Thanks Francesco78 for sharing the update on that strategy one year after. Would it be possible to post the performance report so that we can all see easily how the OOS compares to the IS performance wise?

So that ‘USDJPY 3candles and reversal strategy with ADX and VOL filter’ strategy looks quite promising and has worked similar OOS to IS. The gain/loss ratio has dropped a little but the win rate is very similar. Time in market has increased a bit.

Drawdown is pretty massive for a short time frame strategy both IS and OOS – so it may be one only for those with quite deep pockets!

Thanks Francesco for the repost of the code on USD/JPY, unfortunatly it still doesn’t work on my platform, and no solution have been found if I read the thread… It would be great if someone had a new idea of the cause of the problem. No position opens, and when I reduce the ATR to 0.1, it takes only one position, but loose all the capital at this first position…

Hello,

Since a few month, I’m running live a strategy developed initially by ALE and edited by CKW:

Fractal breakout intraday Strategy EUR/USD 1H –

Not a lot of trades recently, but working well.

Attached the live results on my real account

Since a few month, I’m running live a strategy developed initially by ALE and edited by CKW: https://www.prorealcode.com/topic/fractal-breakout-intraday-strategy-eurusd-1h/page/16/

Thanks for posting that @stefou102 – not quite a year after but the results over seven months look promising 🙂

As always with strategies that place just a few trades it is quite slow to get forward testing results and so difficult to build absolute confidence in the strategy. One to keep watching though.

It would be interesting to compare your results with the backtest results when the strategy was first posted.

I confirm backtest is inline with live since October.

I have confidence in the strategy also because strategy win rates is very consistent year over year, also on 200k bar backtest

