It seems to perform better, but it opens very few trades and the best performance is on the weekly TF!

and the best performance is on the weekly TF!

Nothing wrong with a weekly time frame – most of my best strategies work on the weekly time frame. You get to see the bigger picture and the trades have plenty of room to do their thing.

It seems to perform better, but it opens very few trades and the best performance is on the weekly TF!

Yeah as Vonaso said, ABCD values are 46 60 25 120 for the 2 min TF.

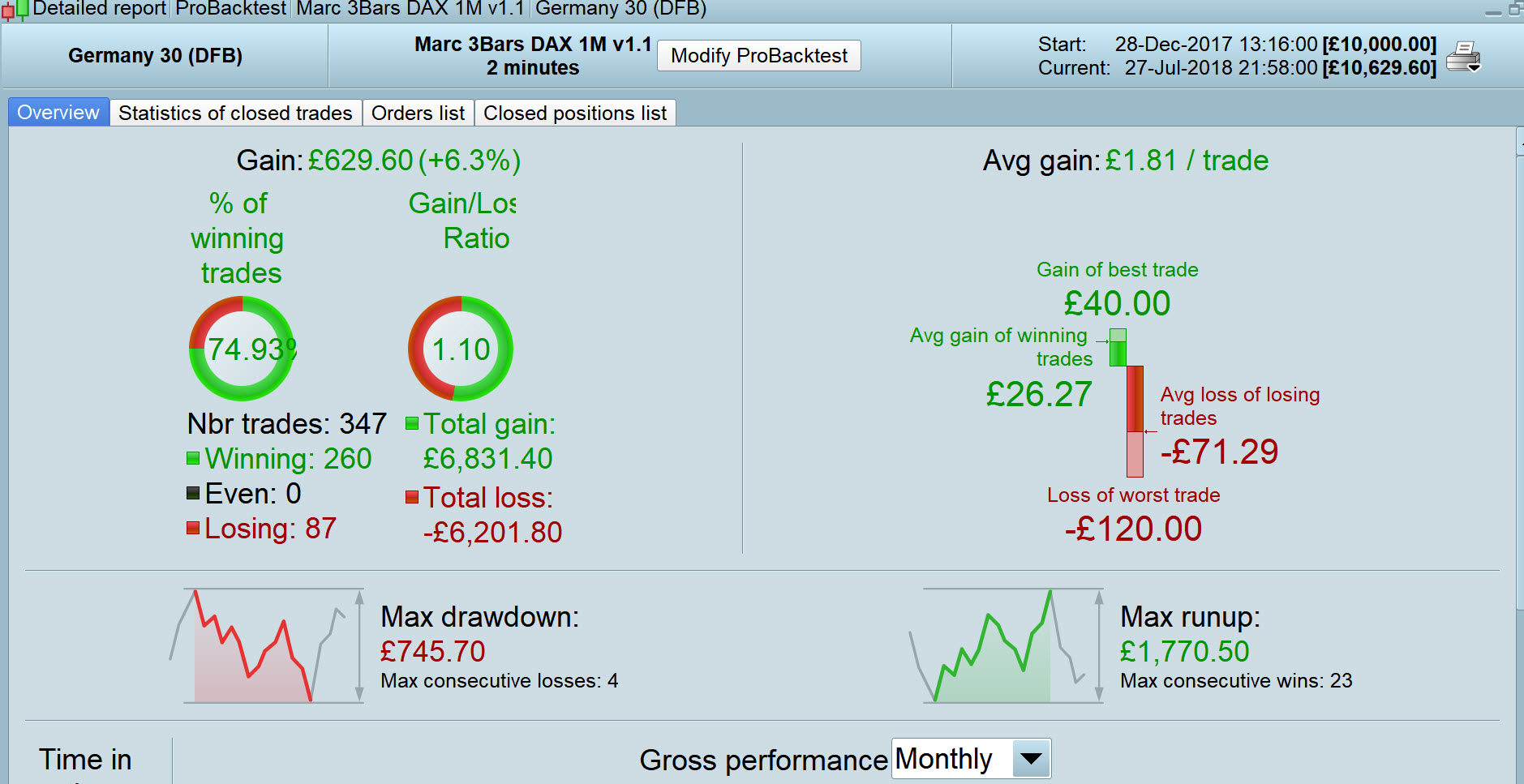

On my backtest the above shows 347 trades since Jan 18 … see attached. Results are with spread = 2.

HI Roberto,

Just a quick question. I saw that you have looked through Marc’s code and said it was all good. However I just wanted to ask confirm a query. In Marc’s code he uses “NextBarOpen” for his market order. Is they anyway to have a market order execute instantaneously as soon as a condition is met ?

Kind Regards,

Simone

I just answered your question in the other topic about MTF.

Marc

MarcParticipant

Average

Hi together,

1st of all thank you very much for your interest and help regarding this system. If I see this correct this system gains profit with a lot of smaller winners, but on the other hand there are some bigger losers.

I’m going to check other possibilities to trade this system more profitable.

When I trade this system during the day (excl. night and early in the morning) it worked well and I was very satisfied with it.

If somebody has a nice idea how to improve please let me and the forum know 🙂

MarcParticipant

Average

Ho together,

I amended the code and it look very good, when searching through different UL’s the backtests become more and more horrible compared to performance before…1st I made some profits and later on when starting Backtest again the gains were negative

when searching through different UL’s

excuse my ignorance please, what is UL’s ? 🙂

amended the code and it look very good,

Why not leave it looking good then? I don’t understand what you are saying?

