The “DAX 10s -vectoril v3p5 v2” is crashing for me when it takes a position, it just did. Does anyone else encounter the same problem ?

Mine says running and the last was position took was at 9:13 that exited at 9:59.

@Artemois,

mine is running, but it didn’t take a position. The last one exited at 10h18 (french time)

@paisantrader Thnx I see you left the stop-loss at 2%. That’s too much for a 10s timeframe I think.

Fortunately if it’s changed to 0.4 or 0.5% it has no or very minimal impact on results, that’s on the dow version.

I realize that I was too focused on the trailing stop and wasn’t 100% how it worked. Thought it set it already from the start and the regular SL was there just to set a default value. But after a test, I see a big difference. Thank you for pointing out our mistakes, much appreciated!

2% -> 0.4% doubled the profit.

@Paisantrader can you post your itf files? 🙂

@Paisantrader can you post your itf files? 🙂

What I posted above was just sll and sls. Changed it from 2 to 0.4.

I’m running 3 version on Dow today, since I’m quite sure that what worked yesterday, will not work today or at least far from yesterdays numbers.

- The one already posted here

- Optimized before opening today and 100k bars

- Optimized before opening today and 5k bars, roughly 22:00 – before opening

Just a little testing for my own sake 🙂

Paul

PaulParticipant

Master

Hi, so if there’s a stoploss of 0.4 or 0.5% why not use as backup an atr stoploss or/and profit target.

I prefer to leave the original setting for the % stoploss with set the set command intact

Here’s a quick code. I’ve doubt if it should close[0] or close[1].

// ATR Stops and targets

IF LONGONMARKET THEN

atrstop = positionprice - (10* AverageTrueRange[14](CLOSE)[0])

atrtarget = positionprice +(10* AverageTrueRange[14](CLOSE)[0])

Endif

if shortonmarket then

atrstop = positionprice + (10* AverageTrueRange[14](CLOSE)[0])

atrtarget = positionprice -(10* AverageTrueRange[14](CLOSE)[0])

endif

if longonmarket then

if high crosses over atrtarget then

sell at market

endif

if low crosses under atrstop then

sell at market

endif

graphonprice atrstop

graphonprice atrtarget

endif

if shortonmarket then

if low crosses under atrtarget then

exitshort at market

endif

if high crosses over atrstop then

exitshort at market

endif

graphonprice atrstop

graphonprice atrtarget

endif

Hi, so if there’s a stoploss of 0.4 or 0.5% why not use as backup an atr stoploss or/and profit target.

I prefer to leave the original setting for the % stoploss with set the set command intact

Here’s a quick code. I’ve doubt if it should close[0] or close[1].

Thank you, much appreciated. I see there’s similarities to the one in use right now . I’ll test them side by side to compare.

// trailing atr stop

once trailingstoptype1 = 1 // trailing stop - 0 off, 1 on

if trailingstoptype1 then

//========================

once tsatrdistlong = 2.3 //3 // ts atr distance

once tsatrdistshort = 2.3 //3 // ts atr distance

once tsincrements = 0.05 // set to 0 to ignore tsincrements

once tsminatrdist = 2

once tsatrperiod = 14 //14 // ts atr parameter

once tsminstop = 10 //10 // ts minimum stop distance

once ts1sensitivity = 2 // [0]close;[1]high/low;[2]low;high

//========================

if barindex=tradeindex then

trailingstoplong = tsatrdistlong

trailingstopshort = tsatrdistshort

else

if longonmarket then

if tsnewsl>0 then

if trailingstoplong>tsminatrdist then

if tsnewsl>tsnewsl[1] then

trailingstoplong=trailingstoplong

else

trailingstoplong=trailingstoplong-tsincrements

endif

else

trailingstoplong=tsminatrdist

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

if trailingstopshort>tsminatrdist then

if tsnewsl<tsnewsl[1] then

trailingstopshort=trailingstopshort

else

trailingstopshort=trailingstopshort-tsincrements

endif

else

trailingstopshort=tsminatrdist

endif

endif

endif

endif

tsatr=averagetruerange[tsatrperiod]((close/10)*pipsize)/1000

//tsatr=averagetruerange[tsatrperiod]((close/1)*pipsize) // (forex)

tgl=round(tsatr*trailingstoplong)

tgs=round(tsatr*trailingstopshort)

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

tsmaxprice=0

tsminprice=close

tsnewsl=0

endif

if ts1sensitivity=1 then

ts1sensitivitylong=high

ts1sensitivityshort=low

elsif ts1sensitivity=2 then

ts1sensitivitylong=low

ts1sensitivityshort=high

else

ts1sensitivitylong=close

ts1sensitivityshort=close

endif

if longonmarket then

tsmaxprice=max(tsmaxprice,ts1sensitivitylong)

if tsmaxprice-tradeprice(1)>=tgl*pointsize then

if tsmaxprice-tradeprice(1)>=tsminstop then

tsnewsl=tsmaxprice-tgl*pointsize

else

tsnewsl=tsmaxprice-tsminstop*pointsize

endif

endif

endif

if shortonmarket then

tsminprice=min(tsminprice,ts1sensitivityshort)

if tradeprice(1)-tsminprice>=tgs*pointsize then

if tradeprice(1)-tsminprice>=tsminstop then

tsnewsl=tsminprice+tgs*pointsize

else

tsnewsl=tsminprice+tsminstop*pointsize

endif

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if tsnewsl>0 then

sell at tsnewsl stop

endif

if tsnewsl>0 then

if low crosses under tsnewsl then

sell at market

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

exitshort at tsnewsl stop

endif

if tsnewsl>0 then

if high crosses over tsnewsl then

exitshort at market

endif

endif

endif

endif

endif

I haven’t put the ones in 10s in demo or live, please keep me updated 😉

I stopped the 10s strategies on wenesday. The algos take too many positions and i can’t understand some of them.