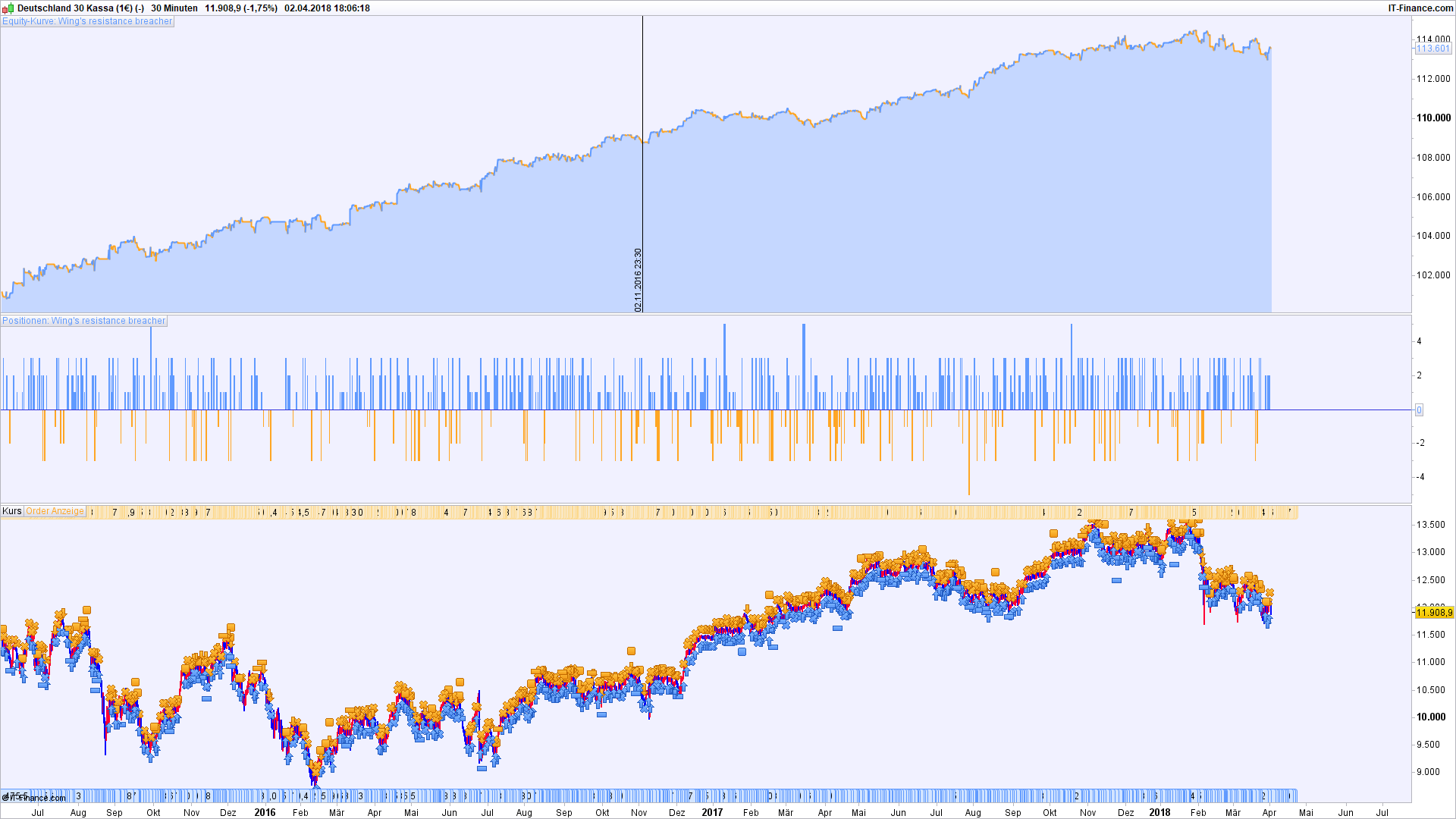

Wing’s resistance breacher has been quite good since November 2016.

Wing’s Resistance Breacher (DAX-30m)

Without position sizing (position size = 1, all the time) , it made about 2300 DAX points since then – not bad at all.

CKW

CKWParticipant

Veteran

Since a few month, I’m running live a strategy developed initially by ALE and edited by CKW: https://www.prorealcode.com/topic/fractal-breakout-intraday-strategy-eurusd-1h/page/16/

Thanks for posting that @stefou102 – not quite a year after but the results over seven months look promising 🙂

As always with strategies that place just a few trades it is quite slow to get forward testing results and so difficult to build absolute confidence in the strategy. One to keep watching though.

It would be interesting to compare your results with the backtest results when the strategy was first posted.

I am also continue running this since Jul’17, result so far so good.

Wing’s resistance breacher has been quite good since November 2016. https://www.prorealcode.com/prorealtime-trading-strategies/wings-resistance-breacher-dax-30m/ Without position sizing (position size = 1, all the time) , it made about 2300 DAX points since then – not bad at all.

From my quick check of this strategy it does seem that the position sizing adds nothing – in fact the gain/loss ratio is slightly improved without it over my test period

With a simple 70/30 IS/OOS walk forward it appears that the OOS has outperformed the IS which is not usually the case if something is over optimized.

Overall this may be one to watch (without position sizing though I think).

Wing’s resistance breacher has been quite good since November 2016. https://www.prorealcode.com/prorealtime-trading-strategies/wings-resistance-breacher-dax-30m/ Without position sizing (position size = 1, all the time) , it made about 2300 DAX points since then – not bad at all.