Did you try my version code? Maybe you not like the 2 min TF, but it does look profitable on 100k bars anyway!? 😉

MarcParticipant

Average

Hi GraHal,

with UL I mean Underlyings sry for using this acronym.

I tested the strategy or some different periods and everytime I tested it with the same period the result became more worse 🙁

MarcParticipant

Average

Hi GraHal,

why did you chose this values?

Rgds

Marc

why did you chose this values?

when you say values, I take it you mean the 2 min TF?

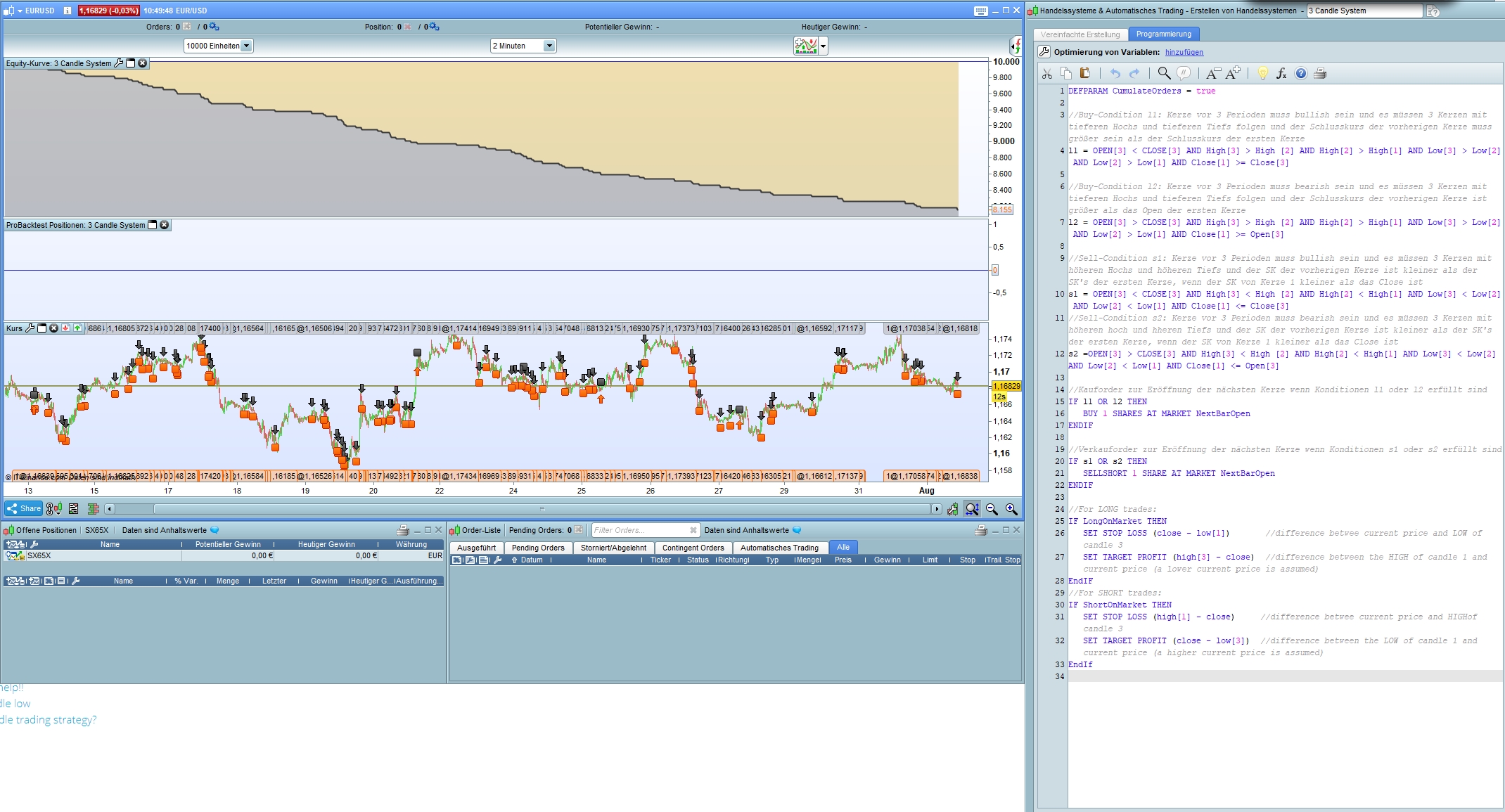

I chose 2 min TF because out of all the intraday TFs the 2 min gave the best equity curve without any optimising. Then I optimised for 2 min TF.

My logic was that the 3 candle strategy must have a better natural affinity for 2 min TF than other TFs. It may just be coincidence of course, but one has to go forward with something else we just go round in circles?? 🙂

everytime I tested it with the same period the result became more worse

If I understand correct what you are saying, I have had this many times … try closing your Platform, open again and carry on where you left off … let us know if results are any better etc?

MarcParticipant

Average

Hi GraHal,

I meant the TP and SL Values…please find attacehd a sample test with TF 2 minutes

With what TP and SL values is your Test?

Have you tried the TP and SL values I show in my 2 min version??

Also your Test is shown as being on EURUSD whereas my results are on the DAX! 🙂

MarcParticipant

Average

Not yet, let me check and I will post results

MarcParticipant

Average

Hi together,

pls find attached a file which shows a trade today in 2 Min TF and “original” settings. I’m wondering that this trade ended in a loss. Perhaps the spread of EURUSD was to big?!

But I can see also that this trade is not correct, because the candles aren’t in right concatentation.