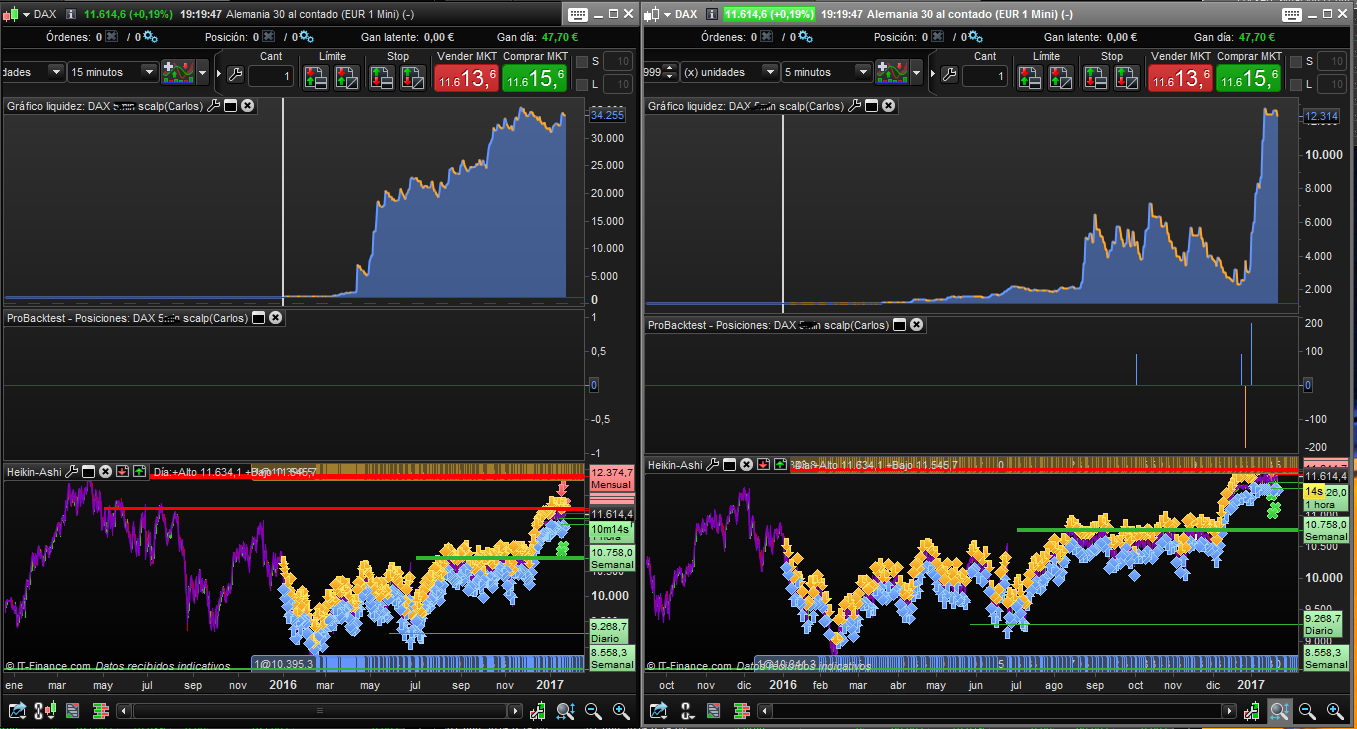

This is only an idea, I tried the strategy in 15 minutes timeframe, only changing some data (attach shot3). I have compared the both timeframe in the last year (small backtest) and the results were sightly diferent.

I changed the code to start both system with only one contract for really small accounts (sadly my case)