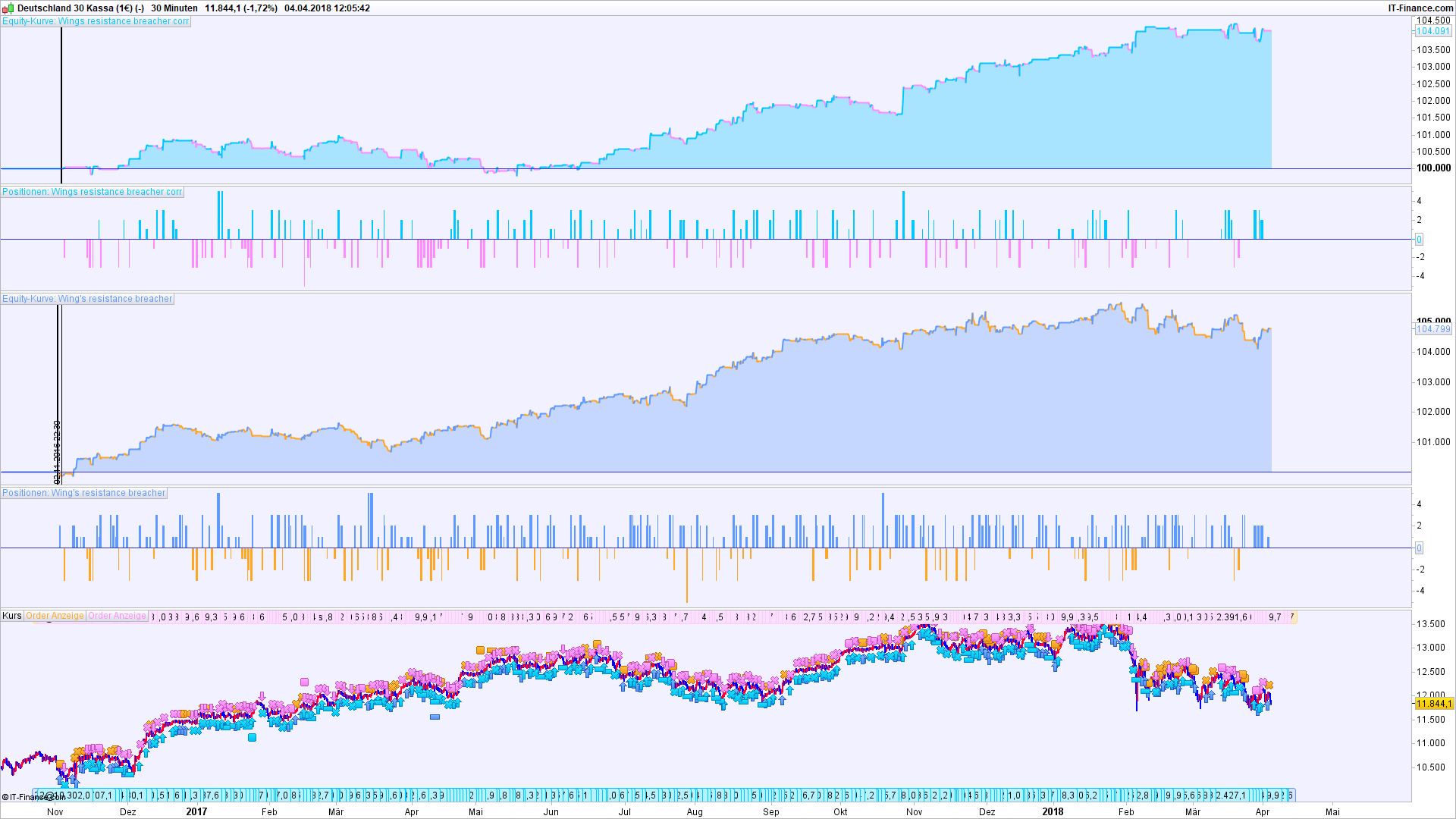

Sorry but i’ve, started the strategy on november 2017 and stopped in the end of march, the result are very bad in the last time, so i’ve got an idea this morning, and i am working on a filter, with huge improove of performance, i will post the result asap.

Wing’s resistance breacher has been quite good since November 2016. https://www.prorealcode.com/prorealtime-trading-strategies/wings-resistance-breacher-dax-30m/ Without position sizing (position size = 1, all the time) , it made about 2300 DAX points since then – not bad at all.

Sorry but i’ve, started the strategy on november 2017 and stopped in the end of march, the result are very bad in the last time, so i’ve got an idea this morning, and i am working on a filter, with huge improove of performance, i will post the result asap.

Result since November 1st, 2017 is + 32 Euro, to date.

When you develop a filter, please do not forget to do a walk forward analysis, at best starting in 2010.

I’ve optimised Wings Resistance breacher and set it going Live, but I’m not sure what’s the gig re posting optimsed versions in this Thread?

Nobody seems to want to use my database https://docs.google.com/spreadsheets/d/11zMhXG7oiSgUfMu2JSU1Un2Q0CbP8iWeAJg1HPaArD8/edit?usp=sharing and without a an easy means of identifying versions then this Thread may get filled up with loads of versions and the only way then would be to laboriously read through post after post etc to see what changes had been made? So I haven’t posted my optimised version here.

What you reckon …?

- Stick with the purist original code ONLY?

- Post optimised versions here, but all / any of us populate my database with v1.0, v1.1.

- Raise new Topics with optimised versions?

- Continue as we are with no definite rules?

- Alternative??

Cheers

GraHal

Stick with the purist original code ONLY? Post optimised versions here, but all / any of us populate my datab

i would use and have a look on it if you don’t mind, i’ve also optimized for 200k bar, the original is very bad on 200k

When you read my comments from 151 days ago in the original post

Wing’s Resistance Breacher (DAX-30m)

there is a logical mistake in the original system. It favors long over short positions and therefore works better in a bull market.

When you remove the error and set

if close<average[yy] or close<exponentialaverage[tt] then

MaBoty=0

MaBotzy=999999999

endif

in lines 125-128 (line numbers of the original post, not of the itf file), the system opens long positions more carefully and therefore works better in a downward trend as we have it now. Of course, this takes profits away of the previous upward trend.

Result since November 1st, 2017 is then + 1593 Euro.

See a comparison of both codes below (upper curve = corrected code). I hope my conclusions from 151 days ago were correct, I did not think about them once again now.

[attachment file=67120]