I prefer launch algos wich run on 5min or 3min timeframes.

Hey @Tanou I haven’t put any of the systems live though I have compiled the last 12 trading days backtest if it can help. Here’s the file

@BobOgden, that’s a fantastic job! 😃

However, this system doesn’t seems to perform well on 10s for now.. I optimised it for 3 minutes at the enhance.

on what schedule did you ran it as I see that you’ve wrote 15/15:30 to 22?

@Tanou it should be the same as the original code, only changed to fit EU time (well, at least I think, I’m not even sure it does fit EU time now).

I’ll try and update it in two week’s time to get a full month or so. As you said, it has performed pretty baldy lately, especially on US election day

The text box is just to remind me to check whether DJ opening hours wouldn’t be better than from 5:00 to 23:00

Positionsize is 0.2 btw

I’ve been running the 3min version, hopefully it does well 🙂

Has anyone tried using this as a mean reversing strategy?

PaulParticipant

Master

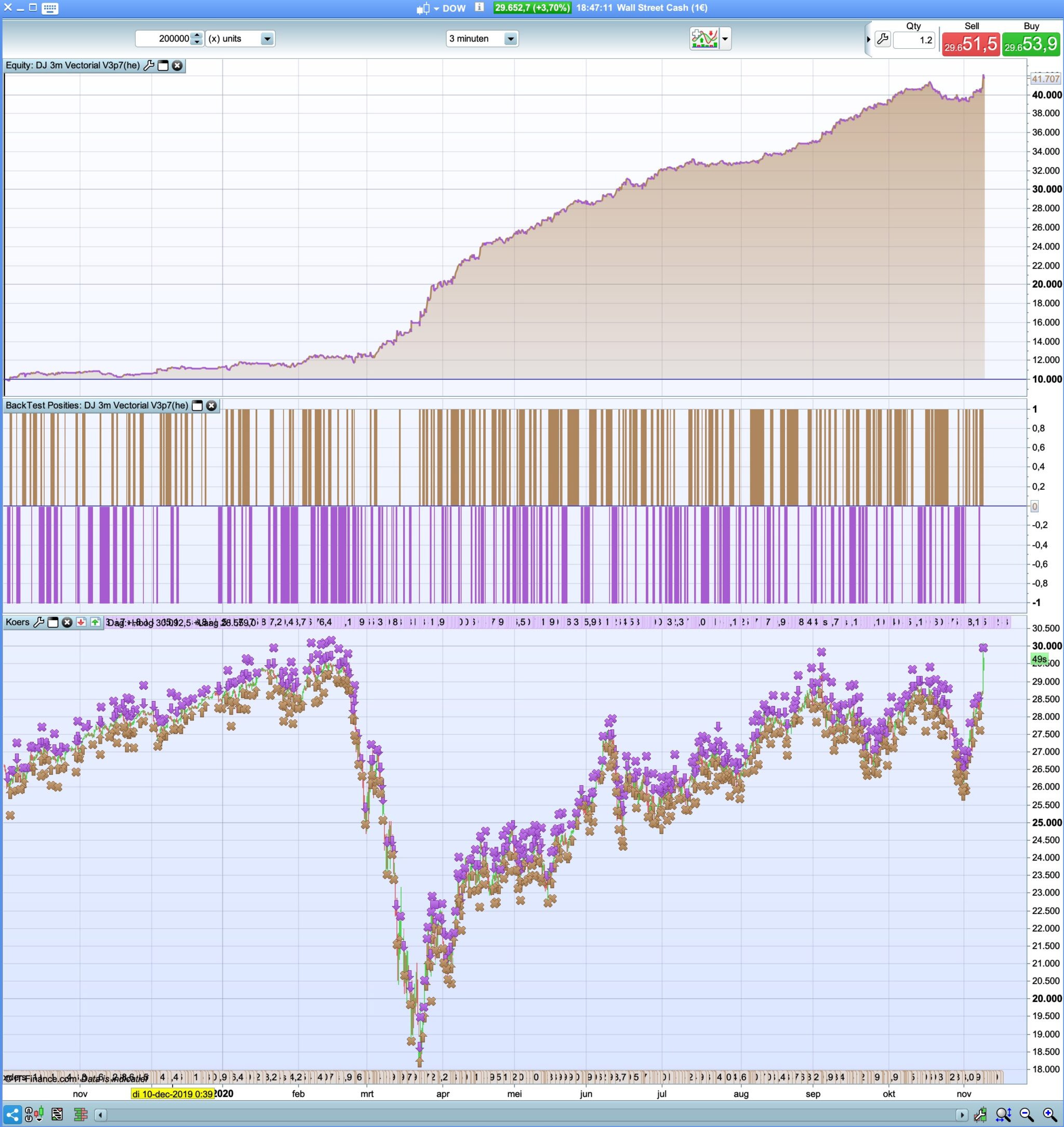

Here’s a version which uses the heuristics engine, but not aggressively.

The way I used the heuristics engine & modified it, while it works in the backtest, i’am not convinced about using it. The engine can easily be switched off.

I had it with he on/off running side by side for a short while and results were identical, but didn’t look into it too much.

Actually I had already deleted this version because it grew too big and curvefitted.

@Paul:

That’s amazing.

Appreciate the tremendous amount of effort you into it.