As you can see, the drawdown is very similar but gains not

So, what’s your opinion

HappyTrading

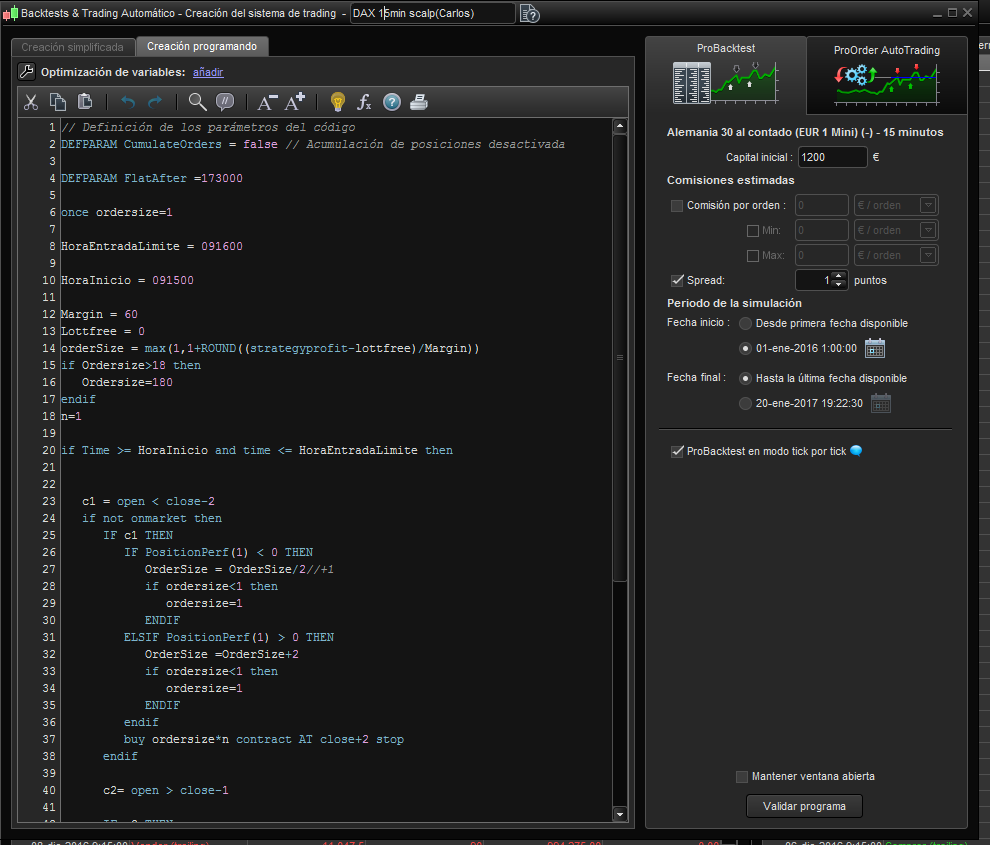

// Definición de los parámetros del código

DEFPARAM CumulateOrders = false // Acumulación de posiciones desactivada

DEFPARAM FlatAfter =173000

once ordersize=1

HoraEntradaLimite = 091600

HoraInicio = 091500

Margin = 60

Lottfree = 0

orderSize = max(1,1+ROUND((strategyprofit-lottfree)/Margin))

if Ordersize>18 then

Ordersize=180

endif

n=1

if Time >= HoraInicio and time <= HoraEntradaLimite then

c1 = open < close-2

if not onmarket then

IF c1 THEN

IF PositionPerf(1) < 0 THEN

OrderSize = OrderSize/2//+1

if ordersize<1 then

ordersize=1

ENDIF

ELSIF PositionPerf(1) > 0 THEN

OrderSize =OrderSize+2

if ordersize<1 then

ordersize=1

ENDIF

endif

buy ordersize*n contract AT close+2 stop

endif

c2= open > close-1

IF c2 THEN

iF PositionPerf(1) < 0 THEN

OrderSize = OrderSize/2//+1

if ordersize<1 then

ordersize=1

ENDIF

ELSIF PositionPerf(1) > 0 THEN

OrderSize =OrderSize+2

if ordersize<1 then

ordersize=1

endif

ENDIF

sellshort ordersize*n contract AT close-1 stop

endif

endif

endif

SET STOP ptrailing 5

Jonjon, Could you pass the backtest from the day of June 2014 that gives you the error until today? Counting that you have it in the dax of 25 € per point, it would have to divide everything between 25.

Hi Carlos, thank you very much, I see in your backtest a benefits curve that is not very attractive and an excessive max drawdown, for example, for the last robot that I have shared the max drawdown is half and profits more than double

The gain / loss ratio is practically half

Thanks for the comment, what capital do you think is the best to start in live account. I would like to get code to start with 2000€ of capital and trying to asuming a real risk

Saludos de Madrid.

Raul – here you go. Your previous code exactly as it was with a trailing stop of 5. Problem seems to be with the data around end June & July 2014. The backtest here is from 1 Aug 2014 until 30 Dec 2016.

Have a good weekend guys. Catch you Monday

@carlos

With the same strategy you are waiting 3 times longer (3 bars of 5 minutes in a 15 minutes timeframe) to place and move stoploss with the trailing stop. As you may already know it, nothing happens between 2 bars in probacktest.

Hi jonjon, Many thanks for your time and for helping me, there is one thing that bothers me, and is that in my backtest of a year and a half earns 33,000euros, and in yours 2 and a half years with a very good profit curve earns 600,000 / 25 = 24,000 euros. I do not understand how it can be so

Hi,

at this time, for me, the best code is this. I have modified the code posted from nicolas in relation to position size leaving only my position size and optimizing the best position trade in max 38 lots. Thanks

// Definición de los parámetros del código

DEFPARAM CumulateOrders = false // Acumulación de posiciones desactivada

// La posición se cierra a las 17:29 p.m. si no toca ni stop ni take.

DEFPARAM FlatAfter =173000

once ordersize=1

HoraEntradaLimite = 090600

HoraInicio = 090500

Margin = 60

Lottfree = 0

orderSize = max(1,1+ROUND((strategyprofit-lottfree)/Margin))

ordersize=min(38,ordersize)

n=1

if Time >= HoraInicio and time <= HoraEntradaLimite then

if not onmarket then

c1 = open < close-2*pointsize

c2= open > close-1*pointsize

IF c1 THEN

buy ordersize*n contract AT close+2 stop

endif

IF c2 THEN

sellshort ordersize*n contract AT close-1 stop

endif

endif

endif

SET STOP ptrailing 5

Thanks